In this project we move from forecasting assets to learning a portfolio policy. The earlier ML work predicted future returns or regimes, then converted those forecasts into weights with hand-built rules. Here we let an agent choose the weights directly, observe what happens to the portfolio, and update the policy from the realized reward.

Main parts in this notebook:

build a portfolio RL environment from weekly cross-asset decisions, previous weights, costs, volatility, drawdown, and market states,

define a continuous action space that turns neural-network outputs into valid long-only portfolio weights,

design a reward based on differential Sharpe with penalties for turnover, drawdown, volatility, concentration, excess cash, and redundant equal-weight behavior,

teach the RL path from MDPs and Bellman equations to Q-learning, DQN, policy gradients, actor-critic, PPO, recurrent PPO, and SAC,

train PPO, recurrent PPO, and SAC policies and compare them against the rule-based and ML portfolio models from earlier projects,

repeat the workflow on sector ETFs through the library implementation.

The repeated material is intentionally kept short. Mean-variance and portfolio backtesting were already covered in Project 2, Black-Litterman and learned confidence in Project 6, robust/tail portfolio models in Project 10, macro financial conditions in Project 12, regime classification in Project 16, and neural forecasting plus Kelly sizing in Project 19. We use those pieces as inputs here. The new subject is reinforcement learning as sequential portfolio control.

For the RL theory, the main backbone follows the standard MDP/value-function/policy-gradient framing from Sutton and Barto’s reinforcement learning text, plus the specific modern algorithms behind DQN, PPO, GAE, and SAC: Sutton & Barto, DQN, GAE, PPO, and SAC. We don’t turn the notebook into a literature review, but those are the concepts the implementation is built on.

A good way to read this project is to treat it as the final step in the portfolio-learning chain. In the earlier ML notebooks, we mostly asked models to predict something: a regime label, a return rank, a volatility state, or a forward alpha. In this project, we ask a more difficult question: after seeing all those signals, what should the portfolio actually do now?

That change sounds small, but it changes the learning problem completely. A forecast model is usually trained with a fixed target. The target could be next-month return, next-month rank, or whether the next period is risk-on. The model predicts the target and we evaluate prediction error. A portfolio policy has a different job. It has to pick an action that changes wealth through time. The quality of that action depends on future return, turnover, drawdown, volatility, concentration, cash use, and the next opportunity set. This is why RL is a natural final project: it lets us write the portfolio decision as a repeated control problem instead of one isolated prediction problem.

We should still be careful with this. Finance is a difficult RL domain because the market doesn’t give us millions of independent training episodes. The agent sees one noisy historical path, and every apparent edge can be a sample artifact. So the goal here isn’t to claim that RL automatically beats everything. The goal is to build a serious, transparent RL allocation framework and understand exactly what the policies learn, what they fail to learn, and how they compare with the more interpretable rule-based models from the previous projects.

Because this is the final project, the markdown also has to do more teaching than a normal research note. The reader should understand the path from the simplest RL objects to the implemented models. So the explanations don’t jump straight from “agent” to PPO or SAC. They build the bridge: state, action, reward, MDP, value, Q-value, advantage, policy gradient, actor-critic, PPO, recurrent PPO, and SAC. The portfolio details are then layered on top of that RL course path.

This is also why the markdown spends less space on repeated data and baseline explanations. The repeated pieces are only there to make the RL setup grounded. The main intellectual work is understanding how a neural policy learns sequential allocation under realistic portfolio frictions.

So this markdown treats RL as a decision framework first and a neural-network technique second. That order is important for understanding the project. Clearly.

1) Reused Inputs and the Portfolio-Control Setup

We start by importing the project dependencies, setting the random seeds, choosing the compute device, and defining the cross-asset universe. This first cell is mostly setup, so the important part is the shape of the decision problem rather than the imports.

The tradable risky assets are:

Equities: SPY, QQQ, IWM, EFA, EEM

Real assets / inflation-sensitive assets: VNQ, DBC, GLD

Rates and credit: IEF, TLT, LQD, HYG

Cash-like defensive asset: SHY

The signal-only assets AGG and UUP still help describe the market state, but they aren’t part of the risky action vector. The agent receives features from these markets, then decides how much risk to take and how to distribute it across the portfolio.

The main data sources are repeated from earlier notebooks, so we only need the reproducibility links:

The first printed output reports the compute device. Here the run used cuda, so the neural-network training was done on GPU. That matters because PPO, recurrent PPO, and SAC all repeatedly collect rollouts and update neural networks. A CPU version would still work, but the training loop would be slower.

The portfolio universe also makes the RL task meaningful. If the universe only contained highly correlated equity ETFs, the action space would mostly be sector rotation. Here the agent can rotate between broad equity, growth, small caps, international equity, emerging markets, real estate, commodities, gold, duration, credit, high yield, and cash. That means one action can represent several economic choices at the same time:

risk exposure: high risky allocation versus more SHY,

growth/cyclical tilt: QQQ and SPY versus IWM, EEM, HYG, and DBC,

inflation hedge: GLD and DBC versus duration,

rate sensitivity: TLT and IEF versus SHY,

credit beta: HYG and LQD versus Treasury exposure,

international risk: EFA and EEM versus US assets.

The RL policy therefore isn’t just choosing tickers. It is choosing a macro allocation shape. This is why the state contains both asset-level signals and global context. A high forecast for HYG means something different when NFCI is loose, VIX is falling, breadth is strong, and SPY drawdown is shallow. The same HYG forecast is more dangerous when financial conditions are tightening and equity breadth is breaking.

The weekly decision frequency is also a design choice. Daily RL allocation would create too much noise and transaction cost. Monthly allocation may be too slow to react when the state changes sharply. Weekly decisions are a middle ground: the agent can adapt more often than the monthly optimizer, but the holding period is long enough that each action has a real portfolio consequence.

Show code

panels = load_yfinance_panel( data_path, fields=("close", "volume"), tickers=all_tickers, source="yfinance_export", start="2007-01-01",)close_all = panels["close"].sort_index().ffill(limit=3)volume_all = panels["volume"].sort_index().ffill(limit=3).reindex(close_all.index)first_valid = close_all[assets + [cash_ticker]].dropna(how="any").index.min()close = close_all.loc[first_valid:, [c for c in all_tickers if c in close_all.columns]].ffill(limit=3)volume = volume_all.reindex(index=close.index, columns=close.columns).ffill(limit=3)r_d = prices_to_returns_panel(close, kind="simple").replace([np.inf, -np.inf], np.nan).fillna(0.0)coverage = pd.DataFrame({"first_valid": close[assets + [cash_ticker]].apply(pd.Series.first_valid_index),"last_valid": close[assets + [cash_ticker]].apply(pd.Series.last_valid_index),"observations": close[assets + [cash_ticker]].notna().sum(),"coverage": close[assets + [cash_ticker]].notna().mean(),})display(coverage)print(close.index.min().date(), "to", close.index.max().date(), close.shape)

The loaded cross-asset panel runs from 2007-04-11 to 2026-06-17 with 4,828 daily observations after alignment. All 13 investable assets in the main environment have full coverage over this aligned period. That is important for RL because missing data would break the state-action-transition sequence. A supervised forecasting model can sometimes drop a row or impute a missing feature; an RL environment needs every step to have a valid next state, action, reward, and next-period return.

The asset summary is also useful. QQQ has the strongest annualized return in the full panel, around 17.9%, with annualized volatility around 22.3%. SPY is lower return but also slightly lower volatility. IWM, EEM, and VNQ carry larger volatility. GLD has a strong standalone return with lower volatility than most equity ETFs. DBC has the weakest return in this window, which reminds us that commodities can be useful in specific regimes without being attractive as a permanent high-weight allocation.

We rebalance the RL policy weekly, using Friday decisions. The output reports 950 weekly decision points, starting in April 2008 and ending in June 2026. Monthly optimizer dates are also created because the earlier portfolio models, like forecast-gated MaxSharpe and Kelly, use monthly timing. RL doesn’t have to follow the monthly optimizer schedule; it can learn at a more frequent weekly control horizon while still being compared against slower rule-based strategies.

1.1 Forecasts, regimes, and portfolio priors as inputs

The next long cell builds the forecasting and rule-based inputs that the RL state will later consume. We don’t need to re-teach the forecasting models from Project 19 or the regime classifier from Project 16. The important point is how we reuse them.

The project builds a forecast table with:

forward 21-day alpha targets, measured relative to the cross-sectional median,

volatility-scaled return labels, so assets with different risk levels can be compared more fairly,

tree-based forecasts from a RandomForest-style model,

TCN rank forecasts from the sequence model developed earlier,

confidence and rank features, so the RL policy can see not only the direction of a forecast but also how strong and stable it appears,

regime probabilities, FCI variables, VIX features, and cross-asset conditions.

The validation grid for lambda_alpha is used to choose how aggressively the forecast-gated optimizer should use the forecast signal. In the output, the best validation Sharpe is reached at lambda_alpha = 1.5, which is the most forecast-sensitive value in the grid. That doesn’t mean the forecast is always strong. It means that, over the validation period used in this notebook, the forecast-gated MaxSharpe model benefited from allowing a larger forecast tilt.

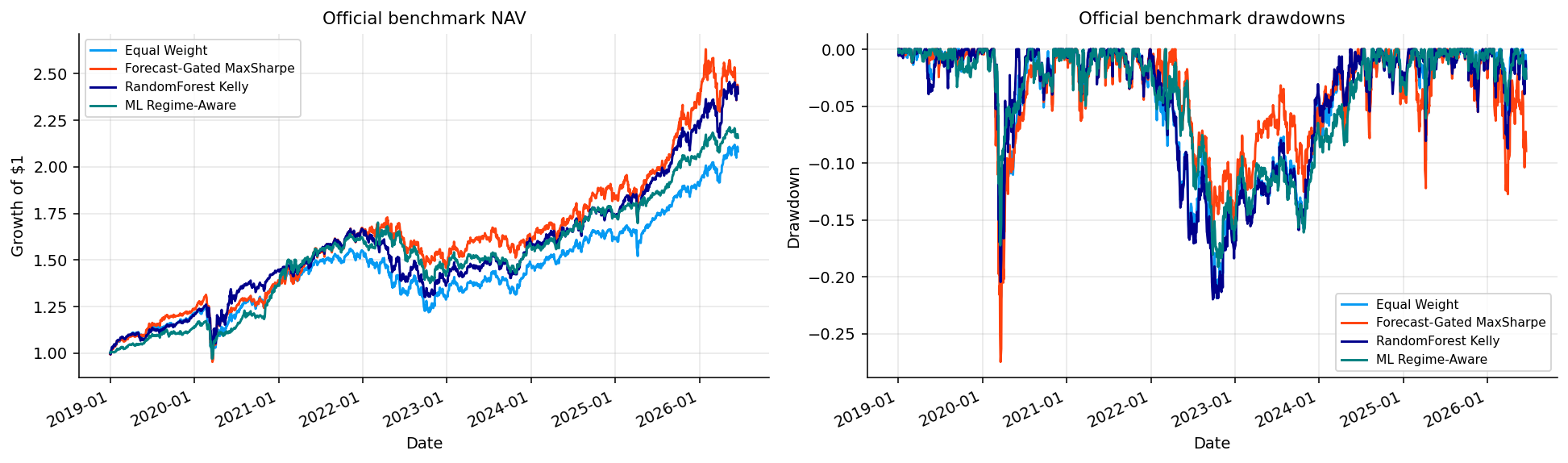

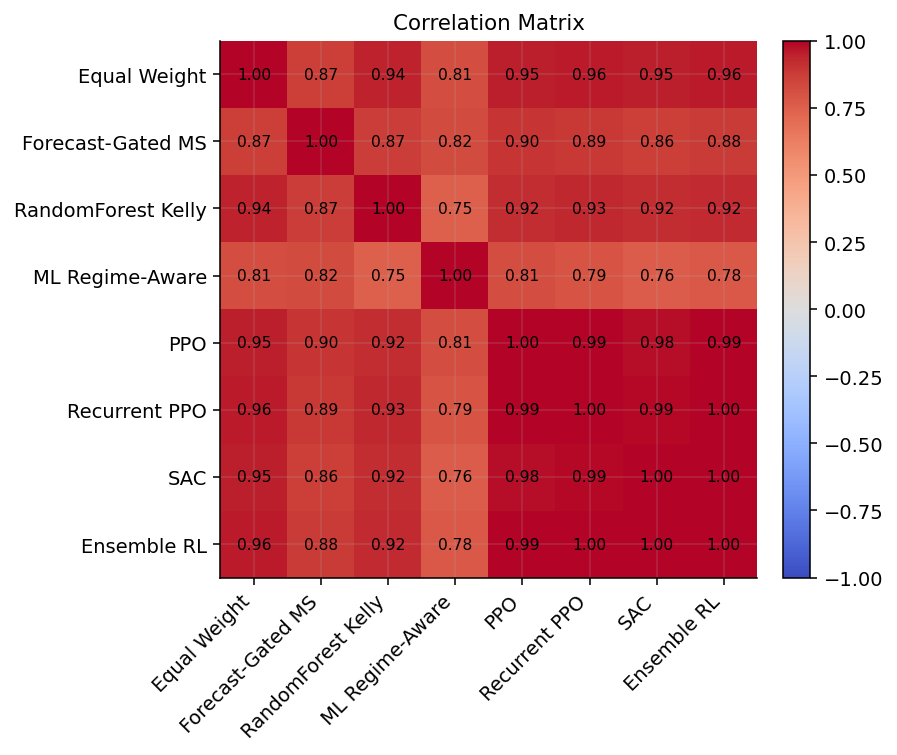

The displayed weight shapes show that we now have four baseline weight frames ready:

Equal Weight: 217 monthly rows and 12 risky assets,

Forecast-Gated MaxSharpe: 217 rows and 13 columns including SHY,

RandomForest Kelly: 217 rows and 13 columns including SHY,

ML Regime-Aware: 201 rows and 12 assets.

