A real-time macro signal stack where every raw macro series is transformed into a comparable stress-oriented signal.

A set of economic blocks for inflation, policy/rates, growth, labor, housing, external trade, and macro breadth/conflict.

Several Financial Conditions Index models: an economic-weighted index, a PCA index, a supervised PLS index, a stress-probability index, and a blended index.

A validation layer that checks whether tighter financial conditions actually line up with future equity stress, higher future volatility, and worse drawdowns.

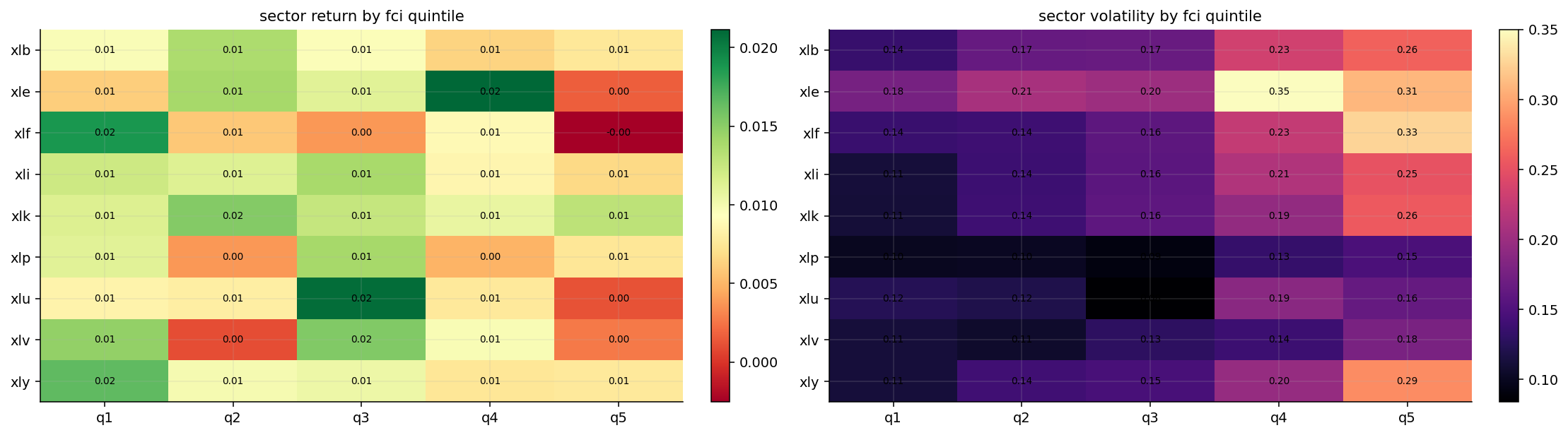

A sector-regime study that connects macro conditions to sector behavior instead of treating sector rotation as pure momentum.

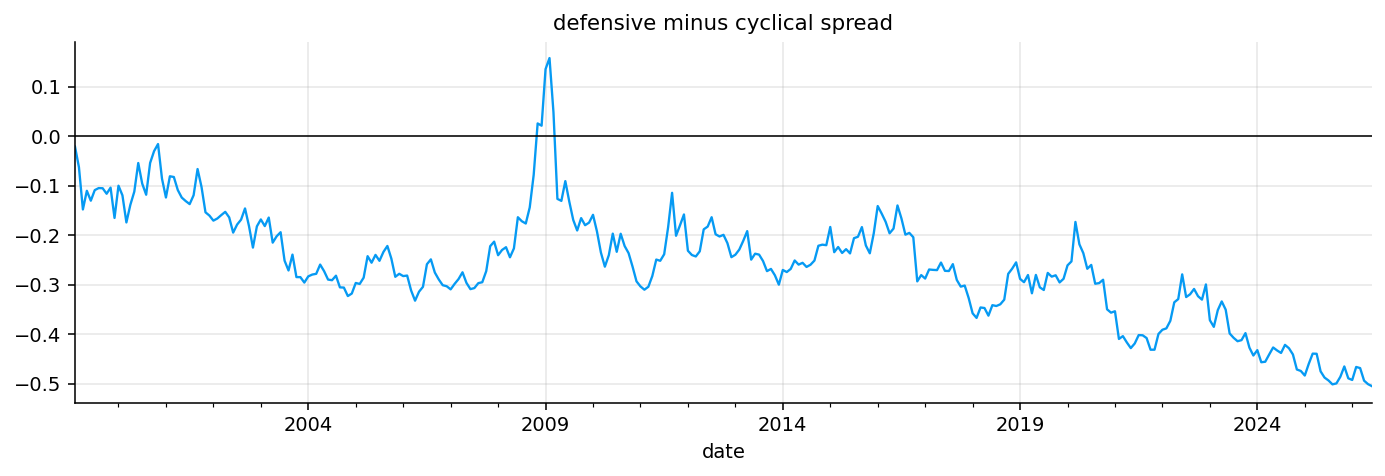

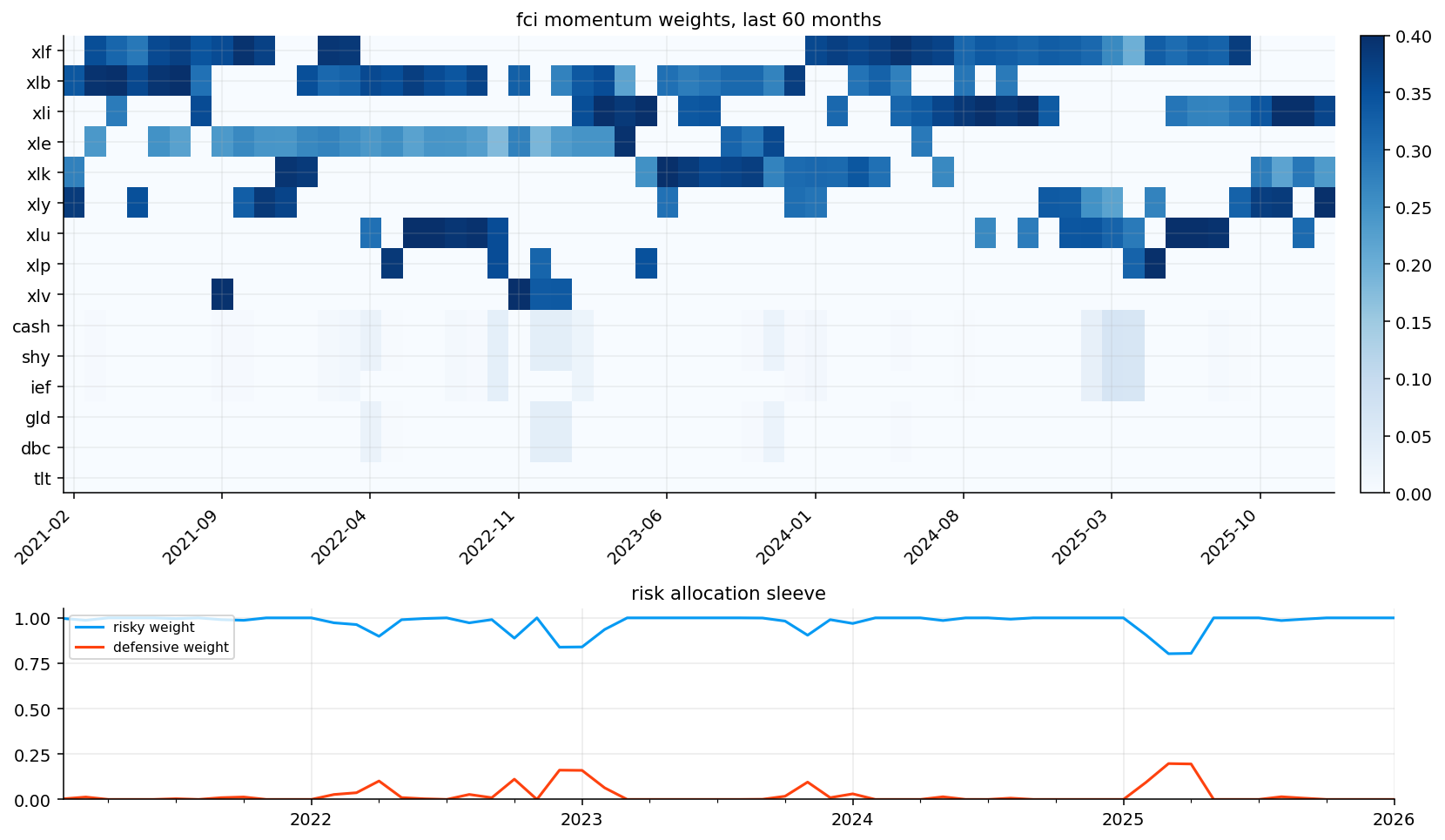

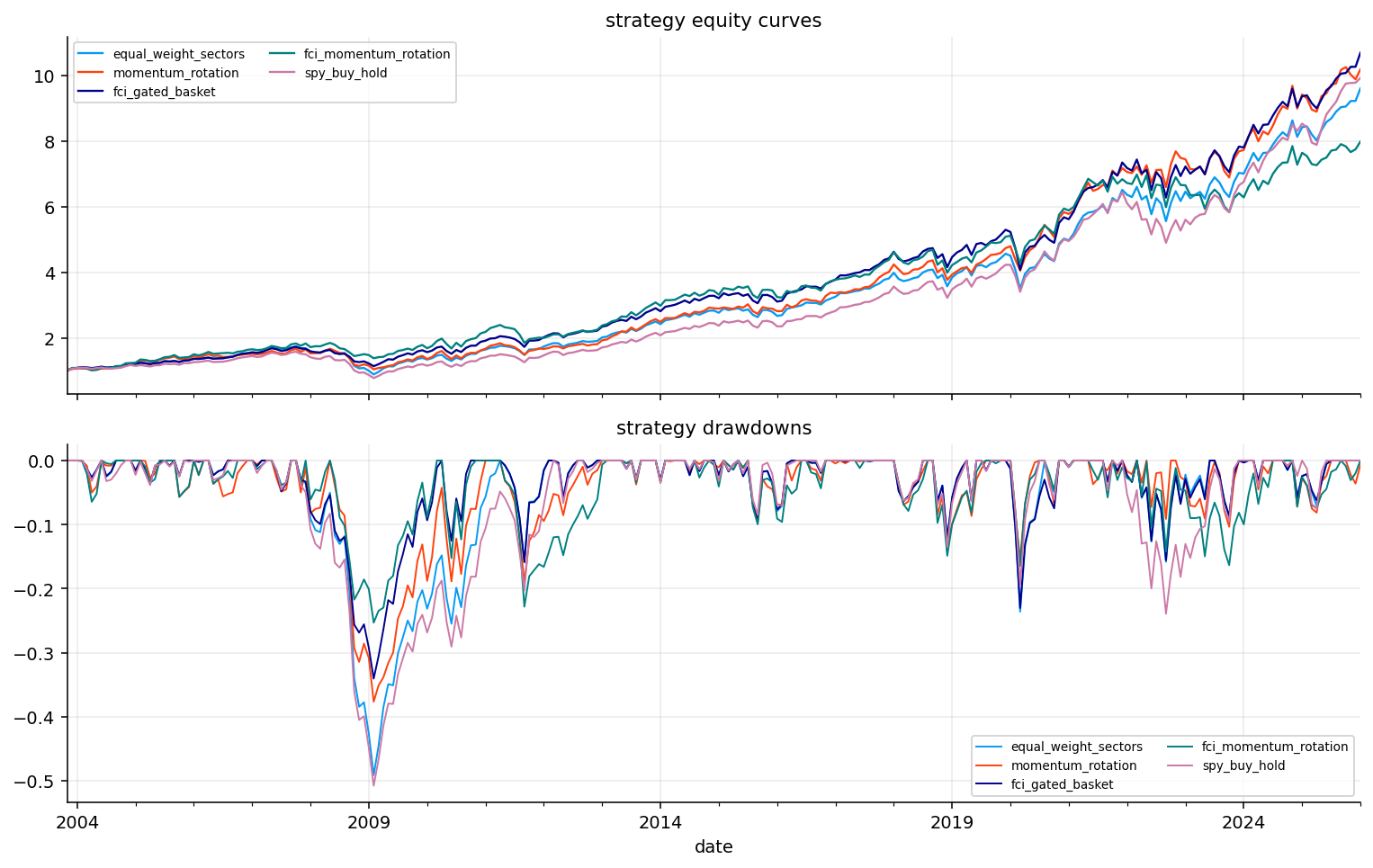

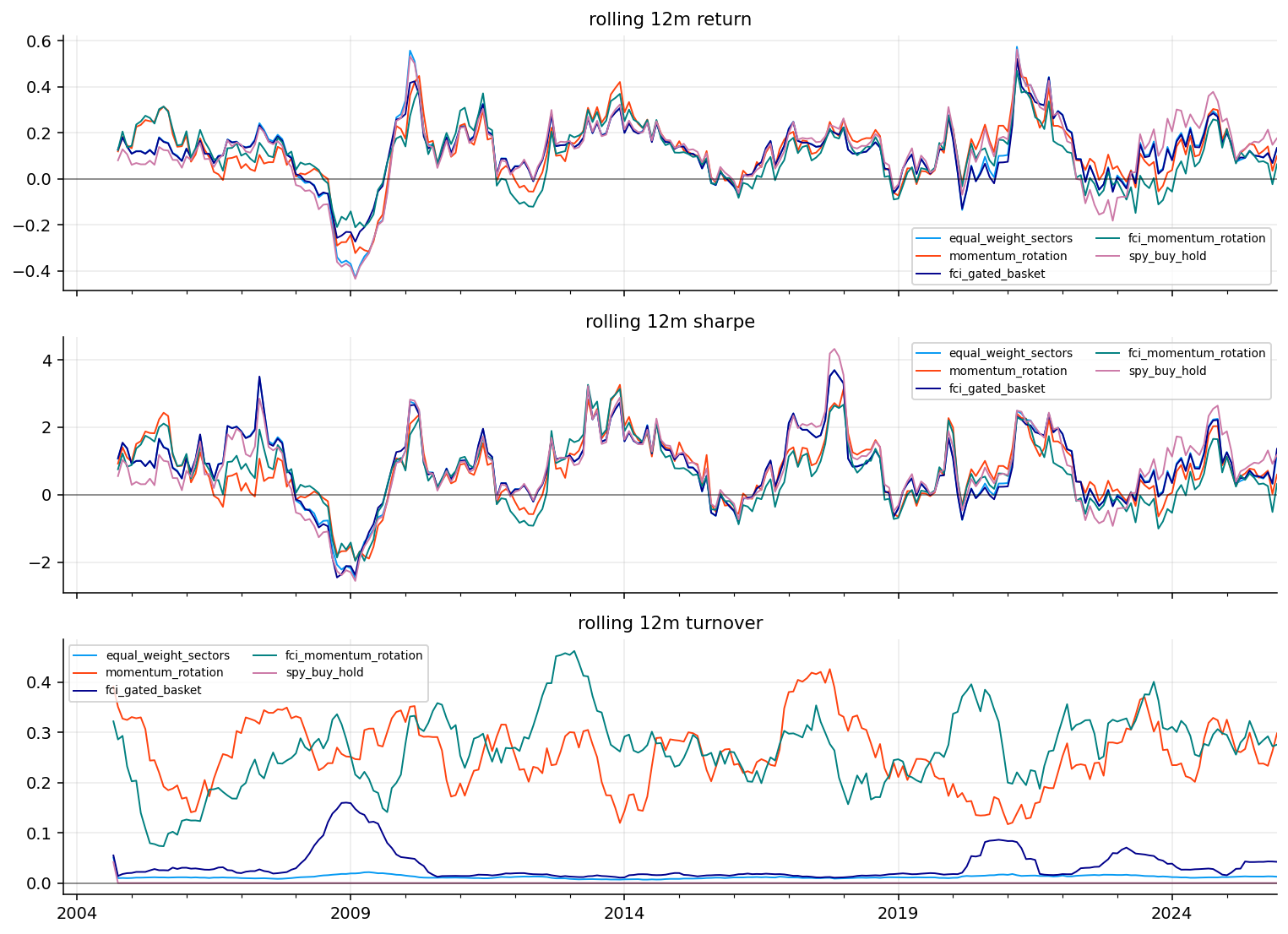

A macro-gated allocation strategy where the FCI changes the risky/defensive split and macro blocks change which sectors are preferred.

