from pathlib import Path

import warnings

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

from quantfinlab.dataio.panel import load_yfinance_panel, prices_to_returns_panel

from quantfinlab.portfolio import covariance, expected_returns

from quantfinlab.portfolio.universe import (

build_liquid_universe_by_date,

clean_close_volume_panels,

make_rebalance_dates,

)

from quantfinlab.portfolio.walkforward import run_walkforward_grid

from quantfinlab.portfolio.hrp import hrp_weight_frame

from quantfinlab.backtest.portfolio import run_many_weights_backtests

from quantfinlab.portfolio.selection import build_strategy_summary, performance_metrics

from quantfinlab.reports.risk_report import risk_report

from quantfinlab.portfolio.network import (

central_peripheral_weights,

centrality_table,

corr_distance,

dense_network,

dependence_to_distance,

kendall_to_t_copula_corr,

mst_network,

network_diversifier_weights,

network_score,

pairwise_corr_for_weights,

pmfg_network,

pseudo_observations,

scale_01,

select_t_copula_nu,

shrink_corr,

student_t_tail_dependence,

)

from quantfinlab.plotting.portfolio import (

corr_heatmap,

distance_heatmap,

network_graph,

performance_heatmap,

score_heatmap,

tail_heatmap,

weight_heatmap,

)

annualization_hk = 252

rf_annual_hk = 0.04

rf_daily_hk = (1.0 + rf_annual_hk) ** (1.0 / annualization_hk) - 1.0

w_max_hk = 0.10

data_path = Path("../data")

if not (data_path / "hkex_close_volume.parquet").exists():

data_path = Path("data")

panel = load_yfinance_panel(

data_path / "hkex_close_volume.parquet",

fields=("close", "volume"),

source="hkex_close_volume",

start="2016-01-01",

)

close_hk, volume_hk = clean_close_volume_panels(

panel["close"], panel["volume"], start="2016-01-01", min_price=1.0

)

ret_hk = prices_to_returns_panel(close_hk).replace([np.inf, -np.inf], np.nan).dropna(how="all")

monthly_candidates_hk = make_rebalance_dates(close_hk.index, freq="M", min_history_days=504)

sampled_dates_hk = pd.DatetimeIndex(monthly_candidates_hk[::3])

universe_hk = build_liquid_universe_by_date(

close=close_hk,

volume=volume_hk,

rebalance_dates=sampled_dates_hk,

top_n=100,

liquidity_lookback=252,

min_listing_days=504,

min_obs=220,

min_price=1.0,

)

dates_hk = pd.DatetimeIndex([dt for dt in sampled_dates_hk if dt in universe_hk])

grid_hk = run_walkforward_grid(

returns=ret_hk,

close=close_hk,

volume=volume_hk,

rebalance_dates=dates_hk,

universe_by_date=universe_hk,

mu_models={"Momentum": expected_returns.momentum_mu},

cov_models={"LedoitWolf": covariance.ledoit_wolf_covariance},

strategy_specs=[

{"name": "Equal Weight", "optimizer": "EW"},

{"name": "MinVar", "optimizer": "MinVar", "cov_model": "LedoitWolf"},

],

cov_lookback=252,

mu_lookback=252,

min_cov_observations=220,

min_mu_observations=220,

max_weight=w_max_hk,

min_weight=0.0,

trading_cost_bps=10,

turnover_penalty_bps=10,

fallback="equal",

rf_daily=rf_daily_hk,

)

w_equal_hk = grid_hk.weights["Equal Weight"].copy()

w_minvar_hk = grid_hk.weights["MinVar"].copy()

w_hrp_hk = hrp_weight_frame(

grid_hk.cache,

grid_hk.metadata["rebalance_dates"],

cov_model="LedoitWolf",

linkage_method="average",

w_min=0.0,

w_max=w_max_hk,

)

first_hk = dates_hk[0]

window_first_hk = ret_hk.loc[:first_hk, universe_hk[first_hk]["tickers"]].tail(252).dropna(axis=0, how="any")