These aren’t the new RL models. They are the reference policies. We use them in two ways: first as benchmarks for performance, and second as state information so the RL policy can see what the earlier models would have done.

The forecast construction also gives us a useful example of how a supervised model becomes an RL feature. A forecast on its own is just a number:

Here \(\hat{\alpha}_{i,t}\) is the expected relative alpha for asset \(i\) over the next horizon. It tells us whether the model thinks the asset should beat the cross-sectional median. In a supervised notebook, we might rank assets by this value and buy the top names. In the RL notebook, we don’t force that rule. We pass the forecast into the state and let the policy learn how much to trust it.

This distinction matters. A forecast can be directionally useful but still too noisy to size directly. A high forecast for EEM might deserve a small tilt in a volatile environment and a larger tilt in a low-volatility, dollar-weak environment. The RL policy can learn these interactions because it sees the forecast together with volatility, regime, previous portfolio, and cost information.

The output showing tree features and neural-network features gives us the feature scale of the problem. We aren’t giving the RL agent raw prices only. We are giving it a research stack built from:

growth, inflation, financial conditions, stress state

Regime features

probability of risk-on, neutral, or defensive market states

Prior weight features

what earlier portfolio models would allocate

Portfolio memory

previous weights, turnover context, cash level

This is one of the best parts of the project. RL doesn’t replace the earlier work; it sits on top of it. The earlier models create structured information, and the policy learns how to turn that information into sequential allocation decisions.

1.2 Forecast features as policy context

The forecast features deserve one more clarification because they are easy to misuse in an RL setting. A forecast feature shouldn’t be treated as an order. If a model ranks QQQ highly, the policy doesn’t have to buy QQQ heavily. The policy sees that rank together with everything else. The forecast is one input to the decision, not the decision itself.

The first mapping predicts. The second mapping allocates. The second one has a harder job because it must consider cost, risk, and path-dependence. That is why a weaker raw forecast can still be useful if the policy learns when to trust it. It is also why a strong raw forecast can be harmful if the policy sizes it too aggressively.

The notebook gives the RL policy access to several prior portfolio models. This is a useful design because previous model outputs contain compressed information. A forecast-gated optimizer weight tells the agent how a disciplined optimizer reacts to the forecast. A Kelly weight tells the agent how growth-optimal sizing reacts. A regime-aware allocation tells the agent how the macro classifier changes exposure. The RL policy can learn to follow, fade, smooth, or ignore those priors.

This is closer to how a human portfolio team might work. A portfolio manager doesn’t look only at one forecast. They look at signals, risk reports, prior allocations, costs, and current exposures, then decide what change is actually worth making.

The benchmark NAV plot confirms that the rule-based baselines have very different behavior. Forecast-Gated MaxSharpe and RandomForest Kelly are more active and more concentrated than equal weight, so they have larger deviations through time. Equal weight is smoother but less informed. The regime-aware strategy tends to change more around stress and recovery periods because it is responding to market-state probabilities.

This matters for RL because we aren’t training the agent in an empty world. The agent receives signals from a full research stack: forecasts, regimes, macro conditions, VIX, and previous portfolio state. The hard part is deciding whether those signals should translate into more risky exposure, more cash, higher concentration, lower turnover, or a different cross-asset allocation.

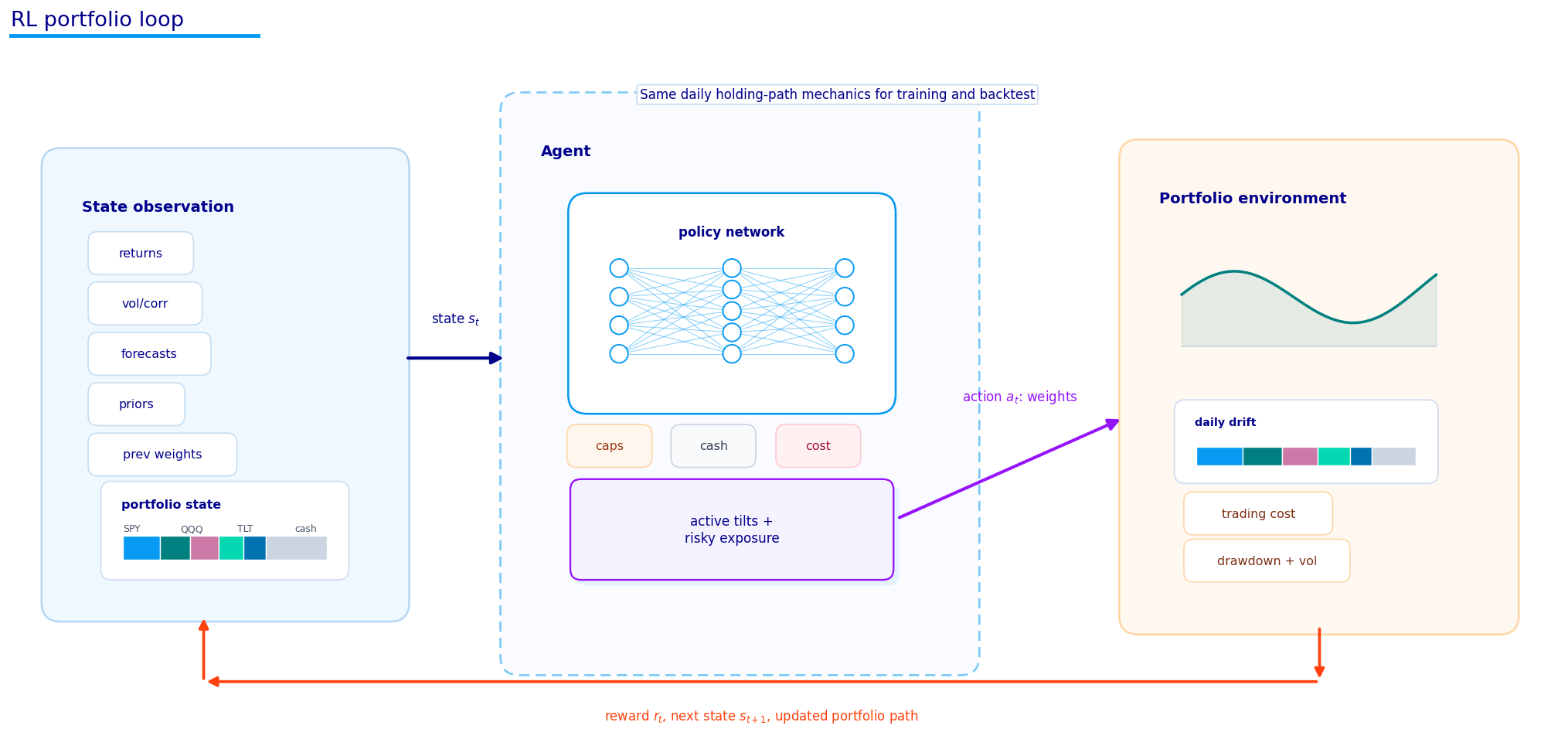

2) The Agent-Environment Loop

Reinforcement learning starts with an interaction loop. At each decision time, the agent observes a state, chooses an action, receives a reward, and moves to the next state.

\(S_t\) is the market and portfolio state at the weekly decision date,

\(A_t\) is the raw action produced by the policy network,

\(w_t\) is the valid portfolio weight vector after the raw action is mapped into constraints,

\(R_{t+1}\) is the reward earned over the next holding interval,

\(S_{t+1}\) is the updated market and portfolio state at the next decision date.

Show code

from quantfinlab.plotting.diagrams import agent_environment_loop_diagramfig, ax = agent_environment_loop_diagram()plt.show()

The first diagram shows this loop directly. The key financial difference from a normal supervised model is that the action changes the future portfolio path. A forecast model can be wrong and still leave the portfolio construction rule to handle the error. An RL agent owns the entire decision: if it chooses a high-turnover, high-concentration, high-risk allocation right before a drawdown, the reward should punish that decision.

A simple example makes the loop concrete. Suppose the state says credit is strong, equity breadth is high, volatility is low, and the previous portfolio is underweight risky assets. The policy may choose a high risky exposure and tilt toward SPY, QQQ, and HYG. The environment then applies that allocation over the next week, subtracts turnover costs, updates drawdown and realized volatility, and gives the agent a reward. If the decision raised return without creating too much risk, the reward improves. If it increased losses, turnover, drawdown, or concentration, the reward gets worse.

2.1 Supervised prediction and reinforcement learning in this project

Supervised learning and reinforcement learning look similar from far away because both train neural networks. The training signal is very different.

In supervised forecasting, we usually have pairs \((x_t, y_t)\) and minimize a prediction loss:

The model sees the input \(x_t\), predicts \(y_t\), and gets judged against the realized label. If the label is next-month return rank, the training target is fixed before the model acts. The model doesn’t change the market path by making a prediction.

In reinforcement learning, the training object is a policy:

\[

\pi_\theta(a_t \mid s_t)

\]

This means the model doesn’t only predict a label. It chooses an action \(a_t\) from state \(s_t\). In this notebook, the action becomes the portfolio weights. The policy is judged by the reward sequence generated after its actions:

The expectation is written under \(\pi_\theta\) because the policy itself influences the path of portfolio weights, costs, drawdowns, and rewards. In a market backtest, asset returns are historical and fixed, but the portfolio path isn’t fixed. The policy decides how much of each return stream it actually experiences.

This gives us the central RL difficulty: credit assignment. If a policy loses money in week 30, which earlier choices caused the problem? Was it the current allocation? A previous high-risk allocation that created drawdown pressure? A turnover decision that reduced wealth? A concentration choice that made the portfolio fragile? RL algorithms exist because this credit-assignment problem is hard.

In this notebook we use three modern continuous-control policy families:

PPO: a stable on-policy actor-critic method that updates cautiously.

Recurrent PPO: the same basic PPO idea, but with memory through an LSTM.

SAC: an off-policy actor-critic method that adds entropy to encourage exploration and robust stochastic policies.

The rest of the notebook builds the machinery needed to understand these three models from the ground up.

The important habit while reading the rest of the notebook is to always connect the algorithmic object back to portfolio behavior. A value function is about future reward. A policy is about allocation. Entropy is about exploration. A critic is about judging whether an allocation was better than expected. Keeping that mapping clear makes the RL math much easier to follow.

The agent-environment diagram should be read from left to right. The agent never sees the future return before it acts. It only sees the current state and the previous portfolio context. The environment receives the action, converts it into realized portfolio behavior, and returns the next reward.

This is also why RL can easily overfit in finance. The sample is one historical market path, not millions of independent games. If the agent memorizes that one path, it may look good during training and fail out of sample. That is why this project uses a clear train/validation/test split, heavy constraints, risk penalties, and comparisons against simple baselines.

2.2 Exploration, exploitation, and portfolio risk

The exploration/exploitation tradeoff is one of the first RL ideas that feels very different in finance. Exploration means trying actions that may not look best right now so the agent can learn whether they work. Exploitation means using the action that currently looks best.

In a game environment, exploration might mean trying a weird move to discover a hidden reward. In a live portfolio, exploration has real cost. Trying a high-HYG/high-IWM/high-EEM allocation in a stress environment can lose money. So we need exploration during training, but we also need strict constraints and risk-aware rewards so the agent doesn’t learn reckless behavior.