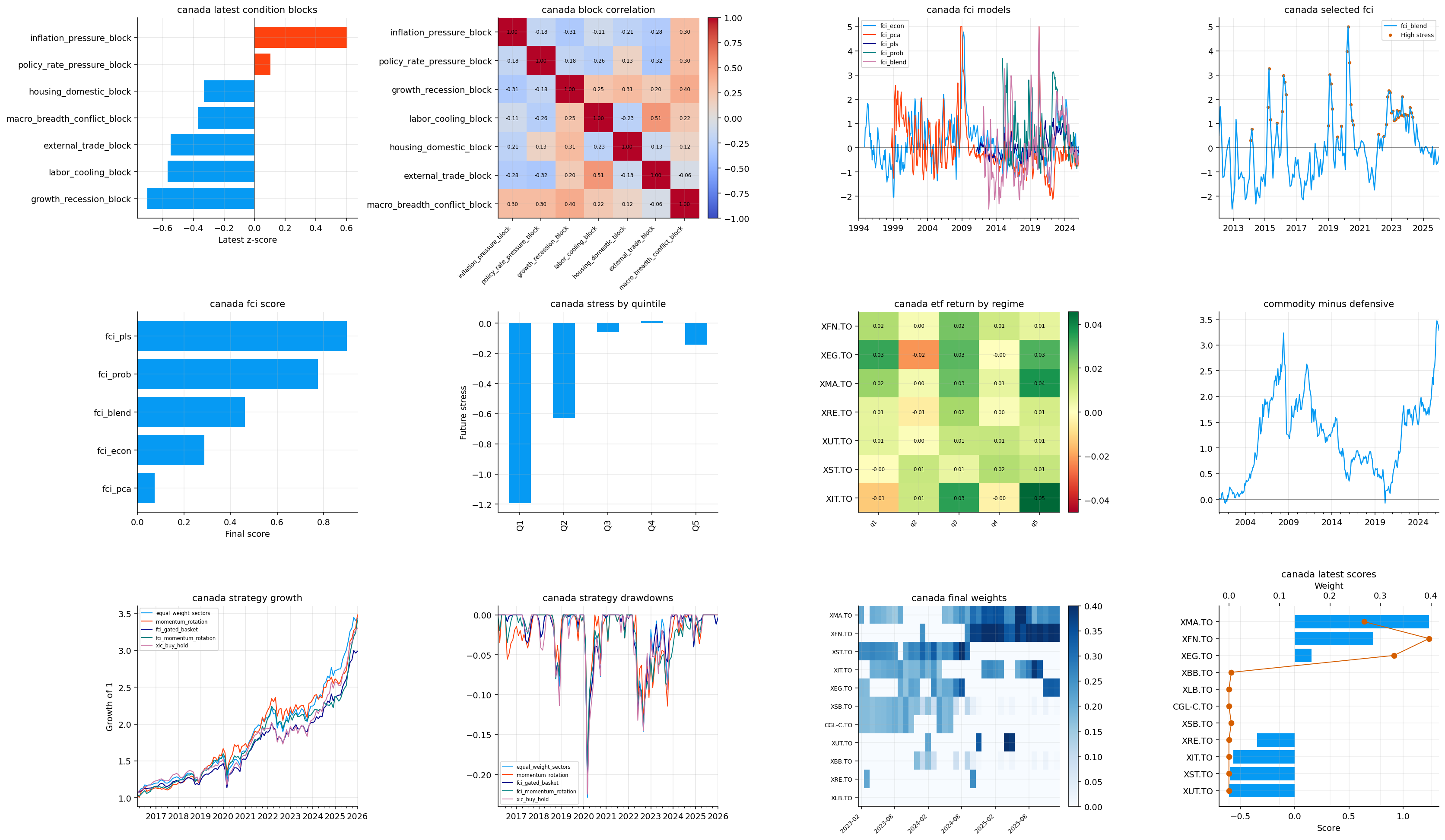

A secondary Canada implementation through the library, using Canadian macro data and Canadian sector ETFs.

This project is mainly about turning macro data into a tradable state variable. A single inflation number or unemployment number doesn’t tell us enough by itself. Markets react to combinations: inflation plus policy, growth plus labor, housing plus rates, domestic demand plus external demand, and whether stress is narrow or spreading across the system.

A Financial Conditions Index, or FCI, tries to compress that large macro state into a smaller signal. In this project, higher FCI values mean tighter / more stressful conditions. Lower values mean easier conditions, stronger risk support, or at least less macro pressure. The important part is that we don’t use one black-box index only. We build the index from interpretable blocks first, then compare several ways of combining those blocks.

The goal is to make the macro signal teachable, testable, and usable.

1) The Macro Object We Want to Build

The object we want is a monthly signal that summarizes how difficult the economic environment is for risk assets. We can write the raw macro panel as:

where each \(x_{i,t}\) is one raw macro series at month \(t\). One series might be CPI inflation, another might be the unemployment rate, another might be industrial production, and another might be a yield or policy rate.

The problem is that these variables live in different units. CPI might be an index, fed funds is a percentage rate, jobless claims are people, oil is dollars per barrel, and a confidence survey may have its own scale. We can’t average them directly. We first need to transform each series into a common language.

Here \(\bar{x}_{i,t}^{\text{expanding}}\) is the mean of series \(i\) using only data available up to month \(t\), and \(s_{i,t}^{\text{expanding}}\) is the corresponding expanding standard deviation. A value of \(z_{i,t}=2\) means the current observation is about two historical standard deviations above its own past normal level.

The real-time part matters. We don’t compute the mean and standard deviation using the full sample, because that would let the future define the past. A macro index built for trading has to use information that would’ve been known at the time.

Macro Transmission Into Asset Prices

A macro variable matters for a portfolio only if it changes cash flows, discount rates, risk premia, or liquidity. A simple present-value formula makes this connection clear:

where \(P_t\) is the asset price, \(CF_{t+h}\) is the future cash flow, \(r_{f,t,h}\) is the risk-free discount rate for horizon \(h\), and \(\lambda_{t,h}\) is the risk premium investors demand for bearing uncertainty. Macro conditions enter both the numerator and the denominator.

Inflation and policy mainly push through the denominator. Higher inflation can raise expected policy rates and bond yields, so \(r_f\) rises. Recession risk and credit stress mainly push through both parts: expected cash flows fall and the risk premium \(\lambda\) rises. Labor and housing affect consumer income, credit losses, and domestic demand. External trade affects exporters, commodities, the dollar, and global earnings.

This is why the project doesn’t treat macro data as decoration. The FCI is a way to summarize whether the macro environment is raising the discount-rate burden, weakening cash-flow expectations, or increasing the required risk premium.

Stress Orientation

After standardization, we also need a sign convention. In this project, higher means more stress.

That convention is straightforward for variables like unemployment, jobless claims, inflation pressure, and policy rates. Higher values usually mean more macro pressure. For variables like industrial production, retail sales, payroll growth, housing activity, and confidence surveys, the direction is reversed. Higher growth is good, so lower growth is the stressful state.

For a raw series where high values are stressful, we keep the sign:

\[

s_{i,t}=z_{i,t}

\]

For a raw series where low values are stressful, we flip it:

\[

s_{i,t}=-z_{i,t}

\]

The final \(s_{i,t}\) is a stress-oriented macro signal. This lets us compare inflation, labor, housing, and growth in the same direction.

A useful example is industrial production. If industrial production is far above its historical expanding mean, the raw z-score is positive. But strong production isn’t recession stress, so the stress signal is negative. If production collapses during a recession, the raw z-score becomes negative and the stress signal becomes positive. That positive value then lines up with other stress variables like rising claims or falling surveys.

A Small Numerical Example of Stress Orientation

Suppose an industrial production series has an expanding mean of 100 and an expanding standard deviation of 5. If the latest value is 110, the raw z-score is:

\[

z_t=\frac{110-100}{5}=2

\]

But industrial production being two standard deviations above normal is usually not recession stress. For a growth variable, we flip the sign:

\[

s_t^{growth}=-2

\]

Now suppose a few months later industrial production falls to 90. The raw z-score is:

\[

z_t=\frac{90-100}{5}=-2

\]

After the sign flip:

\[

s_t^{growth}=2

\]

That positive value now means growth stress. The same stress orientation lets us average growth weakness with labor weakness, housing weakness, and policy pressure. Without the sign convention, the FCI would mix variables where positive means good with variables where positive means bad, and the index would become economically confused.

2) Setup and Reused Data Layer

The first code cells load the scientific Python stack, the project library, and the plotting settings. This part doesn’t need heavy interpretation. The important thing is that the project works at two frequencies:

Monthly macro frequency, where the raw economic indicators are transformed into macro signals and FCI models.

Daily or monthly market frequency, where ETF prices are used for allocation and performance testing.

For reproducibility, the data should be understood through the repo’s data-generation folders, not as isolated final files. Check the relevant folders inside the repo’s data folder. For this project, the important folders are the ones corresponding to the US macro factors, NFCI, sector ETFs, core cross-asset ETFs, Canadian macro factors, Canadian sector ETFs, and international hedging ETFs.

The sector and cross-asset ETF data has already appeared earlier in the series, so we keep it short here. The new and important part is the macro panel: what each group measures, how it becomes a stress signal, and how those signals are turned into regimes.

The raw macro factor panel runs from January 1990 to January 2026, with 433 monthly rows and 56 macro factors. That is a long enough span to include the early 1990s cycle, the dot-com recession, the 2008 crisis, the COVID shock, the 2022 inflation/rate shock, and the post-2023 normalization period.

The availability table tells us that not every series has the same sample. Some external trade series end in 2014. Some OECD survey series end in 2024. Many core macro series, such as CPI/PCE, PPI, import prices, oil, fed funds, and Treasury yields, run through 2026. This is why the project later builds block-level averages and coverage checks rather than requiring every raw input to be present at every date.

This is realistic macro data behavior. Macro datasets are messy because agencies revise series, discontinue series, add new survey formats, and report different variables at different frequencies. The goal isn’t to force a perfectly rectangular panel; the goal is to build a robust index that can still work when some inputs are unavailable.

Timing, Revisions, and Real-Time Discipline

Macro data has a timing problem that price data usually doesn’t have. Many macro variables are released with delays, then revised later. A payroll number, CPI print, GDP estimate, or retail-sales value may be different in the first release than in the final database. This project doesn’t fully reconstruct historical release calendars, but it still keeps an important real-time discipline: transformations use expanding history and allocation features are shifted before trading.

The expanding z-score prevents future distribution information from entering past signals. The one-month shift before allocation prevents the strategy from using a same-month macro reading as if it were known at the rebalance. That is a practical compromise for a notebook project.

A fully production-grade macro strategy would go further. It would use vintage macro data, release timestamps, nowcasting rules, and publication lags. But even without that, the project is much safer than computing full-sample z-scores and immediately trading same-month signals.

This timing discipline is why the strategy interpretation is more credible. The FCI isn’t just a historical chart; it is built in a way that approximates how a real investor could’ve used the information.

3) Real-Time Standardization Functions

Before building the macro blocks, we define a small transformation toolkit.

The most important function is the expanding z-score. For a series \(x_t\), the expanding mean and variance at time \(t\) are:

The implementation requires a minimum number of observations before the score is trusted. In this project the main US run uses a 60-month warmup, so the first valid score needs about five years of history. The score is also clipped, usually inside \([-5,5]\), because macro outliers can otherwise dominate an average. A pandemic collapse or oil shock is real information, but a single extreme value shouldn’t numerically drown every other variable in the block.

Two additional operations matter:

Level pressure, where we standardize the level of a variable.

Impulse pressure, where we standardize the recent change.

For a three-month change:

\[

\Delta_3 x_t=x_t-x_{t-3}

\]

and its stress score is the expanding z-score of \(\Delta_3 x_t\), possibly with a sign flip. This is how we separate a variable being high from a variable getting worse quickly.

Level, Impulse, Acceleration, and Diffusion

Many macro regimes are defined by both level and speed. Inflation at 4% is different if it is falling from 8% versus rising from 2%. Growth that is weak but improving is different from growth that is strong but decelerating fast.

That is why we build several signal types:

Signal type

Mathematical object

Economic meaning

Level

\(z(x_t)\)

Is the variable high or low relative to its own history?

Impulse

\(z(x_t-x_{t-3})\)

Has the variable moved unusually over the last three months?

Acceleration

\(z((x_t-x_{t-3})-(x_{t-3}-x_{t-6}))\)

Is the recent change itself speeding up or cooling?

Diffusion

share of variables above a stress threshold

Is stress broad across many indicators or concentrated in a few?

The diffusion idea is especially important. A single inflation series can spike because of one component. A broad inflation regime means many price measures are elevated together. Formally, if we have \(N\) stress-oriented indicators inside a group, the diffusion share is:

where \(c\) is the threshold, here around \(0.5\), and \(N_t\) is the number of available series at month \(t\). The diffusion share is then standardized through time. High diffusion means stress is not just intense; it is broad.

