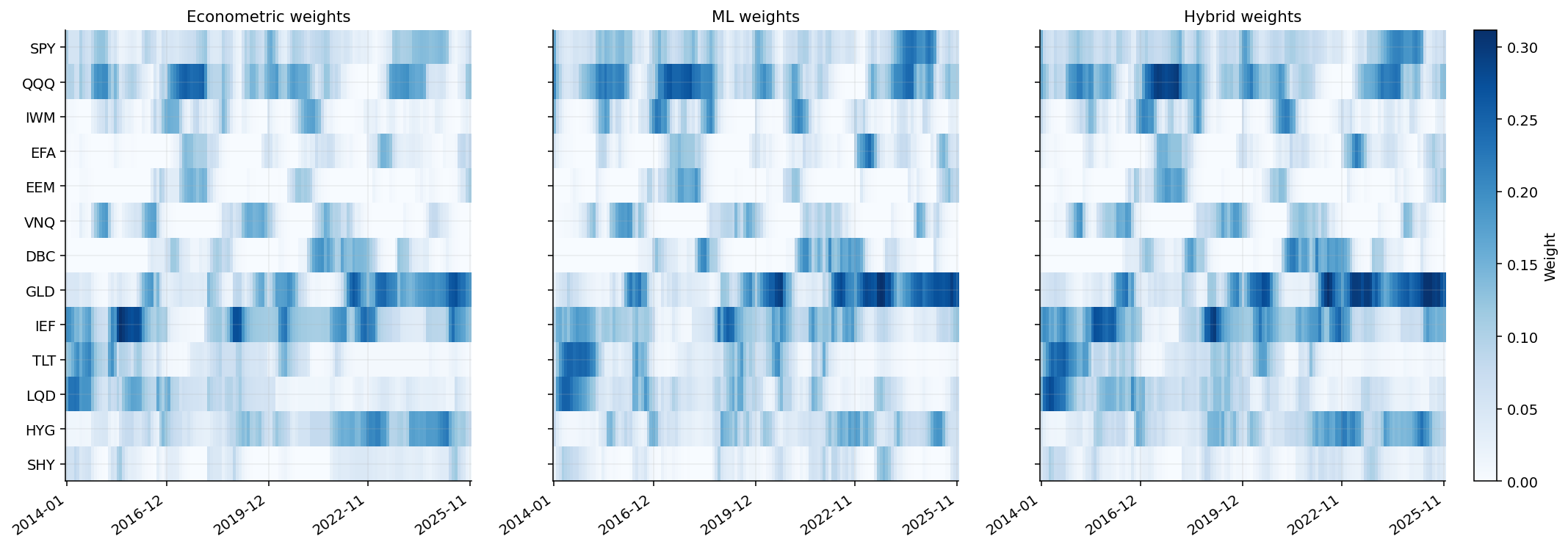

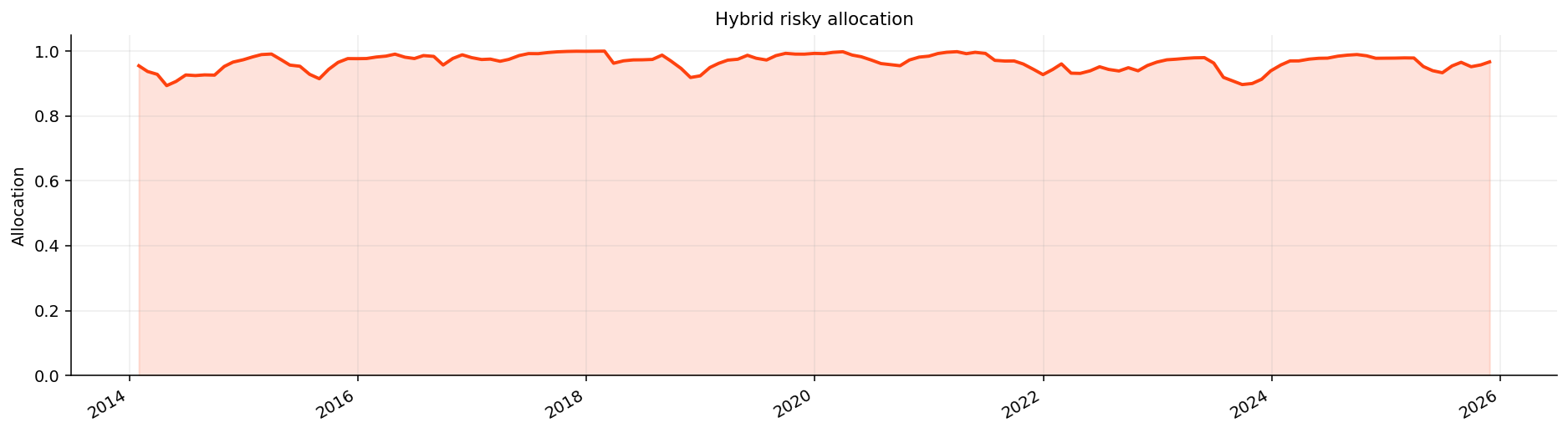

Turn regime probabilities into portfolio weights through state-conditioned sleeves and risk budgets.

Compare regime-aware portfolios against repeated portfolio baselines from earlier projects.

Repeat the full idea on a sector ETF universe using the packaged library implementation.

This one should be read as two connected courses inside one finance application:

Econometrics and stochastic processes, especially Markov chains, Markov regression, and hidden Markov models.

Machine learning, including unsupervised learning, supervised classification, feature selection, model validation, and probability-driven portfolio decisions.

The financial problem is simple to state but hard to solve: markets don’t behave the same way in every environment. A portfolio that works in a calm growth regime can be completely wrong during inflation stress, credit stress, or volatility clustering. The hard part is that the regime isn’t directly visible. We don’t observe a label on the market saying “today is defensive.” We observe returns, rates, spreads, drawdowns, correlations, macro blocks, and sector behavior. The model has to infer the state from those signals.

Market behavior across equity, credit, bonds, commodities, and sectors

Returns and rolling features

Predictors \(X_t\)

Market state variables available at date \(t\)

Diagnostics

Feature quality control

Avoid unstable features, redundancy, and leakage

Clusters, HMM, classifiers

Regime inference

Estimate whether the environment is risk-on, neutral, or defensive

Month-end probabilities

Decision signal

Translate daily state estimates into rebalancing inputs

Regime-aware weights

Portfolio policy

Change risk exposure based on state probabilities

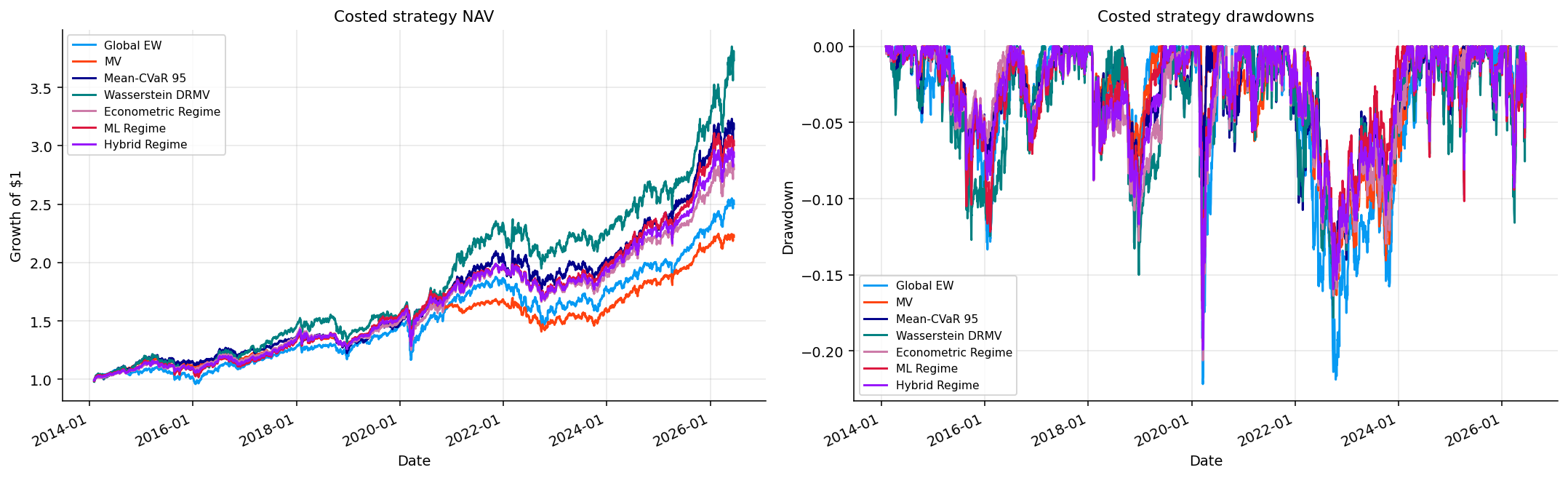

Costed backtest

Out-of-sample evaluation

Check whether the regime layer adds value after trading costs

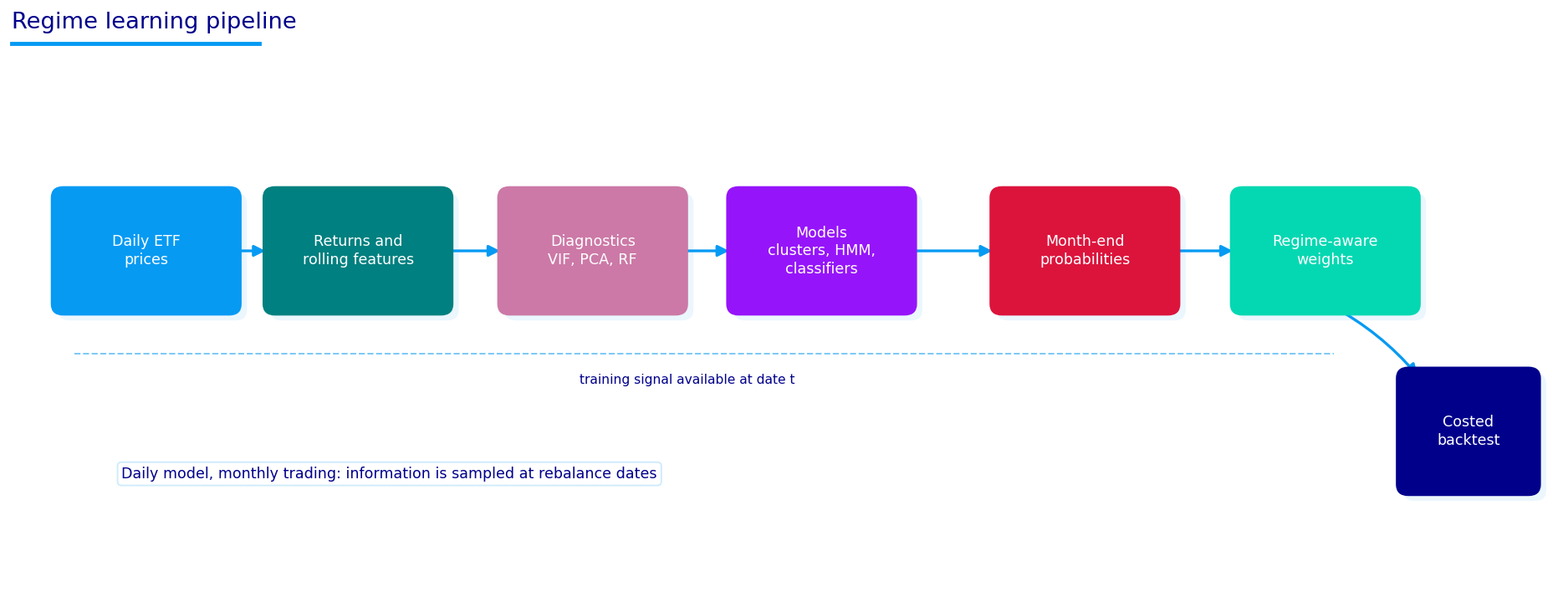

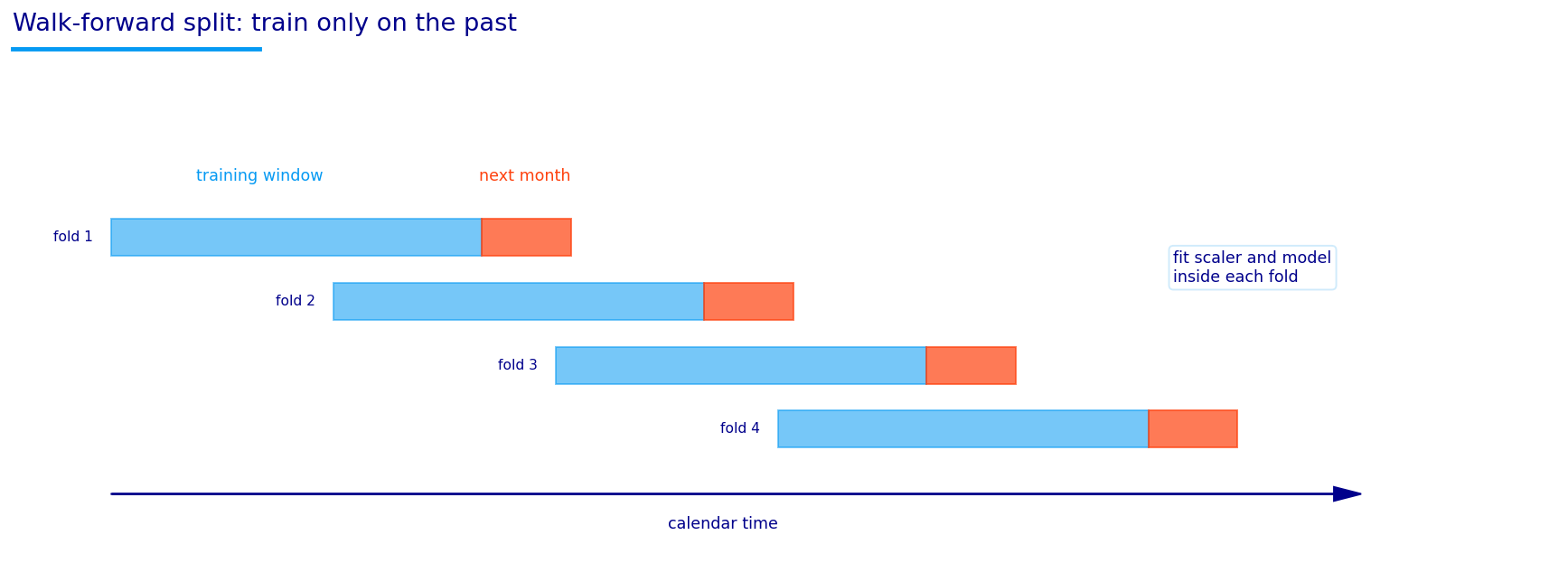

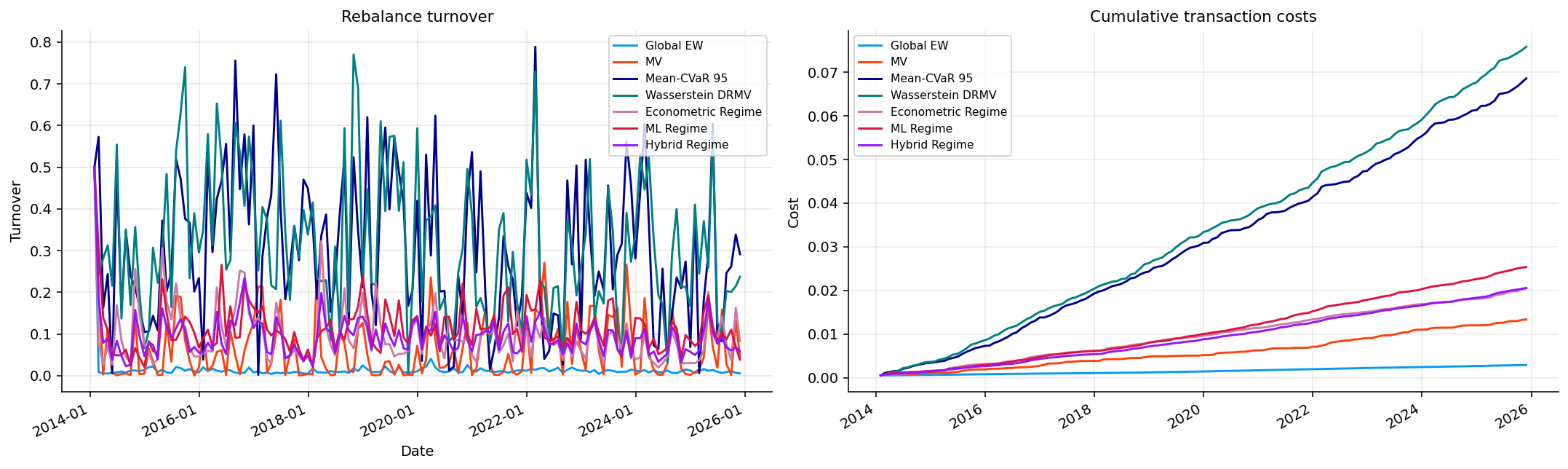

The important design choice is that we sample information daily but trade monthly. Daily observations give the model enough data to learn regime structure. Monthly rebalancing keeps the portfolio from becoming a noisy high-turnover trading system. A regime probability doesn’t need to trigger a trade every day. It needs to make the month-end allocation more aware of the current environment.

The pipeline diagram shows this exactly. The dashed line under the features means the model only uses information that would’ve been available at the rebalance date. That matters because regime models are very easy to overstate if future outcomes accidentally leak into the features. The realized future regime labels are used only for training and evaluation, not as live inputs at the rebalance date.

The diagram also separates learning from trading. A model can learn on daily observations, but the portfolio can still rebalance monthly. This is a good compromise in finance because regimes usually persist longer than one day, while daily noise is high.

For a learner, the useful way to read the rest of the project is:

Features describe today’s market.

Labels describe what happened over the next 63 or 126 trading days.