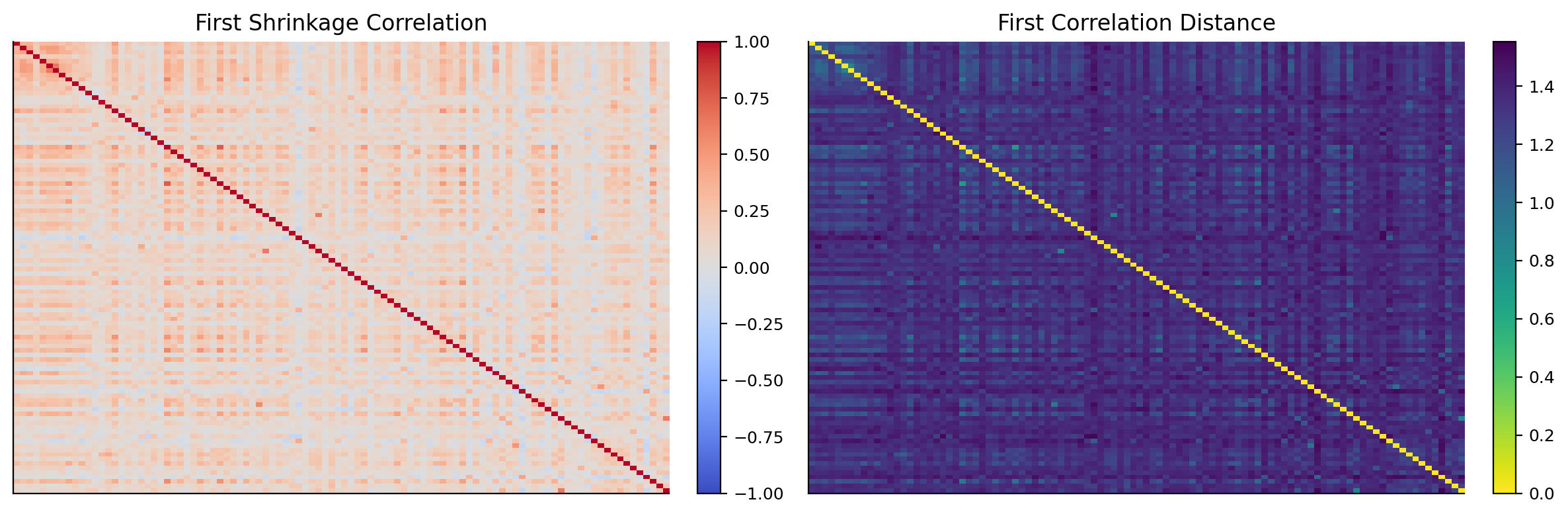

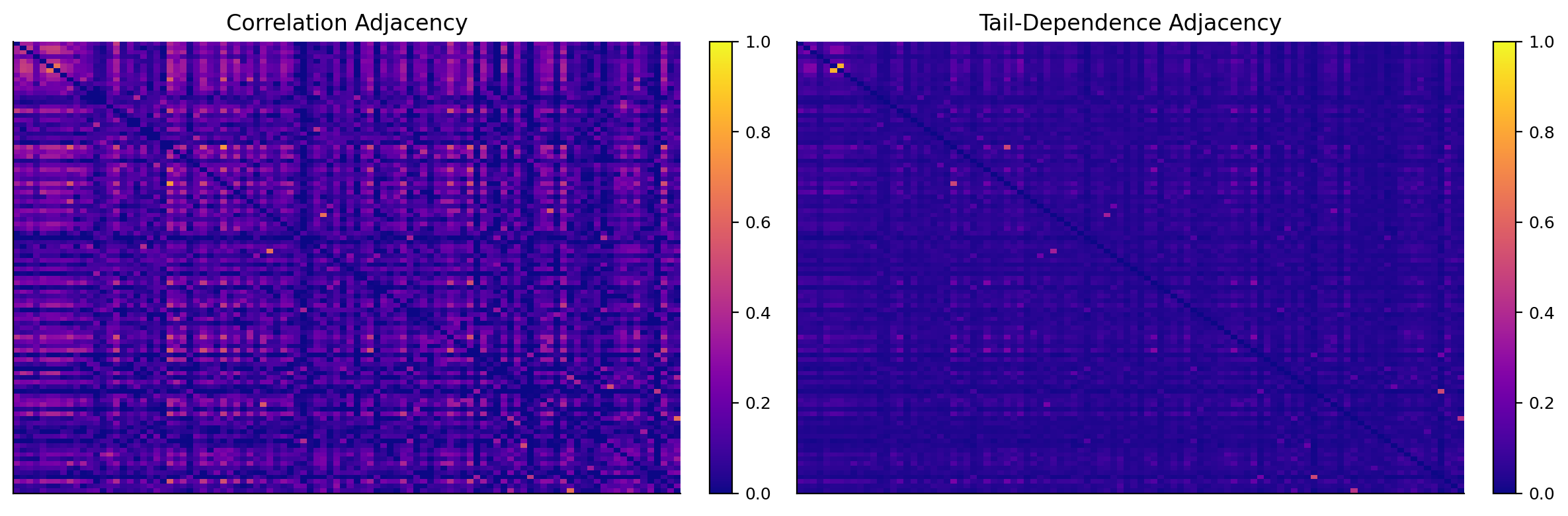

corr_first_hk = shrink_corr(window_first_hk)

dist_first_hk = corr_distance(corr_first_hk)

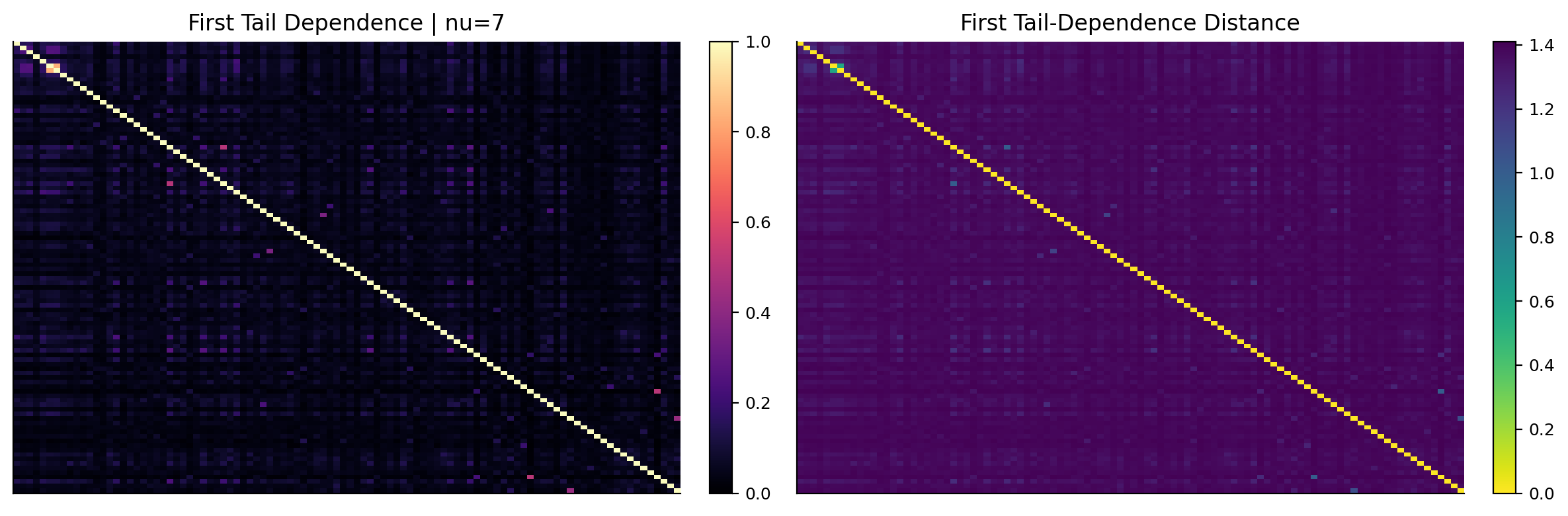

u_first_hk = pseudo_observations(window_first_hk)

nu_first_hk = select_t_copula_nu(u_first_hk, nu_grid=(4, 7, 15), max_pairs=40)

tail_first_hk = student_t_tail_dependence(kendall_to_t_copula_corr(u_first_hk), nu_first_hk)

tail_dist_first_hk = dependence_to_distance(tail_first_hk)