Show code

def expanding_zscore(series, min_obs=60, clip=5.0): series = pd.Series(series, dtype=float).replace([np.inf, -np.inf], np.nan) mean = series.expanding(min_periods=min_obs).mean() std = series.expanding(min_periods=min_obs).std(ddof=1).replace(0.0, np.nan) z = (series - mean) / stdreturn z.clip(-clip, clip) if clip isnotNoneelse zdef prefix_cols(data, prefixes): prefixes =tuple(prefixes)return [col for col in data.columns if col.startswith(prefixes)]def mean_z(data, columns, min_obs=60, sign=1.0):iflen(columns) ==0:return pd.Series(np.nan, index=data.index) z = data[columns].apply(lambda s: expanding_zscore(s, min_obs=min_obs))return sign * z.mean(axis=1, skipna=True)def change_z(data, columns, periods=3, min_obs=60, sign=1.0):iflen(columns) ==0:return pd.Series(np.nan, index=data.index) z = data[columns].diff(periods).apply(lambda s: expanding_zscore(s, min_obs=min_obs))return sign * z.mean(axis=1, skipna=True)def stress_share(data, columns, min_obs=60, threshold=0.5, sign=1.0):iflen(columns) ==0:return pd.Series(np.nan, index=data.index) z = data[columns].apply(lambda s: expanding_zscore(s, min_obs=min_obs)) events = sign * z > threshold share = events.where(z.notna()).mean(axis=1, skipna=True)return expanding_zscore(share, min_obs=min_obs)def plot_signal_group(data, title, ncols=2): cols =list(data.columns) nrows = math.ceil(len(cols) / ncols) fig, axes = plt.subplots(nrows, ncols, figsize=(7* ncols, 2.6* nrows), sharex=True) axes = np.array(axes).reshape(-1)for i, col inenumerate(cols): series = data[col].loc[data.index >= minimum_visible_date].dropna() series.plot(ax=axes[i], lw=1.2, color=colors[i %len(colors)]) axes[i].axhline(0.0, color="black", lw=0.7, alpha=0.4) axes[i].set_title(col, fontsize=9) axes[i].set_xlabel("") axes[i].grid(True, alpha=0.25)for ax in axes[len(cols):]: ax.set_axis_off() fig.suptitle(title, y=1.02, fontsize=11) plt.tight_layout() plt.show()return fig, axes

4) Macro Factor Groups

The macro panel is divided into economically meaningful groups. This grouping is one of the most important design choices in the project because the later FCI is only as good as the information blocks that enter it.

Fed funds, short rates, Treasury yields, curve variables

Monetary tightness and rate pressure

Growth

GDP, industrial production, retail sales, PMIs, ISM, leading indicators

Recession and demand stress when growth weakens

Labor

unemployment, jobless claims, payrolls, hours worked

Labor-market cooling and recession confirmation

Housing

permits, starts, sales, prices, builders’ survey

Rate-sensitive domestic demand stress

External trade

exports, imports, trade/current account balances

Global demand and external vulnerability

Surveys

consumer confidence, business confidence, sentiment surveys

Soft-data warnings and expectations pressure

The design uses both hard data and soft data. Hard data, like payrolls or industrial production, is slower but concrete. Soft data, like surveys, often moves earlier but can be noisy. Combining both helps the index respond to regime changes without letting one noisy survey dominate the whole system.

The Macro Blocks as a Regime Map

Before we build the first block, it helps to think of the seven blocks as a regime map rather than a list of variables.

Inflation and policy describe the nominal pressure side of the economy. Growth, labor, and housing describe the real activity side. External trade adds the global demand and currency-sensitive side. Macro breadth/conflict describes whether the pressure is localized or spreading.

A few common macro regimes can be described in this block language:

Regime

Inflation block

Policy block

Growth/labor blocks

Market interpretation

Goldilocks

low

low

low stress

equities supported, rates less threatening

Classic recession

low or falling

falling

high stress

bonds may help, defensives usually improve

Inflation shock

high

rising/high

mixed

commodities may help, bonds can fail

Stagflation

high

high

high stress

difficult for both equities and bonds

Liquidity crisis

mixed

high or unstable

rising stress

risky assets and credit usually reprice

This framing is important because the strategy later doesn’t only ask whether conditions are tight. It also asks what kind of tightness we have.

Inflation enters asset pricing through several channels at once.

First, it changes the discount rate because central banks raise policy rates when inflation is above target. Second, it changes real purchasing power and can compress household demand. Third, it changes profit margins because firms may face higher input costs before they can pass those costs through to consumers. Fourth, it changes the bond-equity correlation structure because bonds stop behaving like a clean recession hedge when inflation is the shock.

The level tells us whether inflation is high. The impulse tells us whether inflation has recently moved upward. The acceleration tells us whether the inflation impulse is speeding up.

Why Inflation Needs More Than One Measure

Inflation is not one object. CPI, core CPI, PCE, core PCE, PPI, import prices, export prices, and oil all measure different parts of the price system.

CPI is closer to the household cost-of-living basket. PCE is closer to the Federal Reserve’s preferred consumption deflator. Core versions remove food and energy to reduce noise, but they can lag energy-driven shocks. PPI measures producer input and output prices, so it can show cost pressure before it appears in consumer prices. Import prices connect inflation to the dollar and global supply chains. Oil captures a high-volatility but economically important input cost.

A broad inflation block prevents one inflation measure from dominating the story. If oil spikes but core inflation is stable, the diffusion component won’t confirm broad pressure. If CPI, core CPI, PCE, PPI, import prices, and oil all move together, diffusion rises and the FCI treats the inflation regime as more serious.

For asset allocation, broad inflation is more dangerous than narrow inflation. Narrow inflation can rotate between sectors. Broad inflation can force central bank tightening and change the entire discount-rate environment.

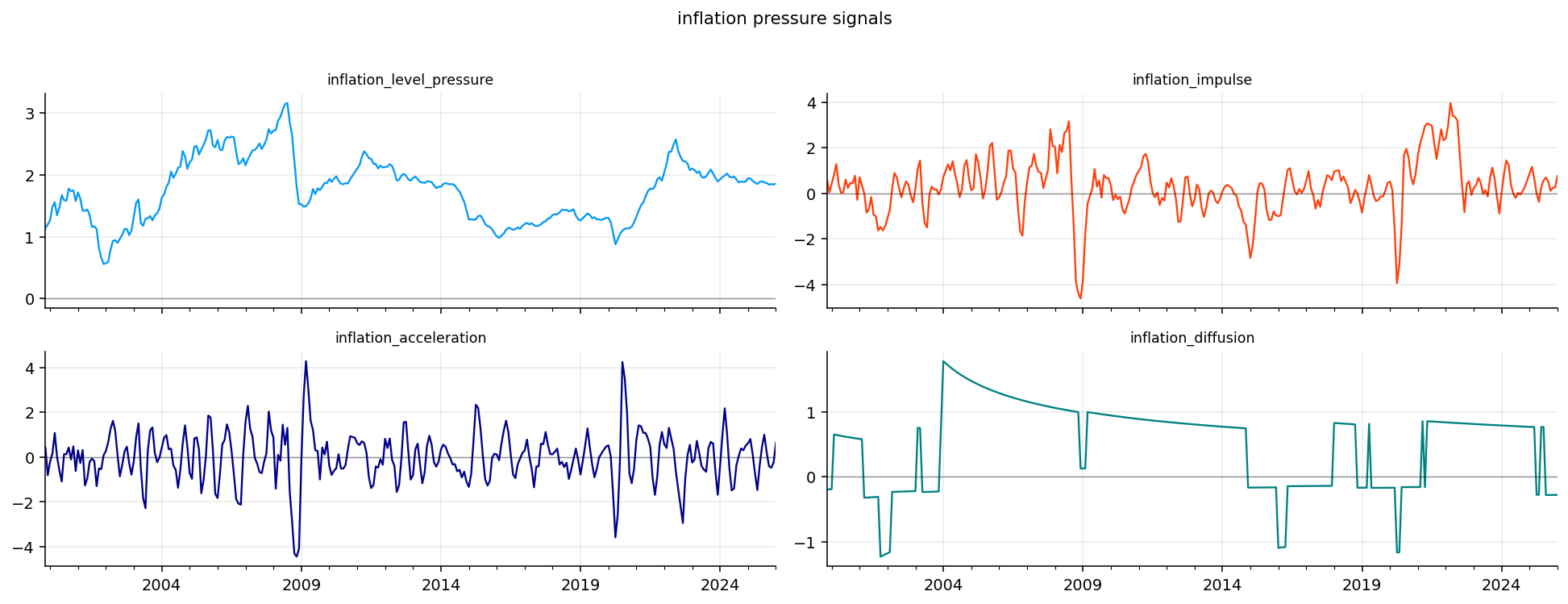

From the inflation plots, the strongest inflation-pressure episode is clearly the post-2021 inflation shock. The level pressure rises sharply and stays elevated for a long period, which matches the broad macro story after the pandemic: supply bottlenecks, energy pressure, fiscal demand, and later tighter labor markets.

The latest table is also informative. In January 2026, inflation level pressure is about 1.86, which means inflation-related variables are still high relative to their own history. The latest inflation impulse is about 0.76, and inflation acceleration is about 0.65, so the latest reading is not just a high-level story. There is also some renewed upward movement in the inflation block.

The diffusion component is negative at about -0.28. That tells us the pressure is not broad in the same way it was during the worst part of the 2021–2022 inflation episode. This distinction matters for markets. A high inflation level with low diffusion can mean inflation remains sticky in some components, while a high level with high diffusion signals a more dangerous broad price regime.

Inflation Regime Interpretation for Assets

Inflation affects sectors differently.

Energy and materials may benefit when inflation is commodity-driven because their revenues are directly linked to commodity prices. Gold can benefit when inflation reduces confidence in real purchasing power or when real rates are low. Financials can benefit from higher rates if the yield curve and credit cycle remain healthy, but they can suffer if policy tightening damages loan growth or credit quality.

Growth stocks usually dislike inflation-driven rate shocks because their valuations depend more heavily on long-dated expected cash flows. A higher discount rate hurts those distant cash flows more. If we write a simplified long-duration equity valuation as:

\[

P_t\approx\frac{CF_{t+H}}{(1+r)^H}

\]

then a change in \(r\) has a larger price effect when \(H\) is large. That is the duration logic behind growth-stock sensitivity to rates.

This is why the inflation block later supports inflation beneficiaries but penalizes some rate-sensitive sectors through the policy block. The model separates inflation pressure from policy pressure because markets don’t react to inflation alone. They react to inflation plus the central bank response.

6) Policy and Rate Pressure

Policy pressure measures the tightness of monetary conditions. The central bank affects markets through the short rate, but the market also prices policy through Treasury yields and the yield curve. A higher policy-rate block generally means financing is more expensive and duration-sensitive assets face more pressure.

The basic policy tightness signal is an average of standardized rate-related variables:

This captures the market impact of a fast policy move. A rate level can be high but stable. A rate shock means investors are being forced to reprice discount rates quickly.

The real-rate squeeze combines policy pressure with inflation impulse:

When this is high, policy is tight relative to recent inflation momentum. When it is low or negative, inflation is moving faster than the policy block, so real tightening may be less forceful.

Policy Catch-Up Risk

The policy catch-up component tries to detect periods where inflation is high but policy has not fully caught up. It is based on the positive gap:

\[

g_t=\max(I_t^{level}-P_t^{tight},0)

\]

and then this gap is standardized:

\[

\text{catchup}_t=z(g_t)

\]

The logic is simple. If inflation pressure is high and policy tightness is still low, the market may eventually price future hikes or a delayed tightening campaign. That is a dangerous setup for long-duration bonds and expensive growth equities.

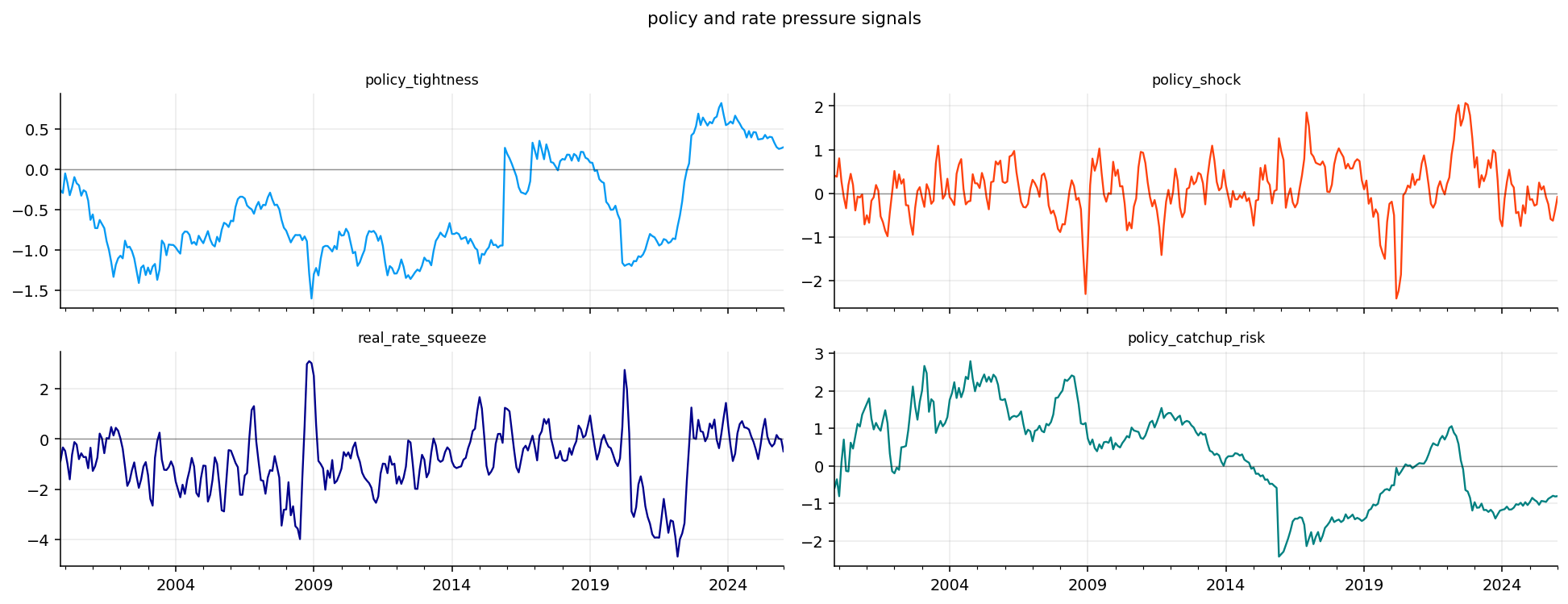

The latest policy table shows a different situation from the 2022 tightening shock. Policy tightness is only around 0.28, policy shock is slightly negative, and policy catch-up risk is around -0.81. This says rate pressure is no longer in the active shock phase. The latest stress is more about inflation still being elevated than about policy rapidly tightening.