Unsupervised models try to discover regimes from the features without seeing labels.

Supervised models learn a direct mapping from features to realized future regime labels.

Markov models add time dependence, meaning today’s state is related to yesterday’s state.

Portfolio rules convert probabilities into allocations instead of converting hard labels into all-or-nothing trades.

That last point is important. A regime model rarely knows the state with certainty. The output is usually something like \(P(\text{risk-on})=0.60\), \(P(\text{neutral})=0.25\), and \(P(\text{defensive})=0.15\). That probability vector carries much more information than a single hard label. It lets us build a portfolio that leans risk-on without pretending the defensive risk has disappeared.

The pipeline diagram is also useful because it separates three ideas that often get mixed together:

Feature learning: turning market history into a matrix \(X_t\) that describes the current state.

Regime inference: estimating probabilities for states such as risk-on, neutral, or defensive.

Portfolio action: turning those probabilities into weights, costs, and realized performance.

These three layers have different failure modes. A weak feature set can make every model bad. A good feature set can still be handled badly if the model overfits or produces unstable probabilities. A good probability model can still fail if the portfolio mapping is too aggressive, too slow, or too costly.

So the project isn’t only about asking which classifier has the highest accuracy. The real workflow is:

where \(X_t\) is the feature vector observed at time \(t\), \(\hat{p}_t(S_t=k)\) is the estimated probability of regime \(k\), \(w_t\) is the portfolio weight vector chosen at the rebalance date, and \(R_{p,t+1}\) is the next realized portfolio return.

The important design choice is that we keep the learning horizon and trading horizon separate. The model can read daily data and learn daily state changes, but the strategy still trades monthly. This avoids the common mistake of building a very active model just because daily predictions are available. In real portfolios, daily switching across ETFs creates cost, slippage, and model noise. Monthly rebalancing forces the regime signal to be economically meaningful enough to survive a practical trading schedule.

A useful way to think about the whole project is this:

We don’t try to predict tomorrow’s return directly. We try to estimate the market environment that makes some portfolio sleeves more attractive than others.

That difference matters. Predicting one-day returns is extremely noisy. Predicting whether the market is in a broad risk-on, neutral, or defensive condition over the next few months is still difficult, but it matches how allocators usually think. A portfolio manager doesn’t usually say “SPY will return 0.12% tomorrow.” They are more likely to say “credit is strong, breadth is healthy, volatility is falling, and duration isn’t being rewarded, so the portfolio can carry more risky exposure.” This project turns that kind of reasoning into a machine-learning and econometric system.

2) Data, Reused Inputs, and Portfolio Baselines

The raw data is mostly reused from earlier projects, so we keep the data explanation focused on how the data is used in this regime-learning setup.

We use a cross-asset ETF universe for the main regime model:

Risk assets: SPY, QQQ, IWM, EFA, EEM, VNQ, HYG.

Real assets and inflation-sensitive assets: DBC and GLD.

Rates and credit assets: IEF, TLT, LQD, HYG, SHY.

Context tickers: XLE and XLU are included because energy and utilities help identify inflation and defensive rotations.

The cash-like ticker is SHY, which behaves as short-duration Treasury exposure. It isn’t pure cash, but it gives a conservative low-duration place for the portfolio to move when the regime model becomes defensive.

The baseline portfolios reuse machinery from earlier projects:

Equal weight and mean-variance logic come from Project 2.

Mean-CVaR and Wasserstein robust optimization come from Project 10.

Financial conditions and macro blocks are based on Project 12.

We don’t need to re-explain Ledoit-Wolf, Bayes-Stein, CVaR, or Wasserstein DRO here. The important part is how regime probabilities change the portfolio relative to those baselines.

The coverage table confirms that the ETF panel is long enough to support a regime-learning workflow. SPY starts in 1999, QQQ in 1999, IWM in 2000, EFA in 2001, and the fixed-income ETFs in 2002. Some assets start later: EEM starts in 2003, VNQ in 2004, DBC in 2006, and HYG in 2007. Because HYG and DBC are important for credit and commodity regimes, the effective fully usable cross-asset regime sample naturally starts later than SPY’s history.

The daily panel runs from 1999-01-04 to 2026-06-17, with 6906 daily rows and 270 monthly rebalance dates after the training-history requirement. This gives enough observations for daily ML fitting, but the number of monthly backtest decisions is much smaller. That distinction matters. Classification metrics are evaluated on many daily observations, while portfolio performance is evaluated on monthly decisions and daily returns between rebalances.

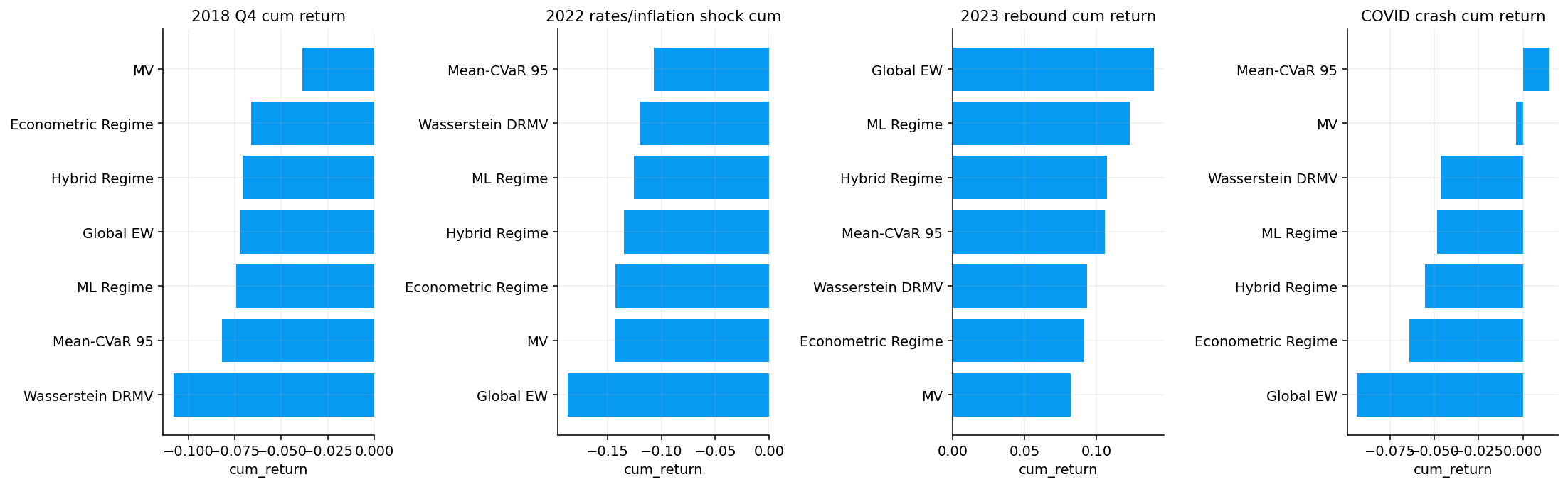

The asset summary shows a wide range of behavior. GLD has the highest sample Sharpe among the listed assets, followed by LQD, SPY, QQQ, and IEF. QQQ has high annualized return but also very high volatility and a huge historical drawdown. DBC has weak Sharpe and a massive drawdown, which fits its commodity-futures behavior over long samples. TLT has a positive long-run return but large rate-cycle drawdowns, especially after the 2021-2022 rate shock.

This matters for regime learning because the labels shouldn’t just identify “stocks up” or “stocks down.” They need to distinguish between:

broad risk-on periods where equities and credit lead,

neutral periods where defensive assets may still do fine,

stress periods where defensive assets and gold can dominate risky sleeves,

inflation-rate stress where bonds don’t protect equity drawdowns well.

The model has to learn from cross-asset relationships, not just from one equity index.

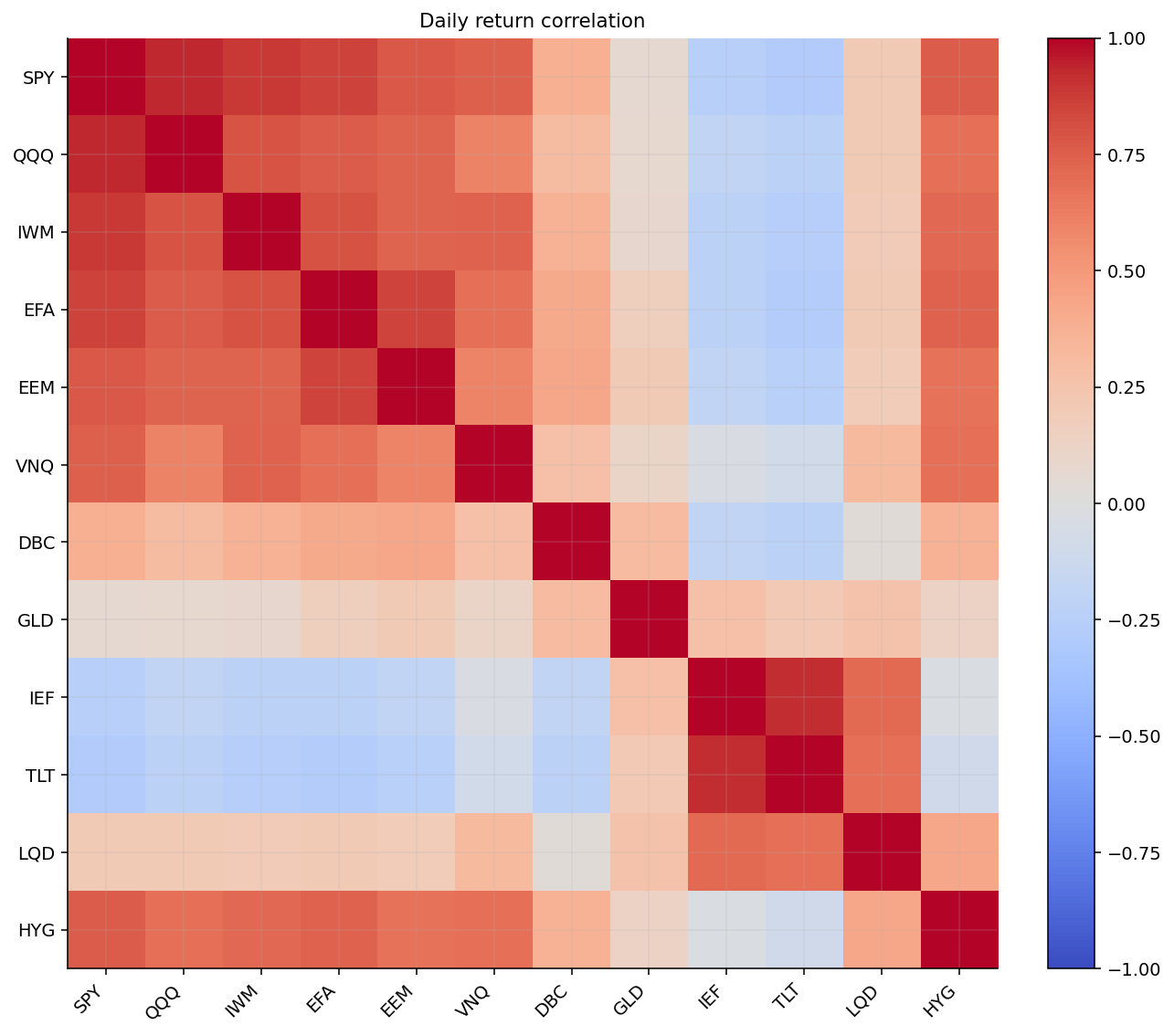

The correlation heatmap after the asset summary shows the expected block structure. Equity ETFs and high-yield credit cluster together. Treasury ETFs cluster together. GLD and DBC are less tightly connected to the equity-credit block, which is exactly why they can help distinguish inflation, risk-off, and diversification regimes.

For regime learning, correlation structure isn’t only a diversification object. It also acts as a state variable. In calm markets, risky assets may rise together but correlations aren’t necessarily extreme. In panic markets, correlations across risky assets often jump because investors sell everything liquid at the same time. In inflation/rate stress, the stock-bond correlation can become less negative or even positive, reducing the protection from long duration.

So when we later build features like average rolling correlation, correlation shocks, and SPY-TLT correlation, we are turning this market structure into predictors. The regime model doesn’t only look at returns. It also asks whether the market’s internal relationships are behaving like a normal expansion, a defensive rotation, or a correlated stress event.

The baseline grid is intentionally short in this project. The mean-variance and MaxSharpe baselines are used to create comparison portfolios and an anchor for the regime allocations. The training-period selection picks MV (EWMA, BayesSteinMomentum) as the MV source in the first main backtest, and it uses a MaxSharpe variant as the source for Mean-CVaR and Wasserstein robust portfolios.

The main lesson from this output is that the baselines are already non-trivial. We aren’t comparing the regime layer only against a weak equal-weight portfolio. We also compare against:

a shrinkage-based MV portfolio,

a Mean-CVaR portfolio that explicitly cares about downside tail risk,

and a Wasserstein robust portfolio that penalizes fragile optimization under distributional uncertainty.

That makes the final comparison more serious. If regime learning only beats equal weight but loses to robust optimization, the result is still useful, but it tells us the ML layer is more of a risk-shaping overlay than a complete replacement for robust portfolio construction.

The new contribution is what we build on top of these pieces: a regime-learning layer that compares unsupervised clustering, Markov models, hidden Markov models, and supervised classifiers, then asks whether their state probabilities improve allocation decisions after costs.

This also explains why the data has to be broad. A regime model trained only on SPY returns would mostly learn equity trend and volatility. That would miss many important transition signals. Credit can weaken before equities sell off. Treasury duration can stop diversifying when inflation becomes the dominant risk. Gold can behave differently in liquidity crises and inflation shocks. International equities can reveal dollar and global-growth pressure. Macro factors add another lens by measuring inflation, growth, labor, policy, and financial conditions.

So the feature space is deliberately cross-asset and macro-aware. The goal isn’t to create a perfect return forecast. The goal is to give the model enough economically meaningful information to distinguish different market environments.

3) Feature Engineering for Financial Regimes

A regime model is only as good as its feature space. The feature vector at date \(t\) is:

where each feature is a market condition that would’ve been observable at time \(t\). The model later learns either:

\[

\hat{S}_t = f(X_t)

\]

for unsupervised/discovery models, or:

\[

P(Y_t = k \mid X_t)

\]

for supervised classifiers, where \(Y_t\) is a realized future regime label.

The feature set is designed around economic blocks, not random technical indicators. The blocks are:

Equity trend and leadership, such as SPY momentum, QQQ vs SPY, small-cap vs large-cap, international vs US, and EM vs developed ex-US.

Credit health, such as HYG vs LQD, high-yield drawdown, high-yield downside volatility, and HYG vs SHY.

Duration and rates, such as TLT vs SHY, IEF vs SHY, Treasury yields, and curve-slope changes.

Real assets and inflation, such as DBC, GLD, DBC vs IEF, GLD vs SPY, and energy vs utilities.

Cross-asset pressure, such as risk-on assets versus defensive assets, credit-equity divergence, inflation-duration spread, and duration-equity divergence.

Market internals, such as breadth, dispersion, volatility shock, drawdown level, drawdown speed, average correlation, and equity-bond correlation.

The reason we use blocks is that regimes aren’t one-dimensional. A high SPY return can happen in several different environments. It can be a broad growth rally, a narrow mega-cap rally, a relief rally after a crash, or an inflationary nominal rally. The regime label becomes more meaningful when the model sees equity, credit, rates, real assets, correlation, and macro conditions together.

3.1 Equity Leadership Features

The first feature block measures equity momentum and leadership.

A basic total return feature over a window \(L\) is:

where \(P_{t,i}\) is the adjusted price of asset \(i\) at date \(t\). This says how much the asset has gained or lost over the last \(L\) trading days.

The skip avoids letting very recent reversal noise dominate the signal. For SPY, the feature spy_252_21 measures roughly 12-month momentum excluding the latest month.

Relative return features take the difference between two total returns:

From the latest table, EEM vs EFA is strongly positive near the end of the sample, while QQQ vs SPY and IWM vs SPY are also positive. This tells us the latest equity leadership isn’t purely defensive. It has signs of EM strength, growth strength, and some small-cap participation. That doesn’t automatically mean the portfolio should be fully risk-on, but it gives the supervised and unsupervised models positive evidence on the risky side.

3.2 Credit, Duration, and Real-Asset Features

Credit features are central because credit often turns before equity. HYG is high-yield corporate credit, and LQD is investment-grade corporate credit. The spread-like relative return:

acts like a price-based credit sentiment indicator. When HYG outperforms LQD, credit investors are accepting default risk and liquidity risk. When HYG underperforms, the market is usually moving toward quality and safety.

We also use high-yield drawdown and downside semi-volatility. If \(r_t\) is the daily return, downside semi-volatility keeps only the negative return side:

When this is positive, long-duration bonds are beating short bills, usually because yields are falling or investors are paying for duration protection. When it is negative, duration is under pressure, usually because rates are rising or inflation risk is high.

Real-asset features use commodities, gold, and energy:

This feature is powerful in environments like 2022, where real assets and energy can hold up while duration bonds fall. In a normal equity crash with falling yields, this feature may behave very differently because Treasuries can rally. That difference helps the model separate classic risk-off from inflation/rate stress.

The latest credit and duration table shows high-yield credit still positive over the recent 63-day window, with HYG drawdown near zero and high-yield volatility low. That supports a calmer credit environment. At the same time, several duration-relative features can be weak when long bonds lag short duration. This combination gives the model a more nuanced state: risk appetite isn’t collapsing, but duration isn’t necessarily attractive.

This is exactly why regime learning can be useful. A simple stock-only rule might say “risk-on.” A cross-asset model can say “risky assets are strong, credit isn’t breaking, but the rate environment still makes long duration risky.” Later, the portfolio weights reflect that nuance by holding risky assets and gold/IEF together rather than simply going all in on equities.