The policies in this notebook explore through stochastic actions. The actor outputs a Normal distribution over raw actions:

\[

a_t \sim \mathcal{N}(\mu_t, \sigma_t^2)

\]

The mean \(\mu_t\) is the policy’s preferred action. The standard deviation \(\sigma_t\) controls how much it explores around that action. A high \(\sigma_t\) means the policy samples many different allocations. A low \(\sigma_t\) means the policy becomes more deterministic.

PPO uses entropy regularization to avoid collapsing too early. SAC goes further and makes entropy part of the main objective. This is useful because portfolio reward is noisy. A policy may look good after one lucky training path, but a more stochastic policy can avoid becoming too committed to one historical pattern.

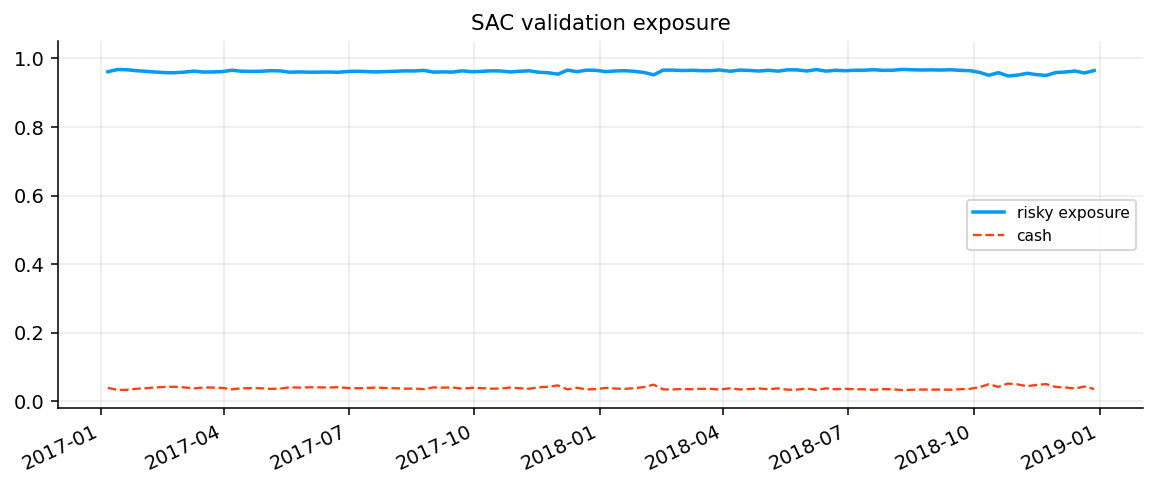

There is also a financial version of exploration that appears through the action constraints. Since the policy can never go below 55% risky exposure or above 35% in one risky asset, its exploration is bounded. The agent can explore different allocation shapes, but it can’t create absurd leverage or all-in positions. This is a strong design choice. It makes the training problem safer and the resulting policies more realistic.

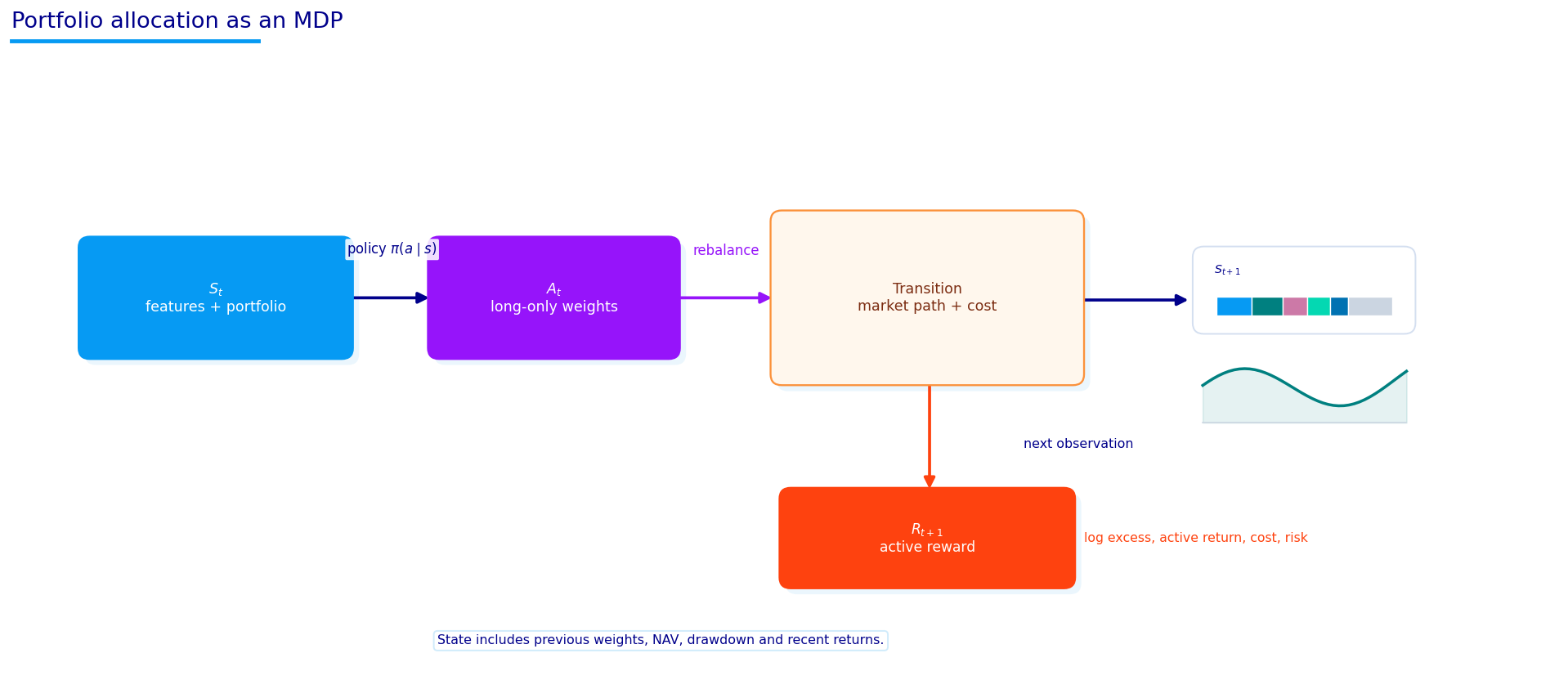

2.3 Markov decision process notation

A fully observed reinforcement-learning problem is usually written as a Markov decision process:

\(\mathcal{S}\) is the set of possible states. In our case, a state contains asset features, global market features, and portfolio features.

\(\mathcal{A}\) is the action space. Here the action becomes a portfolio allocation.

\(P(s' \mid s,a)\) is the transition rule. It describes the probability of moving to next state \(s'\) after taking action \(a\) in state \(s\).

\(r(s,a,s')\) is the reward function. Here it is built from portfolio return, differential Sharpe, costs, volatility, drawdown, and concentration penalties.

\(\gamma\) is the discount factor. It controls how much the agent cares about future rewards relative to immediate rewards.

The Markov part means that the current state is supposed to contain enough information to model the next step:

This formula says that once we know the current state and action, the older history shouldn’t add extra information. In markets this assumption is only approximate. If the state vector includes momentum, volatility, drawdown, forecast features, regimes, previous weights, and recent portfolio behavior, we are trying to compress the useful part of the history into \(S_t\).

A useful way to understand the MDP components in this project is to map each symbol to something in the portfolio code.

MDP object

Portfolio meaning

Concrete example in this notebook

\(S_t\)

observed state

asset tensor, global tensor, prior weights, previous weights

\(A_t\)

raw policy action

risky scores plus exposure score

\(w_t\)

valid portfolio weights

constrained long-only weights after action mapping

\(R_{t+1}\)

reward

DSR-based reward minus penalties

\(P\)

transition law

historical next state after the decision date

\(\gamma\)

future-reward weight

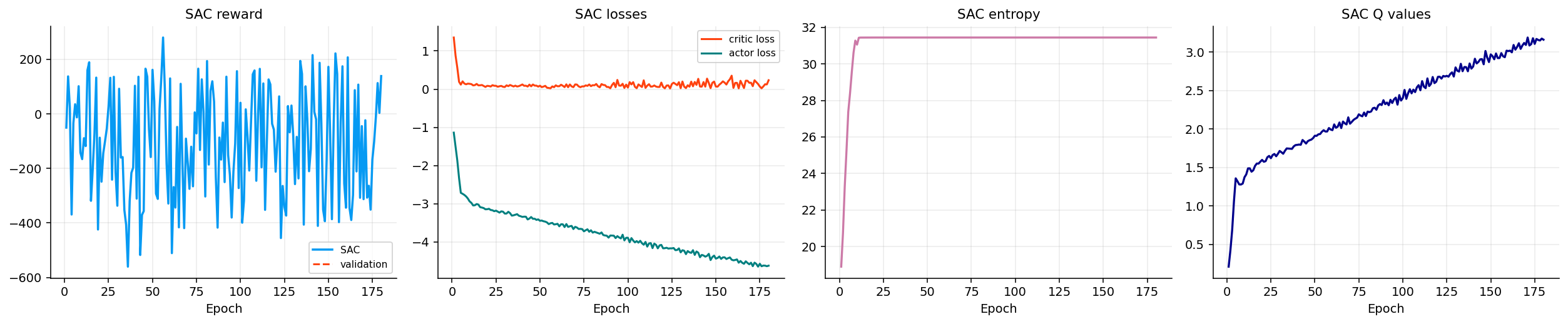

SAC uses \(\gamma=0.97\)

The transition law is the least controllable object. In a game simulator we can sample many possible futures. In finance, the notebook has one realized historical path. That is why the policy must be conservative. It can’t assume it has seen every possible crisis, every possible rate shock, or every possible liquidity event.

The discount factor \(\gamma\) deserves a clear interpretation. If \(\gamma=0\), the agent only cares about immediate reward. If \(\gamma\) is close to 1, it cares about longer-term consequences. With weekly decisions and \(\gamma=0.97\), a reward one week ahead receives full weight, a reward ten weeks ahead receives about:

\[

0.97^{10} \approx 0.74

\]

So the agent still cares about what happens several months later. This is important because drawdown and turnover are path-dependent. A policy that grabs a tiny short-term reward by taking unstable risk can damage future reward through drawdown penalties and a worse wealth path.

The Markov assumption is an approximation, but the state design tries to make it less unrealistic. We add rolling windows, forecast ranks, regime probabilities, previous weights, volatility, drawdown, and macro indicators so the current observation carries information about recent history. The recurrent policy later goes one step further by learning an internal memory state.

Show code

from quantfinlab.plotting.diagrams import mdp_diagramfig, ax = mdp_diagram()plt.show()

The MDP diagram shows how state, action, reward, and transition connect. In a textbook gridworld, the state might be the square where the agent stands, the action might be up/down/left/right, and the reward might be +1 for reaching the goal. In this project, the state is a high-dimensional financial vector, the action is a constrained weight vector, and the reward is a risk-adjusted portfolio outcome.

That difference changes the modeling challenge. The transition law \(P\) isn’t known. We don’t know the true probability distribution of future market states. So we use model-free RL: the agent learns from sampled historical transitions rather than estimating a full economic transition model.