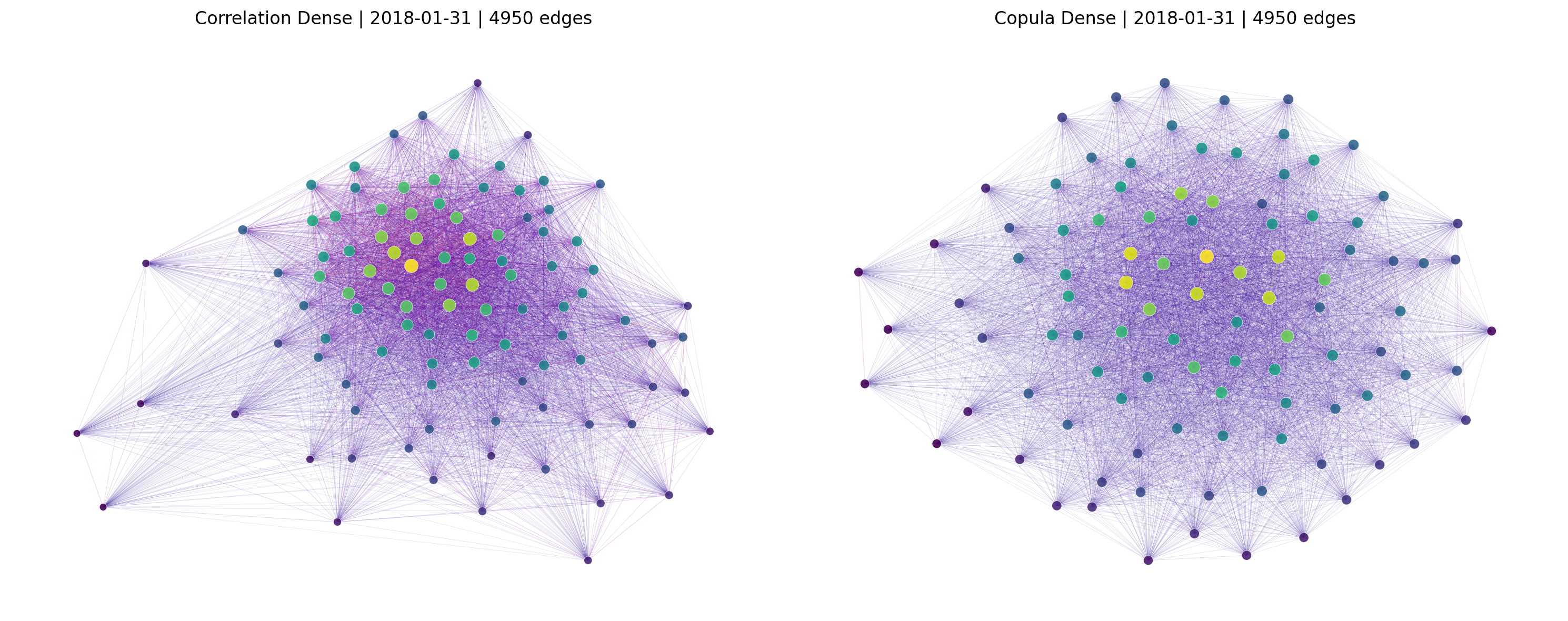

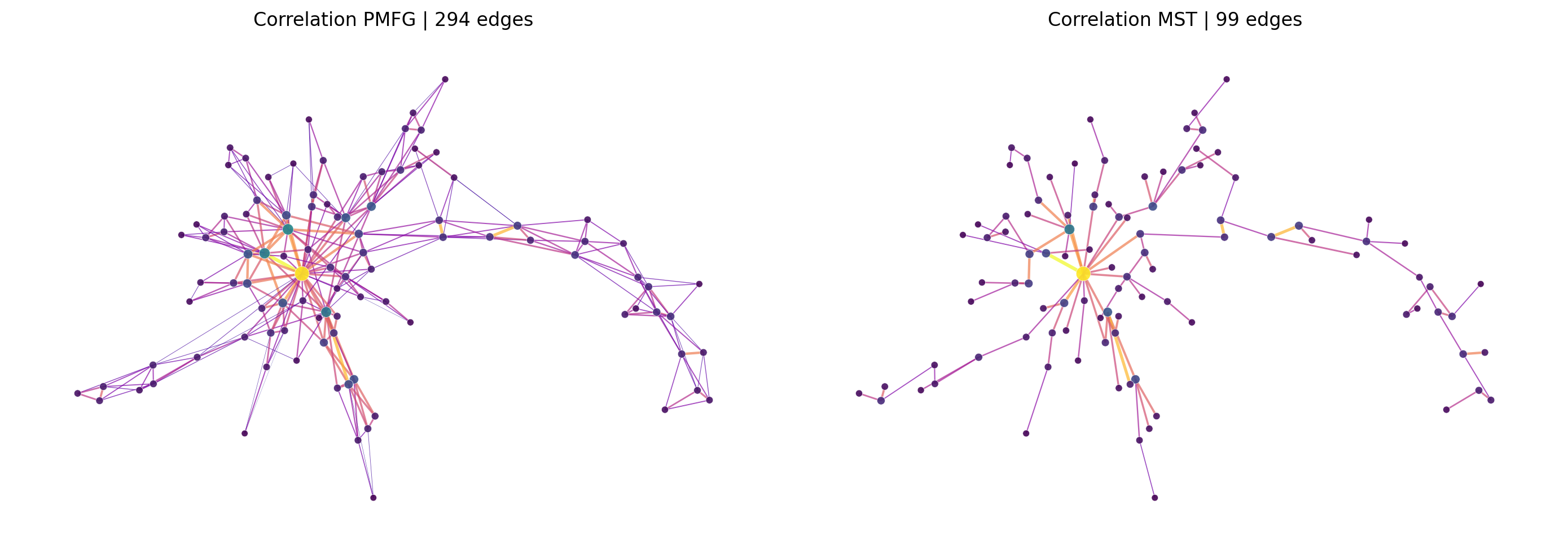

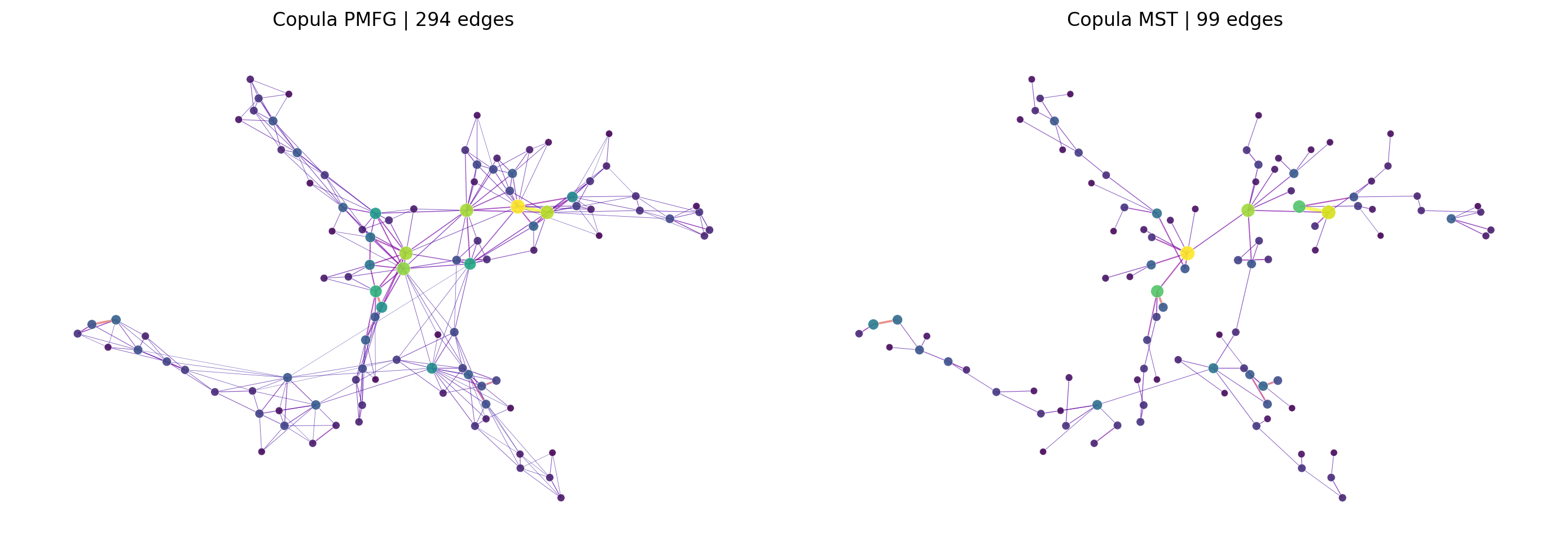

first_networks_hk = {

"Correlation Dense": dense_network(corr_first_hk, distance=dist_first_hk),

"Correlation PMFG": pmfg_network(corr_first_hk, distance=dist_first_hk),

"Correlation MST": mst_network(corr_first_hk, distance=dist_first_hk),

"Copula Dense": dense_network(tail_first_hk, distance=tail_dist_first_hk),

"Copula PMFG": pmfg_network(tail_first_hk, distance=tail_dist_first_hk),

"Copula MST": mst_network(tail_first_hk, distance=tail_dist_first_hk),

}

store_hk, comparison_rows_hk = {}, {}

for dt in dates_hk:

window = ret_hk.loc[:dt, universe_hk[dt]["tickers"]].tail(252).dropna(axis=0, how="any")

if window.shape[0] < 220 or window.shape[1] < 50:

continue

corr = shrink_corr(window)

corr_dist = corr_distance(corr)

pseudo = pseudo_observations(window)

nu = select_t_copula_nu(pseudo, nu_grid=(4, 7, 15), max_pairs=40)

tail = student_t_tail_dependence(kendall_to_t_copula_corr(pseudo), nu)

tail_dist = dependence_to_distance(tail)

graphs = {

("correlation", "pmfg"): pmfg_network(corr, distance=corr_dist),

("correlation", "mst"): mst_network(corr, distance=corr_dist),

("copula", "pmfg"): pmfg_network(tail, distance=tail_dist),

("copula", "mst"): mst_network(tail, distance=tail_dist),

}

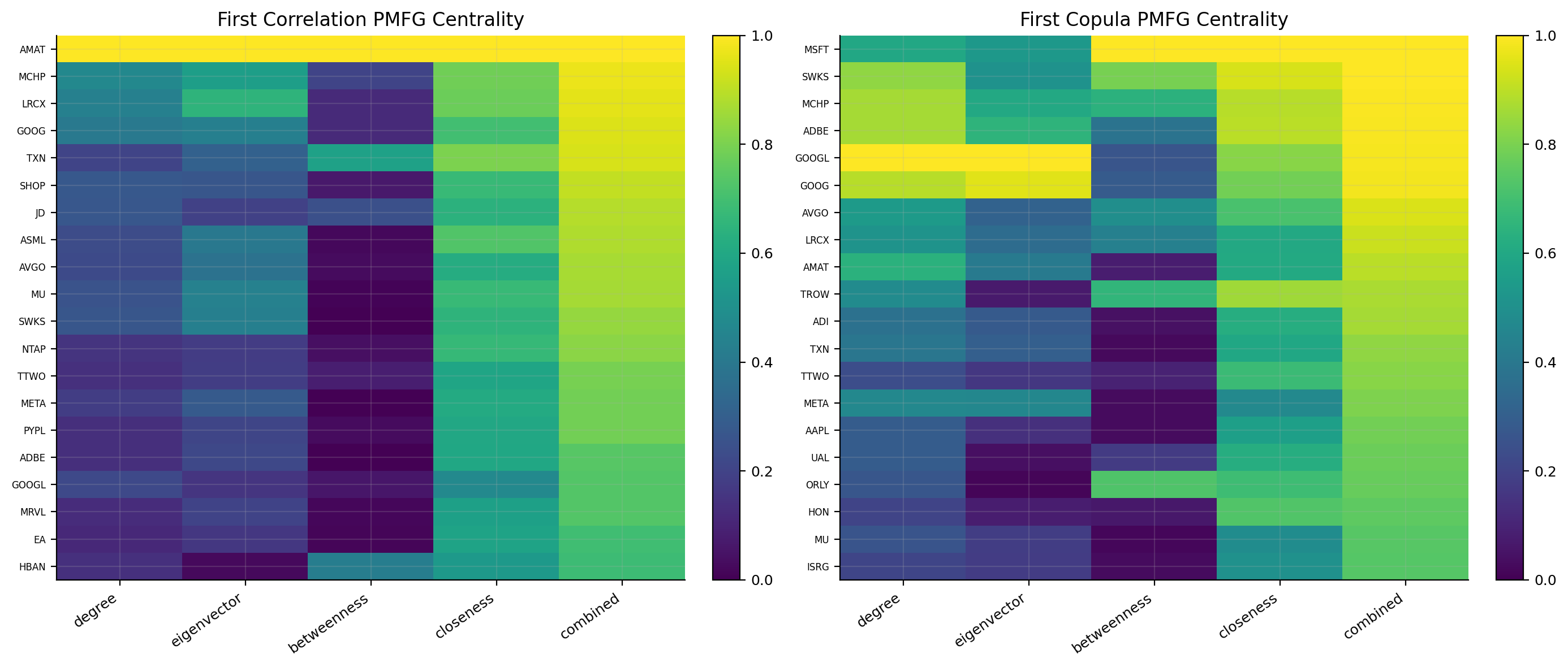

centralities = {key: centrality_table(graph) for key, graph in graphs.items()}

for (dependence, network_type), centrality in centralities.items():

for measure in ["degree", "eigenvector", "betweenness", "closeness", "combined"]:

central = scale_01(centrality[measure])

for direction, selection_score in {"central": central, "peripheral": 1.0 - central}.items():

key = f"{direction}|{dependence}|{network_type}|{measure}"

comparison_rows_hk.setdefault(key, {})[dt] = central_peripheral_weights(

selection_score, returns=window, n_stocks=20, max_weight=w_max_hk

)

store_hk[dt] = {

"window": window,

"corr": corr,

"corr_dist": corr_dist,

"tail": tail,

"tail_dist": tail_dist,

"nu": nu,

"graphs": graphs,

"centralities": centralities,

}

model_dates_hk = (

pd.DatetimeIndex(sorted(store_hk))

.intersection(w_equal_hk.index)

.intersection(w_minvar_hk.index)

.intersection(w_hrp_hk.index)

)

comparison_weights_hk = {

key: pd.DataFrame.from_dict(rows, orient="index").fillna(0.0)

for key, rows in comparison_rows_hk.items()

}

comparison_cols_hk = sorted(set().union(*(set(frame.columns) for frame in comparison_weights_hk.values())))

comparison_weights_hk = {

name: frame.reindex(index=model_dates_hk, columns=comparison_cols_hk).fillna(0.0)

for name, frame in comparison_weights_hk.items()

}

comparison_results_hk = run_many_weights_backtests(

comparison_weights_hk,

returns=ret_hk.reindex(columns=comparison_cols_hk).fillna(0.0),

cost_bps=10,

w_min=0.0,

w_max=w_max_hk,

long_only=True,

weight_timing="next_close",

)

comparison_table_hk = []

for name, result in comparison_results_hk.items():

direction, dependence, network_type, measure = name.split("|")

metrics = performance_metrics(result.net_returns, result.net_values, rf_daily=rf_daily_hk, annualization=annualization_hk)

comparison_table_hk.append(

{

"direction": direction,

"dependence": dependence,

"network": network_type,

"centrality": measure,

"Sharpe": metrics["Sharpe"],

"Max Drawdown": metrics["Max Drawdown"],

"Calmar": metrics["Calmar"],

"turnover": float(result.turnover.mean()),

"avg_pairwise_corr": float(pairwise_corr_for_weights(ret_hk, result.weights).mean()),

}

)

comparison_hk = pd.DataFrame(comparison_table_hk)

comparison_hk["sharpe"] = comparison_hk["Sharpe"]

comparison_hk["max_drawdown"] = comparison_hk["Max Drawdown"]

def parse_hk_choice(name):

direction, dependence, network_type, measure = name.split("|")

return direction, dependence, network_type, measure

def rolling_hk_choice(results, dt, direction, lookback_years=2, min_obs=252):

fallback = f"{direction}|copula|pmfg|combined"

start = pd.Timestamp(dt) - pd.DateOffset(years=lookback_years)

rows = []

for name, result in results.items():

if not name.startswith(f"{direction}|"):

continue

returns_window = result.net_returns.loc[

(result.net_returns.index >= start) & (result.net_returns.index < dt)