3.3 Market Pressure and Internal Structure

The pressure features combine sleeves. We compare average risky performance against defensive performance:

A market where SPY is up but breadth is weak is more fragile than a market where most risky assets are rising together. The model also uses dispersion:

If this ratio jumps above 1, short-term volatility is rising faster than the slower volatility baseline. Drawdown level and drawdown speed measure whether SPY is already below its rolling high and whether the drawdown is worsening.

Correlation features use rolling correlations across assets:

In stress periods, \(\bar{\rho}_{t,L}\) often rises because diversification inside risky assets disappears. We also track correlation shocks, which compare short-window correlation to long-window correlation. This makes the model sensitive to sudden changes in market structure, not only levels.

def breadth(tickers, window): data = pd.concat([total_ret(t, window) for t in tickers], axis=1)return data.gt(0.0).mean(axis=1)def dispersion(tickers, window): data = pd.concat([total_ret(t, window) for t in tickers], axis=1)return data.std(axis=1, ddof=1)def realized_vol(ticker, window):return returns[ticker].rolling(int(window)).std(ddof=1) * np.sqrt(annualization)def drawdown_level(ticker, window):return close[ticker] / close[ticker].rolling(int(window), min_periods=max(63, int(window) //4)).max() -1.0def rolling_avg_corr(tickers, window): data = returns[tickers].astype(float) pairs = []for i, left inenumerate(tickers):for right in tickers[i +1:]: pairs.append(data[left].rolling(int(window)).corr(data[right]))return pd.concat(pairs, axis=1).mean(axis=1)

The internal market-state table near the end of the sample shows full breadth across risky assets, relatively moderate SPY volatility, and drawdown levels close to zero. That leans risk-on. But the average correlation level and correlation changes also matter because high correlation can turn a seemingly diversified risky sleeve into one large equity-credit bet.

The important point for the model is that features are allowed to disagree. We don’t force every signal to say the same thing. A regime classifier can learn that strong breadth with rising volatility means something different from strong breadth with falling volatility. It can learn that gold strength with credit stress means something different from gold strength during a broad commodity rally. The feature set is intentionally redundant at first because the next steps, VIF, PCA, and RandomForest importance, help us diagnose and reduce that redundancy.

A feature matrix for regime learning is different from a feature matrix for a normal cross-sectional prediction problem. In a normal stock-selection problem, each row might be a stock and each column might be a characteristic. Here each row is a date, and each column is a market-state measurement observed on that date.

The important point is that a regime is usually not visible in one variable. A market can have positive equity momentum but deteriorating credit. It can have strong breadth but rising inflation pressure. It can have high Treasury returns because growth is weakening, or because policy rates are falling in a calm disinflationary environment. The same raw asset return can mean different things depending on the rest of the state vector.

where \(A\) and \(B\) are two assets and \(L\) is the lookback window. If \(A=\text{HYG}\) and \(B=\text{LQD}\), this feature asks whether high-yield credit is outperforming investment-grade credit. If it is positive, credit markets are usually accepting more default risk. If it is negative, investors are usually moving toward safer credit quality.

This is always less than or equal to zero. A value near zero means the asset is near its local high. A value like \(-0.20\) means the asset is down 20% from its recent peak. In regime learning, drawdown is useful because it measures accumulated damage, not just recent volatility. A market can be volatile but still near highs; it can also be in a slow grind-down with moderate daily volatility but deep drawdown.

Volatility-shock features measure whether volatility itself is changing:

where \(\sigma_t^{(L)}\) is a rolling volatility estimate and \(m\) is a change window such as 21 or 63 trading days. Rising volatility often marks a transition from calm risk-on to unstable neutral or defensive states. Falling volatility after a selloff can mark recovery.

Correlation features are especially important in this project. A cross-asset portfolio usually depends on diversification. If equities, credit, commodities, and bonds start moving together, the portfolio’s true risk can rise even if individual asset volatilities don’t explode. A rolling average correlation can be written as:

where \(\rho_{ij,t}^{(L)}\) is the rolling correlation between assets \(i\) and \(j\) over window \(L\). High \(\bar{\rho}_t\) means diversification is weaker. A correlation shock can turn many separate trades into one large macro trade.

This is why the feature set starts broad. We aren’t assuming one variable defines the state. We first collect many economically meaningful measurements, then use diagnostics and selection to decide which ones are usable for the models.

Feature scaling matters more here than it might seem at first. Many models in this project are geometry-based. KMeans, GMM, SVM, and KNN all depend on distances, margins, or Gaussian densities in feature space. If one feature is measured in percentage points and another is measured in basis points, the larger-scale feature can dominate the model even if it isn’t economically more important.

So we standardize features before fitting most models:

\[

z_{t,j} = \frac{x_{t,j} - \mu_j}{s_j}

\]

where \(x_{t,j}\) is feature \(j\) at date \(t\), \(\mu_j\) is the training-window mean, and \(s_j\) is the training-window standard deviation. After this transformation, each feature is measured in “number of standard deviations from its normal level.”

In financial language, this makes features comparable as stress signals. A \(+2\) value for vol_change_63 means volatility has risen strongly relative to its own history. A \(+2\) value for fci_blend means financial conditions are meaningfully tight relative to their own history. The units are different, but the z-score puts them on a comparable abnormality scale.

There is also a subtle leakage point here. Scaling parameters must be estimated only from the training window in a walk-forward setting. If we standardize the whole sample using future means and standard deviations, the model learns from the future indirectly. For example, the volatility distribution after 2020 isn’t the same as before 2020. Using full-sample scaling tells the pre-2020 model how extreme future crisis volatility will be, which isn’t available in real time.

The same training mean and training standard deviation are used for the test observation. This is exactly the same logic as fitting a scaler in a normal ML pipeline, but in finance the chronological order is more important because market distributions change through time.

The feature matrix isn’t only a numerical input. It is the economic vocabulary that all later models are allowed to speak.

A good regime model should have features that are interpretable after the fact. This matters because portfolio decisions need explanation. If the model reduces risk, we want to know whether it is because credit weakened, volatility rose, breadth broke, macro pressure tightened, or duration stopped diversifying.

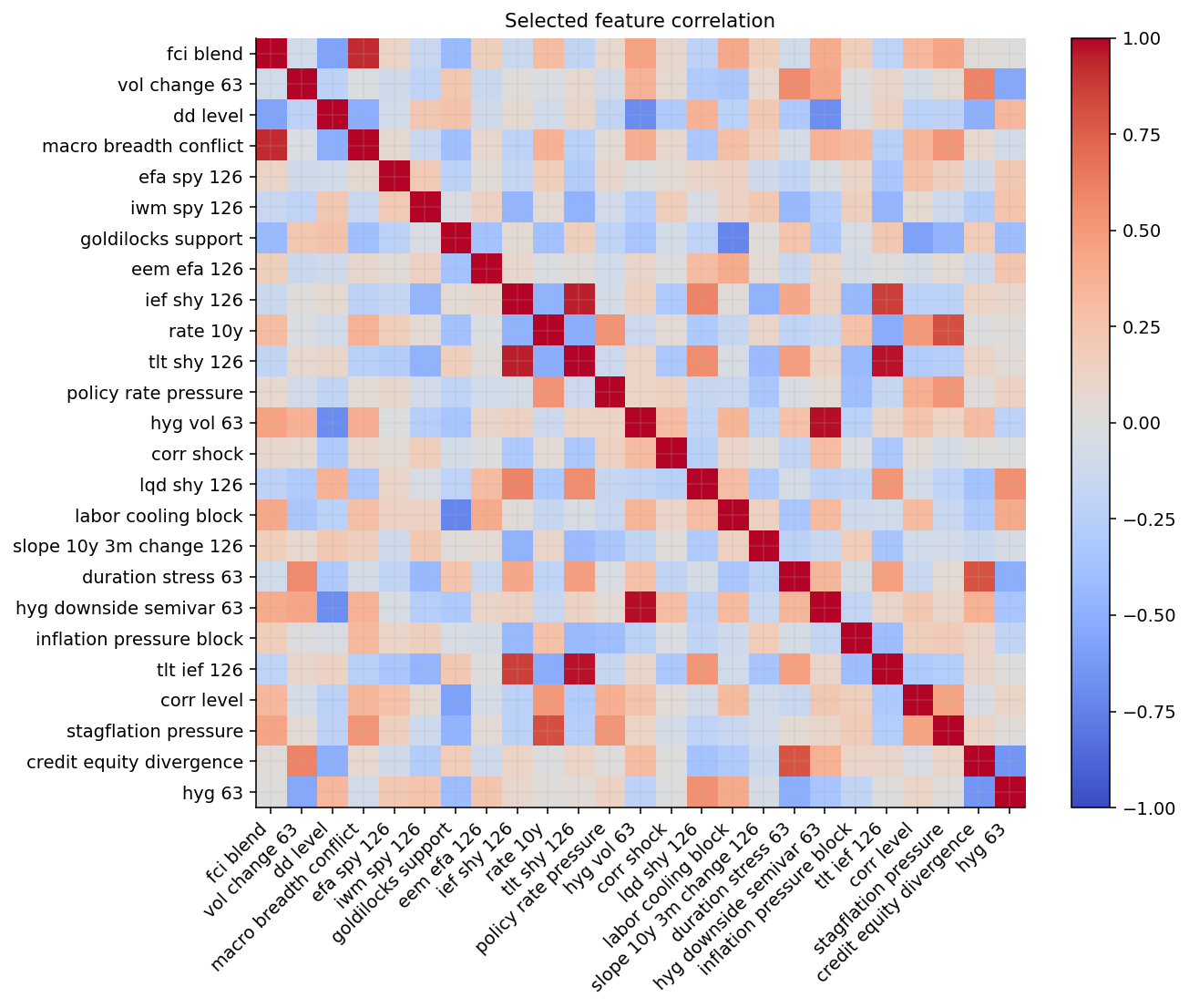

The selected feature list gives us a compact economic dashboard:

FCI and macro blocks describe the macro backdrop. Tight financial conditions usually pressure risky assets because discount rates rise, credit becomes less available, and liquidity becomes less supportive. A high fci_blend can therefore push the model toward defensive or neutral states even before equities fully sell off.

Volatility and drawdown features describe market damage. vol_change_63 captures acceleration in uncertainty. dd_level captures realized drawdown pressure. These features often separate normal pullbacks from real regime shifts.

Credit features describe balance-sheet risk. HYG downside semivariance and HYG volatility show whether lower-quality credit is becoming unstable. Credit weakness is especially important because equity markets can remain calm for a while even when credit risk starts repricing.

Duration features describe the rate side. Features such as ief_shy_126, tlt_shy_126, and tlt_ief_126 tell us whether duration is being rewarded or punished. This is crucial after the 2022 experience, where long bonds weren’t always defensive.

International leadership features describe global risk appetite. EFA vs SPY, EEM vs EFA, and IWM vs SPY help identify whether leadership is broad or narrow. EM strength can indicate global liquidity and dollar conditions are supportive. Small-cap strength can indicate domestic cyclicality and credit appetite.

Correlation and breadth features describe internal market structure. Strong breadth means many risky assets are participating. High correlation means diversification is weaker. A market with strong breadth and low correlation is healthier than a market with high correlation and falling breadth.

This feature interpretation is one of the reasons Project 16 can work as a learning source. The model isn’t a black box sitting on random numbers. Each variable is tied to a market mechanism, and the diagnostics show which mechanisms ended up mattering most.

Before we fit regime models, we inspect the feature matrix. Financial features are usually correlated because they are constructed from overlapping prices and overlapping horizons. For example, tlt_shy_126, tlt_ief_126, and ief_shy_126 are mathematically connected. If TLT beats IEF and IEF beats SHY, then TLT should also beat SHY. That creates multicollinearity.

The variance inflation factor for feature \(j\) is:

\[

\text{VIF}_j = \frac{1}{1 - R_j^2}

\]

where \(R_j^2\) comes from regressing feature \(x_j\) on all the other features. If \(R_j^2\) is close to 1, the feature is almost explained by the others, and \(\text{VIF}_j\) explodes. A high VIF doesn’t mean the feature is useless. It means linear models may have unstable coefficients because the model can’t uniquely assign credit to one correlated feature.

PCA gives another view. If \(X\) is the standardized feature matrix, PCA decomposes it into orthogonal directions:

\[

X = UDV^\top

\]

The columns of \(V\) are loading vectors, and each principal component is:

\[

PC_{t,k} = X_t v_k

\]

The explained variance ratio for component \(k\) is:

where \(\lambda_k\) is the variance explained by component \(k\). If the first few PCs explain a large share of the variance, the feature space has strong common structure. If the variance is spread across many PCs, the features contain more independent dimensions.

RandomForest permutation importance answers a more predictive question. After training a model, we shuffle one feature and see how much the score falls:

where \(X_{\pi(j)}\) is the feature matrix with column \(j\) permuted. If shuffling feature \(j\) hurts balanced accuracy, that feature carries useful predictive information.

Show code

def feature_vif_local(x): z0 = x.replace([np.inf, -np.inf], np.nan).dropna().astype(float) rows = []for col in z0.columns: other = [c for c in z0.columns if c != col]ifnot other: rows.append({"feature": col, "r2": np.nan, "vif": np.nan})continue y0 = z0[col].to_numpy(dtype=float) X0 = z0[other].to_numpy(dtype=float) r2 = LinearRegression().fit(X0, y0).score(X0, y0) vif = np.inf if r2 >=1.0-1e-12else1.0/ (1.0- r2) rows.append({"feature": col, "r2": r2, "vif": vif})return pd.DataFrame(rows).set_index("feature").sort_values("vif", ascending=False)def pca_tables_local(x, n_components=10): z0 = x.replace([np.inf, -np.inf], np.nan).dropna().astype(float) arr = StandardScaler().fit_transform(z0) n =min(int(n_components), min(arr.shape)) pca = PCA(n_components=n, random_state=42).fit(arr) cols = [f"PC{i +1}"for i inrange(n)] explained = pd.DataFrame( {"explained_variance": pca.explained_variance_,"explained_variance_ratio": pca.explained_variance_ratio_,"cumulative": np.cumsum(pca.explained_variance_ratio_), }, index=cols, ) loadings = pd.DataFrame(pca.components_.T, index=z0.columns, columns=cols)return explained, loadings

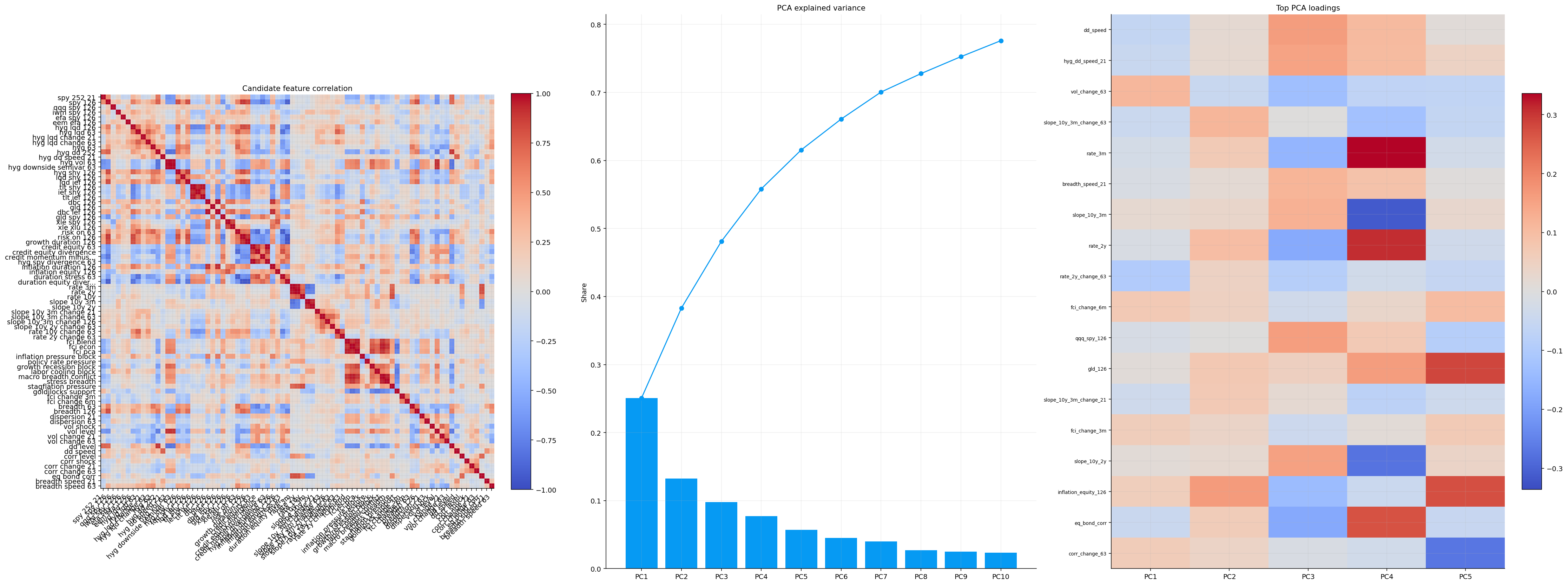

The first diagnostic output shows exactly the expected multicollinearity problem. In the full candidate set, many VIFs are infinite because several features are deterministic or near-deterministic combinations of others. This isn’t surprising. Relative-return features share the same assets, slope changes share the same Treasury yields, and macro blocks are intentionally related.