That difference matters for sector interpretation. If policy pressure were strongly positive, rate-sensitive assets like utilities, real estate, and long-duration growth would face a direct discount-rate headwind. With policy pressure easing, the macro issue becomes more about sticky inflation and whether growth can absorb it.

Real Rates and the Policy Transmission Channel

A policy rate is a nominal rate. What matters for spending and investment is often the real rate, roughly nominal rate minus expected inflation:

\[

r_t^{real}\approx i_t-\pi_t^e

\]

where \(i_t\) is the nominal policy rate and \(\pi_t^e\) is expected inflation. When real rates rise, borrowing becomes expensive after inflation, and financial conditions tighten. Housing, private investment, leveraged companies, and long-duration assets become more vulnerable.

The project doesn’t directly estimate expected inflation. Instead, it uses the relationship between policy tightness and inflation impulse as a practical signal. If policy tightness is high relative to current inflation impulse, the real-rate squeeze becomes positive. If inflation impulse is running ahead of policy, the squeeze becomes lower.

This is a simplified macro proxy, but it captures a useful idea: the same nominal policy rate can mean different things depending on inflation momentum. A 5% policy rate with collapsing inflation is tight. A 5% policy rate with inflation accelerating can feel less restrictive in real terms until policy catches up.

Policy pressure enters sector returns through both funding costs and discount rates.

Utilities and real estate often behave like bond proxies because they have stable cash flows and high sensitivity to yields. When rates rise, their dividend yields become less attractive and their debt costs rise. Technology and consumer discretionary can also be rate-sensitive because a large share of their value depends on future growth expectations.

Banks and financials are more complicated. Higher rates can increase net interest margins, but if rates rise during a growth slowdown, credit losses and funding stress can dominate. That is why the strategy later applies an extra penalty to XLF when policy pressure and growth recession stress are both positive:

The multiplication matters. Policy pressure alone is not always bad for banks. Growth stress alone is not always enough. The combination is dangerous because loan demand weakens, credit losses rise, and funding conditions tighten together.

7) Growth and Recession Signals

Growth data is sign-flipped because weak growth is the stress state. If a growth variable \(g_t\) is high relative to history, its raw z-score is positive, but its stress score is negative:

\[

s_t^{growth}=-z(g_t)

\]

This means positive growth stress corresponds to falling or weak growth, while negative growth stress corresponds to strong growth.

The growth block includes hard activity data such as production and sales, plus survey and leading-indicator information. We build:

and growth breadth stress from the share of growth indicators that are weak. If many indicators are simultaneously below their own trend, the breadth signal rises.

This group is critical because inflation and policy stress do not always become equity stress unless growth deteriorates. A high-rate environment with resilient growth can still support cyclicals and earnings. A high-rate environment with collapsing growth is much more dangerous.

Hard Data Versus Soft Data

Growth analysis becomes more useful when we separate hard and soft data.

Hard data includes industrial production, retail sales, payrolls, and real activity measures. These variables describe actual spending and production. They are slower, sometimes revised, and often confirmed after the economy has already moved.

Soft data includes surveys such as consumer confidence, business confidence, PMIs, and sentiment measures. These variables describe expectations and reported conditions. They can move earlier, but they can also overreact to news, politics, inflation frustration, or media attention.

The project includes both because markets respond to both. Soft data can move valuations and risk appetite quickly. Hard data confirms whether the earnings and labor consequences are actually happening.

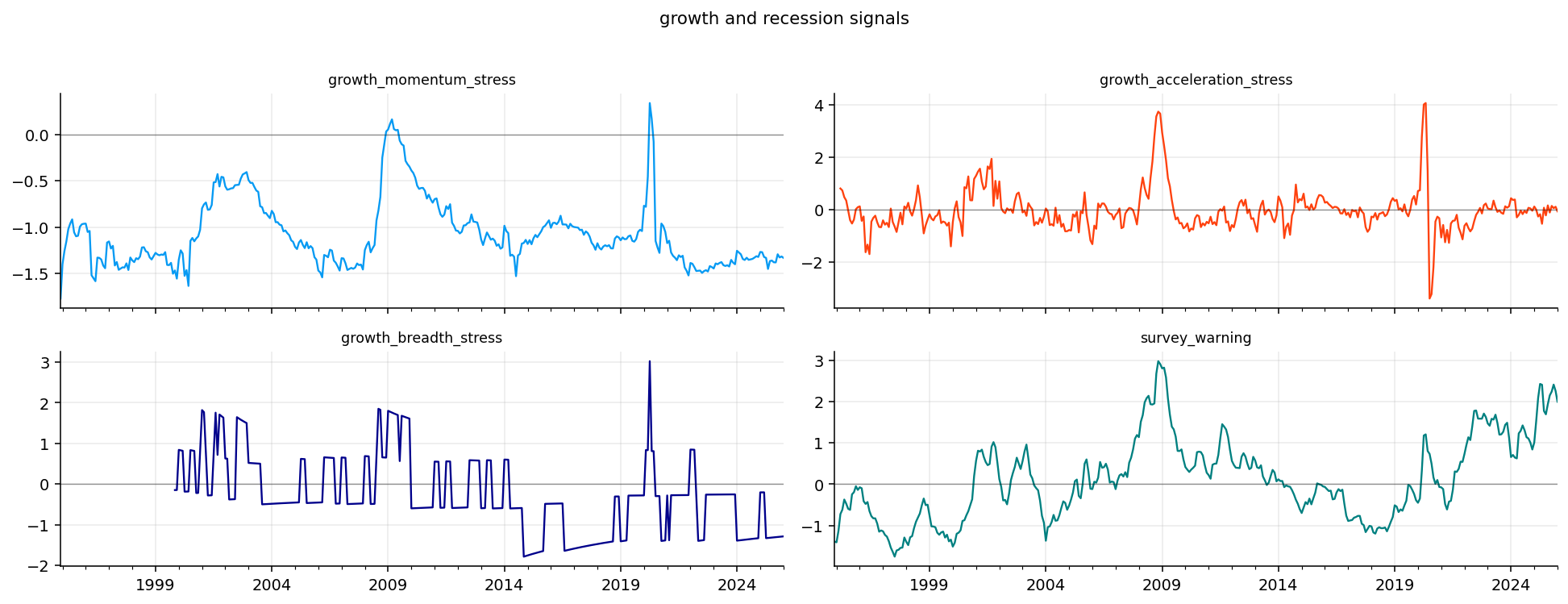

A useful interpretation rule is this: when hard data and soft data agree, the macro signal is stronger. When they disagree, the regime is mixed. In the latest US output, hard growth stress is negative, but survey warning is strongly positive. That is exactly a mixed-growth regime.

The latest growth table gives a very useful mixed signal. Growth momentum stress is around -1.33 and growth breadth stress is around -1.28, which means the hard growth data is still strong relative to its historical distribution. Growth acceleration stress is close to zero, so the immediate hard-data deterioration is limited.

But the survey warning is around 2.00 in January 2026 and was even higher in late 2025. This says soft data is much more pessimistic than hard activity data. That kind of gap is common around turning points: surveys react quickly to uncertainty, inflation frustration, politics, financial tightening, or business caution, while hard data may remain stable until spending and hiring actually change.

For portfolio use, this means we shouldn’t label the environment as a simple recession regime. Hard data is not showing strong recession stress. Surveys are warning that expectations are fragile. A strategy that uses only realized growth data may stay too risk-on, while a strategy that uses only surveys may become too defensive.

Growth Stress and Earnings

Growth stress matters because equity prices ultimately depend on future earnings. At a broad level:

Growth weakness hits revenues first. If companies sell fewer goods or services, revenue expectations fall. If demand weakens while costs remain high, margins compress too. This is why growth recession stress can affect both cyclical sectors and broad equity beta.

Cyclicals like industrials, discretionary, materials, and financials are usually most exposed to growth stress. Defensive sectors like staples and health care have more stable demand, so they tend to hold up better when growth deteriorates.

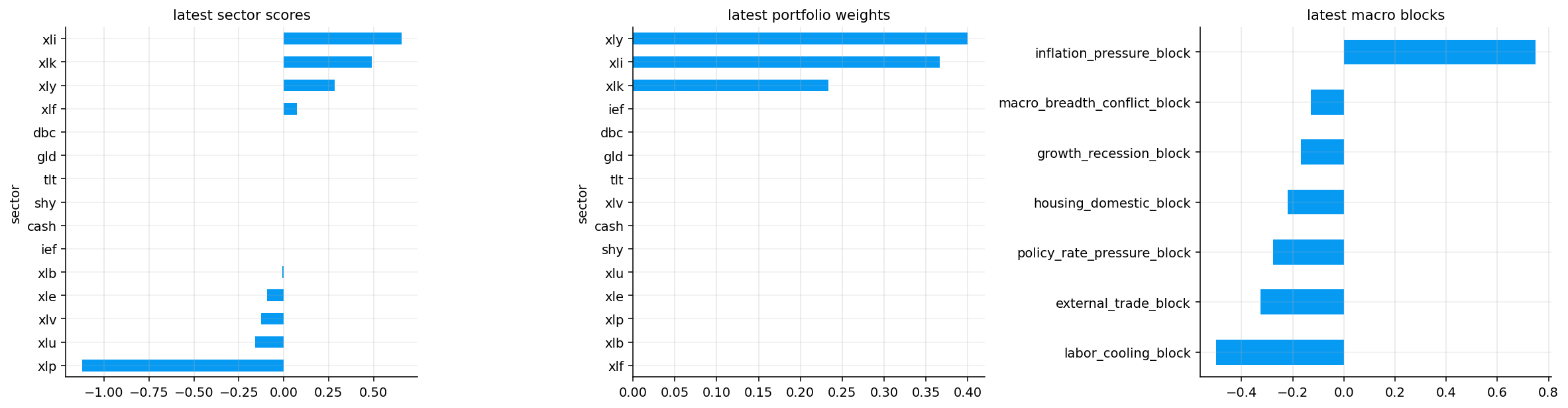

The strategy later reflects this relation. Cyclical sectors receive support when FCI percentile is low and growth stress is low. Defensive sectors receive support when FCI percentile or growth stress rises. That is not arbitrary sector timing; it comes directly from the macro cash-flow channel.

8) Labor Cooling and Sahm Pressure

The labor market is often the most important confirmation layer in macro analysis. Recessions usually become obvious when labor deteriorates. Equity markets may fall before unemployment rises, but once unemployment and claims move, the recession signal becomes much more reliable.

The labor block combines three types of information:

Unemployment level, where higher unemployment is stress.

Claims, where higher initial or continuing claims are stress.

Jobs and hours, where weak payrolls or hours are stress, so the sign is flipped.

The combined labor cooling signal can be written conceptually as:

The project also computes a Sahm-style pressure variable. The Sahm rule compares the recent unemployment rate with its recent low. A simplified version is:

where \(u_t\) is unemployment. The project standardizes this gap rather than using one fixed recession threshold. Rising Sahm pressure means unemployment has moved up enough relative to its recent low to look economically important.

The labor plots show the large labor stress events clearly: the 2008 crisis, the COVID shock, and smaller labor-cooling periods. The latest values are not recession-like. Labor cooling is around -0.92, and Sahm pressure is slightly negative around -0.08.

That means the labor block is currently supporting the idea that the economy is not in a broad labor-market downturn. The labor market may be cooling at the margin in some recent months, but the aggregate signal is not close to the kind of stress seen in 2008 or 2020.

This is economically important because labor is the bridge between macro data and earnings. If labor is stable, households still have income, defaults stay contained, and consumer sectors can keep spending support. If labor breaks, the macro environment becomes much more dangerous for equities, especially financials, discretionary, industrials, and credit-sensitive exposures.

Labor as a Regime Confirmation Variable

Labor data is often late, but it is powerful. Markets can sometimes ignore weak surveys if employment stays strong. It is harder to ignore rising unemployment and rising claims because those variables directly affect income, defaults, and consumption.

Labor also changes the central bank reaction function. If inflation is high and labor is strong, the central bank has more room to stay tight. If inflation is falling and labor is weakening, policy can shift toward easing. This is why labor matters for both cash flows and rates.

The Sahm-style variable is useful because it focuses on changes from a recent low rather than the absolute unemployment rate. A country can have a low unemployment rate and still enter recession if unemployment has risen sharply from its trough. The gap formulation catches that turning-point behavior.

In the latest US data, Sahm pressure is not elevated. That weakens the recession case even though surveys are warning. The labor block is therefore a stabilizing input in the latest macro state.

9) Housing, Domestic Demand, and External Trade

Housing is rate-sensitive and forward-looking. Mortgage rates affect affordability quickly, and housing activity often weakens before the broader economy. The housing block combines the level and impulse of housing indicators, then adds a rate-squeeze component.

This catches the situation where housing is weakening while rates are still restrictive. That mix can be especially painful because housing is a large transmission channel for monetary policy.

External trade is separate. External demand stress captures weakening exports and imports, while external vulnerability captures pressure from trade or current-account balances. For a large domestic economy like the US, external trade may be less dominant than for Canada, but it still matters through global demand, dollar strength, commodities, and multinational earnings.

The housing plots show a strong stress episode during the housing bubble collapse and the 2008 crisis. That is exactly what we want: housing stress should become visible before and during the financial crisis.

The latest housing values are mostly negative: housing impulse stress is around -0.39 and housing rate squeeze is around -0.05. This says housing is not currently driving the broad macro stress index in the same way it did before 2008. Rate pressure exists, but the combined housing stress block is not elevated in the latest reading.

External demand stress is also negative in the latest table, around -0.50, while external vulnerability is slightly negative. So the latest US macro picture is not one of trade-driven weakness either. For the US section, the main current pressure is inflation, while growth, labor, housing, and external trade are not broadly stressed.

Housing and Trade as Transmission Channels

Housing is one of the main channels through which rates affect the real economy. Higher mortgage rates reduce affordability, lower transaction volumes, pressure construction activity, and can eventually affect employment in construction, real estate services, home improvement, and credit.

where \(i_m\) is the monthly mortgage rate and \(n\) is the number of monthly payments. When the mortgage rate rises, the payment rises nonlinearly for a fixed loan size. That is why housing can weaken quickly when rates jump.

External trade matters through global demand and currency channels. A strong dollar can pressure exporters and emerging-market demand, while weak global demand can reduce revenues for multinational firms. For Canada, external trade is even more central because commodities and US demand play a larger role.