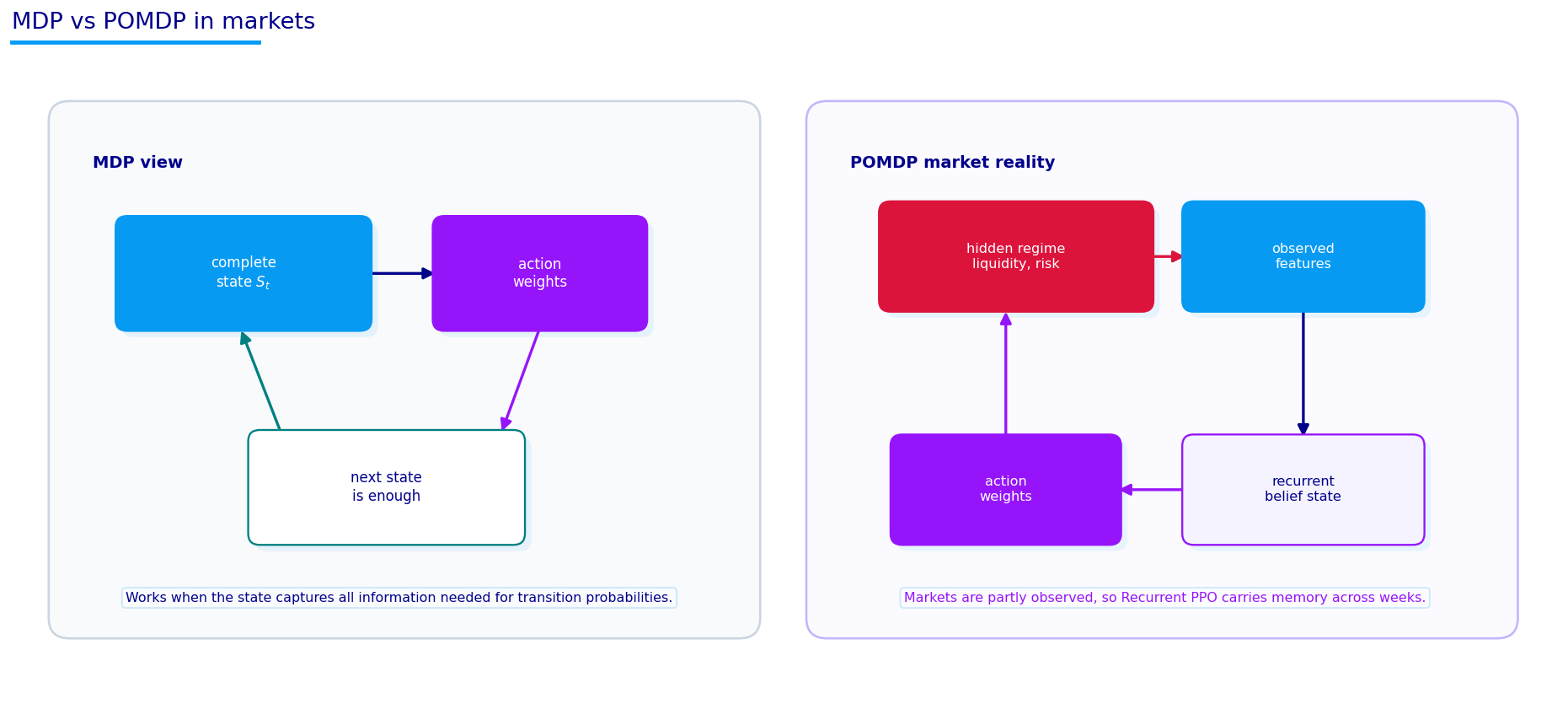

2.4 Partial observability in finance

The POMDP diagram is important because finance is rarely fully observable. We don’t see the true economic state. We observe noisy proxies:

prices and returns,

volatility and drawdown,

macro variables,

FCI and NFCI features,

VIX states,

regime probabilities,

forecast signals from the previous ML project,

previous portfolio weights and turnover.

The hidden state might be something like true growth, liquidity, inflation risk, policy reaction function, investor leverage, or market fragility. We don’t observe those directly. We observe indicators that may be correlated with them.

A partially observed problem can be written as:

\[

O_t \sim Z(\cdot \mid S_t)

\]

Here \(S_t\) is the latent state and \(O_t\) is the observation. The policy doesn’t receive \(S_t\) directly; it receives \(O_t\). In the code, the state vector is really an observation vector. We still call it state because it is the input to the policy, but conceptually it is a compressed observation of the market.

This is one reason recurrent policies can help. If the current observation doesn’t contain the full state, a recurrent network can use previous observations to build an internal memory:

\[

h_t = f_\theta(h_{t-1}, O_t)

\]

The hidden memory \(h_t\) can carry information about how the market got here, not only where it is now.

Partial observability is especially important for portfolio allocation because many of the variables that drive markets are latent. We never directly observe “risk appetite” or “liquidity preference” as clean numeric series. We observe proxies. A positive HYG-LQD signal might suggest credit risk appetite. A negative NFCI value might suggest loose financial conditions. A falling VIX might suggest less demand for crash insurance. None of these is perfect.

This means the policy shouldn’t treat one feature as truth. It has to combine imperfect signals. For example:

high equity breadth and falling VIX point toward risk-on,

rising dollar and weak EEM point against emerging markets,

positive commodity momentum and weak duration point toward an inflation-sensitive environment,

high realized correlation means diversification is weakening.

A non-recurrent policy receives this compressed state and acts immediately. A recurrent policy receives a sequence of states and can learn persistence. If financial conditions have been tightening for eight weeks, the recurrent state can carry that information even if the current observation alone looks neutral.

The hidden state in a recurrent policy is not an economic label. It is a learned vector. But if training works well, the vector can behave like a memory of recent market conditions:

\[

h_t = \text{LSTM}_\theta(h_{t-1}, o_t)

\]

Here \(o_t\) is the current observation, and \(h_t\) is the internal memory after processing it. The policy then chooses an action using \(h_t\) along with the current input. This is why recurrent PPO is a natural second model in the project.

Show code

from quantfinlab.plotting.diagrams import mdp_pomdp_diagramfig, ax = mdp_pomdp_diagram()plt.show()

3) Building the State Tensors

The RL state is split into three parts:

Asset state: a tensor with one row per asset and one column per asset-specific feature.

Global state: a vector of market-wide context variables.

Portfolio state: previous weights and recent portfolio behavior.

The asset-state tensor has shape:

\[

X^{asset}_t \in \mathbb{R}^{N \times F_a}

\]

where \(N\) is the number of risky assets and \(F_a\) is the number of asset features. In the main implementation, the output later shows:

This means we have 949 weekly decision points, 12 risky assets, and 50 asset-level features per asset. Every weekly decision is a small cross-sectional dataset: one row for SPY, one row for QQQ, one row for IWM, and so on.

The global-state tensor has shape:

\[

X^{global}_t \in \mathbb{R}^{F_g}

\]

and the output shows:

\[

X^{global} \in \mathbb{R}^{949 \times 31}

\]

So each decision also has 31 market-wide features. These are not asset-specific; they describe the whole environment.

The next-return matrix has shape:

\[

R^{next} \in \mathbb{R}^{949 \times 13}

\]

The 13 columns are the 12 risky assets plus SHY. This is what the environment uses to compute the realized portfolio return after the policy chooses weights.

The asset tensor structure is one of the cleanest ways to make the policy respect the cross-sectional nature of the problem. Instead of flattening everything into one long vector and asking the model to learn that SPY, QQQ, HYG, and GLD are different assets, we represent the input as a matrix:

\[

X^{asset}_t =

\begin{bmatrix}

\text{features of SPY at } t \\

\text{features of QQQ at } t \\

\vdots \\

\text{features of HYG at } t

\end{bmatrix}

\]

Each row is an asset. Each column is a feature type. This lets the network apply similar transformations across assets while still comparing assets to each other. That is useful for portfolio allocation because many decisions are relative: QQQ versus SPY, HYG versus LQD, EEM versus EFA, GLD versus DBC, and so on.

The global state has a different role:

\[

g_t \in \mathbb{R}^{F_g}

\]

It describes the market environment shared by all assets. A global feature like VIX, NFCI, breadth, or regime probability doesn’t belong to one asset row. It affects the interpretation of every asset feature. A strong QQQ forecast is more attractive in a loose, low-volatility environment than in a tightening, high-correlation environment.

The portfolio state adds information about the agent’s current position:

This matters because the same action has different cost depending on previous weights. If the policy already owns 25% SPY, staying at 25% has almost no turnover cost. Moving from 0% SPY to 25% SPY creates large turnover. RL has to learn this path dependence.

The feature output confirms that the raw asset feature block becomes complete on 2008-04-10. We start the RL decision sequence after that point. The raw feature table has 57,936 rows, which equals daily observations multiplied by assets, and 49 raw features before the later merged forecast features bring the asset-state dimension to 50.

The sample rows show a typical asset-state record for SPY: recent returns over 1, 5, 21, 63, and 126 days, skip-momentum, rolling volatility, group-relative features, trend consistency, residual momentum versus SPY, and TCN forecast features like tcn_alpha, tcn_rank, and tcn_confidence. These features are exactly the sort of variables that a portfolio allocator might use manually: recent strength, risk level, relative ranking, and forecast confidence.

The context-feature table at the end of the sample shows a recent risk-on environment: breadth around 0.75 to 0.83, SPY positive over 63 days, QQQ outperforming SPY, HYG slightly outperforming LQD, and NFCI negative, which means financial conditions are easier than average. The regime probabilities are available on some dates after the model updates. They don’t decide the RL action by themselves, but they are part of the state.

Show code

def align_weight_frame(weights, target_dates, columns, fallback_equal=False): dates = pd.DatetimeIndex(target_dates).sort_values().unique() W = pd.DataFrame(weights).copy()if W.empty: base = pd.DataFrame(0.0, index=dates, columns=columns)if fallback_equal: base[assets] =1.0/len(assets)return base W.index = pd.to_datetime(W.index) W = W.sort_index().reindex(columns=columns) W = W.reindex(W.index.union(dates)).sort_index().ffill().reindex(dates).fillna(0.0) zero = W.sum(axis=1).abs() <=1e-12ifbool(zero.any()) and fallback_equal: W.loc[zero, assets] =1.0/len(assets) row_sum = W.sum(axis=1).replace(0.0, np.nan)return W.div(row_sum, axis=0).fillna(0.0)def period_daily_windows(returns, decision_dates, columns): R = returns.reindex(columns=columns).fillna(0.0) idx = pd.DatetimeIndex(R.index) rows, windows = [], []for i, dt inenumerate(decision_dates): start = idx.searchsorted(pd.Timestamp(dt), side="right")if start >=len(idx):continue end = idx.searchsorted(pd.Timestamp(decision_dates[i +1]), side="right") if i +1<len(decision_dates) elsemin(start +5, len(idx))if end <= start:continue window = R.iloc[start:end].replace([np.inf, -np.inf], np.nan).fillna(0.0) rows.append(((1.0+ window).prod() -1.0).rename(pd.Timestamp(dt))) windows.append(window)return pd.DataFrame(rows).reindex(columns=columns).fillna(0.0), windowsstate_dates = pd.DatetimeIndex([d for d in decision_dates if pd.Timestamp(d) >= state_ready_start])state_columns = assets + [cash_ticker]returns_next, daily_windows = period_daily_windows(r_d, state_dates, state_columns)state_dates = returns_next.indexdaily_windows_np = [w.reindex(columns=state_columns).fillna(0.0).to_numpy(dtype=float) for w in daily_windows]

Show code

feature_cols = [ c for c in asset_x.columnsif c notin {"date", "asset"} and pd.api.types.is_numeric_dtype(asset_x[c])]asset_blocks = []asset_feature_names = []for col in feature_cols: piv = asset_x.pivot_table(index="date", columns="asset", values=col, aggfunc="last") piv = piv.reindex(piv.index.union(state_dates)).sort_index().ffill().reindex(state_dates) piv = piv.reindex(columns=assets) fill_by_asset = asset_feature_fill_by_asset[col].reindex(assets) if col in asset_feature_fill_by_asset.columns else pd.Series(np.nan, index=assets) fill_by_asset = fill_by_asset.fillna(float(asset_feature_fill_values.get(col, 0.0))) asset_blocks.append(piv.fillna(fill_by_asset).fillna(0.0)) asset_feature_names.append(col)asset_blocks.append(pd.DataFrame(0.0, index=state_dates, columns=assets))asset_feature_names.append("previous_weight")asset_state = np.stack([b.to_numpy(dtype=np.float32) for b in asset_blocks], axis=2)global_state_frame = global_x.reindex(global_x.index.union(state_dates)).sort_index().ffill().reindex(state_dates)global_state_frame = global_state_frame.apply(pd.to_numeric, errors="coerce").replace([np.inf, -np.inf], np.nan).fillna(0.0)global_state = global_state_frame.to_numpy(dtype=np.float32)shape_table = pd.DataFrame({"shape": [ asset_state.shape, global_state.shape, returns_next.shape, ]}, index=["asset_state", "global_state", "returns_next"])display(shape_table)

So at each of 949 weekly decision points, the policy sees 12 risky assets, 50 asset-level features, 31 global features, and next-period returns for 13 investable columns including SHY. These shapes are the practical version of the theoretical state/action/reward setup.

3.1 The leakage check

The state construction must avoid target leakage. We don’t want future labels like z_21 or y_alpha to sneak into the RL state. Those labels were used in Project 19 for forecasting, but here the RL policy should only see forecasts and features available at the decision time.

max absolute values that are finite and controlled after feature cleaning.

This is a small output, but it is one of the most important engineering checks. If leakage enters the state, the RL policy can appear to learn a brilliant allocation rule while really reading the answer key. The diagnostic says the state table is complete and clean for the main environment.

Leakage control is more important in this project than in a simple regression because RL can exploit tiny mistakes brutally. If a future-return label accidentally enters the state, the agent doesn’t need to understand finance; it can learn a direct shortcut. That would produce a beautiful backtest and a useless policy.