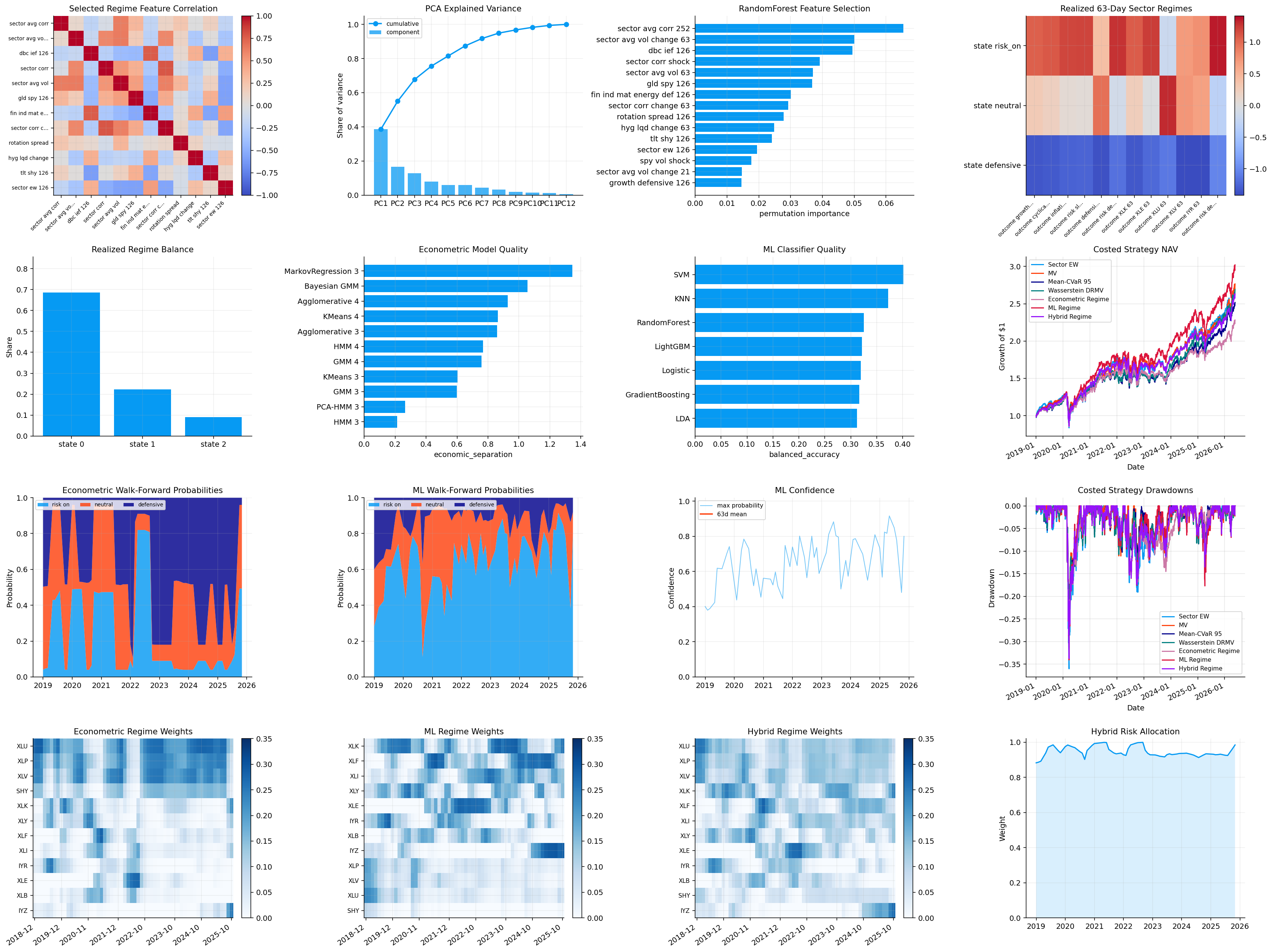

The PCA output on all 79 candidate features shows that PC1 explains about 25.1% of the variance, PC2 explains 13.2%, and the first 10 PCs explain about 77.6%. This means the feature set has strong common structure, but the regime information isn’t one-dimensional. A single “risk-on/risk-off” axis wouldn’t capture the full state. Rates, inflation, credit, equity leadership, correlation stress, and macro pressure all matter.

The correlation/PCA plot makes the same point visually. There are large blocks of correlated features, but there are also pockets of independent behavior. That is exactly the kind of setting where we shouldn’t feed every raw feature into every model. We first let a RandomForest selector identify variables that actually help predict the realized regime labels.

The VIF output looks extreme, but it is actually a useful warning. VIF, or variance inflation factor, asks how well one feature can be explained by the other features. For feature \(j\), we regress it on all other features and compute the \(R^2\) from that auxiliary regression:

\[

x_j = a + X_{-j}b + e

\]

Then:

\[

VIF_j = \frac{1}{1-R_j^2}

\]

If \(R_j^2\) is close to zero, the other features don’t explain feature \(j\), so \(VIF_j\) is close to 1. If \(R_j^2\) is close to 1, feature \(j\) is almost a linear combination of the others, so \(VIF_j\) becomes huge. If \(R_j^2=1\), the VIF is infinite.

In this project, infinite VIF is expected because many features are built from the same underlying assets. For example, tlt_shy_126, ief_shy_126, and tlt_ief_126 are mathematically related. If we know two of them, the third contains very little new information. Similarly, many macro blocks share inflation, policy, and financial-condition components. This doesn’t mean the features are useless. It means some models will over-count the same signal if we feed all features blindly.

The model impact depends on the method:

Linear models can get unstable coefficients because correlated variables compete with each other.

LDA needs covariance estimation, so correlated variables can make \(\Sigma^{-1}\) unstable unless we use shrinkage.

KMeans and KNN can over-weight repeated directions because distance counts every dimension.

GMM/HMM can overfit covariance structure if we use too flexible covariance matrices.

Tree ensembles can handle correlation better, but importance may be split across related features.

PCA gives a complementary view. Instead of asking whether each individual variable is redundant, PCA asks how many independent directions explain the feature space. For standardized feature vector \(Z_t\), PCA finds orthogonal directions \(v_1,\dots,v_p\) such that the first component explains maximum variance:

\[

PC_{1,t} = v_1^\top Z_t

\]

with:

\[

v_1 = \arg\max_{\|v\|=1} Var(v^\top Z_t)

\]

The next component is the highest-variance direction orthogonal to the first one. In matrix form, PCA is based on the eigen-decomposition of the correlation/covariance matrix:

\[

S = V\Lambda V^\top

\]

where \(V\) contains eigenvectors and \(\Lambda\) contains eigenvalues. The explained-variance ratio of component \(m\) is:

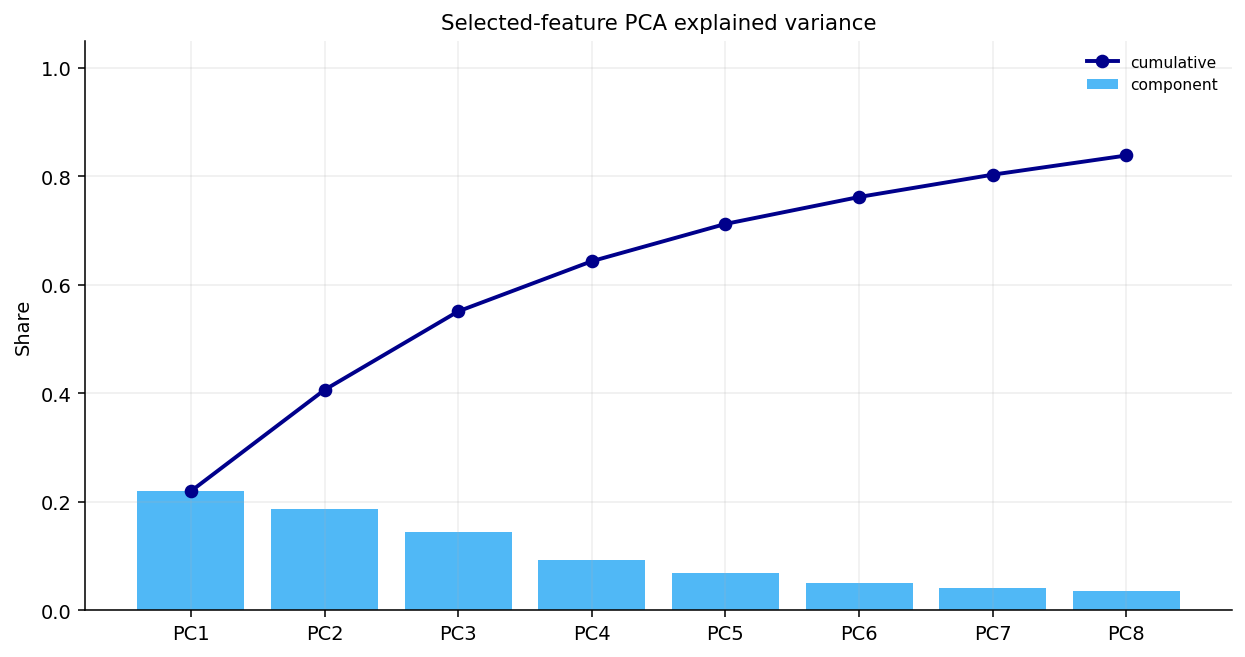

In the full candidate set, the first PC explains about 25% of the variance and the first 10 PCs explain about 78%. This tells us the features have strong common structure, but they aren’t reducible to a single risk factor. The selected set is cleaner: PC1 is about 22%, PC2 about 19%, and the first 8 PCs explain about 84%.

That is exactly the kind of structure that makes regime learning interesting. There is enough commonality for regimes to exist, but enough separate information for different models to disagree. If all features collapsed into one component, the project would only need a one-dimensional risk indicator. If every feature were independent noise, regime learning would fail. The actual result sits between those extremes: a structured but multi-dimensional market-state space.

The threshold avoids labeling tiny differences as meaningful regimes. If the risk sleeve beats the defensive sleeve by only a few basis points, that isn’t enough to call the market risk-on. A regime label should represent an economically meaningful future difference.

with wider thresholds of \(\pm 0.04\). This slower label is useful later when walk-forward classifiers need a more persistent target.

The target construction is one of the most important econometric choices in the project. A bad label can make even a strong model useless. Here the label isn’t “SPY up or down.” It is the future return difference between a risk sleeve and a defensive sleeve. That makes the target directly aligned with allocation.

The risk sleeve represents assets that usually benefit when investors accept growth, credit, and equity risk. The defensive sleeve represents assets that usually benefit when investors want duration, cash-like safety, or crisis hedges. The target spread:

is positive when risk assets beat defensive assets over the next 63 trading days. It is negative when defensive assets beat risk assets.

This target is better aligned with portfolio selection than a single-asset return label because a regime strategy is making a relative allocation decision. It doesn’t only care whether SPY is positive. It cares whether carrying risk beats holding defensive exposure. For example, SPY could rise 2% over a quarter, but if GLD and IEF rise 6%, a defensive allocation was still better. A regime model should capture that.

The neutral class is important because not every date deserves a strong risk-on or defensive label. Financial markets often sit in mixed environments where risky and defensive sleeves perform similarly. If we forced every observation into risk-on or defensive, the model would learn noisy boundaries around tiny return differences. The neutral label reduces that noise.

The 126-day label adds a slower horizon. A 63-day label captures quarter-like tactical conditions. A 126-day label captures a more persistent half-year macro regime. In practice, a strong regime model shouldn’t only recognize short-term market stress; it should also understand slower macro environments such as tightening financial conditions, persistent inflation pressure, or extended growth leadership.

Show code

def state_profile_local(features, labels, outcomes=None): lab = pd.Series(labels, name="state") parts = [features.copy()]if outcomes isnotNone: out = outcomes.copy()ifisinstance(out, pd.Series): out = out.to_frame() parts.append(out.add_prefix("outcome_")) z0 = pd.concat(parts + [lab], axis=1).replace([np.inf, -np.inf], np.nan).dropna(subset=["state"]) cols = [c for c in z0.columns if c !="state"] prof = z0.groupby("state")[cols].mean() prof.insert(0, "share", z0.groupby("state").size() /len(z0)) prof.insert(0, "observations", z0.groupby("state").size()) prof.index = prof.index.astype(int)return prof.sort_index()def sort_profile_states(profile): cols = [c for c in profile.columns if c notin {"observations", "share"}] z0 = profile[cols].astype(float) z0 = (z0 - z0.mean(axis=0)) / z0.std(axis=0, ddof=0).replace(0.0, np.nan) z0 = z0.fillna(0.0) score = pd.Series(0.0, index=profile.index)for col in z0.columns: name =str(col).lower()if"risk_defensive_spread"in name: score +=3.0* z0[col]continueifany(k in name for k in ["spy", "qqq", "iwm", "efa", "eem", "hyg", "risk_on", "breadth", "growth", "credit", "cyclical", "sector_ew"]): score += z0[col]ifany(k in name for k in ["vol", "corr", "dispersion"]): score -= z0[col]if"dd"in name or"drawdown"in name: score += z0[col]if"defensive_sleeve"in name: score -=0.5* z0[col]if"tlt"in name and"outcome"in name: score -=0.5* z0[col]return score.sort_values(ascending=False).index.astype(int).tolist()def remap_series(labels, order): mapping = {int(old): int(new) for new, old inenumerate(order)}return pd.Series(labels).map(mapping).astype(int)

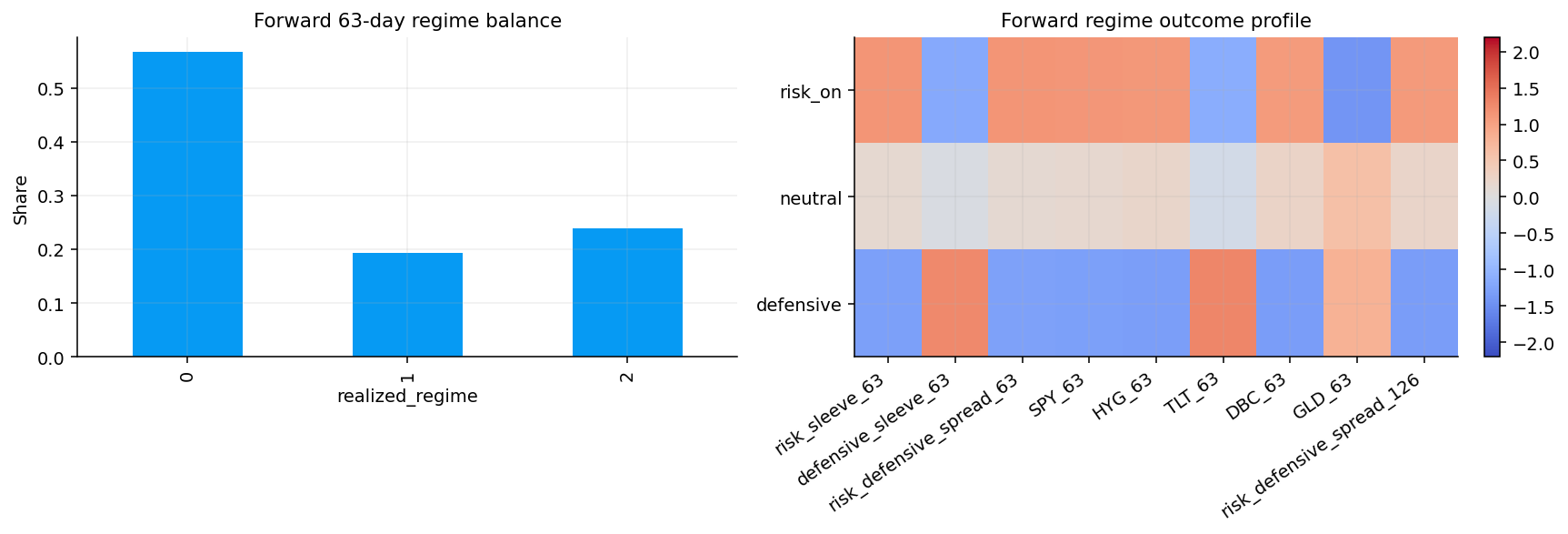

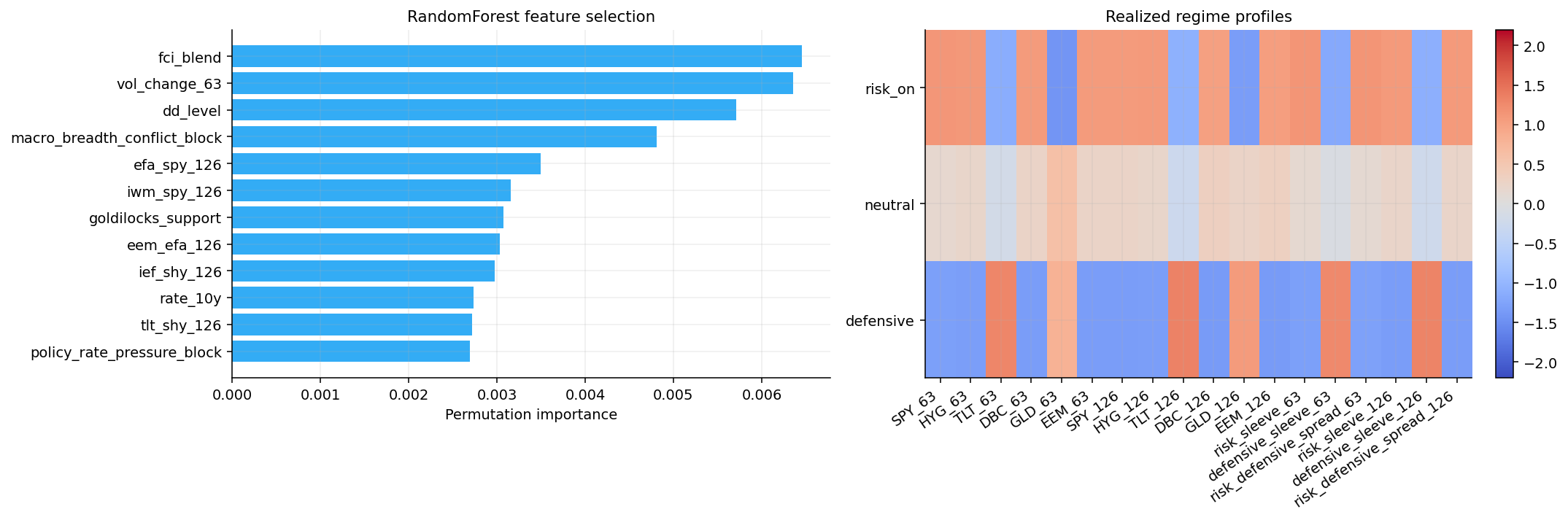

The forward regime profile confirms that the labels have real economic meaning. The risk-on class has strong positive 63-day and 126-day forward outcomes for SPY, HYG, DBC, EEM, and the risk sleeve. The defensive class has negative forward SPY and EEM outcomes, strong TLT and GLD outcomes, and a negative risk-defensive spread. The neutral class sits between those two.