].dropna()

if len(returns_window) < min_obs:

continue

nav_window = (1.0 + returns_window).cumprod()

metrics = performance_metrics(

returns_window,

nav_window,

rf_daily=rf_daily_hk,

annualization=annualization_hk,

)

turnover_window = result.turnover.loc[

(result.turnover.index >= start) & (result.turnover.index < dt)

].dropna()

rows.append(

{

"name": name,

"Sharpe": metrics["Sharpe"],

"Max Drawdown": metrics["Max Drawdown"],

"Calmar": metrics["Calmar"],

"turnover": float(turnover_window.mean()) if len(turnover_window) else np.nan,

}

)

if not rows:

return fallback, {"Sharpe": np.nan, "Max Drawdown": np.nan, "source": "fallback"}

table = pd.DataFrame(rows).replace([np.inf, -np.inf], np.nan).dropna(subset=["Sharpe"])

if table.empty:

return fallback, {"Sharpe": np.nan, "Max Drawdown": np.nan, "source": "fallback"}

best = table.sort_values(

["Sharpe", "Max Drawdown", "turnover"],

ascending=[False, False, True],

).iloc[0]

return best["name"], {

"Sharpe": float(best["Sharpe"]),

"Max Drawdown": float(best["Max Drawdown"]),

"source": "rolling",

}

def train_hk_choice(results, direction, train_end, min_obs=252):

fallback = f"{direction}|copula|pmfg|combined"

rows = []

for name, result in results.items():

if not name.startswith(f"{direction}|"):

continue

returns_window = result.net_returns.loc[result.net_returns.index < train_end].dropna()

if len(returns_window) < min_obs:

continue

nav_window = (1.0 + returns_window).cumprod()

metrics = performance_metrics(

returns_window,

nav_window,

rf_daily=rf_daily_hk,

annualization=annualization_hk,

)

turnover_window = result.turnover.loc[result.turnover.index < train_end].dropna()

rows.append(

{

"name": name,

"Sharpe": metrics["Sharpe"],

"Max Drawdown": metrics["Max Drawdown"],

"turnover": float(turnover_window.mean()) if len(turnover_window) else np.nan,

}

)

if not rows:

return fallback

table = pd.DataFrame(rows).replace([np.inf, -np.inf], np.nan).dropna(subset=["Sharpe"])

if table.empty:

return fallback

return table.sort_values(["Sharpe", "Max Drawdown", "turnover"], ascending=[False, False, True]).iloc[0]["name"]

selector_train_end_hk = model_dates_hk[min(8, len(model_dates_hk) - 1)]

central_fixed_hk = "central|copula|pmfg|combined"

peripheral_train_hk = train_hk_choice(comparison_results_hk, "peripheral", selector_train_end_hk)

def stability_gated_hk_choice(results, dt, direction, train_selection, threshold=0.50):

if pd.Timestamp(dt) <= selector_train_end_hk:

return f"{direction}|copula|pmfg|combined", {"Sharpe": np.nan, "source": "fallback"}

rolling_name, rolling_info = rolling_hk_choice(results, dt, direction)

if not np.isfinite(rolling_info["Sharpe"]) or rolling_info["Sharpe"] < threshold:

return train_selection, {"Sharpe": rolling_info["Sharpe"], "source": "train-fixed"}

return rolling_name, rolling_info

selection_records_hk = []

central_rows_hk, peripheral_rows_hk, diversifier_rows_hk = {}, {}, {}

for dt in model_dates_hk:

central_choice = central_fixed_hk

central_info = {"Sharpe": np.nan, "source": "fixed"}

peripheral_choice, peripheral_info = stability_gated_hk_choice(

comparison_results_hk, dt, "peripheral", peripheral_train_hk

)

network_choice, network_info = stability_gated_hk_choice(

comparison_results_hk, dt, "peripheral", peripheral_train_hk

)

selection_records_hk.append(

{

"date": dt,

"central_choice": central_choice,

"central_sharpe": central_info["Sharpe"],

"central_source": central_info["source"],

"peripheral_choice": peripheral_choice,

"peripheral_sharpe": peripheral_info["Sharpe"],

"peripheral_source": peripheral_info["source"],

"network_choice": network_choice,

"network_sharpe": network_info["Sharpe"],

"network_source": network_info["source"],

}

)

record = store_hk[dt]

_, dependence, network_type, measure = parse_hk_choice(central_choice)

centrality = record["centralities"][(dependence, network_type)]

central_score = scale_01(centrality[measure])

central_rows_hk[dt] = central_peripheral_weights(

central_score, returns=record["window"], side="central", n_stocks=20, max_weight=w_max_hk

)

_, dependence, network_type, measure = parse_hk_choice(peripheral_choice)

centrality = record["centralities"][(dependence, network_type)]

periphery = 1.0 - scale_01(centrality[measure])

peripheral_rows_hk[dt] = central_peripheral_weights(

periphery, returns=record["window"], side="peripheral", n_stocks=20, max_weight=w_max_hk

)

_, dependence, network_type, measure = parse_hk_choice(network_choice)

centrality = record["centralities"][(dependence, network_type)]

periphery = 1.0 - scale_01(centrality[measure])

scores = network_score(

periphery,

returns=record["window"],

momentum_window=126,

momentum_skip=0,

volatility_window=126,

drawdown_window=252,

)

diversifier_rows_hk[dt] = network_diversifier_weights(

scores, returns=record["window"], n_stocks=25, max_weight=w_max_hk

)

selection_hk = pd.DataFrame(selection_records_hk).set_index("date")

w_central_hk = pd.DataFrame.from_dict(central_rows_hk, orient="index").fillna(0.0)

w_peripheral_hk = pd.DataFrame.from_dict(peripheral_rows_hk, orient="index").fillna(0.0)

w_diversifier_hk = pd.DataFrame.from_dict(diversifier_rows_hk, orient="index").fillna(0.0)

common_index_hk = (

w_diversifier_hk.index.intersection(w_equal_hk.index).intersection(w_minvar_hk.index).intersection(w_hrp_hk.index)

)

columns_hk = sorted(

set(w_equal_hk.columns)

| set(w_minvar_hk.columns)

| set(w_hrp_hk.columns)

| set(w_central_hk.columns)

| set(w_peripheral_hk.columns)

| set(w_diversifier_hk.columns)

)

weights_hk = {

"Equal Weight": w_equal_hk.reindex(index=common_index_hk, columns=columns_hk).fillna(0.0),

"MinVar": w_minvar_hk.reindex(index=common_index_hk, columns=columns_hk).fillna(0.0),

"HRP": w_hrp_hk.reindex(index=common_index_hk, columns=columns_hk).fillna(0.0),

"Most Central 20": w_central_hk.reindex(index=common_index_hk, columns=columns_hk).fillna(0.0),

"Most Peripheral 20": w_peripheral_hk.reindex(index=common_index_hk, columns=columns_hk).fillna(0.0),

"Network Diversifier": w_diversifier_hk.reindex(index=common_index_hk, columns=columns_hk).fillna(0.0),

}

results_hk = run_many_weights_backtests(

weights_hk,

returns=ret_hk.reindex(columns=columns_hk).fillna(0.0),

cost_bps=10,

w_min=0.0,

w_max=w_max_hk,

long_only=True,

weight_timing="next_close",

rf_daily=rf_daily_hk,

)

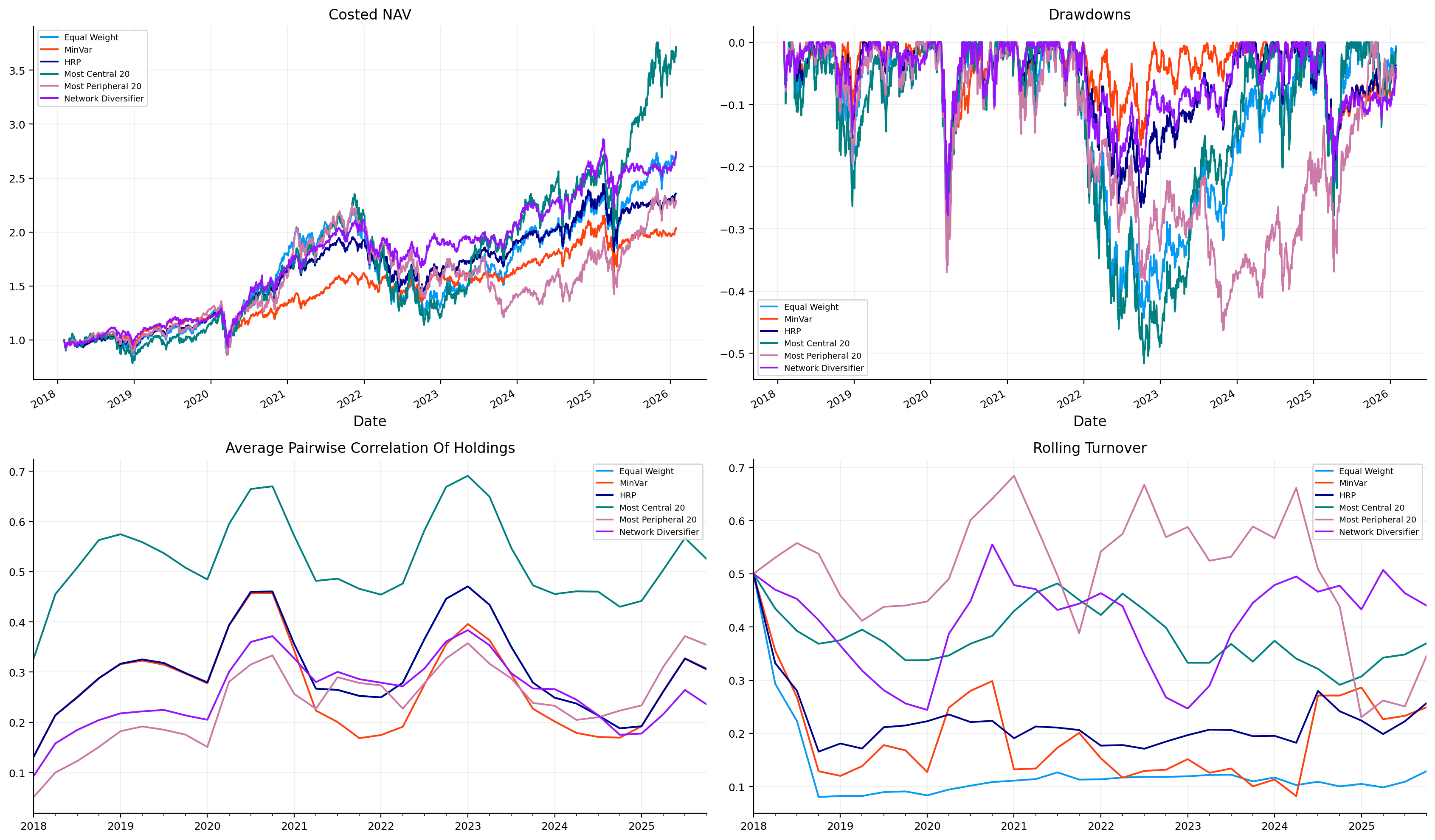

summary_hk = build_strategy_summary(results_hk, rf_daily=rf_daily_hk, annualization=annualization_hk)

display(summary_hk[["CAGR", "Vol", "Sharpe", "Max Drawdown", "Calmar", "Turnover", "Cost Drag", "Effective N"]].round(4))

display(selection_hk.tail(8))

display(

pd.concat(

{

"Most Central 20": selection_hk["central_choice"].value_counts(),

"Most Peripheral 20": selection_hk["peripheral_choice"].value_counts(),

"Network Diversifier": selection_hk["network_choice"].value_counts(),

},

axis=1,

).fillna(0).astype(int)

)

latest_dt_hk = common_index_hk[-1]

latest_hk = store_hk[latest_dt_hk]

latest_network_choice_hk = selection_hk.loc[latest_dt_hk, "network_choice"]

_, latest_dependence_hk, latest_network_type_hk, latest_measure_hk = parse_hk_choice(latest_network_choice_hk)

centrality_hk = latest_hk["centralities"][(latest_dependence_hk, latest_network_type_hk)]

central_score_hk = scale_01(centrality_hk[latest_measure_hk])

periphery_hk = 1.0 - central_score_hk

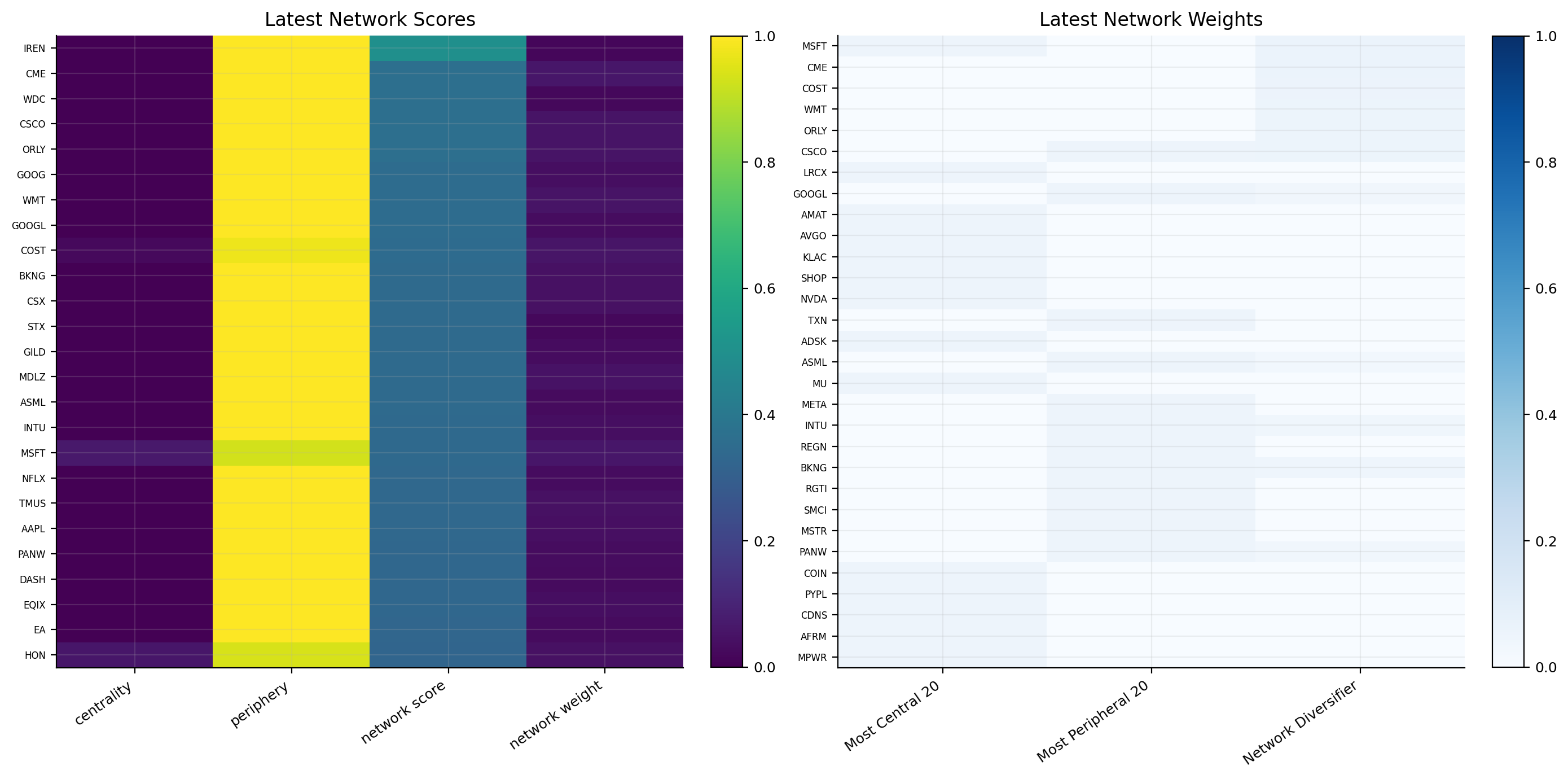

network_scores_hk = network_score(periphery_hk, returns=latest_hk["window"])

score_frame_hk = pd.concat(

{

"centrality": central_score_hk,

"periphery": periphery_hk,

"network score": network_scores_hk,

"weight": weights_hk["Network Diversifier"].loc[latest_dt_hk],

},

axis=1,

).sort_values("network score", ascending=False).head(25)

weight_frame_hk = pd.concat(

{

"Most Central 20": weights_hk["Most Central 20"].loc[latest_dt_hk],

"Most Peripheral 20": weights_hk["Most Peripheral 20"].loc[latest_dt_hk],

"Network Diversifier": weights_hk["Network Diversifier"].loc[latest_dt_hk],

},

axis=1,

).fillna(0.0)

nav_hk = pd.concat({name: result.net_values for name, result in results_hk.items()}, axis=1)

drawdowns_hk = nav_hk / nav_hk.cummax() - 1.0

fig, axes = plt.subplots(2, 4, figsize=(22, 9))

axes = axes.ravel()

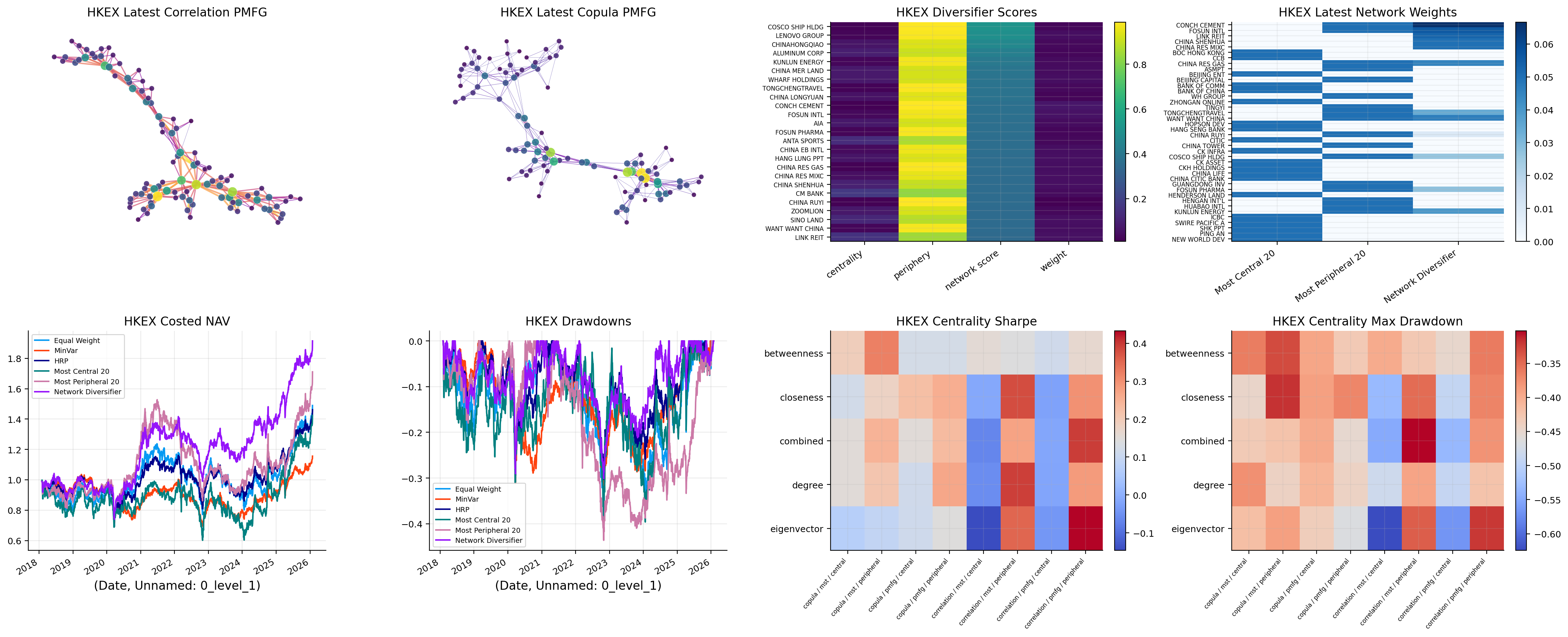

network_graph(

axes[0],

latest_hk["graphs"][("correlation", "pmfg")],

title="HKEX Latest Correlation PMFG",

)

network_graph(

axes[1],

latest_hk["graphs"][("copula", "pmfg")],

title="HKEX Latest Copula PMFG",

)

score_heatmap(axes[2], score_frame_hk, title="HKEX Diversifier Scores")

weight_heatmap(axes[3], weight_frame_hk, title="HKEX Latest Network Weights")

nav_hk.plot(ax=axes[4], title="HKEX Costed NAV")

drawdowns_hk.plot(ax=axes[5], title="HKEX Drawdowns")