These blocks are not always the largest drivers, but they give the FCI more economic coverage than an index built only from inflation, rates, and unemployment.

10) Breadth, Severe Breadth, Stagflation, and Goldilocks

After building the first-level signals, we build aggregate macro-state signals. These are not tied to one specific economic category. They measure how stress is distributed across the whole macro system.

The stress breadth signal begins with the share of first-level signals above a stress threshold:

This breadth logic is useful because regimes differ by concentration. A single inflation pressure variable above one standard deviation is not the same as inflation, policy, labor, housing, and growth all above one standard deviation.

The stagflation pressure signal averages the main conflict variables:

High stagflation pressure means inflation and rates are high while growth is weak. That is one of the worst environments for balanced portfolios because equities face earnings pressure and bonds face inflation/rate pressure.

Goldilocks support is the opposite type of macro environment. It is built from inflation pressure, policy pressure, growth stress, and labor cooling:

Higher goldilocks support means inflation is not pressuring policy, rates are not tight, growth stress is low, and labor is healthy. In that environment, risk assets usually get support because earnings can grow while discount-rate pressure is limited.

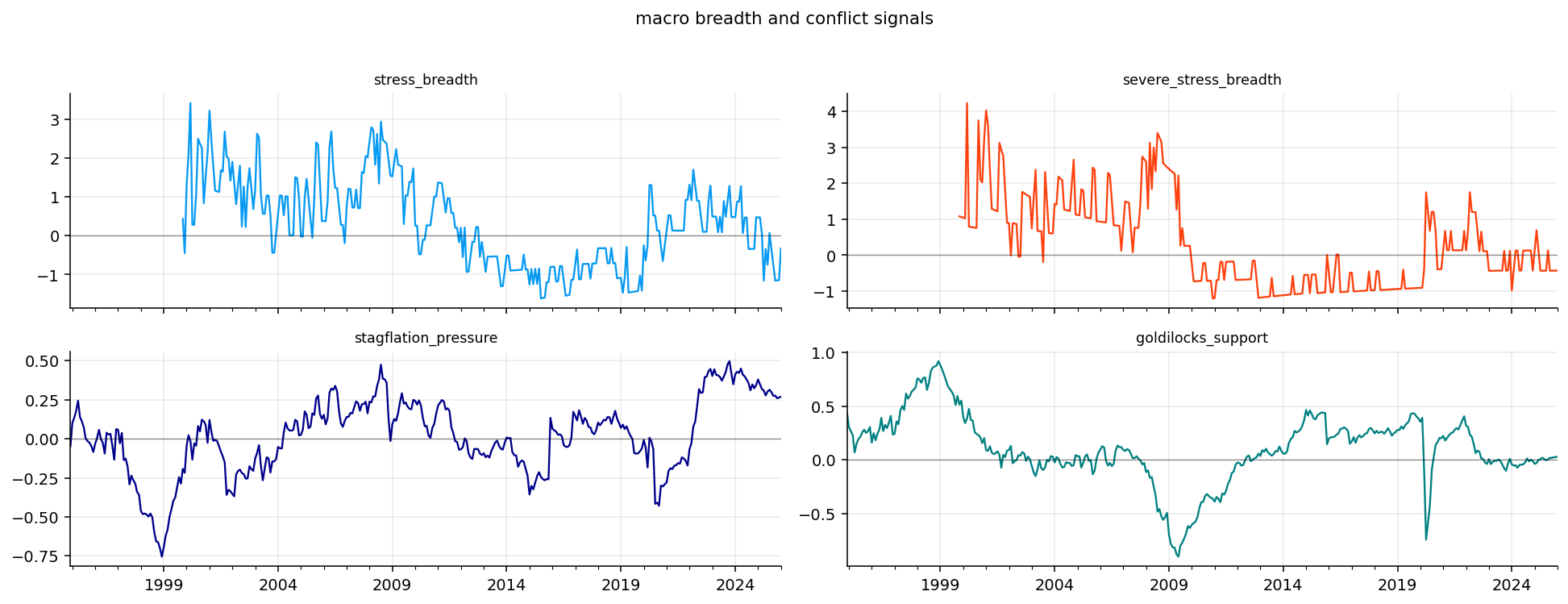

The latest breadth table shows stress breadth is negative, severe stress breadth is negative, and stagflation pressure is only around 0.27. Goldilocks support is near zero. The interpretation is a mixed but contained macro environment: inflation is still high, but stress is not broad across the whole economy.

That is exactly the type of state where a macro model can help. Pure momentum might keep buying what has worked. Pure defensive allocation might overreact to inflation. A block-level FCI can say: inflation pressure exists, but broad recession stress is not yet confirmed.

where the blocks are inflation pressure, policy/rate pressure, growth recession, labor cooling, housing/domestic demand, external trade, and macro breadth/conflict.

Each block is an average of related signals. For example:

The same logic applies to the other groups. Averaging reduces noise because one macro variable can be revised, delayed, or distorted. The block is meant to capture the common stress inside a category.

A block-level FCI has two advantages:

It remains interpretable. We can explain whether the index is high because of inflation, labor, growth, or housing.

It becomes statistically more stable. PCA, PLS, and logistic models work better on seven economic blocks than on dozens of noisy raw macro variables.

After coverage filtering, the analysis starts in December 1994 and runs to January 2026, giving 374 monthly observations. All seven blocks are available across the analysis sample, which is important because the FCI models later compare block combinations through time.

The availability table shows that most first-level signals and all block variables have full coverage inside the analysis window. Some inputs like policy catch-up risk, stress breadth, and severe stress breadth have fewer observations because they need additional warmup history. But once blocks are formed, the final macro state is complete.

This is a strong design choice for macro work. We let raw-series availability be uneven, but we require enough block coverage before the FCI is considered valid. That avoids making early-sample FCIs from only one or two macro categories.

Coverage Scores and Why We Keep Blocks Stable

Coverage is a quiet but important part of macro modeling. If a macro index changes because the economy changed, that is useful. If it changes because the available variable set changed, that is a data artifact.

The analysis keeps rows where at least six blocks are available and enough raw series are present. This protects the FCI from early-sample distortion. If only inflation and policy were available in early years, the FCI would look like an inflation/rate index rather than a broad financial conditions index.

The stable block coverage from 1994 onward is therefore a major strength of the dataset preparation.

12) ETF and NFCI Inputs

The market data section loads US sector ETFs, defensive assets, and signal assets. The sector ETFs are used later for allocation. The defensive assets include cash, short/intermediate/long Treasuries, gold, and commodities. The signal assets include broad equity, growth equity, small caps, credit, and the dollar.

We don’t re-explain these ETFs here because the sector and cross-asset data has already appeared earlier. The important point is how they are used:

Sector ETFs let us test whether macro regimes line up with sector performance.

Defensive assets let the strategy reduce risky sector exposure when the FCI tightens.

Signal assets support the broader allocation environment, but the macro blocks are the main new information layer.

We also load the external NFCI series. It acts as a benchmark financial-conditions index. Comparing our index with NFCI is useful because it tells us whether our macro-built FCI agrees with an established external stress gauge during major crises.

nfci_raw = pd.read_csv(nfci_path)nfci_raw.columns = [str(col).lower() for col in nfci_raw.columns]nfci_raw["date"] = pd.to_datetime(nfci_raw["date"], errors="coerce")nfci = nfci_raw.dropna(subset=["date"]).set_index("date").sort_index().drop(columns=["date"], errors="ignore")nfci = nfci.apply(pd.to_numeric, errors="coerce")nfci_month = nfci.groupby(nfci.index.to_period("M")).last()nfci_month.index = nfci_month.index.to_timestamp("M")nfci_month = nfci_month.loc[nfci_month.index >= macro_start]

The ETF coverage table confirms that all US sector ETFs start in 1999 and run through June 2026. Defensive ETFs start later: SHY, IEF, TLT, and LQD begin around 2002, GLD begins in 2004, DBC starts in 2006, and HYG/UUP start in 2007.

That coverage pattern matters for allocation. The strategy can run sector-only from the late 1990s, but a full defensive sleeve with gold and commodities becomes available later. The project handles this by using available assets at each date and by reporting a separate full-defensive-window performance table.

Cash is included as a synthetic defensive asset using a monthly risk-free rate assumption. That matters because a macro strategy needs somewhere to go when risk is unattractive and bond/commodity ETFs are unavailable or unsuitable.

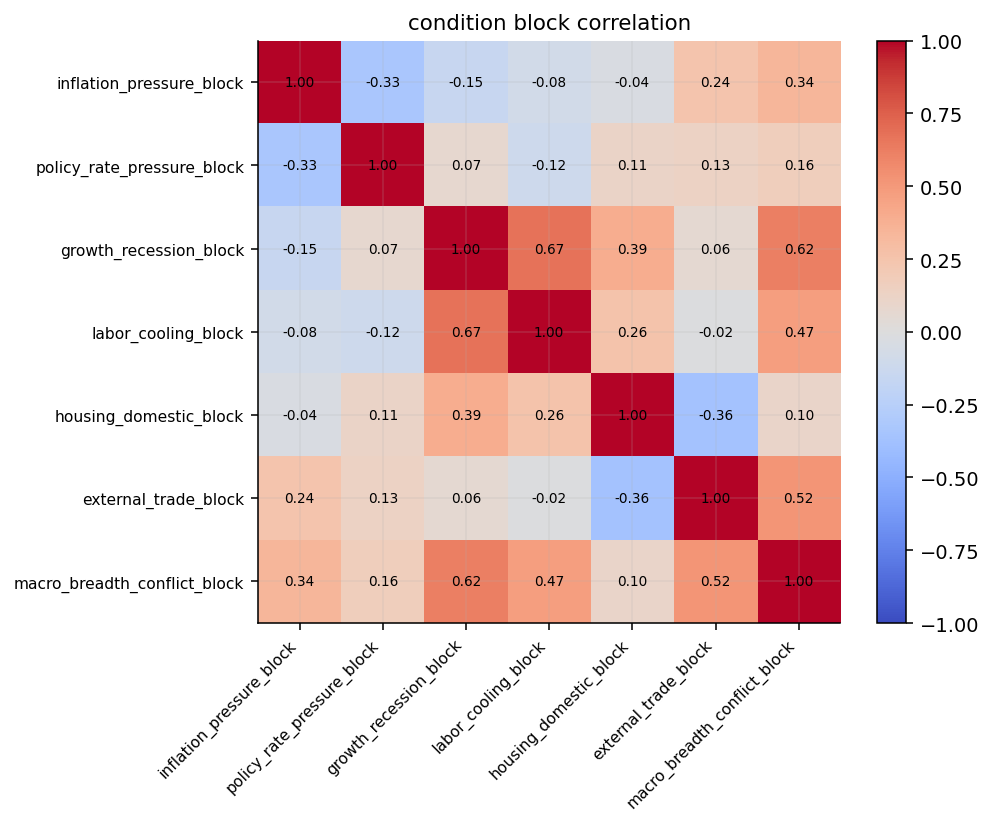

13) Block Correlations and Macro Structure

The block correlation heatmap checks whether the macro blocks are truly different. If every block were almost perfectly correlated, then a seven-block FCI would mostly be pretending to be diversified. If correlations are moderate and economically sensible, the blocks are adding different regime information.

The heatmap shows several meaningful relationships.

Inflation and policy pressure have a positive relationship, around 0.41. That makes sense: when inflation rises, policy and yields tend to rise. Growth recession and labor cooling are strongly related, around 0.71, because labor usually deteriorates when growth weakens. Growth recession and housing stress also have positive correlation, around 0.52, consistent with housing acting as a recession-sensitive domestic-demand channel.

External trade has weaker relationships with most domestic blocks. That is useful because it gives the FCI an external dimension instead of just repeating domestic growth and labor information. Macro breadth/conflict is positively related to several blocks because it measures whether stress is spreading.

The heatmap supports the block design. The blocks are connected enough to represent one macro system, but different enough to justify separate interpretation.

14) Recent Macro Blocks and Historical Conflict Peaks

The recent block table shows the last 12 months of the macro state. In January 2026, the largest positive block is inflation pressure, around 0.75. Policy pressure is negative, growth recession is negative, labor cooling is negative, housing stress is negative, external trade is negative, and macro breadth/conflict is slightly negative.

The recent picture is therefore not a broad stress regime. Inflation pressure remains the main concern, while the rest of the macro system is not confirming a recessionary shock.

The historical top macro-breadth/conflict readings are concentrated around 2000–2001 and 2008. That is exactly what we want from a breadth/conflict block. It becomes high when many macro categories start sending stress information at the same time. A high conflict/breadth reading is usually more important than a single block spike because it tells us the stress has spread across the macro system.

Show code

selected_dates = ["2008-10", "2020-03", "2022-09", str(macro.index.max().date())[:7]]contribution_rows = []for text in selected_dates: date = pd.to_datetime(text).to_period("M").to_timestamp("M") loc = macro.index.searchsorted(date, side="right") -1 date = macro.index[loc]for block, value in macro.loc[date, block_cols].items(): contribution_rows.append({"date": date, "block": block, "value": value})block_contribution_table = pd.DataFrame(contribution_rows).pivot(index="date", columns="block", values="value")display(block_contribution_table.round(2))

block

external_trade_block

growth_recession_block

housing_domestic_block

inflation_pressure_block

labor_cooling_block

macro_breadth_conflict_block

policy_rate_pressure_block

date

2008-10-31

0.47

1.66

0.71

-1.24

2.05

1.46

0.71

2020-03-31

-0.82

0.87

-0.13

-0.60

0.52

-0.17

-0.79

2022-09-30

-0.11

-0.01

-0.06

-0.18

-0.82

0.28

0.78

2026-01-31

-0.32

-0.17

-0.22

0.75

-0.50

-0.13

-0.28

15) Crisis Block Contributions

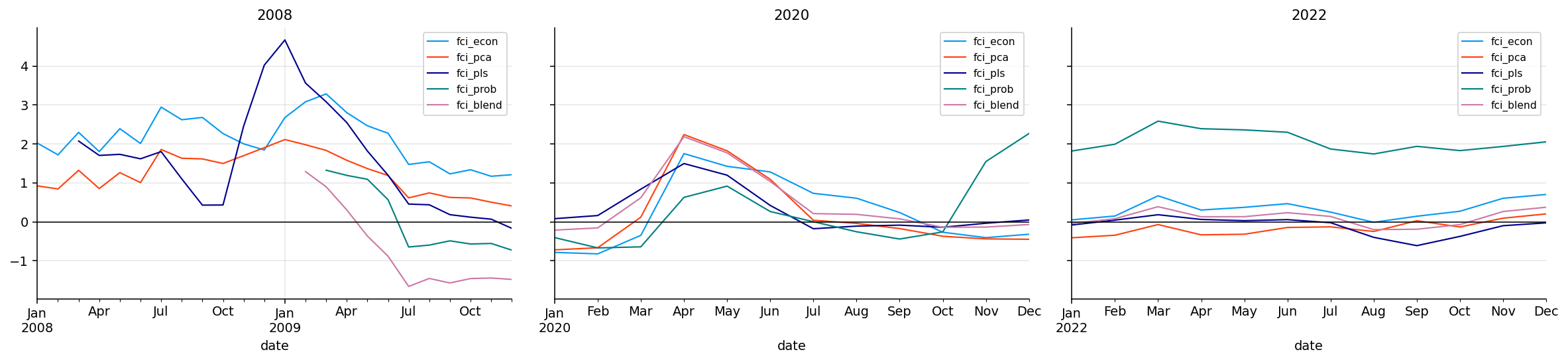

The crisis contribution table is one of the most useful macro diagnostics in the project because it explains why each stress period is different.