The class balance isn’t perfectly equal. Risk-on is the largest class, neutral is smaller, and defensive is meaningful but less frequent. This is normal for market regimes. Most days aren’t crisis days. But this creates an ML problem: raw accuracy can reward a model that mostly predicts risk-on. That is why balanced accuracy and macro F1 matter later.

This punishes models that perform well only on one class. In finance, that is crucial because the rare class is often the one we care about most. A model that misses defensive periods can still have acceptable accuracy, but it can fail as a portfolio tool.

Show code

fig, axes = plt.subplots(1, 2, figsize=(12.5, 4.3))y.value_counts(normalize=True).sort_index().plot(kind="bar", ax=axes[0])axes[0].set_title("Forward 63-day regime balance")axes[0].set_ylabel("Share")profile_cols = [ c for c in ["outcome_risk_sleeve_63","outcome_defensive_sleeve_63","outcome_risk_defensive_spread_63","outcome_SPY_63","outcome_HYG_63","outcome_TLT_63","outcome_DBC_63","outcome_GLD_63","outcome_risk_defensive_spread_126", ]if c in future_profile.columns]profile_z = future_profile[profile_cols]profile_z = (profile_z - profile_z.mean()) / profile_z.std(ddof=0).replace(0, np.nan)im = axes[1].imshow(profile_z.fillna(0.0).values, aspect="auto", cmap="coolwarm", vmin=-2.2, vmax=2.2)axes[1].set_yticks(range(len(profile_z.index)))axes[1].set_yticklabels(profile_z.index)axes[1].set_xticks(range(len(profile_z.columns)))axes[1].set_xticklabels([c.replace("outcome_", "") for c in profile_z.columns], rotation=35, ha="right")axes[1].set_title("Forward regime outcome profile")fig.colorbar(im, ax=axes[1], fraction=0.046, pad=0.04)plt.tight_layout()plt.show()

The class distribution also teaches an important ML lesson. Risk-on observations are the largest class because most market days aren’t stress days. Defensive regimes are less frequent, but they matter disproportionately for portfolio outcomes because they usually coincide with large drawdowns or rapid rotations.

This is why raw accuracy can be misleading. Suppose risk-on is 57% of observations. A lazy model that always predicts risk-on could get decent raw accuracy while being useless in crises. In a portfolio context, missing the defensive class is more costly than missing a few neutral periods.

Balanced accuracy fixes part of that problem by averaging recall across classes:

where \(TP_k\) is the number of true positives for class \(k\) and \(FN_k\) is the number of missed observations from class \(k\). This metric gives equal importance to risk-on, neutral, and defensive regimes even if they aren’t equally common.

Precision asks whether predicted class \(k\) observations really belong to class \(k\). Recall asks whether the model finds the actual class \(k\) observations. In regime switching, both matter. If the model predicts defensive too often, the portfolio may sit in safe assets and miss rallies. If it predicts defensive too rarely, it may stay risk-on into drawdowns. The metrics help us detect those two different errors.

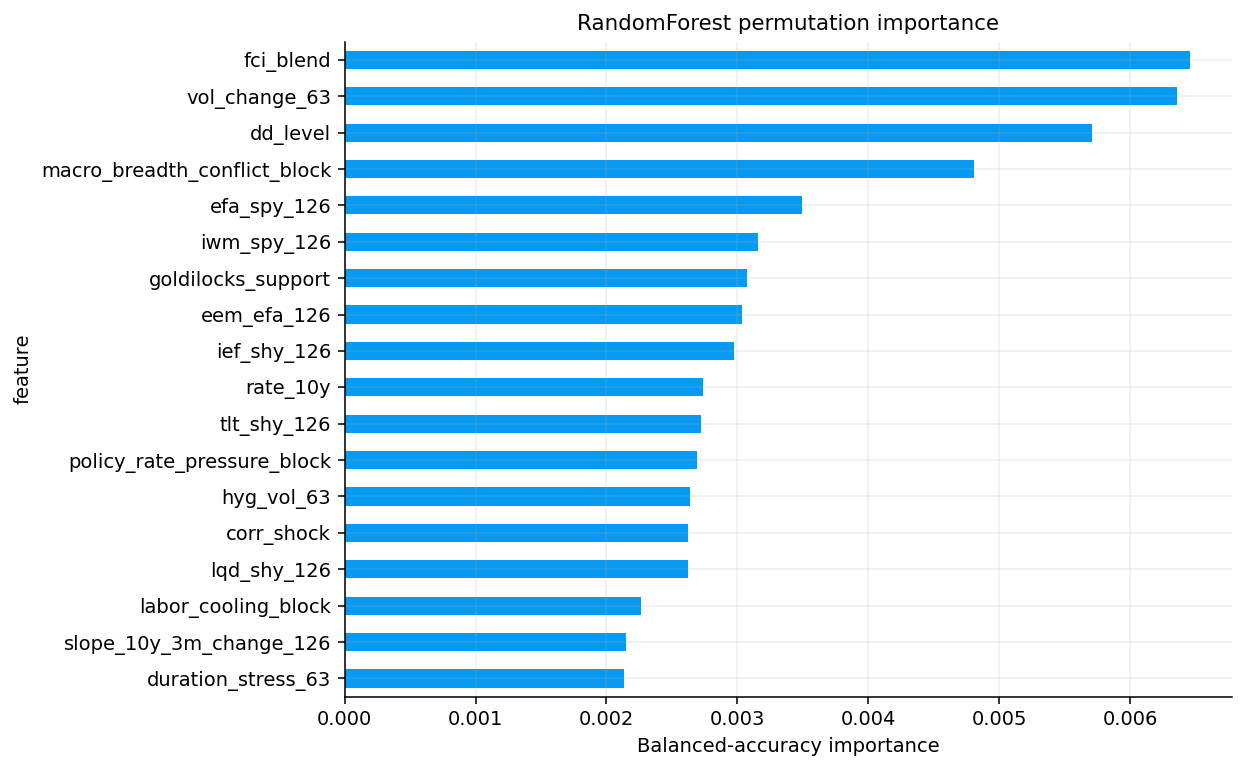

The RandomForest importance table selects features that are economically meaningful, not just statistically convenient. The top features include:

fci_blend, linking the regime model to the macro/financial-condition framework from Project 12.

vol_change_63, showing that rising volatility carries regime information.

dd_level, because deep drawdowns often separate defensive states from normal volatility.

macro_breadth_conflict_block, which captures disagreement between macro stress blocks and market breadth.

international and cross-asset relative returns such as efa_spy_126, iwm_spy_126, and eem_efa_126.

duration and policy features such as ief_shy_126, rate_10y, tlt_shy_126, and policy_rate_pressure_block.

credit and downside risk features such as hyg_vol_63, hyg_downside_semivar_63, and hyg_lqd_change_63.

This is a good feature-selection result because it doesn’t collapse into one category. The selected set includes macro pressure, volatility, drawdown, international leadership, credit, duration, and inflation. That gives the regime models enough information to distinguish:

equity-led risk-on,

credit-supported risk-on,

neutral defensive yield environments,

inflation-rate stress,

and broad market stress.

After selection, we transform features with an expanding z-score:

where \(\bar{x}_{t-1,j}\) and \(s_{t-1,j}\) are computed only from observations before date \(t\). This avoids lookahead. The clip at \(\pm 4\) prevents extreme crisis observations from dominating the scale forever.

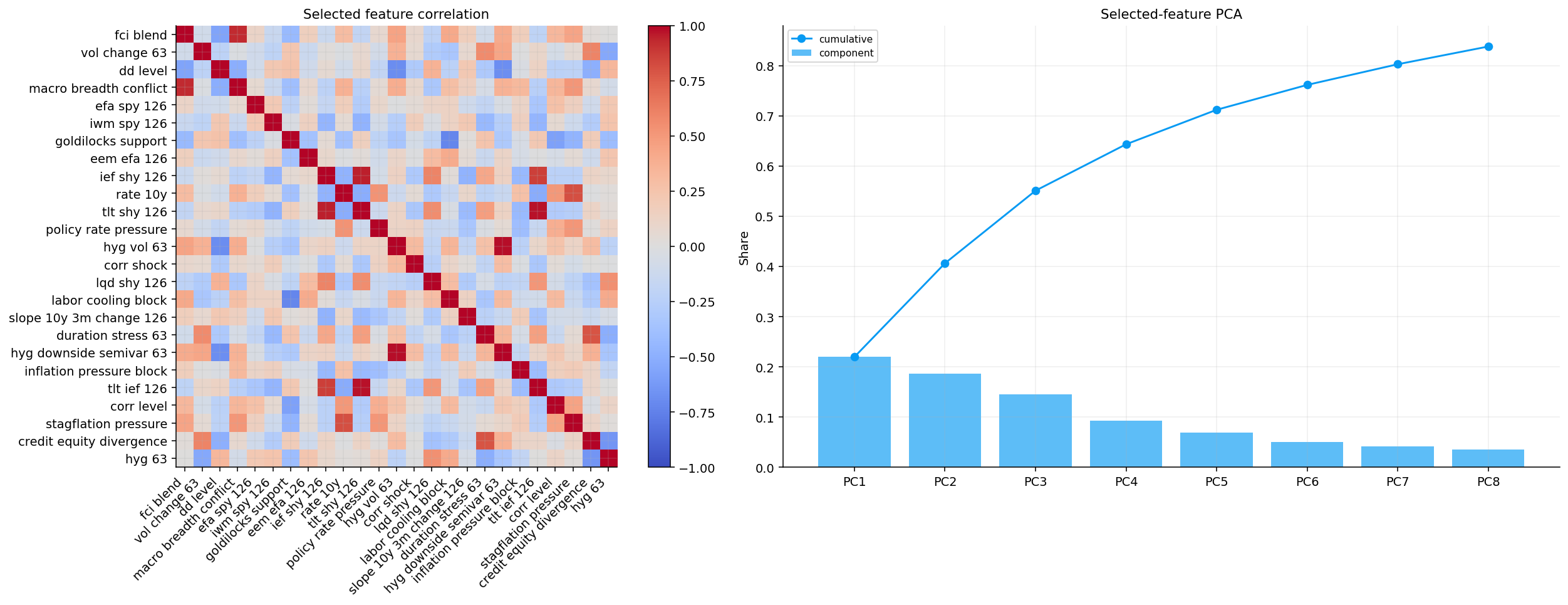

The selected-feature VIF table still shows high VIF for duration features, especially tlt_shy_126, tlt_ief_126, and ief_shy_126. This is expected because those spreads share assets. The model doesn’t remove all redundancy. Instead, it keeps economically useful redundancy and relies on methods like PCA-HMM, tree models, regularization, and validation to handle it.

RandomForest feature selection is used as a pragmatic filter, not as the final truth about causality. The idea is to ask: if a nonlinear tree ensemble tries to predict future regime labels, which features actually help out of sample?

Permutation importance is especially useful because it measures the loss of predictive performance when one feature is randomly shuffled. If feature \(j\) is important, shuffling it breaks its relationship with the target and model performance drops. If shuffling it barely changes performance, the feature may be redundant or uninformative.

where \(X^{\pi_j}\) is the same feature matrix after randomly permuting column \(j\). The bigger \(I_j\) is, the more the model depended on that feature.

The selected features make economic sense. fci_blend is the highest-ranked feature, which means the macro/financial-condition system from Project 12 carries information about future cross-asset regimes. vol_change_63 and dd_level are also near the top, which means recent volatility acceleration and drawdown damage matter. macro_breadth_conflict_block is important because markets often become vulnerable when price breadth and macro conditions disagree. Relative equity features such as efa_spy_126, iwm_spy_126, and eem_efa_126 show whether leadership is U.S.-centric, small-cap-led, or international/EM-led.

This feature selection stage also helps with interpretability. Instead of saying “the model saw 79 variables,” we can say the final regime models are mostly learning from:

financial conditions,

volatility acceleration,

drawdown pressure,

macro-market disagreement,

international leadership,

duration and policy pressure,

credit downside risk,

and inflation/stagflation blocks.

That is a coherent economic state space. It gives the model a chance to separate regimes in ways that match market intuition.

The selected-feature PCA is cleaner than the full candidate PCA. PC1 explains about 22.0%, PC2 about 18.7%, and the first 8 components explain about 83.8%. So the selected feature set is still strongly structured, but it is less bloated than the 79-feature candidate set.

This matters for the models:

KMeans and GMM can be sensitive to correlated dimensions because distance and Gaussian density can over-count repeated information.

PCA-HMM deliberately compresses features before fitting the sequence model.

LDA benefits from shrinkage because class covariance estimates can become unstable when predictors are correlated.

RandomForest and boosting can handle correlated features better, but importance can be split across related variables.

SVM and KNN depend on geometry, so scaling and redundancy strongly affect the margin and nearest-neighbor structure.

This diagnostic stage isn’t just a plot-making step. It tells us what kind of model risk each method faces before we compare the results.

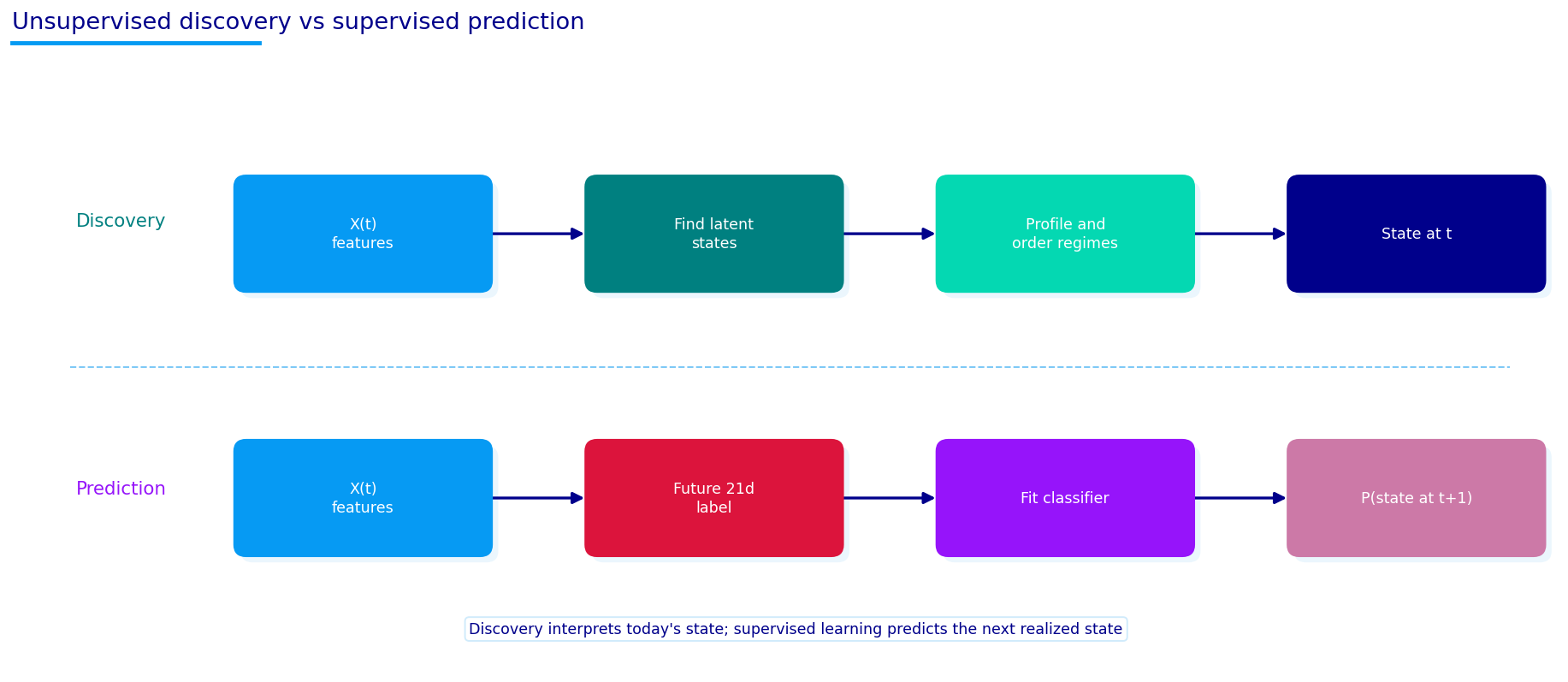

6) Unsupervised Learning for Regime Discovery

We now split the problem into two learning styles.

Unsupervised learning sees only \(X_t\). It tries to discover structure in the feature space without using future labels. The output is a state assignment:

\[

\hat{S}_t = g(X_t)

\]

The model doesn’t know the future risk-defensive spread. After fitting, we profile each discovered state by looking at its realized future outcomes. Then we order the states as risk-on, neutral, or defensive.

Supervised learning sees pairs \((X_t, Y_t)\) during training. It directly learns:

\[

P(Y_t = k \mid X_t)

\]

and evaluates whether those probabilities predict future regimes.

The teaching plot in this section shows the difference cleanly. Discovery takes today’s features and finds latent states. Prediction uses future labels during training and then predicts the next realized state.

For finance, both styles are useful.

Unsupervised models are closer to econometric regime discovery. They ask: “What clusters or latent states exist in the market data?” Supervised models are closer to forecasting. They ask: “Given today’s features, which future sleeve outcome is most likely?”

We include both because regime modeling has two separate goals:

Interpretation, which benefits from unsupervised and Markov-style models.

Prediction, which benefits from supervised classifiers and explicit out-of-sample labels.

Unsupervised learning is the discovery layer. It doesn’t use the forward regime labels when fitting the states. It only sees the feature matrix \(X_t\) and tries to find structure. Afterward, we evaluate whether the discovered states correspond to economically meaningful future outcomes.

This gives us a useful separation:

Discovery: identify clusters or latent states from today’s market conditions.

Economic mapping: inspect future returns conditional on those states.

Portfolio usefulness: test whether the states produce useful weights after costs.

In notation, unsupervised models estimate:

\[

\hat{S}_t = g(X_t)

\]

or, for probabilistic models:

\[

\hat{p}_{t,k} = P(S_t=k \mid X_t)

\]

without directly using \(Y_t\) during fitting. That makes them appealing for regime discovery because they can find states we did not label by hand. The danger is that a statistically clean cluster can still be financially weak. A cluster might separate high volatility from low volatility, but if both clusters have similar future risk-defensive spreads, the separation doesn’t help allocation.

So every unsupervised model is judged on both statistical and economic criteria:

Silhouette: are observations geometrically well separated?

Minimum state share: is every state large enough to matter?

Average duration: are states persistent enough for monthly allocation?

Transitions per year: is the state path too jumpy?

Posterior confidence: are probabilities decisive or diffuse?

Economic separation: do states actually differ in future returns?

This is why the output table is more important than the individual model label. We aren’t looking for a pretty clustering result. We are looking for a state representation that can support a real portfolio policy.

Update step: replace each centroid with the mean of the points assigned to it.

\[

\mu_k = \frac{1}{N_k}\sum_{t:c_t=k}X_t

\]

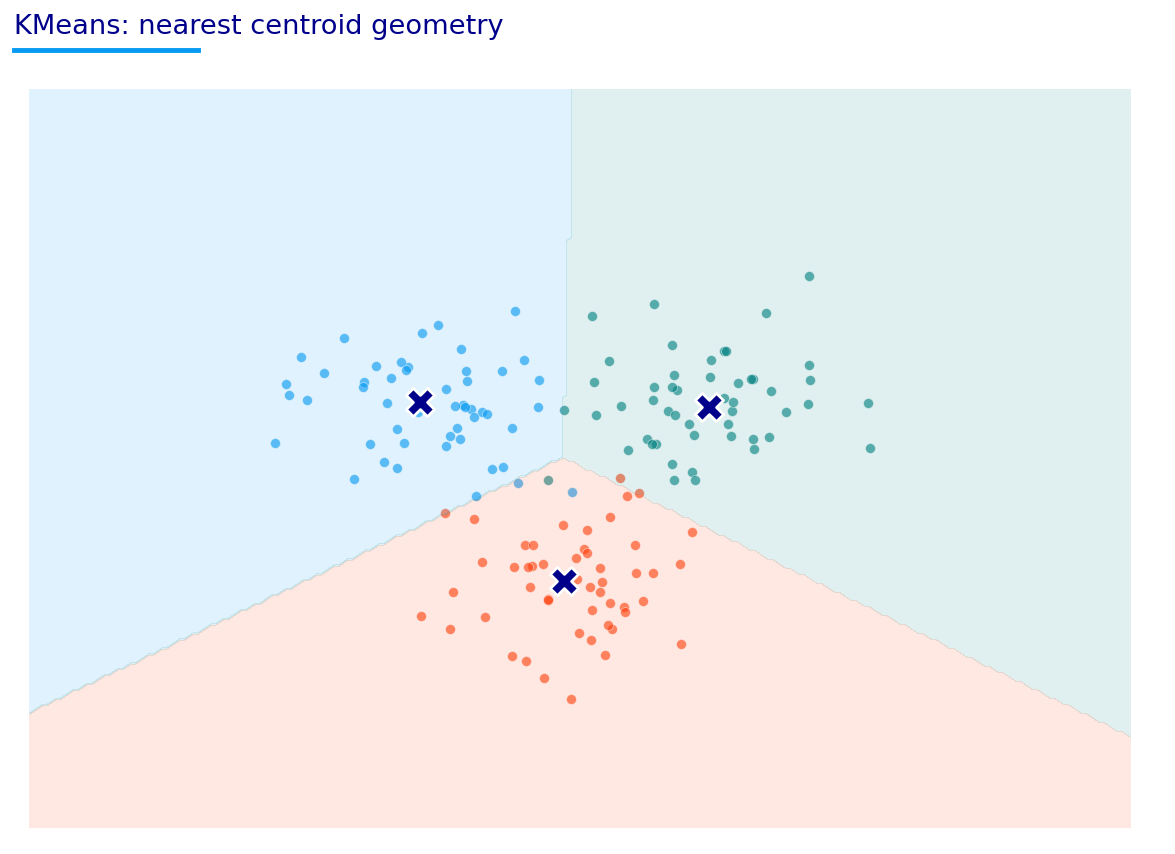

The geometry plot shows the result in a two-dimensional teaching example. Each colored region is the area closest to one centroid. The boundaries are straight lines because the model is using Euclidean distance. That makes KMeans easy to understand, but it also creates limitations. Regime clusters in finance are rarely spherical, equally sized, or separated by straight boundaries.

For example, a defensive regime may not be a compact cloud. It can include the COVID crash, the 2022 inflation-rate shock, and smaller volatility shocks. Those episodes may share “stress” behavior, but they don’t need to occupy one neat ball in feature space. KMeans can still be useful as a baseline, but we shouldn’t expect it to be the most realistic regime model.

The KMeans objective is simple but powerful. For \(K\) clusters, it chooses centroids \(\mu_1,\dots,\mu_K\) and assignments \(c_t\) to minimize within-cluster squared distance:

Each centroid is the average feature vector of observations assigned to that cluster. The algorithm alternates between:

assigning each observation to the nearest centroid,

recomputing each centroid as the mean of assigned observations.

The financial interpretation is that each centroid becomes a typical market environment. One centroid might represent calm risk-on: positive breadth, low volatility, healthy credit, and normal financial conditions. Another might represent stress: negative breadth, rising volatility, weak credit, and tight FCI. A third might represent mixed conditions.

The main weakness is the geometry assumption. KMeans works best when clusters are roughly spherical and similar in size after scaling. Financial regimes rarely behave like clean spherical clusters. Stress states can be smaller, more extreme, and more stretched. Neutral states can be broad and overlapping. Because KMeans uses hard assignments, it also doesn’t express uncertainty. A date just on the boundary is treated as fully belonging to one state.

The teaching plot helps here: cluster boundaries are straight Voronoi regions around centroids. In a real market-state space, that means the model assigns regimes based on nearest average environment. This is clear and interpretable, but it can miss nonlinear or overlapping regimes.

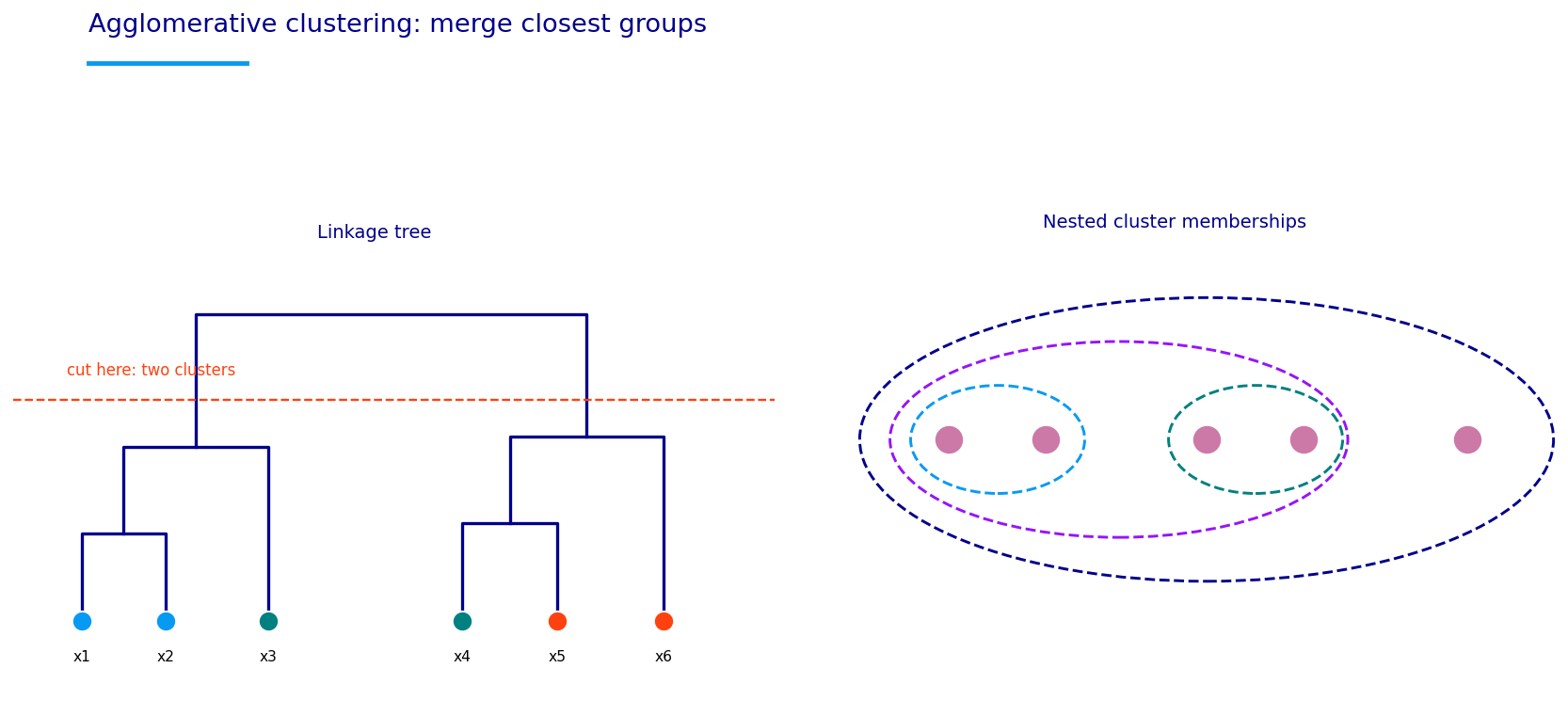

Agglomerative clustering builds a hierarchy. It starts with every observation as its own cluster and then repeatedly merges the closest groups. The teaching diagram shows this as a dendrogram. Cutting the tree at a chosen height gives the number of clusters.

With Ward linkage, the merge cost between two clusters \(A\) and \(B\) is:

\(\bar{X}_A\) and \(\bar{X}_B\) are cluster centroids.

Ward linkage tries to merge clusters in a way that increases within-cluster variance as little as possible. That makes it somewhat similar to KMeans, but the hierarchical path is different. Once two observations are merged, they stay together.

The useful part for market regimes is the nested structure. A broad stress group may contain subgroups: credit stress, rate stress, and equity crash. Agglomerative clustering can reveal that hierarchy. The limitation is that it still doesn’t model sequence dynamics. It doesn’t know that regimes tend to persist over time.

Agglomerative clustering builds the state structure from the bottom up. At the start, every observation is its own cluster. Then the algorithm repeatedly merges the closest clusters until only \(K\) clusters remain. The merge rule depends on the linkage method. A common choice is Ward linkage, which merges clusters that create the smallest increase in within-cluster variance.

If \(A\) and \(B\) are two clusters, Ward linkage chooses the merge that minimizes the increase in:

\[

W = \sum_{k=1}^{K}\sum_{t\in C_k}\left\|X_t-\bar{X}_{C_k}\right\|_2^2

\]

This produces a hierarchical tree, or dendrogram. The tree diagram in we is important because it shows that clustering doesn’t have to be a flat one-step assignment. The same data can have nested structure. For example, the top-level split might separate stress from normal markets. Inside normal markets, another split might separate growth leadership from reflation leadership. Inside stress, another split might separate inflation stress from recession stress.

In portfolio terms, hierarchy is useful because regimes often have nested meanings. A two-state model might say “risk-on vs risk-off.” A three-state model might add neutral. A four-state model might split defensive into “duration works” and “duration fails.” Agglomerative clustering helps us see whether such nested structure exists.

The smoother state duration in the output suggests that hierarchical clusters are less jumpy than KMeans here. That is good for turnover, but it also means the model may be slow to detect sudden transitions. This tradeoff appears repeatedly in regime modeling: fast models adapt quickly but can whipsaw; slow models are stable but can lag.

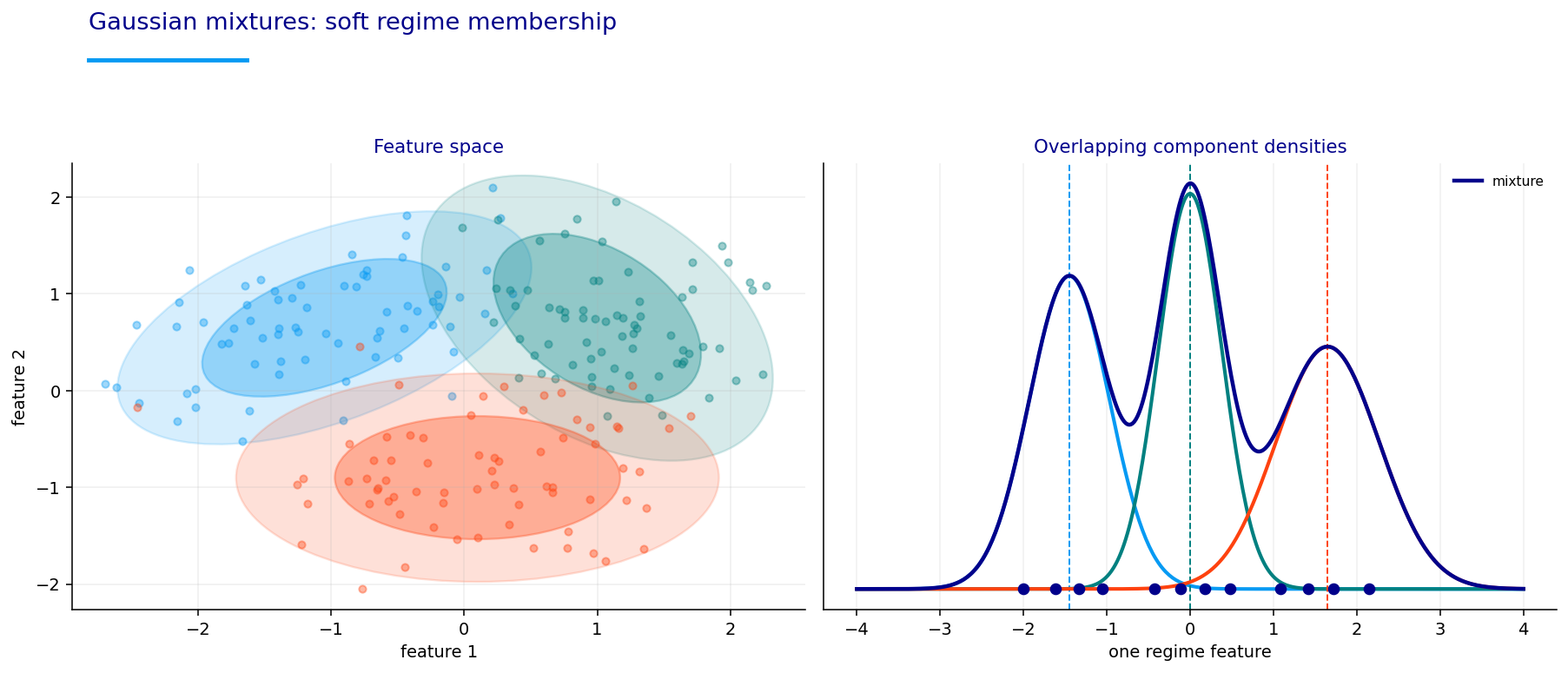

KMeans assigns each observation to one nearest centroid. A Gaussian Mixture Model (GMM) is more flexible. It assumes the feature distribution is a weighted sum of Gaussian components:

This is a soft membership probability. Instead of saying “today is exactly state 1,” the model can say today’s feature vector is 70% close to risk-on, 20% close to neutral, and 10% close to defensive.

GMM parameters are usually estimated by expectation-maximization (EM). The EM logic is:

E-step: compute responsibilities \(\gamma_{t,k}\) using current parameters.

M-step: update \(\pi_k\), \(\mu_k\), and \(\Sigma_k\) using those responsibilities.

The mixture plot shows why this is more realistic than KMeans. The component ellipses can overlap. Financial states often overlap because the transition from expansion to stress is gradual. GMM captures that uncertainty with probabilities.

A Gaussian mixture model adds probability to clustering. Instead of saying each date belongs entirely to one cluster, it says each date has a probability of coming from each component:

This soft assignment is more useful for portfolios than KMeans hard labels. If a date is 55% risk-on and 45% neutral, the allocation can be blended. It doesn’t need to jump fully from one sleeve to another.

The diagonal covariance choice is conservative. A full covariance matrix for state \(k\) has \(p(p+1)/2\) parameters, where \(p\) is the number of features. With many correlated features and a limited number of stress observations, that can overfit badly. A diagonal covariance only estimates one variance per feature inside each state:

This assumes conditional independence across features within each state. That assumption isn’t literally true in markets, but it can be a good regularization choice. It lets each state have different feature volatility without trying to estimate every cross-feature covariance.

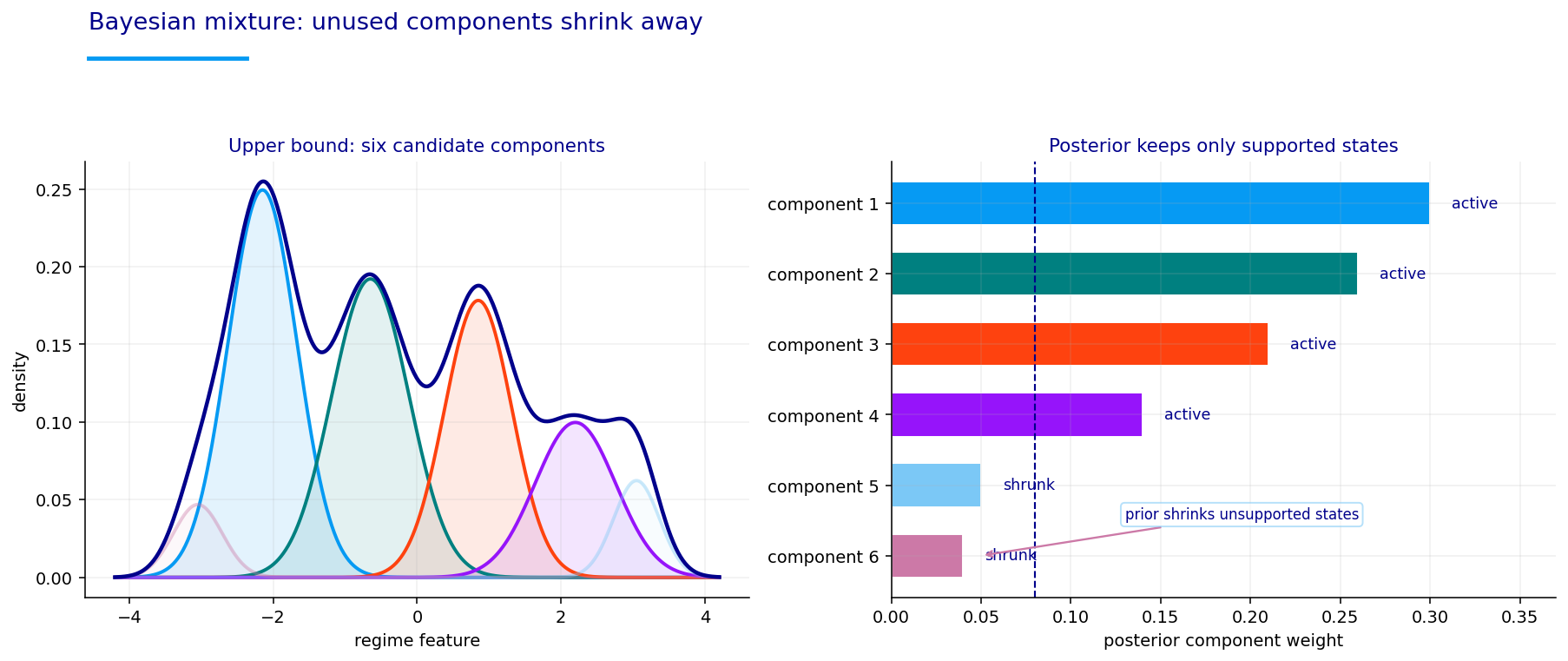

The Bayesian mixture goes one step further by making component weights uncertain. A Dirichlet prior gives the model a way to shrink unused components:

If the data doesn’t support a component, its posterior weight can become small. This is useful because we often don’t know the right number of regimes. Financial markets may have two dominant regimes in one era, four in another, and several small transition states around crises. A Bayesian mixture can start with more possible components and let weak ones fade.

The main implementation uses diagonal covariance for the GMM variants. A diagonal covariance means each state has its own variance per feature, but it doesn’t estimate all feature-to-feature covariance inside each component:

This is a practical design choice. With many correlated features and limited regime history, a full covariance GMM can overfit badly. Diagonal covariance sacrifices some flexibility but makes the density estimate more stable.

The Bayesian Gaussian mixture adds a prior over component weights. In we, we start with an upper bound of six candidate components, but the prior lets weak components shrink away. This is useful when we don’t know the right number of states.

If the prior concentration is small, the posterior can push unsupported components toward very low weights. In a Dirichlet-process-style mixture, this acts like “let the data decide how many components are active.”

The teaching plot shows six possible component densities, but only the supported components remain meaningfully weighted. This is helpful because market data may have a dominant risk-on regime, a neutral regime, a stress regime, and maybe a few smaller transition states. We don’t want to force every candidate component to matter.

Unsupervised labels are arbitrary. If a KMeans model returns labels 0, 1, and 2, those numbers don’t automatically mean risk-on, neutral, and defensive. The model only knows geometry. It doesn’t know finance.

So after fitting, we build an economic profile for each discovered state. For state \(k\), the profile is:

Then we order states by economic meaning. A state with high future risk-sleeve return and high risk-defensive spread becomes risk-on. A state with low future risky returns, better defensive returns, and negative spread becomes defensive. A state in the middle becomes neutral.

This step is crucial. Without economic ordering, a cluster label could flip between runs. The model could call risk-on “cluster 2” in one run and “cluster 0” in another. Portfolio rules need stable names, so we remap discovered states into a consistent economic order.

The profile table is also a guard against fake regimes. If two clusters have very similar future outcomes, they may be statistically separated but financially unimportant. A good regime isn’t only a pretty cluster. It should correspond to different future asset behavior.

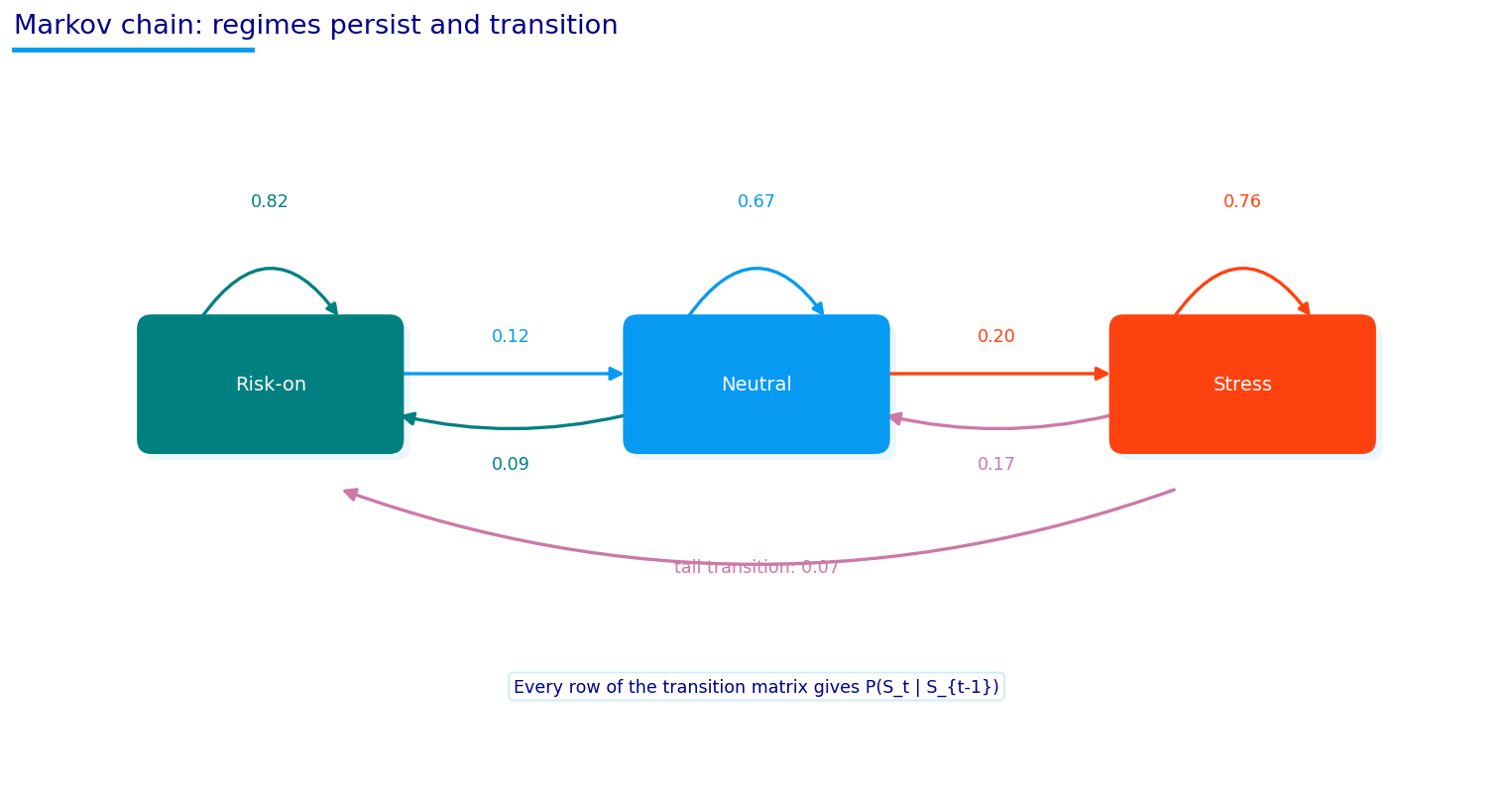

7) Markov Chains and State Persistence

The next step is the stochastic-process part of the project. A regime process is a sequence:

\[

S_1, S_2, \dots, S_T

\]

where each \(S_t\) takes one of a small number of states, such as risk-on, neutral, or defensive.

A Markov chain assumes the next state depends on the current state, not the full past path:

The diagonal entries are persistence probabilities. If \(A_{00}=0.82\), then a risk-on day has an 82% probability of being followed by another risk-on day. The expected duration of state \(i\) is:

\[

E[D_i] = \frac{1}{1-A_{ii}}

\]

So if a state has a self-transition probability of 0.82, its expected duration is about:

\[

E[D] = \frac{1}{1-0.82} \approx 5.56

\]

observations, under the geometric-duration assumption. If the self-transition probability is 0.98, the expected duration becomes 50 observations. This is why small changes in diagonal probabilities can create much smoother regime paths.

Show code

fig, ax = markov_chain()plt.show()

The Markov chain diagram in we is a teaching simplification. It shows risk-on, neutral, and stress states with self-transition probabilities and cross-transition probabilities. The point is that regimes usually persist. A stress state doesn’t usually appear for one isolated day and vanish forever. A risk-on trend can persist for months. A neutral state can act as a transition zone.

We can update a state distribution forward through time using:

\[

p_t = p_{t-1}A

\]

where \(p_t\) is a row vector of state probabilities. If today’s distribution is \(p_t = [0.70, 0.20, 0.10]\), and \(A\) has strong diagonal probabilities, tomorrow’s distribution will still be mostly risk-on unless the observed features provide strong contrary evidence.

This persistence is financially useful because it reduces whipsaw. A clustering model can flip states whenever the feature vector crosses a boundary. A Markov model adds inertia. It says the market can change regimes, but the prior probability of staying in the same state is usually high.

A Markov chain is the first true stochastic-process model in the project. It models a sequence of states:

\[

S_1,S_2,\dots,S_T

\]

where each \(S_t\) belongs to a finite state space such as:

The diagonal entries are persistence probabilities. If \(A_{00}=0.95\), a risk-on state tends to remain risk-on. If \(A_{22}=0.80\), defensive states also persist, but less strongly. Off-diagonal entries describe transitions. For example, \(A_{02}\) is the probability of jumping from risk-on directly to defensive.

A state distribution evolves by multiplication:

\[

p_{t+1} = p_t A

\]

If today’s probability vector is \(p_t=[0.70,0.20,0.10]\), then tomorrow’s prior state distribution is the weighted average of the transition rows. This is the “state inertia” that clustering lacks.

The \(n\)-step transition matrix is:

\[

A^n = \underbrace{A A \cdots A}_{n\text{ times}}

\]

The entry \((A^n)_{ij}\) gives the probability of being in state \(j\) after \(n\) steps if we start in state \(i\). This is useful for thinking about multi-month regimes. If the strategy rebalances monthly, we caren’t only about tomorrow’s state but whether a state is likely to persist long enough to justify a portfolio tilt.

The expected duration of state \(i\) is approximately:

\[

E[D_i] = \frac{1}{1-A_{ii}}

\]

If \(A_{ii}=0.90\), expected duration is about 10 periods. If \(A_{ii}=0.50\), expected duration is only 2 periods. This formula comes from the geometric distribution: if the probability of leaving the state each period is \(1-A_{ii}\), the expected waiting time before leaving is the inverse of that exit probability.

This duration formula is one of the cleanest links between stochastic-process math and trading. A model with very low state duration creates high turnover and unstable allocations. A model with very high duration may fail to adapt. The transition matrix lets us quantify that tradeoff rather than describe it vaguely.

7.1 Markov Regression

The Markov regression model in this project is a regime-switching time-series model applied to the global equal-weight return series. Instead of clustering a multivariate feature vector, it models a univariate return process whose mean and variance can switch by regime.

A simple Markov-switching regression can be written as:

\(\sigma_{S_t}^2\) is the regime-specific variance,

\(S_t\) follows a Markov chain.

The likelihood must sum over unobserved state paths. Directly summing over all possible paths would be impossible for long time series because there are \(K^T\) possible state sequences. Instead, the Hamilton filter updates state probabilities recursively.

The filtered probability is:

\[

P(S_t=k \mid y_1,\dots,y_t)

\]

It combines two pieces:

the predicted probability from yesterday’s state distribution and the transition matrix,

the likelihood of today’s return under each regime.

For a regime with low volatility and positive mean, a calm positive return gets high likelihood. For a high-volatility stress regime, a large negative return gets higher likelihood. The filter updates the posterior regime probabilities accordingly.

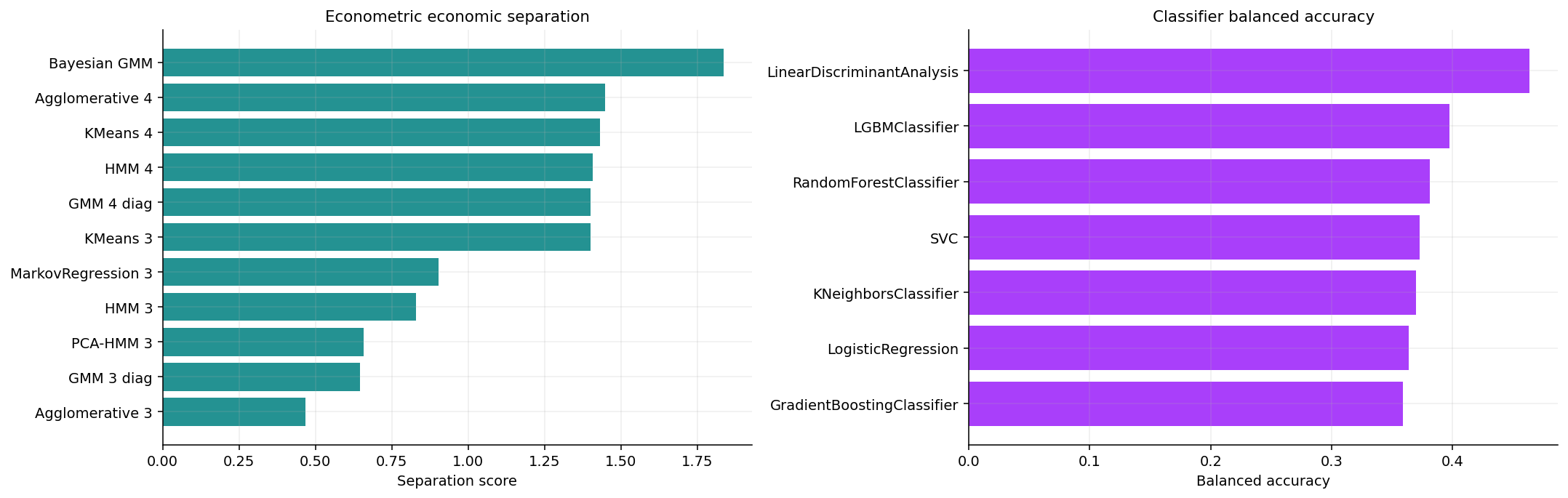

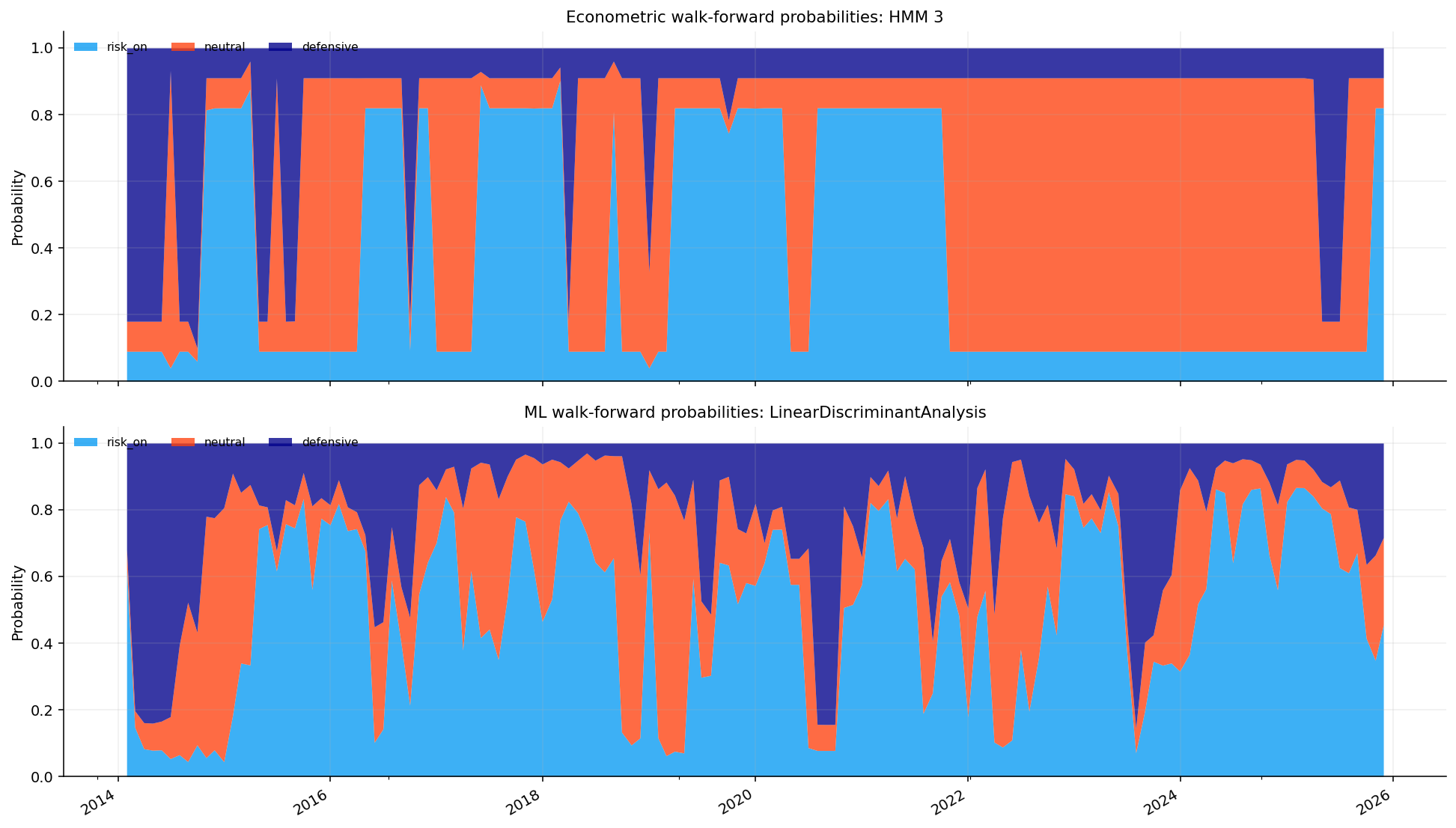

The MarkovRegression output has strong likelihood diagnostics because it is directly a time-series likelihood model, but its economic separation in the main table isn’t the highest. That makes sense. It sees one return series, while the feature-based models see macro, credit, rates, commodities, and internal market structure.

The transition matrix gives several diagnostics that are useful beyond the basic state plot.

Stationary distribution. If a Markov chain is stable and ergodic, it has a long-run distribution \(\pi\) satisfying:

\[

\pi = \pi A

\]

with:

\[

\sum_{k=1}^{K}\pi_k = 1

\]

This means that if we keep applying the transition matrix for a very long time, the state distribution tends toward \(\pi\) regardless of the starting state. In finance, the stationary distribution can be interpreted as the model’s long-run regime mix. If \(\pi_{\text{risk-on}}\) is very high, the model believes risk-on is the dominant long-run environment. If \(\pi_{\text{defensive}}\) is too small, the model may underrepresent crises.

A stationary distribution isn’t a forecast that the future must match the historical regime mix. It is a diagnostic of the fitted transition structure. If the stationary distribution says the defensive state is basically impossible, but the realized sample contains meaningful stress periods, the transition model may be too optimistic.

Expected duration. The formula:

\[

E[D_i]=\frac{1}{1-A_{ii}}

\]

turns transition probabilities into a trading concept. If the state is expected to last only a few days, monthly allocation won’t benefit much from detecting it. If the state lasts several months, it can support a regime sleeve.

For example, if a defensive state has \(A_{22}=0.96\), then:

\[

E[D_2]=\frac{1}{1-0.96}=25

\]

If the time unit is daily observations, this is roughly one trading month. If the model is fit on monthly observations, the same number would mean 25 months, which would be far too persistent. So duration must always be interpreted together with the observation frequency.

Transition asymmetry. Market regimes are often asymmetric. Risk-on may drift slowly into neutral before turning defensive. Defensive states may recover quickly after policy support or liquidity intervention. This asymmetry appears in off-diagonal transition probabilities:

A chain with high \(A_{\text{risk-on},\text{defensive}}\) allows direct crash transitions. A chain with low direct transition but high risk-on-to-neutral and neutral-to-defensive movement implies deterioration tends to pass through a transition state.

For portfolio construction, the transition path matters. If the model often moves through neutral before defensive, the portfolio can gradually reduce risk. If direct risk-on-to-defensive transitions are common, the strategy needs faster risk controls.

Regime entropy. A Markov or HMM probability vector can be summarized by entropy:

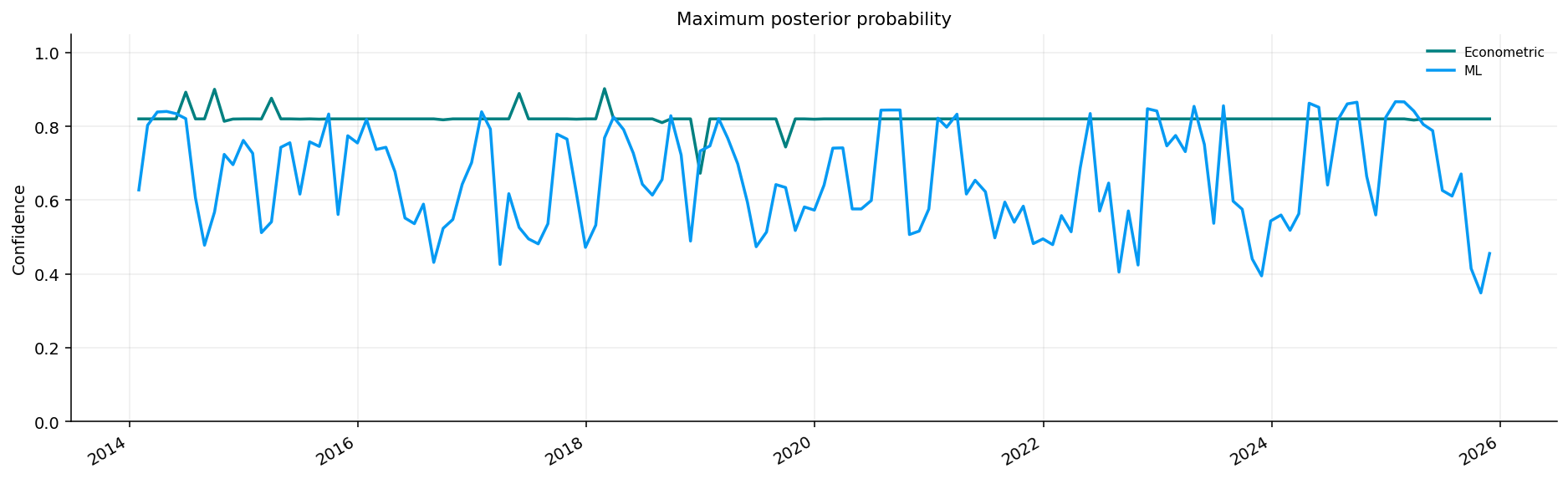

Entropy is close to 0 when one state dominates and close to 1 when probabilities are spread evenly. This becomes a risk-control input later because uncertain probabilities shouldn’t create extreme allocations. A confident 80% defensive probability and a mixed 35/35/30 probability have different portfolio meanings even if defensive is the largest class in both.

This is why Markov models fit portfolio work so naturally. They produce probabilities, persistence, duration, transition risk, and uncertainty. Those are exactly the objects a portfolio layer can use.

A small numerical Markov example makes the persistence idea concrete. Suppose the transition matrix is:

The first row says a risk-on state stays risk-on with 92% probability, moves to neutral with 7%, and jumps directly to defensive with 1%. The third row says a defensive state stays defensive with 75%, recovers to neutral with 20%, and jumps back to risk-on with 5%.

Even before observing tomorrow’s features, the model is still mostly risk-on because the transition matrix has persistence. But defensive probability rises slightly from 5% to 6.8% because there is some chance of deterioration through neutral or direct transition.

Now suppose tomorrow’s features show a strong volatility shock and weak credit. The HMM emission likelihood for the defensive state rises, and the filtering update can move the defensive probability much more. The transition matrix gives inertia, while the emission likelihood gives evidence. The final probability is the balance between both.

This is the whole appeal of Markov regime modeling in finance. We don’t want the model to forget yesterday’s regime instantly, and we don’t want it to ignore today’s new stress evidence either.

This means each hidden state has its own average feature profile and feature volatility. A risk-on state might have high breadth, positive credit momentum, lower volatility pressure, and positive equity leadership. A defensive state might have negative breadth, higher drawdown, high volatility shock, stronger GLD/TLT behavior, and worse risk-defensive forward outcomes.

The joint probability of states and observations is:

where \(\pi_{S_1}\) is the initial state probability.

This equation is the full HMM story in one line. The state path has Markov persistence, and each state emits observations according to its own feature distribution.

8.1 Filtering, Smoothing, and State Probabilities

The HMM doesn’t observe \(S_t\) directly. It infers probabilities. The forward recursion computes:

\(\alpha_{t-1}(i)\) is yesterday’s joint probability of being in state \(i\).

\(A_{ij}\) moves probability from state \(i\) to state \(j\).

\(p_j(X_t)\) checks whether today’s features look likely under state \(j\).

For numerical stability, the probabilities are normalized at each step. The normalized version gives filtered probabilities:

\[

P(S_t=j \mid X_1,\dots,X_t)

\]

Smoothing uses the full sample:

\[

P(S_t=j \mid X_1,\dots,X_T)

\]

Filtering is closer to real-time use. Smoothing is helpful for diagnostics because it uses future observations to classify historical states more cleanly. In backtesting, we need walk-forward probabilities, so the model is refit through time and probabilities are produced using information available up to the decision date.

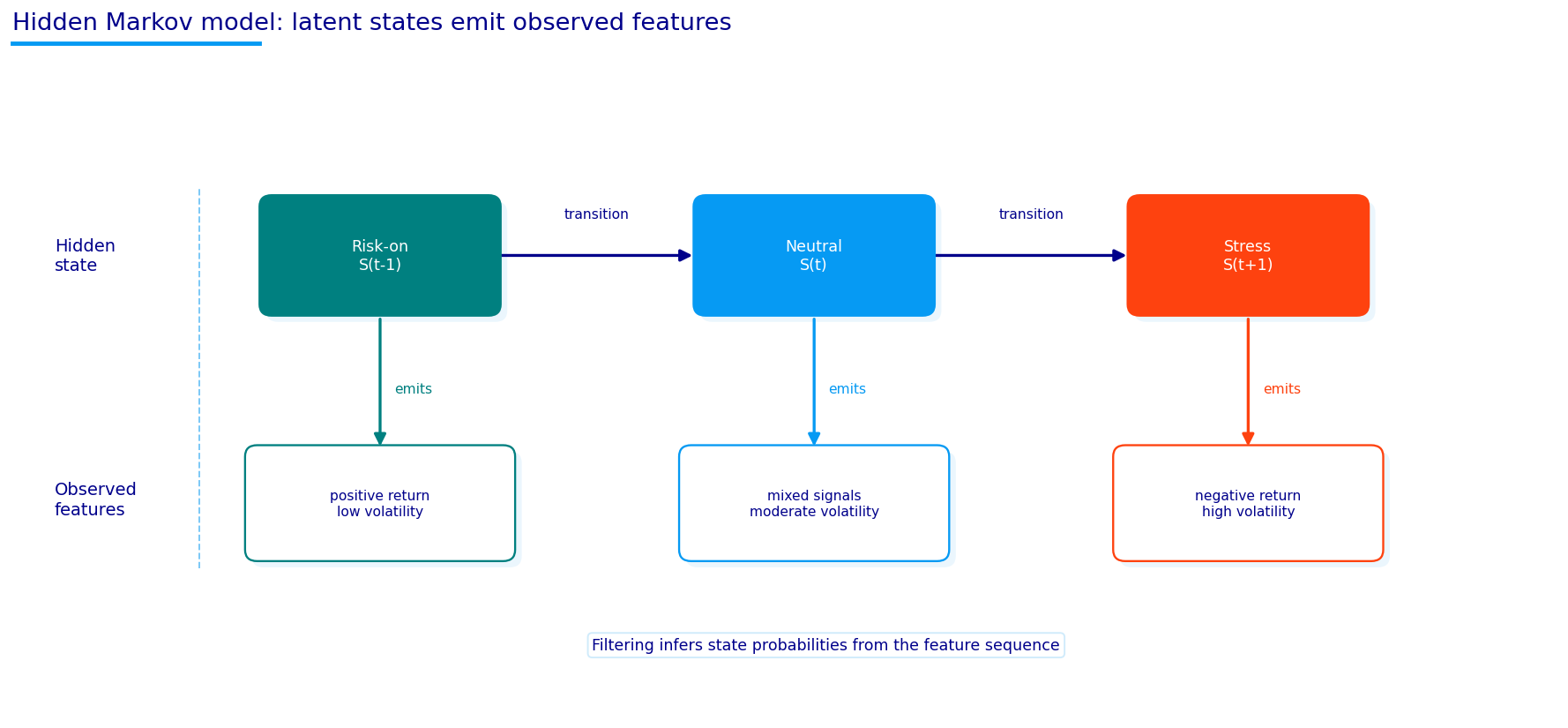

The HMM teaching diagram shows hidden states at the top and observed features at the bottom. The state sequence transitions through time, and each state emits feature observations. This is exactly the right structure for markets: the regime is latent, but returns, volatility, credit, rates, and macro conditions are observable emissions of that latent regime.

A Hidden Markov Model adds one more layer: the regime state isn’t directly observed. We only observe market features. The state is hidden, and the model infers it from the feature sequence.

The first equation is the transition model. It says how hidden regimes move through time. The second equation is the emission model. It says what feature vectors we expect to observe inside each regime.

The joint probability of a full state path and observation sequence is:

This formula is the backbone of the model. It combines persistence from the transition matrix with feature evidence from the emission densities.

There are three probability objects that matter:

Filtering estimates the current state using observations up to today:

\[

\alpha_t(k) = P(S_t=k \mid X_{1:t})

\]

This is what a real-time strategy can use. At date \(t\), we only know \(X_{1:t}\).

Smoothing estimates the state using the full sample:

\[

\gamma_t(k) = P(S_t=k \mid X_{1:T})

\]

This is useful for diagnosis because it uses future observations to better infer what historical states probably were. It isn’t a real-time trading probability.

Prediction projects the state distribution forward:

This update has a clear intuition. A state gets high probability if:

it was likely based on yesterday’s state distribution and transition matrix,

today’s features look likely under that state’s emission distribution.

For example, suppose the model was mostly risk-on yesterday. If today’s features show low volatility, strong breadth, and healthy credit, the risk-on probability remains high. If today’s features suddenly show volatility shock, credit stress, and falling breadth, the emission likelihood of the defensive state rises and the probability can shift.

The backward recursion computes future evidence:

\[

\beta_t(i) = P(X_{t+1:T}\mid S_t=i)

\]

Then smoothing combines forward and backward information:

This is useful for analyzing historical plots. Smoothed probabilities usually look cleaner than filtered probabilities because they know what happened afterward. But for live portfolio construction, filtered or walk-forward probabilities are the honest object.

The HMM filtering update can also be understood with a simple probability example. Suppose the prior state probability after applying the transition matrix is:

Now today’s feature vector arrives. The emission densities say how likely today’s features are under each state. Suppose the features are moderately stressful:

The result is still not fully defensive because the prior was heavily risk-on. But defensive probability rises from 10% to 25% because today’s features look more defensive than risk-on. That is the filtering logic.

This example also explains why HMM probabilities often move smoothly. The model needs enough evidence to overcome the transition prior. A single noisy feature movement may not flip the state. A persistent sequence of stressful observations can.

Show code

fig, ax = hidden_markov_model()plt.show()

8.2 HMM Training with EM

The HMM parameters are usually estimated by an EM algorithm called Baum-Welch. The observed data are \(X_{1:T}\), but the state path \(S_{1:T}\) is hidden. EM handles this by alternating between estimating state probabilities and updating parameters.

This is very similar to the GMM EM update, but with one important addition: transition probabilities \(\xi_t(i,j)\). GMM treats observations as independent. HMM treats observations as a sequence.

That difference is the main reason HMMs are so natural for market regimes. The current state isn’t only determined by today’s feature vector. It also depends on where the market probably was yesterday.

The Baum-Welch EM algorithm is important enough to unpack slowly. The difficulty is that we don’t observe \(S_t\). If we did observe the state path, estimating parameters would be easy. We would count transitions to estimate \(A\), and compute the mean/variance of features inside each state to estimate \(\mu_k\) and \(\Sigma_k\).

Because the states are hidden, EM replaces hard counts with probability-weighted counts.

The E-step computes:

\[

\gamma_t(k)=P(S_t=k\mid X_{1:T})

\]

and:

\[

\xi_t(i,j)=P(S_t=i,S_{t+1}=j\mid X_{1:T})

\]

Here \(\gamma_t(k)\) is the probability that date \(t\) belongs to state \(k\). \(\xi_t(i,j)\) is the probability that the model moved from state \(i\) to state \(j\) between \(t\) and \(t+1\).

The numerator is the expected number of transitions from \(i\) to \(j\). The denominator is the expected number of times we were in state \(i\) before a transition. So \(A_{ij}\) is an expected transition frequency.

This is a weighted average of feature vectors. Dates that strongly belong to state \(k\) get high weight. Dates that barely belong to state \(k\) get low weight.

For diagonal covariance, the variance of feature \(m\) in state \(k\) is:

So the model learns not only the average feature level in each regime but also the typical variability of each feature inside that regime.

This is exactly why HMMs are more appropriate than static clustering for market regimes. A GMM estimates similar emission distributions, but it treats observations as independent. The HMM adds the transition matrix, so a state assignment is shaped by both today’s feature vector and yesterday’s inferred state. That is the econometric structure we want for markets.

PCA-HMM first compresses the selected feature matrix into principal components, then fits an HMM on those components. This helps when features are correlated and high-dimensional.

If \(Z_t\) is the standardized feature vector and \(V_m\) contains the first \(m\) PCA loadings, then the compressed vector is:

\[

F_t = V_m^\top Z_t

\]

The HMM is then fit on \(F_t\) instead of \(Z_t\).

The advantage is that PCA removes redundant directions. Instead of fitting emissions on many correlated features, the HMM sees a smaller set of orthogonal factors. The downside is interpretability. A hidden state defined by PCs is less directly tied to original macro and market features.

The HMM and the supervised classifier answer different questions, so their disagreement is useful.

The HMM estimates:

\[

P(S_t=k\mid X_{1:t})

\]

where \(S_t\) is a latent state. It tries to explain the sequence of observed features through hidden regimes. It cares strongly about persistence because the transition matrix makes today’s state depend on yesterday’s state.