The leakage check verifies that the state doesn’t include target columns such as next-period realized return, future alpha, or future rank. The output shows missing share equal to zero and bounded feature magnitudes. This means two things:

The state tensors are complete, so the environment won’t be forced to handle missing rows during training.

The standardized features don’t contain extreme numerical explosions that would destabilize neural-network training.

The maximum absolute feature values are also useful. Asset features reach about 7.32 in standardized units, while global features reach about 3.29. That is large but still manageable. If the model saw values in the hundreds or thousands, gradient updates could become unstable, especially in PPO and SAC where policy log-probabilities and value losses interact.

For a finance ML notebook, this small diagnostic is one of the most important quality checks. It protects the credibility of everything that follows.

4) Continuous Actions as Portfolio Weights

In many RL examples the action space is discrete. An Atari agent chooses a joystick action. A gridworld agent chooses up, down, left, or right. A portfolio agent has a different problem: it needs to choose a vector of weights.

The first \(N\) elements are risky-asset logits. The last element controls total risky exposure. The code maps this raw action into valid weights through two transformations.

First, the exposure logit becomes a risky-exposure level using a sigmoid:

where \(E_{min}=0.55\) and \(E_{max}=1.00\). The sigmoid \(\sigma(e_t)\) maps any real number into \((0,1)\), so the model can output unconstrained neural-network values while the final exposure remains bounded. If \(e_t=0\), then \(\sigma(0)=0.5\) and the exposure becomes halfway between 55% and 100%:

\[

E_t = 0.55 + 0.45 \times 0.5 = 0.775

\]

Second, the risky logits become cross-sectional risky weights through a softmax:

This is a good action design because the neural network doesn’t have to learn the fully invested constraint from scratch. The transformation guarantees nonnegative weights and a controlled risky exposure. After that, the code caps each risky asset at 35% and redistributes any excess weight to assets with remaining room. Cash is the leftover:

So the final action is always a valid long-only portfolio.

4.1 From raw neural-network output to valid weights

The policy network doesn’t directly output final portfolio weights. It outputs an unconstrained action vector. That raw action must be translated into weights that obey the portfolio rules.

This creates a long-only allocation across risky assets. Every \(\tilde{w}_{i,t}\) is positive, and the risky weights sum to 1. The exposure score is passed through a sigmoid and scaled into a range:

where \(E_{min}=0.55\) and \(E_{max}=1.00\). This means the policy is always at least 55% invested in risky assets and can go up to 100%. SHY receives the leftover cash-like weight:

\[

w_{SHY,t} = 1 - E_t

\]

Then the risky weights become:

\[

w_{i,t} = E_t \tilde{w}_{i,t}

\]

A cap is applied so no single risky asset can dominate the portfolio:

\[

w_{i,t} \le 0.35

\]

If an asset hits the cap, the excess weight is redistributed across the uncapped assets. This keeps the policy from solving the problem by putting everything into one high-forecast asset.

A small example helps. If the network gives equal scores to all 12 risky assets and chooses the neutral exposure, the output shows about 6.46% in each risky asset and 22.5% in SHY. The policy starts from a diversified risky sleeve plus defensive cash-like ballast. Training then teaches it how to move away from that neutral shape.

This mapping is one of the most important implementation choices in the notebook. Instead of asking RL to learn portfolio constraints from penalties, we build the constraints into the action transformation. That makes training easier and keeps every sampled action investable.

The simplex constraint is strict. A policy can’t output weights that sum to 1.08 or -3% in an asset unless shorting/leverage is allowed. This project is long-only and fully invested, so every final action must land inside the simplex.

The raw action lives in unconstrained Euclidean space:

\[

a_t\in\mathbb{R}^{N+1}

\]

The action mapping is therefore a projection-like transformation from unconstrained scores to feasible portfolio weights. The softmax handles relative risky weights, the sigmoid handles total risky exposure, and the cap redistribution handles maximum position size.

This separation is cleaner than asking the neural network to learn feasibility by itself. If the policy output final weights directly, we would need penalties for invalid weights or a complicated constrained distribution. Here every sampled action is valid after transformation. That lets the RL algorithm focus on learning which valid portfolio shapes produce better reward.

The max-weight cap is also important for exploration. Without it, an early lucky sequence could teach the policy that one asset deserves extreme allocation. The cap forces the model to express conviction through a diversified sleeve. For example, if SAC likes risk, it can overweight SPY, IWM, QQQ, and HYG, but it can’t put 80% in one ticker.

This is a practical finance choice, not only a machine-learning choice. Real allocators usually care about concentration, liquidity, and mandate limits. Building those into the environment makes the learned policy more credible.

The neutral action output helps verify the transformation. When the raw action is all zeros, the model doesn’t choose an equal 1/13 allocation. It chooses about 6.46% in each risky asset and 22.50% in SHY.

That comes directly from the exposure formula. A zero exposure logit gives 77.5% risky exposure. Split equally over 12 risky assets, that is:

\[

\frac{0.775}{12} \approx 0.0646

\]

and the remaining 22.5% goes to cash-like SHY. This is a very useful sanity check because it tells us the default policy is neither all-cash nor fully risky. It begins from a balanced point and then learns to tilt.

5) Transaction Costs, Returns, and Portfolio Path Updates

The environment has to translate a weekly weight decision into a realized portfolio path. The realized return over the holding interval is computed from the asset returns and the chosen weights. If the action changes the portfolio from \(w_{t-1}\) to \(w_t\), the turnover is approximately:

The factor \(1/2\) avoids double-counting buys and sells. If we sell 10% of one asset and buy 10% of another, the absolute changes sum to 20%, but the traded portfolio notional is 10%.

With 10 bps cost, turnover of 0.50 costs 0.0005, or 5 basis points of portfolio value. The printed check returns exactly (0.01956, 0.5, 0.0005), meaning the test portfolio produced about 1.96% gross net step return with 50% turnover and 5 bps cost.

This is important because RL can otherwise learn unrealistic churning. A policy that changes weights aggressively every week may look good before costs and much weaker after costs. The environment makes turnover part of both the realized return and the reward penalty.

The transaction-cost formula is simple but important:

Here \(w^{pre}_{i,t}\) is the portfolio weight just before rebalancing, after market moves have changed the previous weights. The factor \(1/2\) appears because buying one asset and selling another creates two absolute weight changes for one dollar of portfolio rotation. If we sell 10% of SPY and buy 10% of GLD, the absolute changes sum to 20%, but the actual portfolio turnover is 10%.

With 10 bps cost, a turnover of 0.50 costs 0.0005, or 5 basis points of portfolio value. The sanity output (0.01956, 0.5, 0.0005) confirms exactly this logic: the example action produces a portfolio path return around 1.96%, turnover of 50%, and cost of 0.05%.

This cost term is a major reason RL policies shouldn’t chase every small forecast wiggle. A forecast must be strong enough to overcome the cost of changing weights. If the policy learns to trade too much, the reward should punish it through the cost penalty and through lower net portfolio returns.

6) Reward Design with Differential Sharpe

Reward design is where portfolio RL becomes finance-specific. If we reward only next-period return, the agent can learn to maximize upside by taking too much risk. If we reward only low volatility, it may hide in cash. The reward has to push the agent toward a usable investment policy.

The primary reward in this project is based on the differential Sharpe ratio (DSR). The idea is to approximate how a new return observation changes the running Sharpe ratio. We maintain exponentially updated moments:

\[

A_t = A_{t-1} + \eta(r_t - A_{t-1})

\]

\[

B_t = B_{t-1} + \eta(r_t^2 - B_{t-1})

\]

Here \(A_t\) is a running mean estimate, \(B_t\) is a running second-moment estimate, and \(\eta\) controls how quickly the estimates update. The variance estimate is:

\[

\sigma_t^2 \approx B_t - A_t^2

\]

A normal Sharpe ratio is roughly:

\[

SR_t = \frac{A_t}{\sqrt{B_t - A_t^2}}

\]

The differential Sharpe asks how the current return changes this running ratio. The code computes:

The numerator has two parts. The first part rewards returns above the current average. The second part penalizes returns that increase the second moment too much. So a positive return with modest volatility can have a positive DSR, while a large noisy return can be less attractive than its raw return suggests.

The reward doesn’t stop there. The full reward is:

Each penalty targets a specific portfolio failure mode:

\(P^{dd}_t\) penalizes drawdowns below the -12% floor,

\(P^{vol}_t\) penalizes realized volatility above the 18% target,

\(P^{cost}_t\) penalizes turnover cost,

\(P^{conc}_t\) penalizes excessive concentration using HHI,

\(P^{cash}_t\) penalizes cash above 20%,

\(P^{corr}_t\) penalizes policies that are too correlated with equal weight.

This reward is deliberately opinionated. We are not asking the agent to maximize raw wealth at all costs. We are training it to be a cost-aware, drawdown-aware, volatility-aware portfolio allocator.

6.1 Differential Sharpe from running moments

The reward is based on differential Sharpe ratio (DSR), which is useful when an agent receives rewards step by step. A normal Sharpe ratio is computed after a full return series:

\[

SR = \frac{\bar{r}}{\sqrt{\overline{r^2} - \bar{r}^2}}

\]

This is not directly convenient as a per-step reward because the Sharpe ratio depends on the whole history. DSR turns the idea into an incremental signal. We maintain running estimates of the first and second moments:

\[

A_t = A_{t-1} + \eta(r_t - A_{t-1})

\]

\[

B_t = B_{t-1} + \eta(r_t^2 - B_{t-1})

\]

Here:

\(A_t\) is the running mean return estimate,

\(B_t\) is the running second-moment estimate,

\(\eta\) is the update speed,

\(B_t - A_t^2\) is the running variance estimate.

The DSR approximation used in the environment measures how the new return changes the Sharpe estimate:

This formula looks dense, so let’s unpack it. The term \(r_t-A_{t-1}\) asks whether today’s return is above the current running mean. That improves the numerator. The term \(r_t^2-B_{t-1}\) asks whether today’s squared return is above the current running second moment. That increases estimated volatility, which can hurt Sharpe. So DSR rewards returns that improve mean more than they increase variance.

This is a good fit for allocation. A high-return week with huge volatility doesn’t automatically receive a huge reward. A moderate positive return with controlled volatility can be more valuable. That matches the financial objective of building a stable risk-adjusted portfolio rather than maximizing raw return.

6.2 Reward components as portfolio behavior constraints

Each penalty is connected to a real portfolio failure mode:

\(C_t\) penalizes turnover cost.

\(V_t\) penalizes realized volatility above the target.

\(D_t\) penalizes drawdown beyond the floor.

\(H_t\) penalizes concentration through HHI.

\(K_t\) penalizes excessive cash above the cap.

\(M_t\) penalizes portfolios that remain too close to equal-weight behavior when correlation is high.

The concentration penalty uses the Herfindahl-Hirschman index:

\[

HHI_t = \sum_i w_{i,t}^2

\]

If the portfolio is equally spread across 12 risky assets, HHI is low. If the portfolio puts 35% into one asset and large weights into only a few others, HHI rises. The effective number of assets is:

\[

N_{eff,t} = \frac{1}{HHI_t}

\]

This is easier to interpret. An HHI of 0.10 means the portfolio behaves roughly like 10 equally weighted assets. An HHI of 0.25 means it behaves like only 4 equally weighted assets.

The reward-settings table shows the exact values used in the environment. The daily risk-free rate is about 0.000156, corresponding to a 4% annual risk-free assumption. The reward mode is DSR, scaled by 4.0. The drawdown floor is -12%, target volatility is 18%, maximum risky exposure is 100%, minimum risky exposure is 55%, and maximum single risky asset weight is 35%.

The cash penalty matters because the action map allows cash through SHY. Without a cash penalty, a risk-aware reward might encourage the agent to hold too much SHY and avoid learning meaningful allocation. With a cash cap of 20% and a penalty above that, the policy can still de-risk, but it has to pay a reward cost for excessive defensiveness.

The environment sanity check is excellent: the path total return from the environment and the daily backtest total return both equal 6.2521, with an absolute gap of 0.0000. That tells us the RL environment is aligned with the later backtest engine. If this check failed, the agent could train on one reward accounting system and be evaluated on another, which would make the results unreliable.

The reward table for the baselines is very helpful. Equal weight has tiny turnover and no concentration penalty, but it suffers from larger drawdown and volatility penalties. Forecast-Gated MaxSharpe has lower drawdown penalty but more turnover and some concentration. RandomForest Kelly has a large cash penalty, which means it often becomes too defensive relative to the reward design. ML Regime-Aware has strong DSR but still takes drawdown penalty.

This reward decomposition is the teacher signal for the RL models. The agent learns from these tradeoffs. It isn’t being told “buy SPY” or “avoid TLT.” It is being told what kind of portfolio path is valuable.