In October 2008, the stress is broad and classic recessionary. Labor cooling is very high at 2.05, growth recession is 1.66, macro breadth/conflict is 1.46, housing/domestic stress is positive, policy/rate pressure is positive, and external trade stress is positive. Inflation pressure is negative because the crisis was deflationary rather than inflationary.

In March 2020, growth recession is positive and labor cooling is positive, but policy pressure is strongly negative because policy was easing aggressively. Inflation pressure is also negative. This matches the COVID shock: a sudden real-economy collapse with emergency policy support.

In September 2022, policy/rate pressure is the main positive block at 0.78, while the growth and labor blocks are not strongly stressed. This captures the rate-shock nature of 2022. The macro pain came more from inflation and policy repricing than from a classic labor-led recession.

In January 2026, inflation pressure is positive, but most other blocks are negative. The macro condition is mixed rather than crisis-like.

Why We Need More Than One FCI

A macro index is a model, and every model has a bias.

An economic-weighted index is stable and explainable, but its weights are chosen before seeing the data relationship. A PCA index is data-driven and long-history friendly, but it chases the largest common variation, which may not always be the most market-relevant variation. A supervised PLS index targets future stress, but it can overfit the few crisis episodes in the sample. A logistic stress probability gives a clean high-risk interpretation, but it compresses the target into a binary label.

Using several FCIs lets us see whether the macro conclusion is robust. If all models say conditions are tight, the message is strong. If only supervised models say tight while economic and PCA models are neutral, the interpretation becomes more cautious.

This multi-model design is especially important in macro because we only have a few true crisis episodes. A model that looks excellent on three recessions may simply be memorizing the structure of those three events. Comparing model families helps reduce that risk.

16) The FCI Modeling Layer

Once the seven blocks are built, we create multiple FCI models. Each model answers a different statistical question.

where each block is stress-oriented. We want a scalar index:

\[

F_t=f(B_t)

\]

where higher \(F_t\) means tighter conditions.

The project builds five versions:

Model

Main idea

What it can do well

Economic FCI

Weighted block average

Interpretable and stable

PCA FCI

First common statistical factor

Finds the dominant co-movement in blocks

PLS FCI

Supervised factor targeting future stress

Learns which block combinations predict market stress

Probability FCI

Logistic probability of high future stress

Produces a stress-likelihood style signal

Blend FCI

Weighted mixture of PLS, PCA, and economic FCI

Combines supervised and unsupervised information

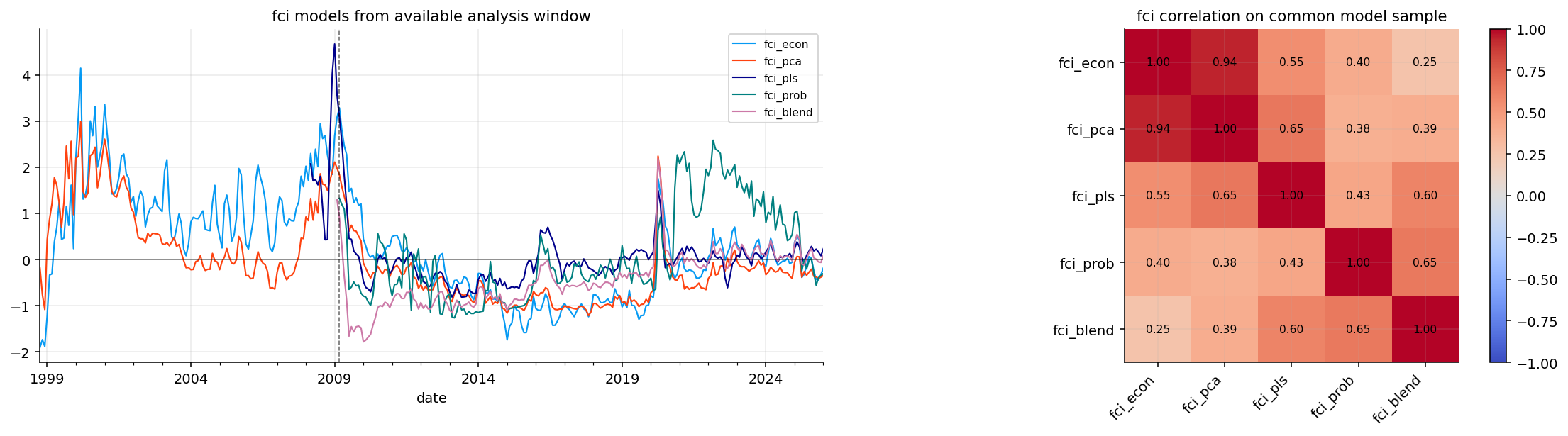

We don’t pick one model immediately. We compare them through future stress tests, crisis behavior, and external NFCI validation.

Rolling Percentiles

The raw FCI value is useful, but the percentile is often easier to interpret. A value of \(F_t=1.2\) means something only relative to the model’s own distribution. The rolling or expanding percentile asks:

where \(n_t\) is the number of past valid FCI observations. A percentile of 0.80 means the current FCI is tighter than about 80% of its own history up to that point.

This matters for allocation. We can use the percentile to gate risk:

Below 0.40: conditions are relatively easy or neutral.

Around 0.40 to 0.60: conditions are mixed.

Above 0.60 or 0.80: conditions are tight enough to justify reducing risky exposure.

Percentiles help compare different FCI models even when they have different raw scales.

17) Economic-Weighted FCI

The economic FCI is the most transparent model. We assign weights to the seven blocks and compute a weighted average:

The denominator is important because it handles missing block values. If one block is unavailable at some date, the model renormalizes the available weights instead of treating the missing value as zero.

The weights are economically motivated. Inflation, policy, and growth receive the largest weights because they are the primary macro drivers of discount rates, earnings, and risk appetite. Labor, housing, external trade, and macro breadth/conflict receive smaller but still meaningful weights.

The advantage is interpretability. If the economic FCI rises, we know exactly which blocks contributed. The weakness is that the weights are chosen by economic reasoning rather than estimated from data, so it may miss relationships that change across regimes.

This score is then sign-aligned so that higher values correspond to higher average stress. Without sign alignment, PCA can flip signs because both \(v_1\) and \(-v_1\) explain the same variance.

Financially, PCA is asking: what is the dominant common macro pressure running through the blocks? During a broad crisis, many blocks move together, so PC1 can become a clean stress factor. During a narrow shock, like inflation without labor stress, PCA may be less aggressive because not all blocks agree.

PCA Loadings Intuition Without Overcomplicating It

Even when we don’t print loadings in this section, the PCA score has a clear interpretation. The first principal component is a weighted average of standardized blocks:

Each loading \(v_{1,j}\) tells us how much block \(j\) contributes to the dominant common macro factor. If crisis periods make growth, labor, housing, and breadth move together, PCA will often assign similar signs to those blocks. If inflation behaves differently from classic recession blocks, its loading can be smaller or even different depending on the sample.

The sign alignment step compares the historical PCA score with average stress. If the correlation is negative, we multiply the score by \(-1\). This doesn’t change the statistical content, but it makes interpretation consistent: higher PCA FCI means tighter conditions.

This is one of the cleanest uses of PCA in the project series. We are not trying to forecast with dozens of components. We are extracting the first macro stress factor and checking whether it lines up with crises and future risk.

Show code

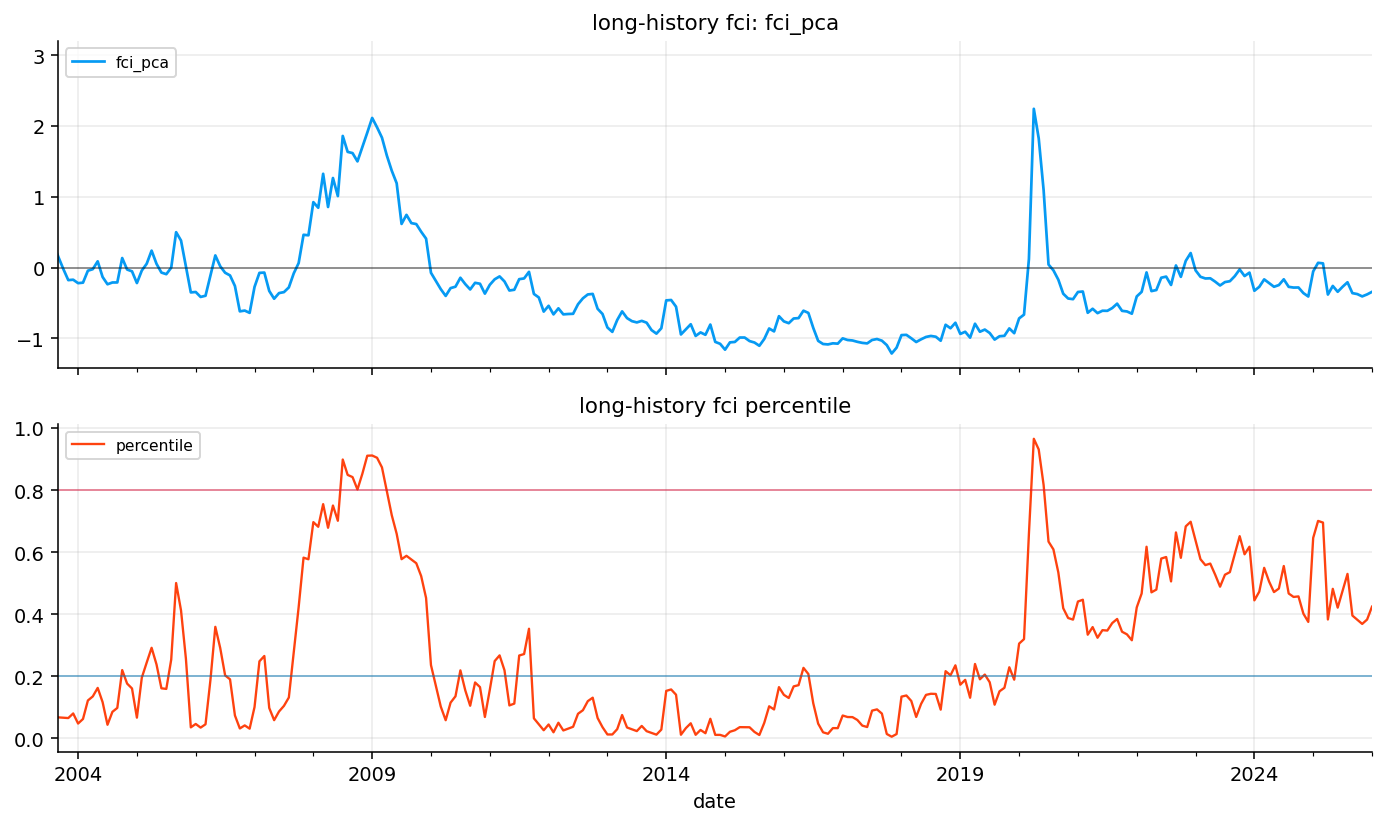

def pca_index(blocks, min_obs=60, min_cols=6): out = pd.Series(np.nan, index=blocks.index, name="fci_pca") average_stress = blocks.mean(axis=1, skipna=True)for date in blocks.index: hist = blocks.loc[:date] good_cols = [col for col in blocks.columns if hist[col].notna().sum() >= min_obs] row = blocks.loc[date, good_cols] good_cols = [col for col in good_cols if np.isfinite(row.get(col, np.nan))]iflen(good_cols) < min_cols:continue sample = hist[good_cols].dropna(how="any")iflen(sample) < min_obs:continue scaler = StandardScaler() train = scaler.fit_transform(sample) model = PCA(n_components=1) model.fit(train) current = scaler.transform(blocks.loc[[date], good_cols]) score =float(model.transform(current)[0, 0]) hist_score = pd.Series(model.transform(train)[:, 0], index=sample.index) align = pd.concat([hist_score, average_stress.reindex(sample.index)], axis=1).dropna()iflen(align) >12and align.iloc[:, 0].corr(align.iloc[:, 1]) <0: score =-score out.loc[date] = scorereturn zscore(out, 12).rename("fci_pca")fci_pca_full = pca_index(macro_full[block_cols], 36, 6)fci_pca = fci_pca_full.reindex(macro.index)

19) The Future Stress Target

The supervised models need a target. We define future stress from the next three months of SPY behavior. The target combines three pieces:

Future 3-month return, with losses treated as stress.

Future 3-month volatility.

Future 3-month maximum drawdown, with deeper drawdowns treated as stress.

High \(Y_t\) means future returns were weak, future volatility was high, and future drawdowns were severe. This is the market outcome we want the FCI to anticipate.

Why the Target Combines Return, Volatility, and Drawdown

A future stress target based only on return would miss important market states. Sometimes returns are mildly positive but volatility is high. Sometimes returns recover by month-end, but the path includes a severe intra-window drawdown. A risk manager cares about the path, not only the endpoint.

That is why the target combines three dimensions.

The return term captures realized direction. The volatility term captures uncertainty and choppiness. The drawdown term captures path pain. Together, they describe the kind of future environment that a macro FCI should warn about.

For example, if SPY loses 2% over three months with low volatility and shallow drawdown, the stress target may only be mildly elevated. If SPY ends flat but falls 8% inside the window and volatility spikes, the target can still be high. That makes the supervised FCI more aligned with portfolio risk than a simple next-return forecast.

Embargo and Lookahead Control

When we train supervised FCI models, we need to avoid leaking future information. The target uses returns from the next three months, so we apply an embargo. At date \(t\), training only uses observations whose target window ends before the current date.

Conceptually, for a current month \(t\), the training sample is:

\[

\mathcal{T}_t=\{s: s<t-3\text{ months}\}

\]

This avoids using a target that overlaps with the period we are trying to predict.