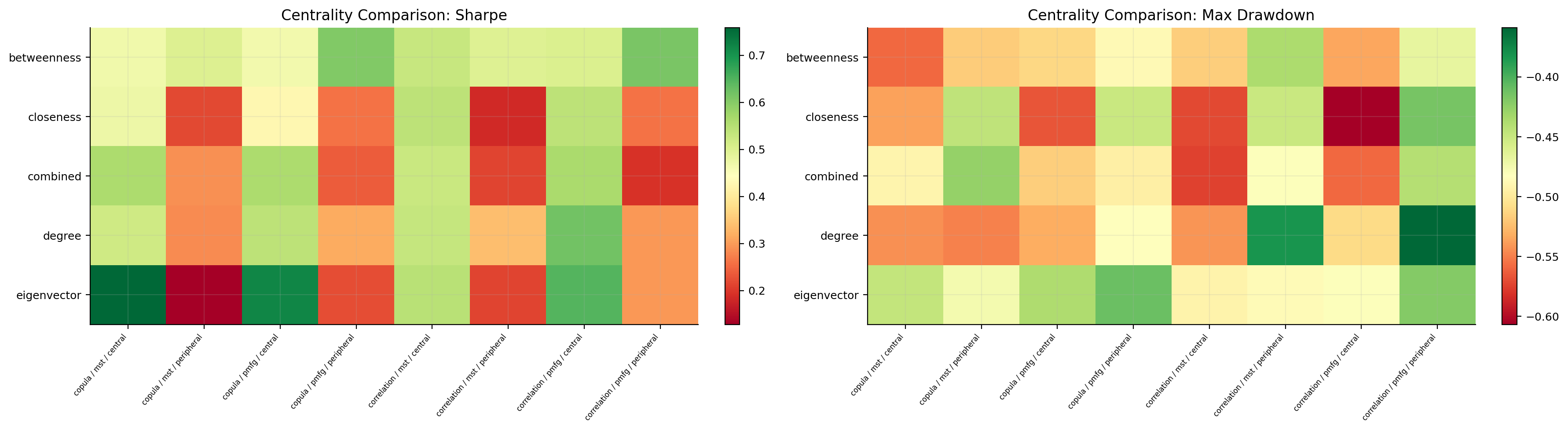

performance_heatmap(axes[6], comparison_hk, value="sharpe", title="HKEX Centrality Sharpe")

performance_heatmap(axes[7], comparison_hk, value="max_drawdown", title="HKEX Centrality Max Drawdown")

for ax in axes[4:6]:

ax.grid(True, alpha=0.25)

fig.tight_layout()

plt.show()

warnings.filterwarnings("ignore", message="obj.round has no effect with datetime, timedelta, or period dtypes.*", category=UserWarning)

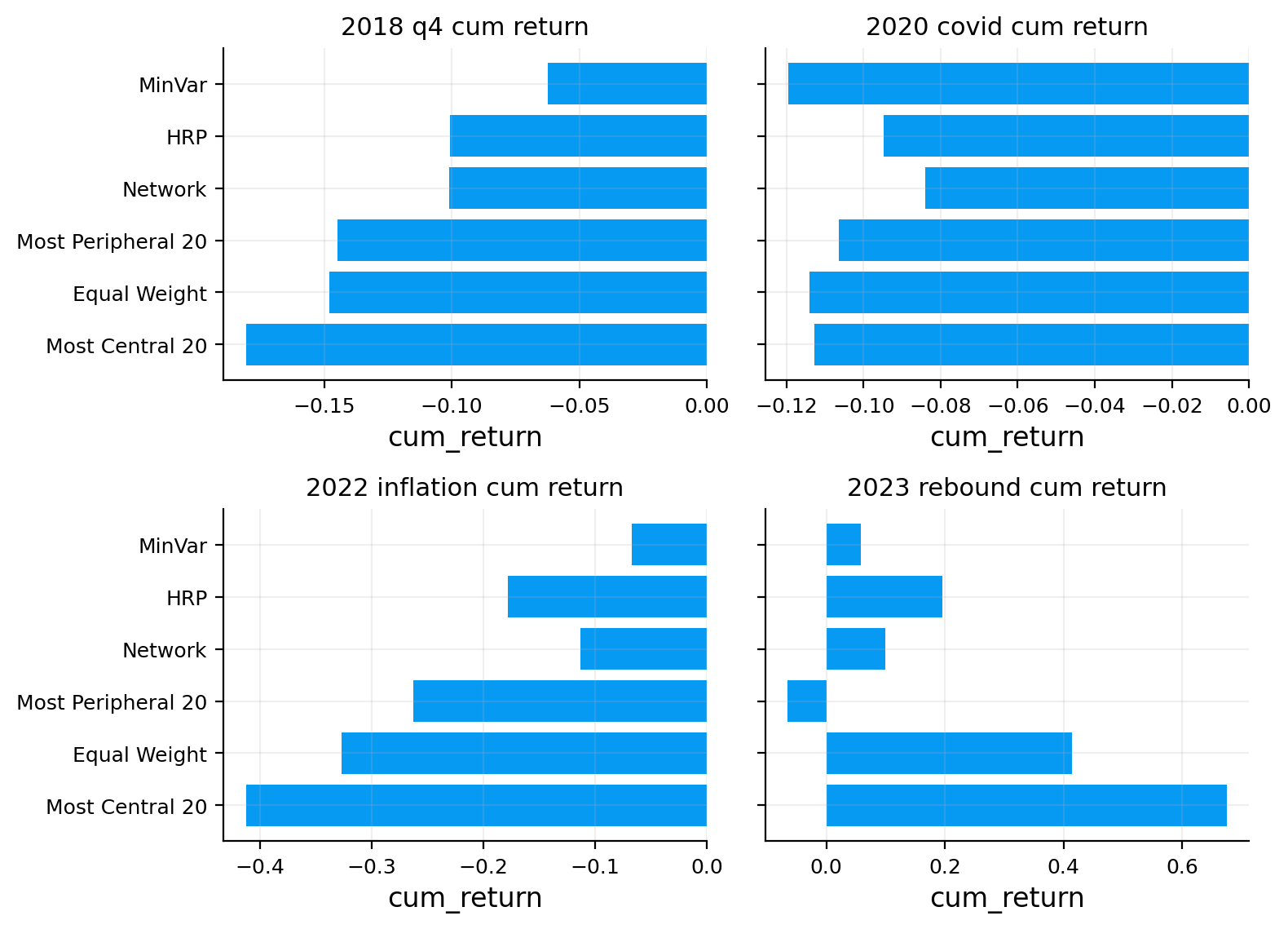

risk_hk = risk_report(

objects={name: result.net_returns for name, result in results_hk.items()},

rf_daily=rf_daily_hk,

include={

"performance_tables": False,

"shape_tables": False,

"drawdowns": False,

"drawdown_episodes": True,

"var_es": True,

"var_backtest": False,

"stress": True,

"capm": False,

"rolling_beta": False,

"correlation": False,

"attribution": False,

"exec_bullets": False,

},

var_settings={"alpha": 0.05, "methods": ["hist", "cf"], "lookback": 252},

stress_settings={

"windows": {

"2018_q4": ("2018-10-01", "2018-12-31"),

"2020_covid": ("2020-02-20", "2020-04-30"),

"2022_inflation": ("2022-01-03", "2022-10-31"),

"2023_rebound": ("2023-01-01", "2023-12-31"),

},

"worst_only": False,

},

output={"display_tables": True, "show_figures": False, "round_tables": 4},

)

plt.close("all")