6.3 Reward shaping without hiding the real objective

Reward shaping can make RL easier to train, but it can also create strange behavior if the shaped reward is misaligned with portfolio goals. The reward here tries to keep the main objective close to risk-adjusted wealth growth while adding penalties that represent real implementation constraints.

A pure return reward would be:

\[

R_t = r^{portfolio}_t

\]

That would push the agent toward high-risk assets because the sample contains long bull-market periods. A pure Sharpe-style reward is better, but it can still ignore costs, concentration, and drawdown path. The DSR reward plus penalties gives a more complete training signal.

Think of each penalty as a guardrail:

Guardrail

What it prevents

Cost penalty

constant reshuffling for tiny forecast changes

Volatility penalty

high-return but unstable portfolios

Drawdown penalty

accepting deep losses for short-term reward

Concentration penalty

hiding all risk in one or two assets

Cash penalty

solving the problem by staying defensive forever

Decorrelation penalty

pretending to be active while staying close to equal-weight under high correlation

The cash penalty is easy to misunderstand, so it’s worth being clear. SHY is a valid defensive asset, and the agent is allowed to hold it. But if the reward didn’t penalize excess cash at all, a defensive policy could avoid volatility and drawdown by hiding in SHY too often. That might produce stable rewards but wouldn’t be a useful allocation model. The cash penalty says: use cash when it helps, but don’t let it become the default answer.

The decorrelation penalty also has a specific purpose. If the policy behaves almost exactly like equal weight while paying turnover costs, it isn’t adding value. During high-correlation periods, many assets move together, so diversification can be weaker than the number of tickers suggests. The decorrelation term encourages the policy to make meaningful allocation choices instead of producing a noisy version of equal weight.

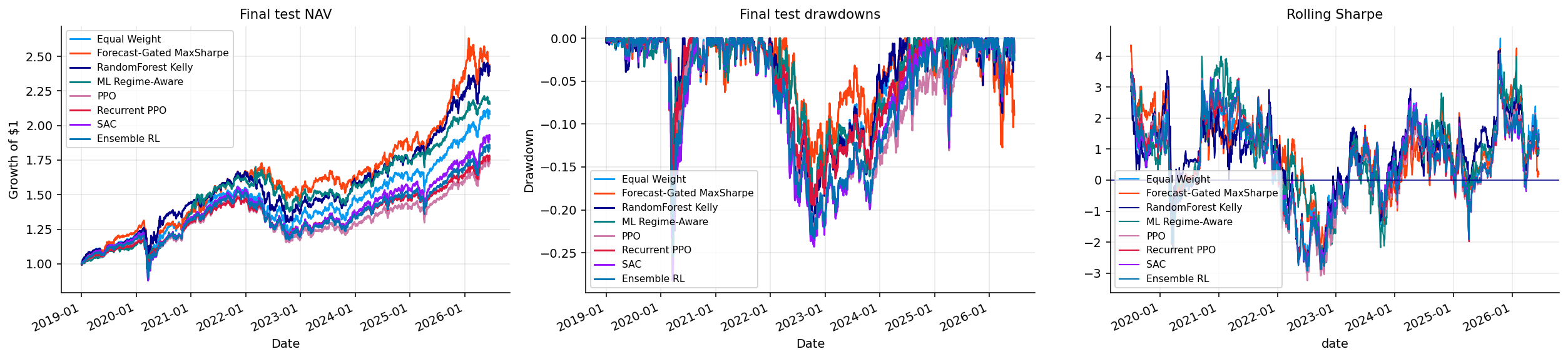

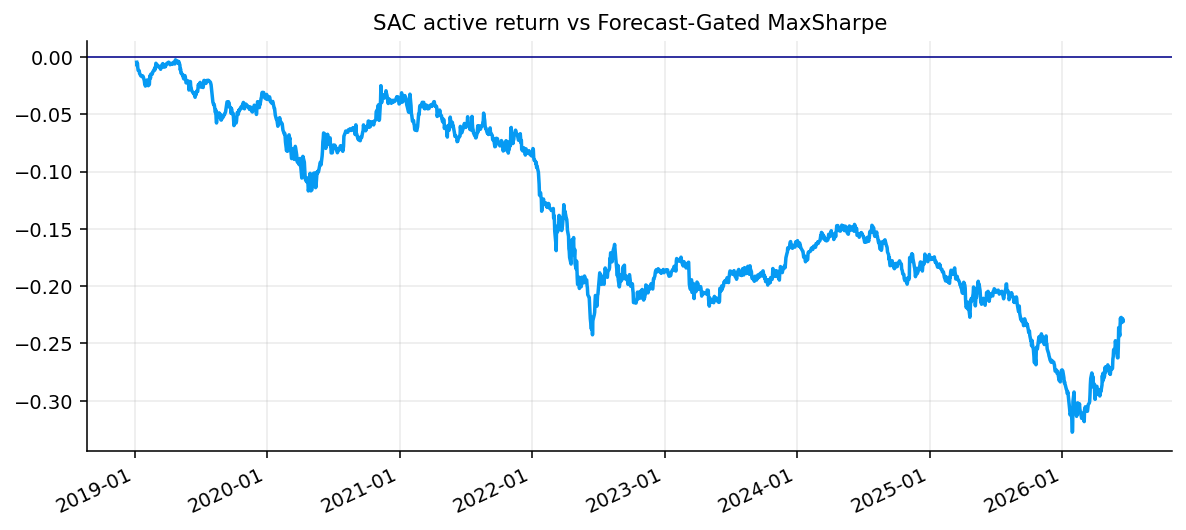

The reward design doesn’t guarantee success. It encodes what we care about. If the reward is too strict, the policy becomes too defensive. If it is too loose, the policy becomes too aggressive. The later results show this tension clearly: recurrent PPO is defensive, SAC is aggressive, and the best rule-based models still win on out-of-sample risk-adjusted performance.

6.4 Reward scale and learning stability

The scale of the reward matters because policy-gradient updates are sensitive to advantage magnitude. If rewards are extremely small, the policy barely receives a learning signal. If rewards are extremely large or unstable, the gradients become noisy and the policy may chase outliers.

This is why the DSR term is multiplied by 4. The raw DSR value is a small incremental statistic, so scaling it makes the reward visible to the optimizer. The penalties are then calibrated to live on a comparable scale. This doesn’t change the economic direction of the reward; it changes how strongly the agent feels that direction during training.

Return quality comes from DSR. Implementation damage comes from costs, drawdown, volatility, concentration, cash, and correlation penalties. If the implementation penalties dominate too much, the agent becomes defensive and static. If they are too weak, the agent becomes aggressive and unstable. The reward settings table is therefore not just a configuration table. It is the investor preference encoded into the RL environment.

The baseline reward decomposition is useful because it tells us whether the reward is sane before training. Equal weight receives almost no turnover or concentration penalty but suffers drawdown and volatility penalties. Forecast-Gated MaxSharpe pays more turnover but controls drawdown better. RandomForest Kelly gets punished for cash usage. These patterns make sense, so the reward is at least directionally aligned with real portfolio behavior.

The baseline reward decomposition is useful before any neural policy appears.

Equal weight has reward close to zero. It has very low turnover and no cash penalty, but it receives larger volatility and drawdown penalties. Forecast-Gated MaxSharpe has lower drawdown and volatility penalties, but higher turnover. RandomForest Kelly has a strong primary reward but pays a large cash penalty because it spends too much time in the defensive asset. ML Regime-Aware has a good primary reward but also drawdown and volatility penalties.

This table shows the reward is not just ranking strategies by CAGR. It is judging behavior. A strategy can earn high returns and still receive a weak reward if it relies on cash too much, trades too aggressively, or creates drawdown risk. That is exactly the kind of reward shaping we need before training PPO or SAC.

This split is stricter than random cross-validation. RL training has to respect time ordering. The policy learns on earlier market environments, gets selected on the validation period, and is evaluated on the later test period. The sample is still small for deep RL. A few hundred weekly steps is tiny compared with robotics or game environments. This is one of the biggest practical limitations of financial RL, and it is the reason the notebook uses constraints, priors, and compact policies instead of an unconstrained huge agent.

7) Value Functions, Bellman Equations, and Q-Learning

Before policy gradients, PPO, and SAC, we need the value-function foundation. The return from time \(t\) is the discounted sum of future rewards:

The discount factor \(\gamma \in [0,1]\) controls the future horizon. If \(\gamma\) is close to 1, the agent cares about long-term reward. If it is small, the agent becomes short-term. In this notebook, SAC uses \(\gamma=0.97\), so rewards several weeks ahead still matter.

A policy \(\pi\) maps states to actions. If the policy is stochastic, \(\pi(a\mid s)\) is the probability density of choosing action \(a\) in state \(s\). The value function is:

\[

V^\pi(s) = \mathbb{E}_\pi[G_t \mid S_t=s]

\]

This means: if we start in state \(s\) and follow policy \(\pi\), what is the expected total future reward? The action-value function is:

This means: if we start in state \(s\), take action \(a\) now, and then follow policy \(\pi\), what is the expected total future reward?

The difference between them gives the advantage:

\[

A^\pi(s,a) = Q^\pi(s,a) - V^\pi(s)

\]

The advantage tells us whether action \(a\) was better or worse than the policy’s typical action in state \(s\). In portfolio terms, if the current policy usually holds 70% risky exposure in a risk-on state, and one sampled action increases exposure to 90%, the advantage measures whether that more aggressive decision improved future reward relative to the baseline behavior.

7.1 Return, value, and the meaning of delayed reward

The return in RL is the discounted sum of future rewards:

Each term is a future reward. The discount factor \(\gamma\) controls how quickly those future rewards fade. In this project, rewards are weekly, so \(\gamma=0.97\) still gives meaningful weight to the next several months.

The state-value function is the expected return from a state under policy \(\pi\):

\[

V^\pi(s) = E_\pi[G_t \mid S_t=s]

\]

This is the value of being in state \(s\) if we keep following policy \(\pi\). In portfolio language, a state with strong breadth, low volatility, loose financial conditions, and positive forecasts should generally have higher value than a state with high volatility, negative breadth, and rising drawdown risk, but the value also depends on the policy’s ability to act.

The action-value function is:

\[

Q^\pi(s,a) = E_\pi[G_t \mid S_t=s, A_t=a]

\]

This is the value of taking action \(a\) now and then following policy \(\pi\) afterward. For portfolio allocation, \(Q(s,a)\) answers: if we choose these weights today, and then continue with our policy, what future reward should we expect?

The advantage function compares an action to the average action from the same state:

\[

A^\pi(s,a) = Q^\pi(s,a) - V^\pi(s)

\]

If \(A^\pi(s,a)>0\), the action was better than the policy’s typical action in that state. If it is negative, the action was worse. Advantage is the object PPO uses to decide which sampled actions should become more likely and which should become less likely.

A portfolio example makes this clearer. Suppose the state is a high-breadth, low-volatility, positive-forecast environment. A high-risky-exposure action may have positive advantage if it earns return without large penalties. In a high-volatility, high-drawdown state, the same high-exposure action may have negative advantage. The action isn’t good or bad by itself; it is judged relative to the state.

7.2 Monte Carlo targets and temporal-difference targets

There are two broad ways to estimate value. A Monte Carlo target waits until the end of a trajectory and uses realized future rewards:

\[

\hat{V}^{MC}(s_t)=G_t

\]

This is unbiased if the trajectory is sampled from the policy, but it can be very noisy. In finance, one realized path can contain unusual crises, rebounds, and rate shocks. A Monte Carlo return from one path may say more about that specific period than about the true value of the state.

A temporal-difference target bootstraps from the critic:

This is lower variance, but it depends on the critic being accurate. If the critic is wrong, the target is biased.

GAE blends these ideas. It doesn’t rely only on one-step TD, and it doesn’t wait for a full Monte Carlo return. It sums a decaying sequence of TD errors. This is a practical compromise, which is why PPO implementations often use it.

For portfolio RL, this compromise is valuable because rewards are noisy and path-dependent. A weekly return may be positive because the whole market went up, not because the action was smart. A drawdown penalty may appear several weeks after the risky allocation that caused the vulnerability. Multi-step advantage estimation helps the algorithm connect these delayed effects without relying entirely on long-horizon returns.

7.3 Discrete actions and continuous actions

Q-learning and DQN become easier when the action set is finite. For example, a discrete allocation agent might choose from:

Then the model only needs to learn the value of each action in each state. That can work, but it restricts the portfolio. We would have to predefine all possible allocation templates.