This detail is important because macro signals are slow moving. Without an embargo, nearby observations can share future return windows and make the supervised model look more predictive than it really is. The project is careful about this by training PLS and logistic probability models with a three-month gap.

Supervision Changes the Meaning of the Index

The unsupervised FCIs, economic and PCA, summarize macro conditions themselves. The supervised FCIs, PLS and probability, summarize macro conditions through their historical relationship with future market stress. That changes the meaning of the number.

If a supervised FCI is high, it doesn’t necessarily mean every macro block is high. It means the current combination of blocks resembles historical combinations that were followed by high future stress. A moderate inflation block, weak survey data, and a certain policy configuration may be more predictive than a single extreme block.

Mathematically, the supervised index is closer to a fitted conditional expectation:

\[

F_t^{sup}\approx E[Y_t\mid B_t]

\]

where \(Y_t\) is the future stress target. The unsupervised index is closer to a common macro-state score:

\[

F_t^{unsup}=g(B_t)

\]

This distinction explains why the latest PLS and blend readings can be tighter than the economic and PCA readings. The broad macro state is not strongly stressed, but the supervised relationship sees a higher-risk combination.

Partial Least Squares, or PLS, is a supervised dimension-reduction method. PCA finds the direction in macro blocks with the most variance. PLS finds a direction in macro blocks with the strongest relationship to the target.

Let \(X\) be the standardized block matrix and \(y\) be the future stress target. A one-component PLS model finds a weight vector \(w\) such that the latent factor:

\[

t=Xw

\]

has high covariance with \(y\). A simplified objective is:

after the PLS transformation and regression steps.

The financial interpretation is direct: PLS tries to learn which combination of macro blocks historically came before worse future SPY stress. It may put more weight on blocks that matter for asset markets, even if those blocks are not the largest source of macro variation.

The risk is sample dependence. A supervised model can overfit a few crisis patterns, especially when the number of macro cycles is small. That is why we later score the models across full-sample, common-sample, and test windows.

Show code

def pls_index(blocks, target, min_obs=60, min_cols=6, embargo_months=3): out = pd.Series(np.nan, index=blocks.index, name="fci_pls") target = pd.Series(target, dtype=float)for date in blocks.index: cutoff = pd.Timestamp(date) - pd.offsets.MonthEnd(embargo_months) hist_x = blocks.loc[blocks.index < cutoff] hist_y = target.reindex(hist_x.index) good_cols = [col for col in blocks.columns if hist_x[col].notna().sum() >= min_obs] row = blocks.loc[date, good_cols] good_cols = [col for col in good_cols if np.isfinite(row.get(col, np.nan))]iflen(good_cols) < min_cols:continue train = pd.concat([hist_x[good_cols], hist_y.rename("target")], axis=1).dropna()iflen(train) < min_obs:continue scaler = StandardScaler() train_x = scaler.fit_transform(train[good_cols]) components =min(2, len(good_cols), len(train) -1) model = PLSRegression(n_components=components) model.fit(train_x, train["target"].to_numpy(dtype=float)) current = scaler.transform(blocks.loc[[date], good_cols]) prediction = np.asarray(model.predict(current), dtype=float).reshape(-1) out.loc[date] =float(prediction[0])return zscore(out, 36).rename("fci_pls")fci_pls_full = pls_index(macro_full[block_cols], target_table["future_stress"], 36, 6, 3)fci_pls = fci_pls_full.reindex(macro.index)

21) Stress-Probability FCI

The stress-probability model turns the future stress target into a binary event. The event is defined as future stress being above a rolling high-stress threshold, usually the 75th percentile of historical target values.

The output is a probability between 0 and 1. A high value means the macro block state looks similar to historical states that were followed by high market stress.

We then standardize the probability through time so it can be compared with the other FCIs:

\[

F_t^{prob}=z(P(Y_t^{bin}=1\mid B_t))

\]

This model is appealing because it matches how risk managers often think: the question is not only expected return, but whether we are entering a high-stress zone. The weakness is that binary labels discard information. A mildly bad future and an extremely bad future can both become the same class if they are above the threshold.

Show code

def prob_index(features, target, min_obs=60, embargo_months=3): x = features.apply(pd.to_numeric, errors="coerce").replace([np.inf, -np.inf], np.nan) y = pd.Series(target, dtype=float).reindex(x.index) threshold = y.expanding(min_periods=min_obs).quantile(0.75).shift(1) label = (y > threshold).where(threshold.notna()) out = pd.Series(np.nan, index=x.index, name="fci_prob")for date in x.index: current = x.loc[date].dropna() cutoff = pd.Timestamp(date) - pd.offsets.MonthEnd(embargo_months) history = x.loc[x.index < cutoff] cols = [col for col in current.index if history[col].notna().sum() >= min_obs]iflen(cols) <4:continue train = pd.concat([history[cols], label.loc[history.index].rename("label")], axis=1).dropna()iflen(train) < min_obs or train["label"].nunique() <2:continue scaler = StandardScaler() train_x = scaler.fit_transform(train[cols]) model = LogisticRegression(C=1.0, max_iter=1000, solver="lbfgs") model.fit(train_x, train["label"].astype(int)) current_x = scaler.transform(x.loc[[date], cols]) out.loc[date] =float(model.predict_proba(current_x)[0, 1])return outprob_features = pd.concat([macro_full[block_cols], fci_econ_full, fci_pca_full, fci_pls_full], axis=1)fci_prob_full = prob_index(prob_features, target_table["future_stress"], 36, 3)fci_prob_z_full = zscore(fci_prob_full, 12).rename("fci_prob")fci_prob_z = fci_prob_z_full.reindex(macro.index)

The weights give the largest role to PLS because it is explicitly targeted to future stress. PCA receives a meaningful weight because it captures the common macro factor without needing a market target. The economic index receives a smaller but important weight because it is stable and interpretable.

This blend is a compromise between prediction and robustness. Supervised models can be more responsive to market stress, but they can also overfit. Unsupervised models can have better long-history behavior, but they may ignore the exact combination that matters for future equity stress. A blend gives the strategy more than one source of information.

The model availability table shows the expected pattern. Economic FCI starts earliest, PCA starts after enough block history is available, and the supervised models start later because they need both macro history and target history.

The FCI plot compares all five models. They agree strongly around major crisis periods, but they diverge in calmer or mixed regimes. That divergence is useful information rather than a problem to hide.

The latest model table gives a very clear split. In January 2026:

fci_econ is neutral, with value about -0.18 and percentile around 0.40.

fci_pca is also neutral, with value about -0.34 and percentile around 0.42.

fci_pls is tight, with percentile around 0.82.

fci_prob is neutral, around percentile 0.46.

fci_blend is tight, around percentile 0.83.

The unsupervised models say broad macro stress is not high. The supervised PLS and blend are more cautious, likely because the combination of sticky inflation and survey weakness resembles past market-risk setups more than the broad blocks alone suggest. That difference matters later when choosing which index should control an allocation strategy.

Model Agreement and Disagreement

The latest FCI readings show a useful kind of model disagreement. Economic and PCA indexes are neutral, while PLS and blend are tight. This means the broad macro blocks are not screaming crisis, but the supervised relation to future stress is more cautious.

A portfolio manager can use that disagreement in several ways:

If all indexes are high, reduce risk with more confidence.

If only supervised indexes are high, watch for market fragility but avoid an extreme risk-off move.

If only unsupervised indexes are high, the macro environment may be broadly stressed even if the specific equity-stress target has not learned that pattern strongly.

If all indexes are low, macro conditions are likely supportive or at least not restrictive.

This project later selects PCA for the main strategy because it has long history and avoids supervised model-selection lookahead. But the latest model table still provides useful diagnostic context. It tells us that the current macro regime has some supervised stress features despite neutral broad stress.

A good FCI should have a monotonic relationship with future market stress. We test this by sorting each FCI into quintiles and checking future SPY outcomes.

For each model, we rank the FCI values and place them into five groups:

\[

q_t \in \{Q1,Q2,Q3,Q4,Q5\}

\]

where \(Q1\) means easiest conditions and \(Q5\) means tightest conditions.

Then we compute the average future 1-month return, future 3-month return, future volatility, future max drawdown, and future stress target inside each quintile.

The clean pattern we want is:

higher FCI quintiles have lower future returns,

higher FCI quintiles have higher future volatility,

higher FCI quintiles have deeper future drawdowns,

the future stress target rises from low quintiles to high quintiles.

This is a practical validation test. It doesn’t require the model to predict every month correctly. It checks whether the distribution of future outcomes worsens when macro conditions are tighter.

Show code

def quintile_report(fci, target): data = pd.concat([fci.rename("fci"), target], axis=1).dropna(subset=["fci", "future_stress"])iflen(data) <30:return pd.DataFrame() ranks = data["fci"].rank(method="first") data["fci_quintile"] = pd.qcut(ranks, 5, labels=["q1", "q2", "q3", "q4", "q5"]) report = data.groupby("fci_quintile", observed=False)[["future_1m_return", "future_3m_return", "future_3m_volatility", "future_3m_max_drawdown", "future_stress"]].mean() report["observations"] = data.groupby("fci_quintile", observed=False).size()return reportquintile_reports = {name: quintile_report(fci_models[name], target_table) for name in fci_models.columns}for name, report in quintile_reports.items():print(name) display(report.round(4))

fci_econ

future_1m_return

future_3m_return

future_3m_volatility

future_3m_max_drawdown

future_stress

observations

fci_quintile

q1

0.0119

0.0256

0.1046

-0.0216

-0.5124

58

q2

0.0141

0.0426

0.1177

-0.0167

-0.7198

58

q3

0.0114

0.0360

0.1367

-0.0260

-0.3345

57

q4

0.0064

0.0210

0.1166

-0.0233

-0.7064

58

q5

-0.0003

0.0066

0.1401

-0.0381

0.0958

58

fci_pca

future_1m_return

future_3m_return

future_3m_volatility

future_3m_max_drawdown

future_stress

observations

fci_quintile

q1

0.0128

0.0232

0.0984

-0.0229

-0.5191

58

q2

0.0083

0.0359

0.1181

-0.0170

-0.6656

58

q3

0.0136

0.0331

0.1137

-0.0229

-0.6676

57

q4

0.0067

0.0303

0.1281

-0.0218

-0.5638

58

q5

0.0021

0.0092

0.1570

-0.0411

0.2331

58

fci_pls

future_1m_return

future_3m_return

future_3m_volatility

future_3m_max_drawdown

future_stress

observations

fci_quintile

q1

0.0090

0.0294

0.1263

-0.0228

-0.4229

43

q2

0.0131

0.0360

0.1162

-0.0185

-0.6199

43

q3

0.0070

0.0181

0.1292

-0.0324

0.0937

43

q4

0.0175

0.0461

0.1456

-0.0220

-0.2839

43

q5

0.0047

0.0224

0.1442

-0.0350

0.2608

43

fci_prob

future_1m_return

future_3m_return

future_3m_volatility

future_3m_max_drawdown

future_stress

observations

fci_quintile

q1

0.0136

0.0309

0.1161

-0.0209

-0.6073

41

q2

0.0084

0.0346

0.1237

-0.0189

-0.5463

40

q3

0.0110

0.0342

0.1152

-0.0211

-0.5351

41

q4

0.0179

0.0503

0.1231

-0.0192

-0.7261

40

q5

0.0143

0.0387

0.1534

-0.0291

0.0949

41

fci_blend

future_1m_return

future_3m_return

future_3m_volatility

future_3m_max_drawdown

future_stress

observations

fci_quintile

q1

0.0152

0.0447

0.1278

-0.0199

-0.7383

41

q2

0.0115

0.0262

0.1104

-0.0215

-0.5882

41

q3

0.0091

0.0325

0.1007

-0.0186

-0.7017

40

q4

0.0120

0.0269

0.1329

-0.0261

-0.0404

41

q5

0.0189

0.0635

0.1578

-0.0225

-0.3508

41

The quintile reports show that the relationship is present, but not perfectly monotonic for every model. That is normal for macro data. Macro conditions shape probabilities, not exact next-month outcomes.

For the economic FCI, the tightest quintile has weaker future returns and worse future drawdowns than easier quintiles. In the fci_econ report, the tightest quintile has a future 3-month return around 0.66%, compared with 2.56% in the easiest quintile and 4.26% in the second quintile. Its future max drawdown is also worse, around -3.81%.

For the PCA FCI, the tightest quintile has higher future volatility, around 15.7%, and the worst future max drawdown, around -4.11%. That supports the idea that the unsupervised common macro factor contains risk information.

The supervised models have mixed shapes. PLS and probability capture some high-stress behavior, but the sample is shorter and the relationship can become uneven across quintiles. The blend is especially interesting: the tightest quintile has high future volatility, but it also has strong future returns in this sample. That means a high blend signal may sometimes identify volatile upside environments, not only crash risk.

How to Read a Non-Monotonic Quintile Table

Macro validation rarely gives perfectly ordered quintiles. There are several reasons.

First, macro variables are slow. A high FCI can persist after the market has already sold off, so forward returns may rebound even though the FCI remains high. Second, policy reaction can offset stress. A tight or stressful macro state may trigger rate cuts, fiscal support, or liquidity provision. Third, financial markets price expectations before macro data confirms them. By the time a macro signal is extreme, some of the bad news may already be in prices.

So we shouldn’t demand that every column rises perfectly from Q1 to Q5. We look for distributional evidence: worse drawdowns, higher volatility, lower average future returns, and positive rank association with future stress. The model scoreboard does this by combining several diagnostics instead of relying on one table cell.

This is why fci_pca can win the full sample even with modest rank IC. It may not perfectly order every quintile, but it identifies the distributional deterioration around stress regimes and has long crisis coverage.

24) Model Scoreboard

The model scoring function turns the quintile validation into a compact ranking. For each FCI model, we compute several diagnostics.

The rank information coefficient measures whether higher FCI values are associated with higher future stress:

The drawdown spread compares future max drawdown in easy and tight regimes:

\[

\Delta DD=DD_{Q1}-DD_{Q5}

\]

Since drawdowns are negative, a positive spread means the tightest FCI quintile has a worse drawdown than the easiest quintile.

The volatility spread is:

\[

\Delta\sigma=\sigma_{Q5}-\sigma_{Q1}

\]

A positive value means future volatility is higher when conditions are tighter.