This notebook uses continuous control. The action lives in a real-valued space:

\[

a_t\in\mathbb{R}^{N+1}

\]

The model can choose smooth changes in exposure and relative weights. This is more flexible and closer to real portfolio management, but it makes learning harder. The agent has to learn both direction and sizing. Policy-gradient and actor-critic methods are designed for this kind of continuous decision.

The key transition in the RL course flow is therefore:

Bellman equations explain what optimal sequential value means.

Q-learning shows how value can be learned from temporal differences.

DQN shows how neural networks approximate value functions.

Policy gradients show how to optimize continuous stochastic policies directly.

Actor-critic combines policy learning with value estimation.

PPO and SAC are modern, stable versions of actor-critic learning.

7.4 The full model bridge from DQN to modern actor-critic

It helps to see the algorithm family as one continuous path instead of disconnected model names.

Step 1: value learning. We start with \(V(s)\) and \(Q(s,a)\). These functions answer how good a state or state-action pair is. The learning signal is Bellman consistency: today’s value should match today’s reward plus discounted next value.

Step 2: Q-learning. If actions are discrete, we can learn \(Q(s,a)\) and choose the action with the highest value:

\[

a^*(s)=\arg\max_a Q(s,a)

\]

This is intuitive but works poorly when the action is a high-dimensional continuous portfolio vector.

Step 3: DQN. We replace the Q-table with a neural network. The model can generalize across states, so it can handle complex observations. But it still usually assumes a discrete action set. For portfolio allocation, we would need to discretize weights into templates, and that would remove much of the flexibility.

Step 4: policy gradients. Instead of scoring every action, we directly learn a policy distribution. This fits continuous control:

Now the model can sample any raw action vector and map it to a valid portfolio.

Step 5: actor-critic. Policy gradients can be noisy, so we add a critic. The critic estimates value and produces advantages. This makes learning more stable.

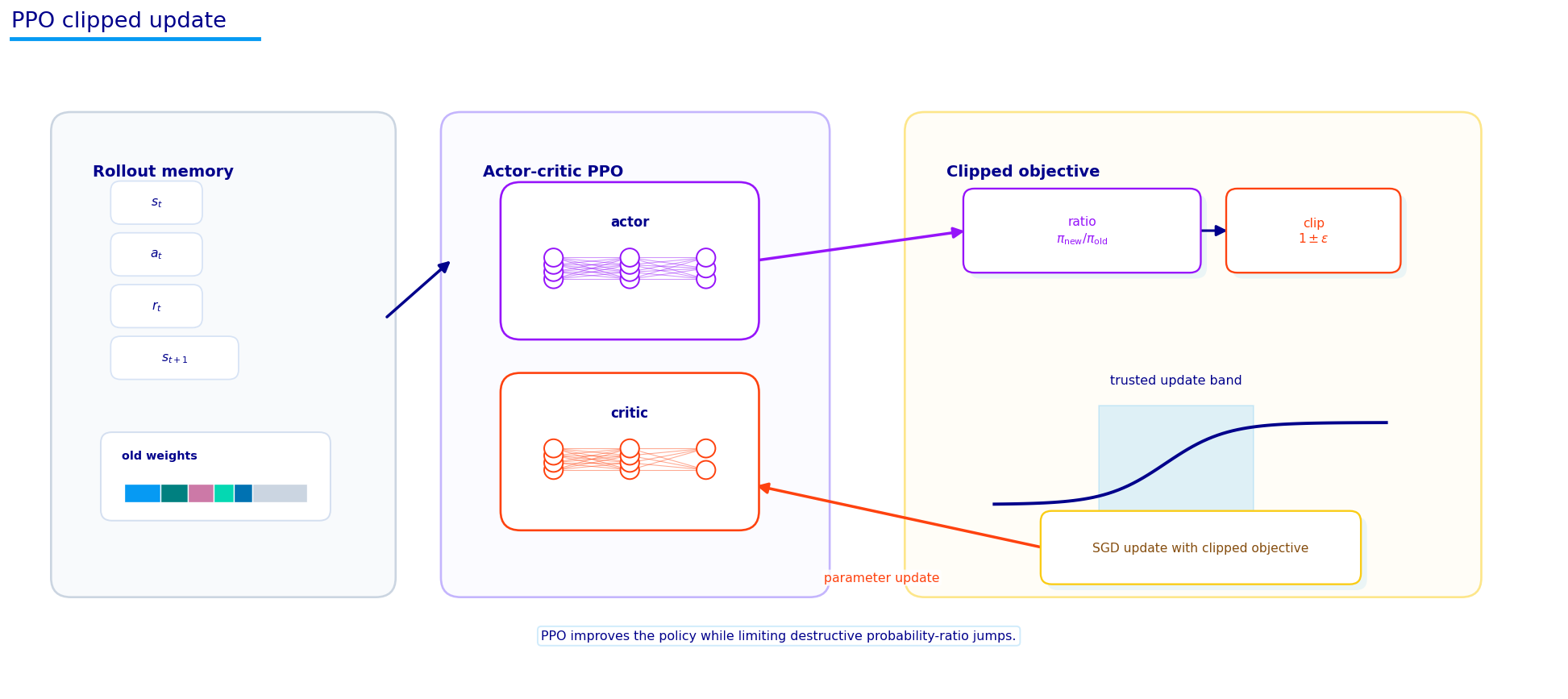

Step 6: PPO. We keep actor-critic, but make policy updates conservative through clipping. PPO is popular because it is stable, simple enough to implement, and works across many continuous-control problems.

Step 7: recurrent PPO. We add memory for partial observability. This is useful when the current state doesn’t fully reveal the market regime.

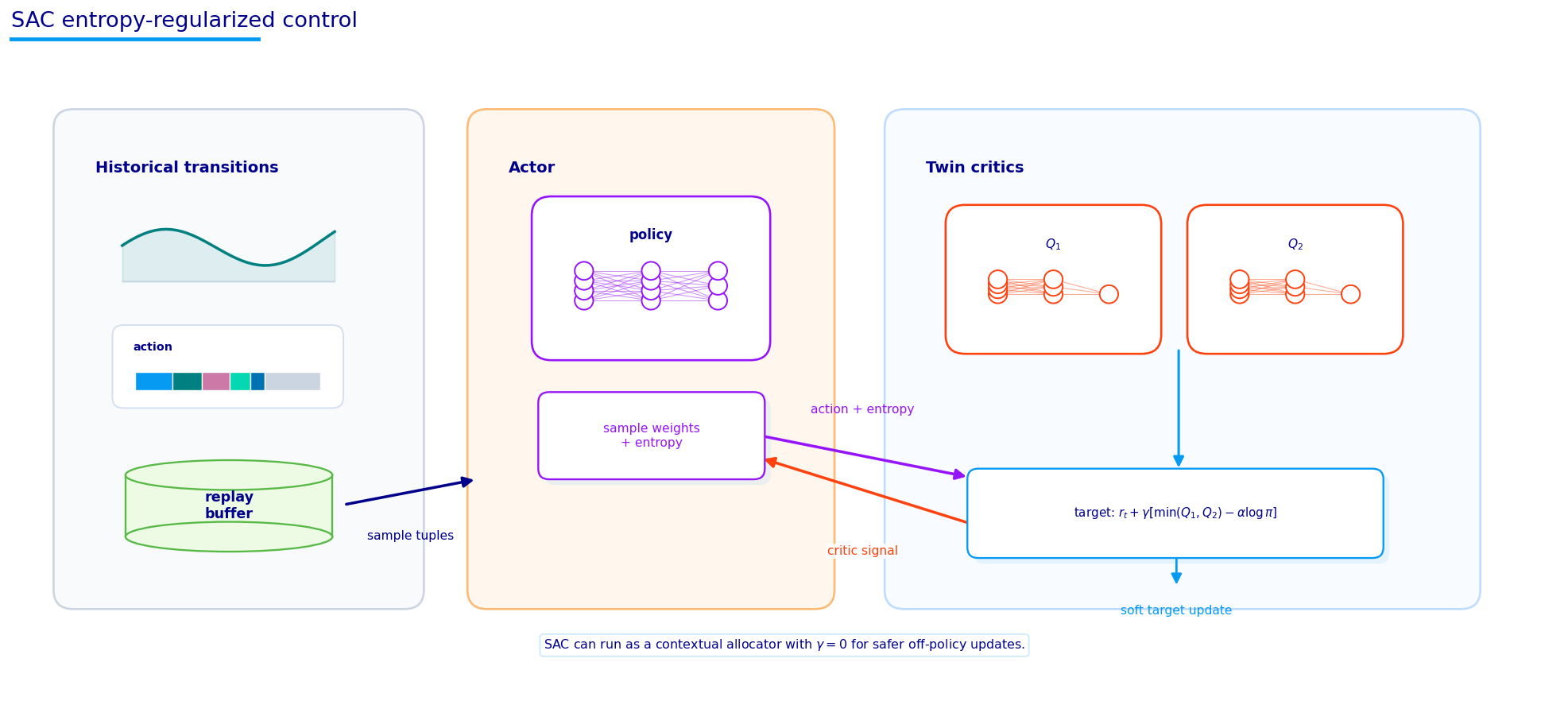

Step 8: SAC. We move to off-policy actor-critic with twin Q-functions, replay buffer, and entropy maximization. This is more sample-efficient and often stronger in continuous-control tasks.

That is the complete path this notebook wants the reader to understand. We don’t use every model in the code, but each idea explains the next one. Q-learning explains value. DQN explains neural value approximation. Policy gradient explains continuous action learning. Actor-critic explains how value and policy work together. PPO and SAC are the implemented modern versions.

7.5 Bellman recursion

The Bellman equation is the recursive identity behind RL. For a fixed policy:

The formula is simple but powerful. The value of being in state \(s\) equals the immediate reward plus the discounted value of the next state. The expectation appears because both the action and the next state can be random.

The max means that after this action, we assume the agent will choose the best possible future action. This is the basis of Q-learning.

In a tiny discrete problem, we can store \(Q(s,a)\) in a table. In portfolio allocation, the state is continuous and high-dimensional, and the action is also continuous. A table is impossible. That is why we use neural networks.

The Bellman equation is the recursive structure behind value learning:

This equation says: the value of the current state equals the immediate reward plus the discounted value of the next state. The expectation appears because the policy may be stochastic and the next state may be uncertain.

This is the same idea with the current action fixed. We take action \(a\), receive reward, move to \(s'\), and then average over future actions from the policy.

In finance, this recursion is the mathematical reason RL can account for path effects. A one-week reward may look good, but if it leaves the next state in a bad position, the future value term should reduce the action’s attractiveness. For example, a policy could increase return by going almost fully into high beta assets. If this creates a deeper drawdown and worse future reward, the Bellman recursion should eventually learn that the action’s total value is lower than its one-week return suggests.

The Bellman idea also explains why value estimation is noisy. The value target includes future values, and those values are estimated by another neural network. That creates bootstrapping error. PPO controls this partly through conservative on-policy updates. SAC controls it with twin critics and target networks.

7.6 Temporal difference learning and Q-learning

Temporal-difference learning updates a value estimate using a one-step target. The TD error is:

If \(\delta_t\) is positive, the outcome was better than expected. If it is negative, the state was overvalued. A value model can update in the direction of that error.

Here \(\alpha\) is the learning rate. The term in brackets is the Q-learning TD error. The target uses the best next action according to the current Q estimate.

\[

y = r + \gamma \max_{a'} Q_{\theta^-}(s',a')

\]

The network \(Q_{\theta^-}\) is a target network, a slower-moving copy that stabilizes training.

DQN is a bridge concept here. We don’t use DQN as the final model because a portfolio action is continuous and constrained. The action isn’t one of a few buttons. It is a full vector of allocation weights. Continuous-action problems are usually easier to handle with policy-gradient or actor-critic methods, which is why the implementation focuses on PPO and SAC.

Q-learning is the classic bridge from Bellman equations to practical RL. In tabular Q-learning, we update an estimate of \(Q(s,a)\) using:

The target is \(r_{t+1} + \gamma \max_{a'}Q(s_{t+1},a')\). It says: take the reward we just saw, then assume we choose the best action next time. If the target is higher than the current estimate, raise \(Q(s_t,a_t)\). If it is lower, reduce it.

Deep Q-Networks replace the table with a neural network:

\[

Q_\phi(s,a) \approx Q^*(s,a)

\]

DQN is important historically and conceptually, but it is less natural for this notebook’s action space. DQN works best when the action set is discrete: buy, sell, hold; move left/right; choose one of a finite number of options. Portfolio weights are continuous. We could discretize the allocation space, but with 12 risky assets plus cash, the number of possible weight combinations explodes.

That is why the notebook uses policy-gradient and actor-critic methods. Instead of scoring every possible discrete action, the actor directly outputs a continuous action distribution. This fits portfolio allocation much better.