The monotonicity score checks whether future stress rises across quintiles in a roughly ordered way. The stability score penalizes overly noisy indexes:

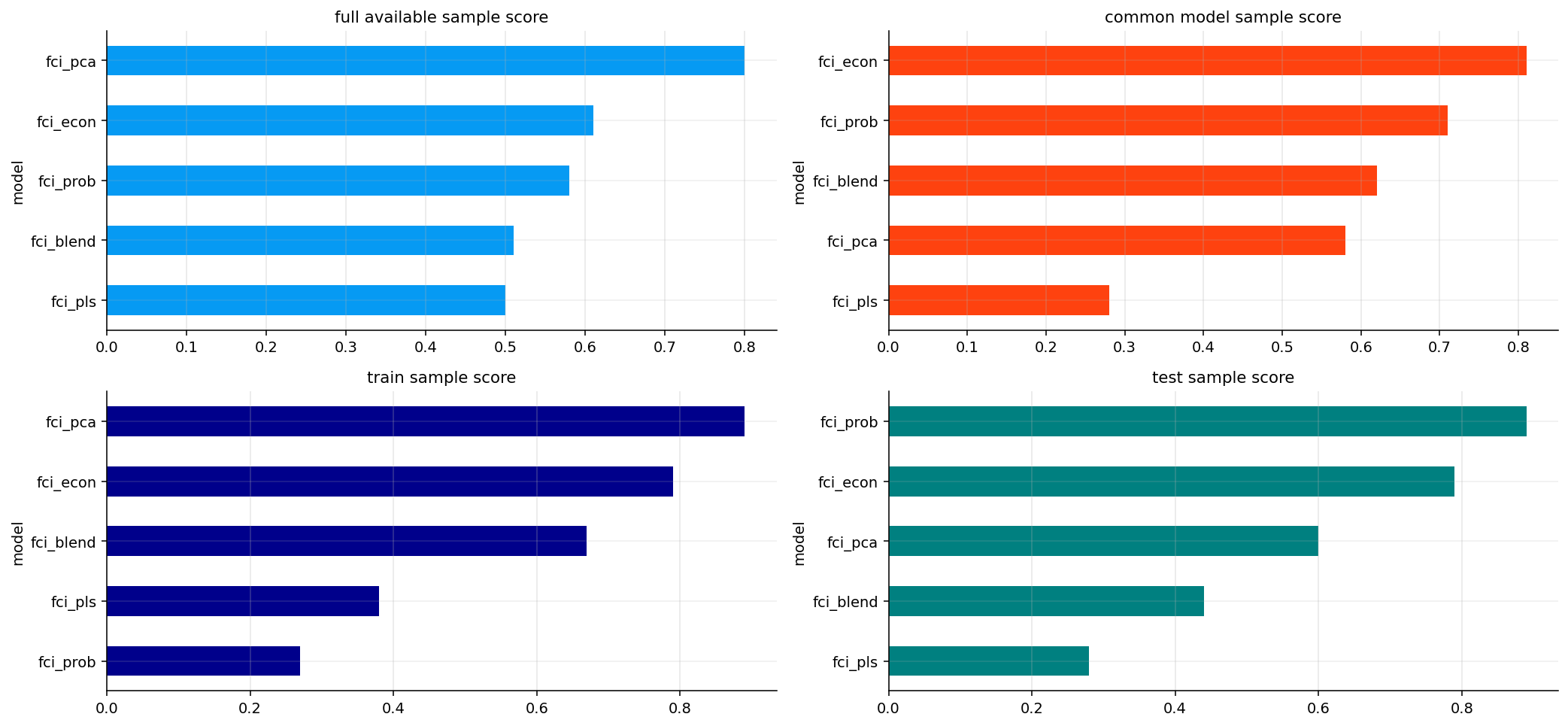

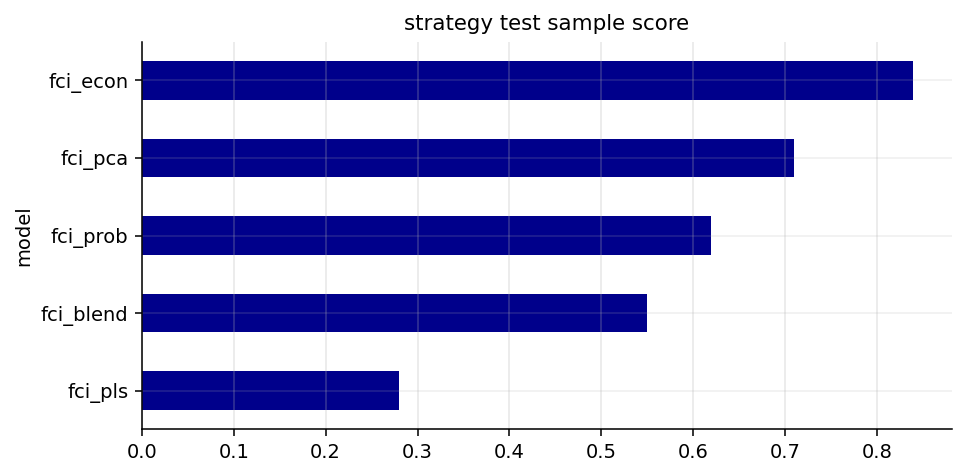

The full-sample scoreboard selects fci_pca as the top model, with a final score around 0.80. It has the strongest drawdown spread and volatility spread in the full available sample, and it is long-history eligible because it starts in 1998.

The common-sample scoreboard changes the ranking. When all models are compared over the same later sample, fci_econ rises to the top with a final score around 0.81. This says the economic-weighted index holds up well when sample length is equalized.

The test-sample scoreboard, from February 2020 to January 2026, ranks fci_prob first with a final score around 0.89, followed by fci_econ around 0.79. The supervised probability model works well in the recent high-volatility period, but it has a shorter history.

For strategy design, the project selects fci_pca as the long-history strategy FCI. This is a conservative choice. It avoids choosing a supervised model mainly because it did well in the recent period, and it preserves coverage of the dot-com and 2008 regimes.

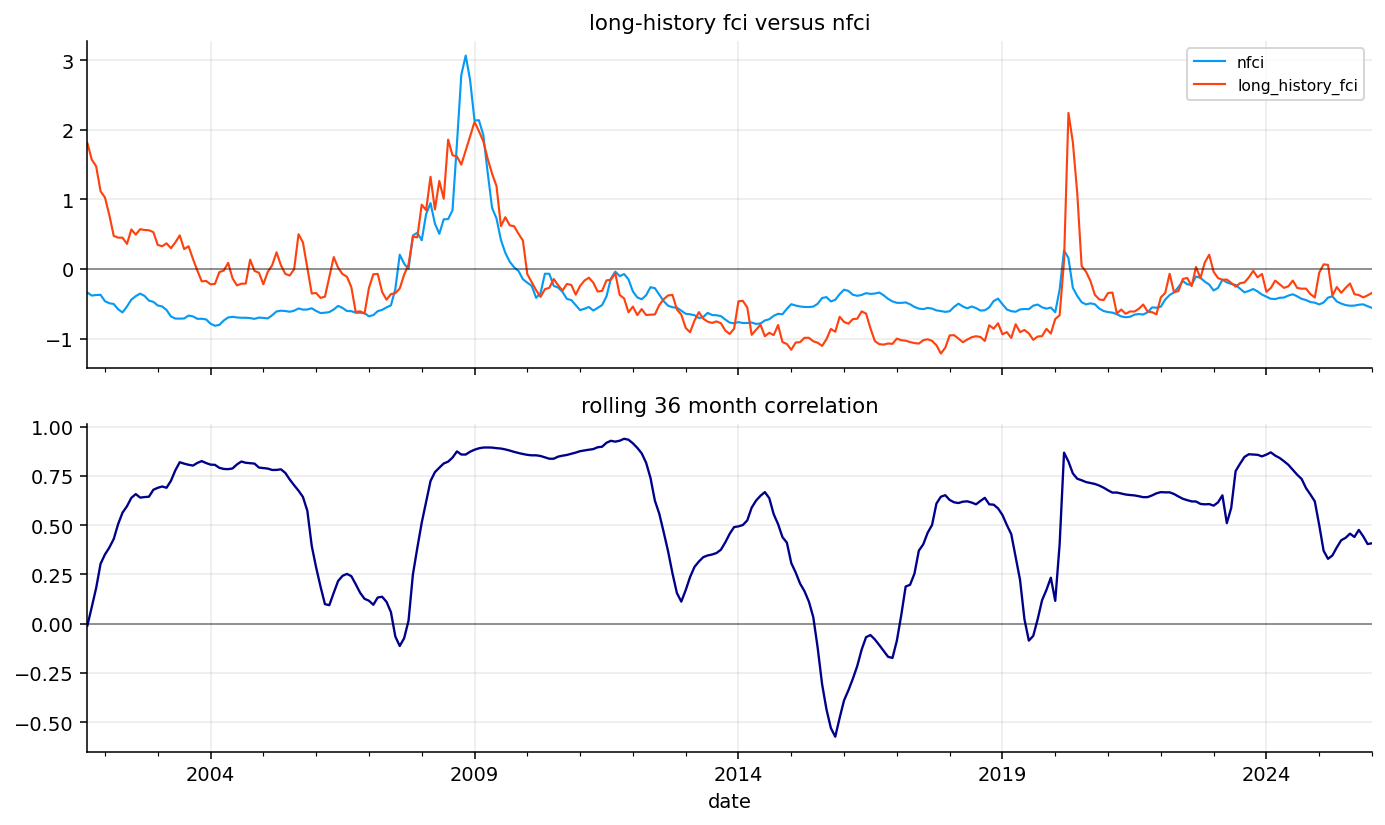

We compare the selected long-history FCI with the external NFCI benchmark. This is not a perfect apples-to-apples test because NFCI is built from financial variables, while our FCI is built mainly from macro blocks. Still, crisis agreement is useful.

The correlation between the selected FCI and NFCI is about 0.525. That is a meaningful positive relationship, especially because the inputs are different. It says the macro-built FCI captures a substantial part of broad financial stress.

The crisis agreement table is more important than the correlation alone:

During the financial crisis, selected FCI mean is about 1.81, NFCI mean is about 2.36, and sign agreement is 1.0.

During the COVID crash, selected FCI mean is about 0.57, NFCI mean is about 0.04, and sign agreement is 1.0.

During the inflation/rate shock, selected FCI mean is about -0.21, NFCI mean is about -0.28, and sign agreement is 0.9.

The model captures classic credit/liquidity stress well. The inflation/rate shock is different because macro pressure can be high while broad financial stress indexes are not necessarily crisis-high.

Show code

sector_assets = us_sector_assets[:]defensive_sector_assets = [x for x in ["xlp", "xlu", "xlv"] if x in returns.columns]cyclical_sector_assets = [x for x in ["xlf", "xli", "xly", "xlb"] if x in returns.columns]inflation_assets = [x for x in ["xle", "xlb", "dbc", "gld"] if x in returns.columns]rate_sensitive_assets = [x for x in ["xlk", "xly", "tlt"] if x in returns.columns]strategy_assets =sorted(set(sector_assets + defensive_assets + ["spy"]))required_strategy_assets = sector_assets + ["spy", "cash"]asset_first_month = monthly_close[sector_assets + ["spy"]].apply(pd.Series.first_valid_index)strategy_start =max(macro_start, asset_first_month.max() + pd.offsets.MonthEnd(6))score_strategy_dates = fci_models.index.intersection(returns.index)score_strategy_dates = score_strategy_dates[score_strategy_dates >= strategy_start]strategy_split_date = score_strategy_dates[int(len(score_strategy_dates) *0.65)] iflen(score_strategy_dates) else pd.NaTstrategy_test_dates = score_strategy_dates[score_strategy_dates >= strategy_split_date]strategy_sample_scoreboard = score_fci_models(fci_models.reindex(strategy_test_dates), target_table.reindex(strategy_test_dates))strategy_sample_scoreboard["strategy_test_sample"] =Trueprespecified_strategy_fci_name = long_history_fci_namestrategy_fci_name = prespecified_strategy_fci_name if prespecified_strategy_fci_name in fci_models.columns else"fci_econ"best_fci_name = strategy_fci_namebest_fci_series = fci_models[best_fci_name].rename("best_fci")best_fci_percentile = rolling_percentile(best_fci_series, 60).rename("best_fci_percentile")best_fci_3m_change = best_fci_series.diff(3).rename("best_fci_3m_change")tradable_macro = macro.shift(1)allocation_features = tradable_macro[["inflation_pressure_block", "policy_rate_pressure_block", "growth_recession_block", "macro_breadth_conflict_block", "goldilocks_support"]].copy()allocation_features["best_fci_percentile"] = best_fci_percentile.shift(1)allocation_features["best_fci_3m_change"] = best_fci_3m_change.shift(1)allocation_features["best_fci_value"] = best_fci_series.shift(1)dominant_block_values = tradable_macro[block_cols].abs()dominant_macro_block = pd.Series(np.nan, index=dominant_block_values.index, dtype=object)has_dominant_block = dominant_block_values.notna().any(axis=1)dominant_macro_block.loc[has_dominant_block] = dominant_block_values.loc[has_dominant_block].idxmax(axis=1)allocation_features["dominant_macro_block"] = dominant_macro_blockallocation_features = allocation_features.dropna(subset=["best_fci_percentile", "best_fci_3m_change"])model_choice_table = pd.DataFrame({"full_sample_score_winner": [full_sample_scoreboard.index[0]],"common_sample_score_winner": [common_model_scoreboard.index[0]],"test_sample_score_winner": [test_model_scoreboard.index[0]],"selected_strategy_fci": [strategy_fci_name],"selection_rule": ["Pre-specified long-history unsupervised FCI selected to avoid supervised model-selection lookahead and preserve crisis coverage."],})display(strategy_sample_scoreboard.round(4))display(model_choice_table)display(pd.DataFrame({"long_history_fci": [long_history_fci_name], "prespecified_strategy_fci": [strategy_fci_name], "strategy_start": [strategy_start], "strategy_test_start": [strategy_split_date]}))fig, ax = plt.subplots(figsize=(7, 3.5))strategy_sample_scoreboard["final_score"].sort_values().plot(kind="barh", ax=ax, color=colors[2])ax.set_title("strategy test sample score")ax.grid(True, axis="x", alpha=0.3)plt.tight_layout()plt.show()

observations

first_valid_date

last_valid_date

future_stress_rank_ic

drawdown_spread

monotonicity_score

volatility_spread

stability_score

future_stress_rank_ic_rank

drawdown_spread_rank

monotonicity_score_rank

volatility_spread_rank

stability_score_rank

final_score

strategy_test_sample

model

fci_econ

112

2016-10-31

2026-01-31

0.1919

0.0114

0.7

0.1000

0.7765

1.0

0.6

1.0

1.0

0.4

0.84

True

fci_pca

112

2016-10-31

2026-01-31

0.0918

0.0151

0.3

0.0957

0.7832