Still, Q-learning is useful to understand because SAC uses a critic that estimates \(Q(s,a)\). The difference is that SAC learns a continuous-action \(Q\) function and an actor that samples actions likely to have high \(Q\) value while maintaining entropy.

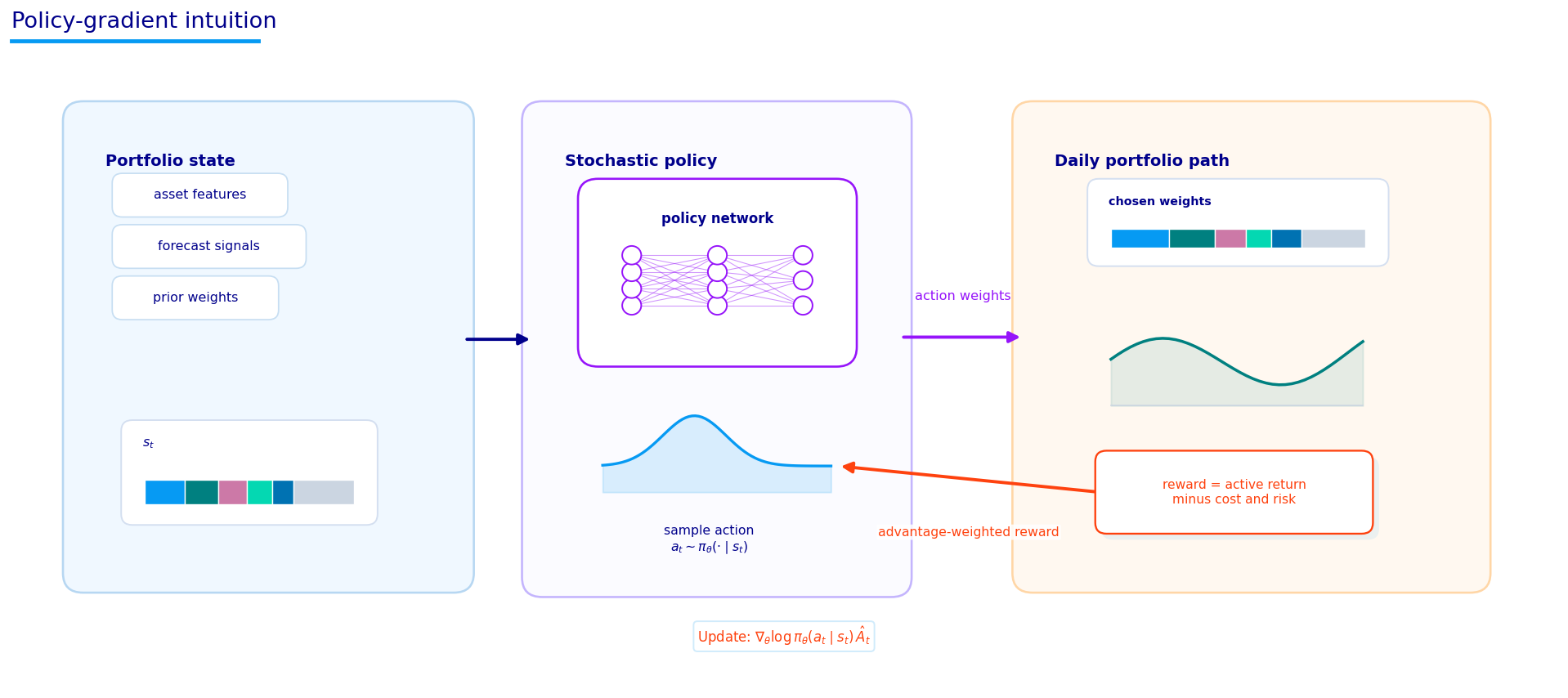

8) Policy Gradients and Actor-Critic Learning

A policy-gradient method directly parameterizes the policy:

\(\nabla_\theta \log \pi_\theta(A_t\mid S_t)\) tells us how the policy parameters affected the probability of the action we took,

\(A^\pi(S_t,A_t)\) tells us whether that action was better or worse than expected,

multiplying them increases the probability of good actions and decreases the probability of bad actions.

In this notebook, the policy outputs a Gaussian distribution over raw action vectors. So the policy can sample slightly different actions during training. That exploration is necessary. If the model always chose its current mean action, it would never learn whether nearby actions are better.

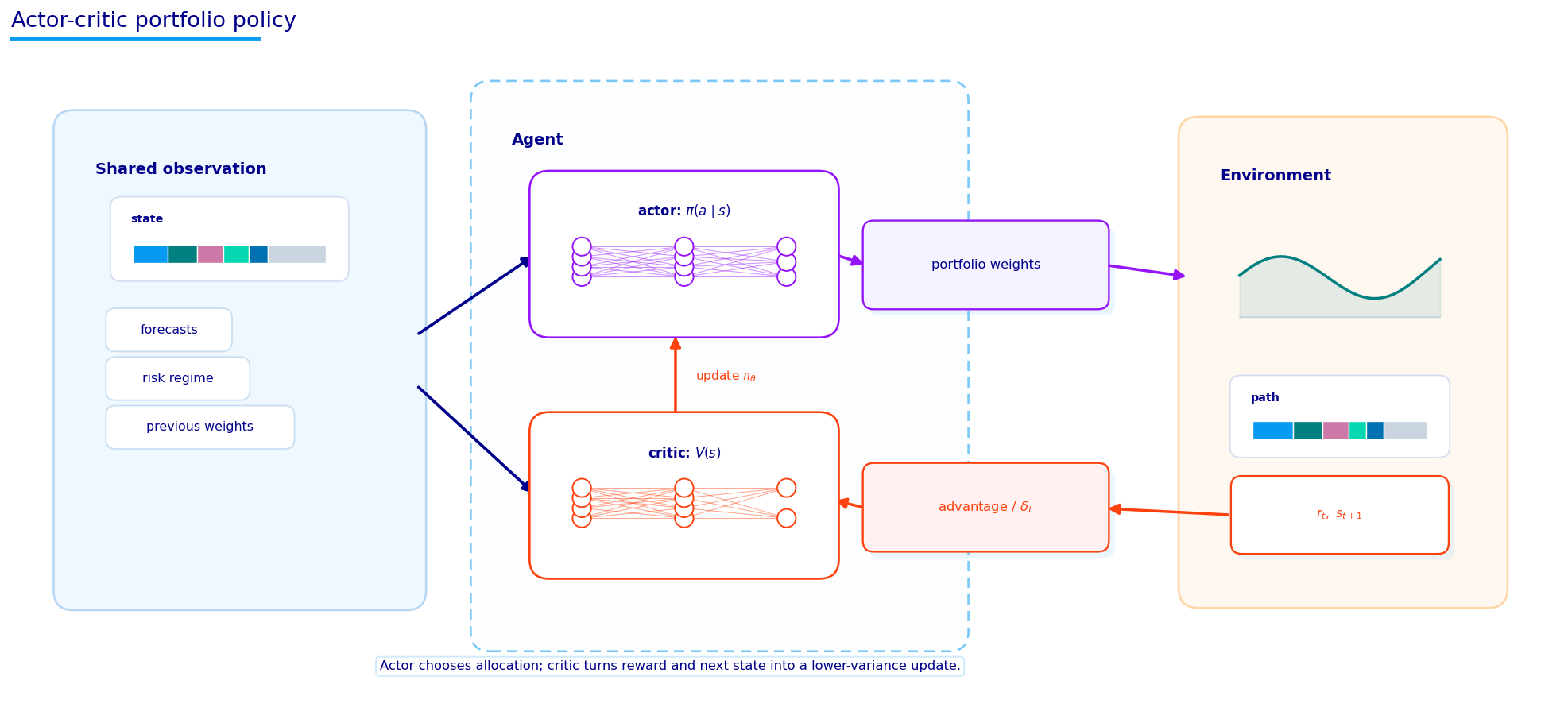

An actor-critic method combines two networks or two heads:

the actor proposes actions through \(\pi_\theta(a\mid s)\),

the critic estimates value, usually \(V_\phi(s)\) or \(Q_\phi(s,a)\).

The critic reduces variance. Instead of treating every positive return as good and every negative return as bad, we ask whether the action beat the expectation for that state. That expectation comes from the value function.

8.1 Policy gradients from the objective

Policy-gradient methods optimize the policy directly. The objective is:

Here \(\tau\) means a trajectory: states, actions, and rewards generated by policy \(\pi_\theta\). The policy-gradient theorem gives a practical gradient direction:

\(\nabla_\theta \log \pi_\theta(a_t\mid s_t)\) tells us how to change the policy parameters to make the sampled action more or less likely.

\(A^\pi(s_t,a_t)\) tells us whether the action was better or worse than expected.

If the advantage is positive, the update increases the probability of that action in similar states. If the advantage is negative, the update decreases it.

In continuous portfolio control, the policy outputs a Normal distribution over raw actions:

The action is then mapped into weights. The policy doesn’t output fixed weights deterministically during training; it samples. That sampling is exploration. Without exploration, the policy would keep repeating the same allocation and never learn whether nearby allocations are better.

The actor-critic diagram shows the two-network idea:

the actor produces actions,

the critic estimates value,

the advantage connects the two.

The critic reduces variance. Instead of comparing every reward to zero, we compare it to what the critic expected from that state. This makes policy-gradient learning much more stable.

8.2 Log probabilities and continuous actions

The term \(\log \pi_\theta(a_t\mid s_t)\) is central to policy gradients. Since the policy is stochastic, it assigns a probability density to the action it sampled. The log-probability tells us how likely that exact raw action was under the current policy.

For a Normal policy with diagonal standard deviation:

This formula says an action has high log-probability if it is close to the policy mean and the policy standard deviation is not too small. During training, the gradient of this log-probability tells the network how to shift its mean and standard deviation.

The raw action distribution is defined before the action-to-weight transformation. That is simpler because the raw action is unconstrained. After sampling, we map the raw action into a valid portfolio. The policy gradient is still computed using the raw action’s log-probability. This is common in continuous-control implementations: the network explores in an unconstrained action space, and the environment transforms the action into a legal control.

The portfolio interpretation is direct. If a sampled raw action leads to a better-than-expected reward, PPO increases the chance of similar raw actions in similar states. If the action leads to worse reward, PPO decreases it. Over many rollouts, this should shape the policy distribution toward useful allocation choices.

8.3 Actor-critic learning in portfolio language

Actor-critic can be described without losing the finance intuition:

The actor is the portfolio decision maker.

The critic is the evaluator of market states and actions.

The advantage is the critic’s correction signal.

At time \(t\), the actor samples an allocation. The environment returns a reward and a next state. The critic estimates whether that outcome was better than expected. If the action produced a positive advantage, the actor is nudged toward similar actions. If it produced a negative advantage, the actor is nudged away.

The critic is not a performance report. It is a learned function approximator. That means it can be wrong. If the critic overestimates the value of risky actions in a fragile regime, the actor can learn a bad policy. PPO reduces the damage by clipping updates. SAC reduces overestimation through twin critics and entropy. These algorithmic details matter because financial rewards are noisy and nonstationary.

The actor also doesn’t directly know the Sharpe ratio. It receives the shaped reward. So if the reward over-penalizes volatility, the actor may become too defensive. If the reward under-penalizes drawdown, the actor may become too aggressive. The reward design and the actor-critic update are connected. A good algorithm can’t save a badly aligned reward.

This is why the notebook reports reward components, policy diagnostics, stress windows, and risk reports. We need to see not only that the RL loss went down, but also what kind of portfolio behavior emerged.

Show code

from quantfinlab.plotting.diagrams import policy_gradient_diagramfig, ax = policy_gradient_diagram()plt.show()

Show code

from quantfinlab.plotting.diagrams import actor_critic_diagramfig, ax = actor_critic_diagram()plt.show()

The policy-gradient diagram shows this idea visually. The policy samples an action, the environment returns reward, and the advantage estimate tells the policy whether that action should become more or less likely. The actor-critic diagram adds the critic: the actor still chooses the action, but the critic learns a value estimate and gives the actor a lower-variance learning signal.

For portfolio allocation, this division is natural. The actor asks, “what weights should I hold?” The critic asks, “given the current market state and portfolio condition, how valuable is this situation?” If the actor makes a risky allocation in a fragile state and the next reward is poor, the critic helps convert that poor outcome into a parameter update.

8.4 Generalized advantage estimation

PPO and recurrent PPO use generalized advantage estimation. The one-step TD residual is:

\[

\delta_t = r_t + \gamma V(s_{t+1}) - V(s_t)

\]

This residual says how surprising the reward plus next-state value was relative to the current value. GAE combines many TD residuals: