import warnings

from pathlib import Path

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from cycler import cycler

from IPython.display import display

from quantfinlab.dataio.equity_ohlcv import load_ohlcv

from quantfinlab.dataio.option_chain import load_option_chain

from quantfinlab.dataio.rates import load_par_yield_curve

from quantfinlab.options.quote_cleaning import (

attach_spot_from_series,

convert_quotes_to_usd_equivalent,

clean_option_quotes,

surface_ready_quotes,

)

from quantfinlab.options.rates_dividends import (

attach_rates,

add_discount_factors,

infer_carry_from_forward,

infer_dividend_yield_from_forward,

)

from quantfinlab.options.parity import infer_forwards_from_parity

from quantfinlab.options.iv import implied_vol_table

from quantfinlab.options.greeks import compute_greeks_numpy

from quantfinlab.options.model_risk import (

choose_model_engine,

add_calibration_weights,

calibration_quotes,

choose_surface_date,

balanced_model_quotes,

common_model_quotes,

compare_model_fits,

model_fair_values,

residual_scores,

signal_dates,

next_day_residual_check,

residual_entry_schedule,

market_summary,

)

from quantfinlab.options.svi import fit_svi_surface, fit_svi_holdout

from quantfinlab.options.ssvi import fit_ssvi_surface

from quantfinlab.options.sabr import fit_sabr_surface, fit_sabr_holdout

from quantfinlab.options.merton import fit_merton_jump_diffusion

from quantfinlab.options.heston import fit_heston_mc

from quantfinlab.options.bates import fit_bates_mc

from quantfinlab.backtest.options import (

matched_option_schedule,

hedge_book_from_schedules,

run_scheduled_option_hedging_backtest,

hedging_diagnostics,

scheduled_hedge_comparison,

)

from quantfinlab.plotting.options import (

calibration_quote_map,

smile_term_structure,

model_quote_overlay,

svi_smiles,

svi_ssvi_errors,

ssvi_residuals,

sabr_smiles,

sabr_terms,

merton_tail_fit,

heston_mc_check,

heston_bates_fit,

model_speed_accuracy,

benchmark_errors,

model_disagreement,

residual_deciles,

scheduled_hedge_equity,

)

warnings.filterwarnings("ignore")

pd.set_option("display.float_format", lambda x: f"{x:,.6f}")

pd.set_option("display.max_columns", 120)

colors = ["#069AF3", "#FE420F", "#00008B", "#008080", "#CC79A7", "#DC143C", "#9614fa", "#0072B2", "#7BC8F6", "#04D8B2", "#800080", "#FF8072"]

plt.rcParams["axes.prop_cycle"] = cycler(color=colors)

plt.rcParams.update({"figure.figsize": (7, 3.5), "figure.dpi": 300, "savefig.dpi": 250, "axes.grid": True, "grid.alpha": 0.20, "axes.spines.top": False, "axes.spines.right": False, "axes.titlesize": 11, "axes.labelsize": 10, "xtick.labelsize": 9, "ytick.labelsize": 9, "legend.fontsize": 8})

engine = "auto"

ann_days = 365.25

random_state = 7

root = Path.cwd()

if root.name.lower() == "notebooks":

root = root.parent

data_dir = root / "data"

backend_report = choose_model_engine(engine=engine)

display(backend_report)

btc_spot = load_ohlcv(

data_dir / "btc_usd_ohlcv.csv",

source="yfinance_csv",

fields=("close",),

)

btc_spot = btc_spot["close"].rename("BTC")

btc_spot = btc_spot[btc_spot > 0]

btc_options = load_option_chain(

data_dir / "btc_options_chain.parquet",

source="btc_deribit",

annualization_days=365.0,

)

us_rates = load_par_yield_curve(

data_dir / "us_treasury_yields.csv",

source="us_treasury",

)

btc_quotes = attach_spot_from_series(

btc_options,

btc_spot,

date_col="date",

spot_col="spot",

method="previous",

overwrite=False,

)

btc_quotes = convert_quotes_to_usd_equivalent(

btc_quotes,

spot_col="spot",

price_cols=("bid", "ask", "mid", "last", "mark"),

unit="auto",

contract_size=1.0,

)

clean_quotes, clean_report = clean_option_quotes(

btc_quotes,

min_dte=3,

max_dte=180,

moneyness_range=(0.45, 1.75),

max_relative_spread=0.60,

closest_atm_pairs=None,

min_pairs_per_expiry=0,

annualization_days=365.0,

)

rate_start = clean_quotes["date"].min() - pd.Timedelta(days=30)

rate_end = clean_quotes["date"].max()

us_rates = us_rates.loc[(us_rates.index >= rate_start) & (us_rates.index <= rate_end)].copy()

clean_quotes = attach_rates(

clean_quotes,

us_rates,

date_col="date",

tau_col="tau",

out_col="rate",

)

clean_quotes = add_discount_factors(

clean_quotes,

rate_col="rate",

tau_col="tau",

out_col="discount_factor",

)

clean_quotes = infer_forwards_from_parity(

clean_quotes,

date_col="date",

expiry_col="expiry",

strike_col="strike",

option_type_col="option_type",

mid_col="mid",

discount_col="discount_factor",

spot_col="spot",

out_col="forward",

)

forward_bad = ~np.isfinite(pd.to_numeric(clean_quotes["forward"], errors="coerce")) | (pd.to_numeric(clean_quotes["forward"], errors="coerce") <= 0)

forward_fallback = clean_quotes["spot"] * np.exp(clean_quotes["rate"].fillna(0.0) * clean_quotes["tau"].fillna(0.0))

clean_quotes.loc[forward_bad, "forward"] = forward_fallback.loc[forward_bad]

forward_report = pd.DataFrame([{"forward_fallback_share": float(forward_bad.mean()), "forward_fallback_rows": int(forward_bad.sum())}])

clean_quotes = infer_carry_from_forward(

clean_quotes,

spot_col="spot",

forward_col="forward",

tau_col="tau",

out_col="implied_carry",

)

clean_quotes = infer_dividend_yield_from_forward(

clean_quotes,

rate_col="rate",

carry_col="implied_carry",

out_col="implied_dividend_yield",

)

iv_quotes = implied_vol_table(

clean_quotes,

price_cols=("bid", "mid", "ask"),

option_type_col="option_type",

spot_col="spot",

forward_col="forward",

strike_col="strike",

tau_col="tau",

rate_col="rate",

discount_col="discount_factor",

model="black76",

engine=engine,

)

iv_quotes["iv_ok"] = iv_quotes["iv_mid_success"].fillna(False) & np.isfinite(iv_quotes["iv_mid"])

iv_quotes = compute_greeks_numpy(iv_quotes, iv_col="iv_mid")

surface_quotes = surface_ready_quotes(

iv_quotes,

min_iv=0.05,

max_iv=3.50,

min_tau=3 / 365.0,

max_tau=180 / 365.0,

min_weight=0.05,

max_weight=20.0,

)

surface_quotes = add_calibration_weights(

surface_quotes,

price_uncertainty="half_spread",

iv_uncertainty="spread_over_vega",

expiry_balance=True,

)

btc_calibration = calibration_quotes(

surface_quotes,

min_dte=3.0,

max_dte=120.0,

min_vega=0.0,

max_relative_spread=0.85,

otm_only=True,

)

main_date = choose_surface_date(

btc_calibration,

min_expiries=4,

min_quotes=80,

prefer_tail_coverage=True,

)

btc_day = btc_calibration.loc[btc_calibration["date"].eq(main_date)].copy()

btc_model_quotes = balanced_model_quotes(

btc_day,

target_dtes=(7, 14, 21, 30, 45, 60),

target_ks=(-0.35, -0.25, -0.17, -0.10, -0.04, 0.00, 0.04, 0.10, 0.17, 0.25),

min_quotes_per_expiry=6,

prefer_tail_coverage=True,

)

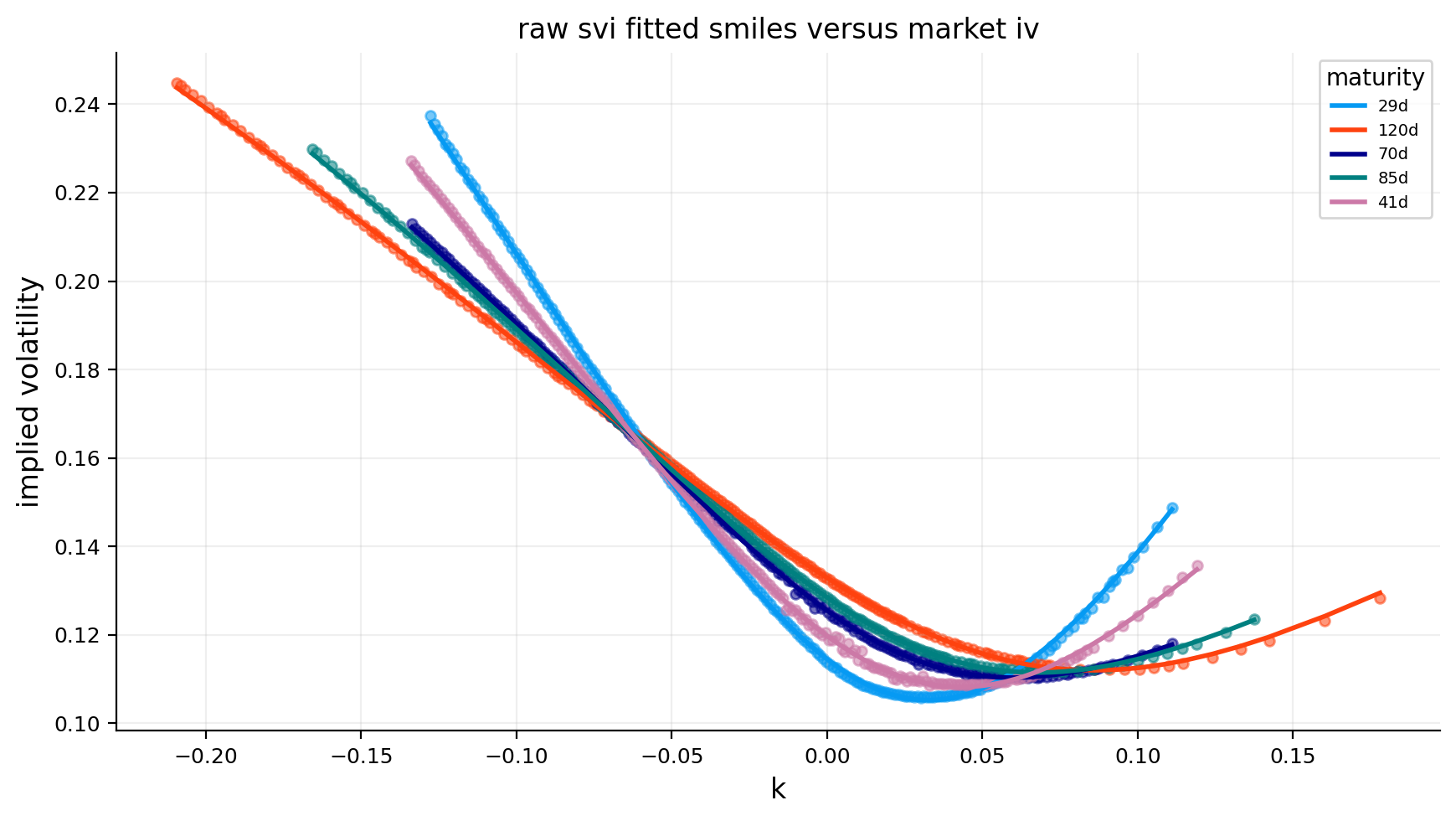

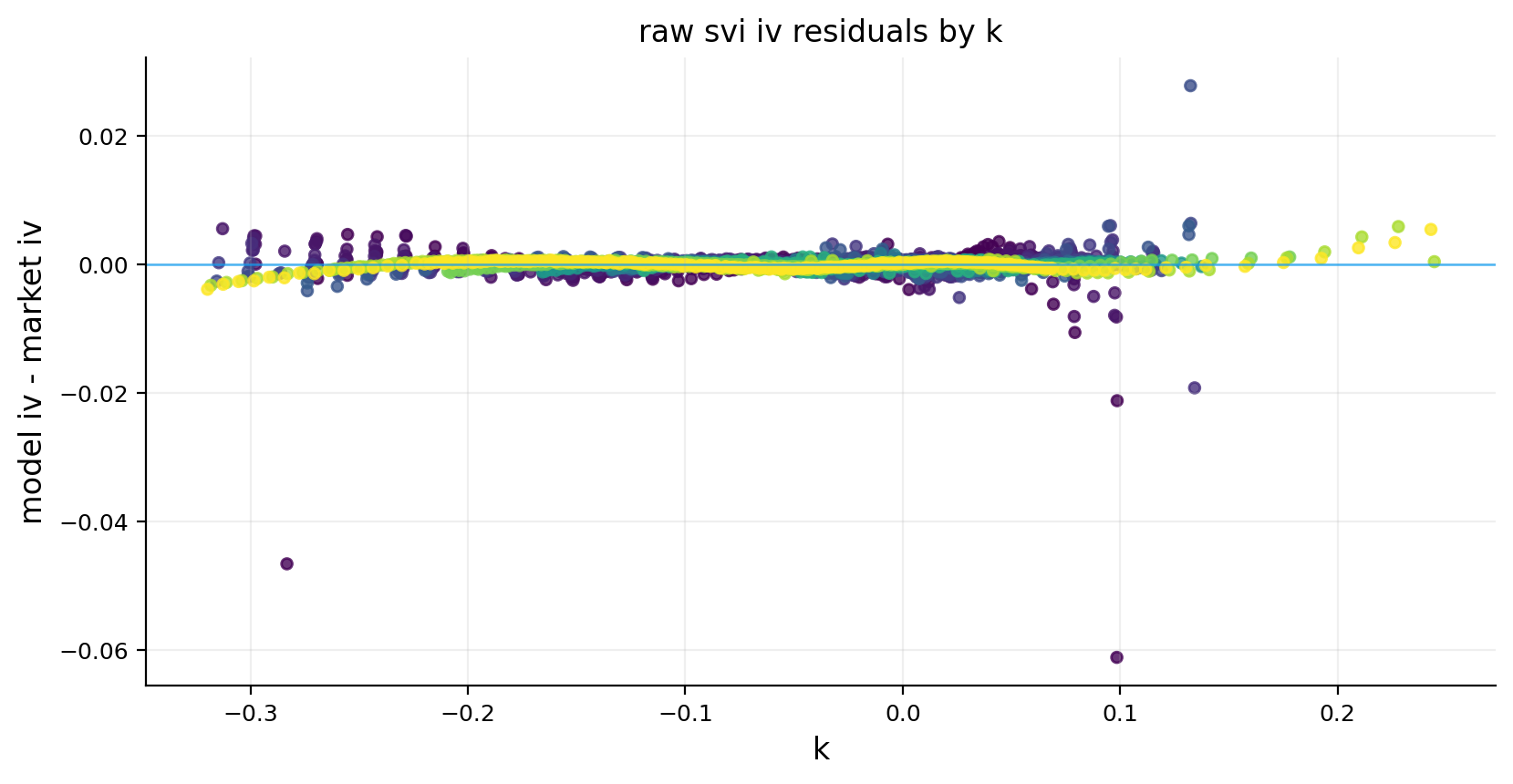

btc_svi = fit_svi_surface(

btc_day,

weight_col="obs_weight",

engine=engine,

)

btc_ssvi = fit_ssvi_surface(

btc_day,

weight_col="obs_weight",

engine=engine,

)

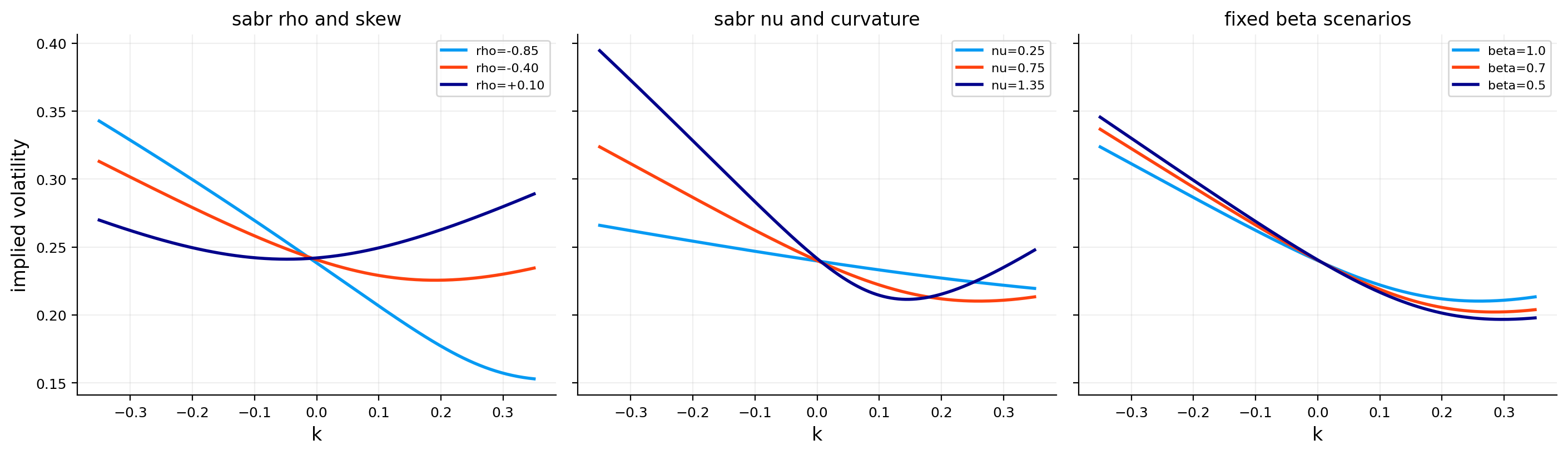

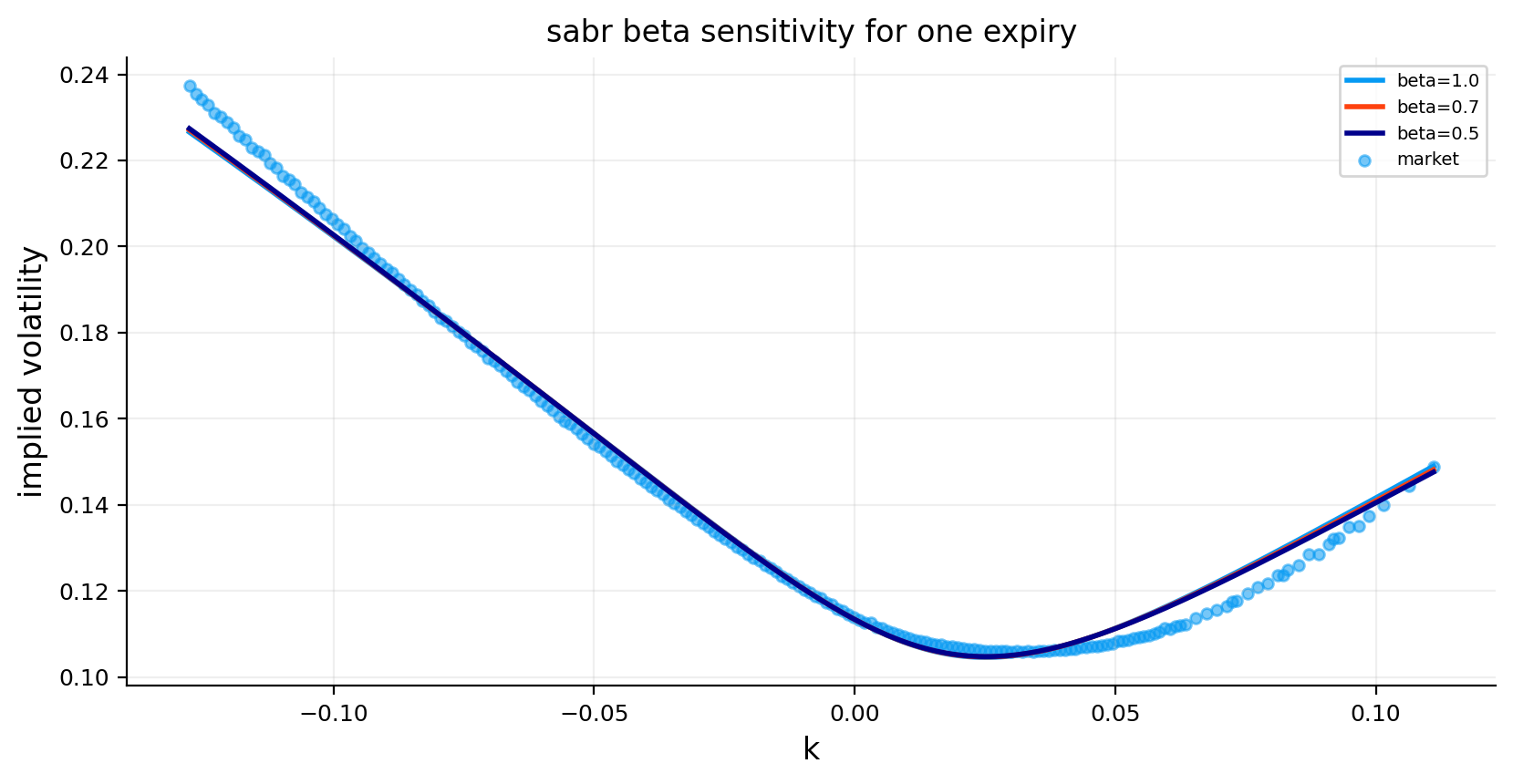

btc_sabr = fit_sabr_surface(

btc_day,

betas=(1.0, 0.7, 0.5),

primary_beta=1.0,

weight_col="obs_weight",

engine=engine,

)

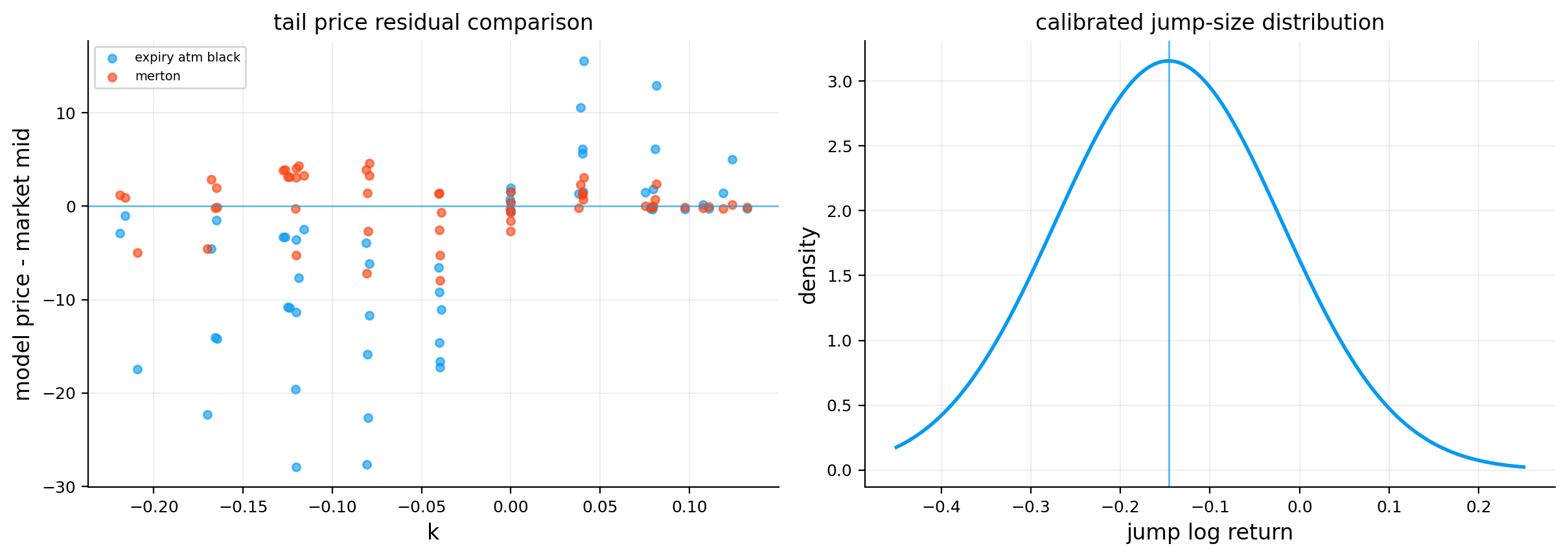

btc_merton = fit_merton_jump_diffusion(

btc_model_quotes,

weight_col="obs_weight",

engine=engine,

max_nfev=45,

fit_by_expiry=True,

)

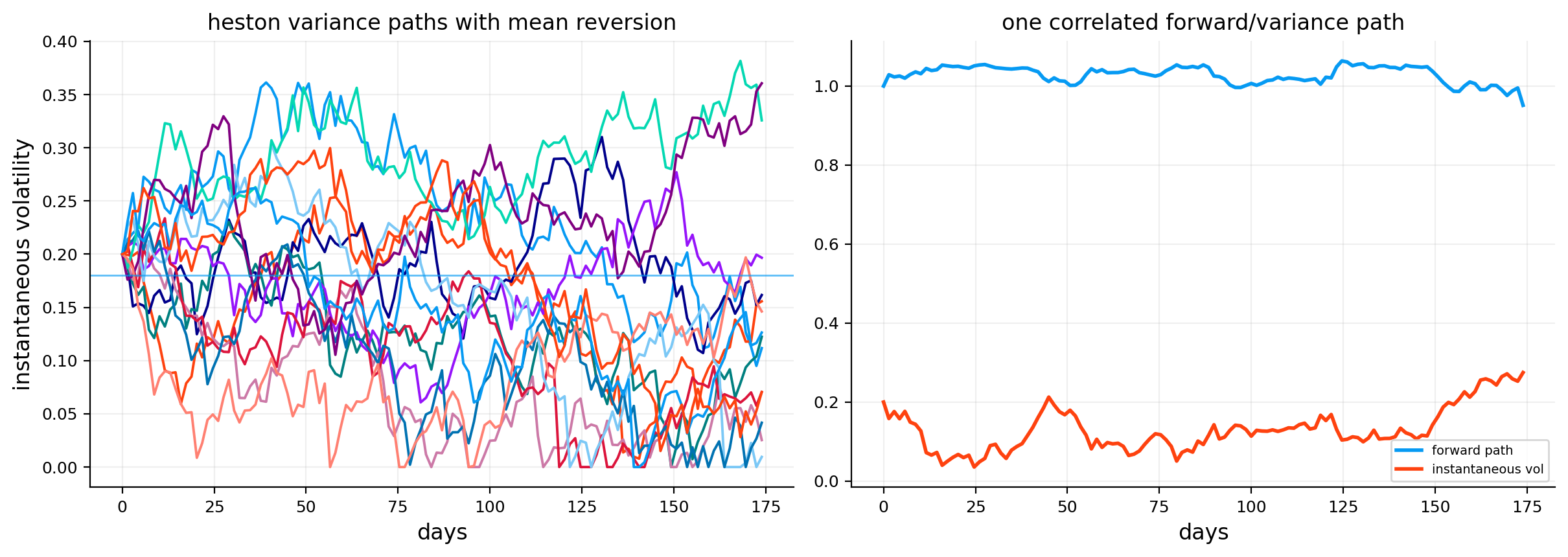

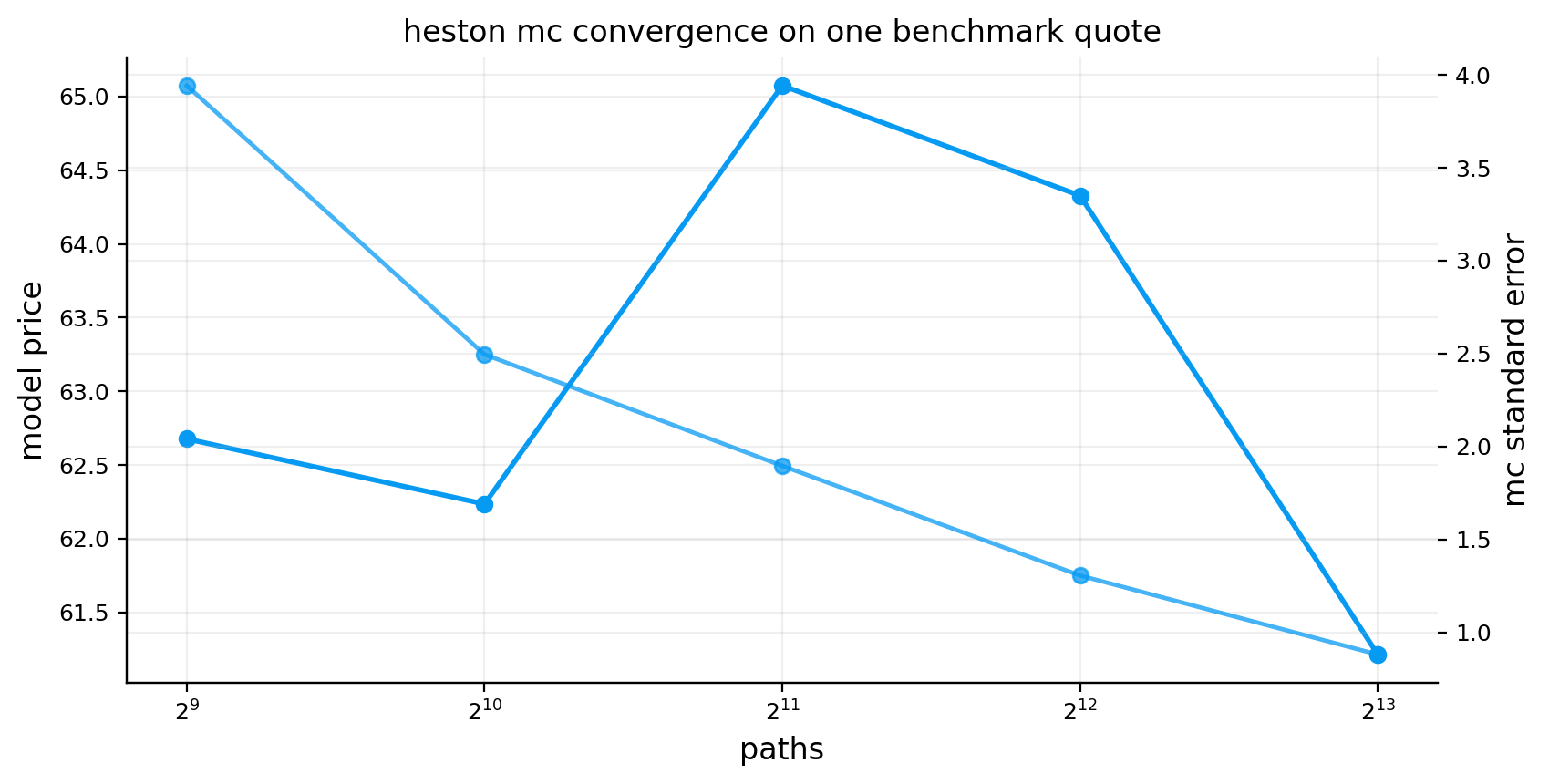

btc_heston = fit_heston_mc(

btc_model_quotes,

paths_opt=2048,

paths_final=8192,

steps_per_year=52,

random_method="antithetic",

common_random_numbers=True,

engine=engine,

random_state=random_state,

max_nfev=70,

)

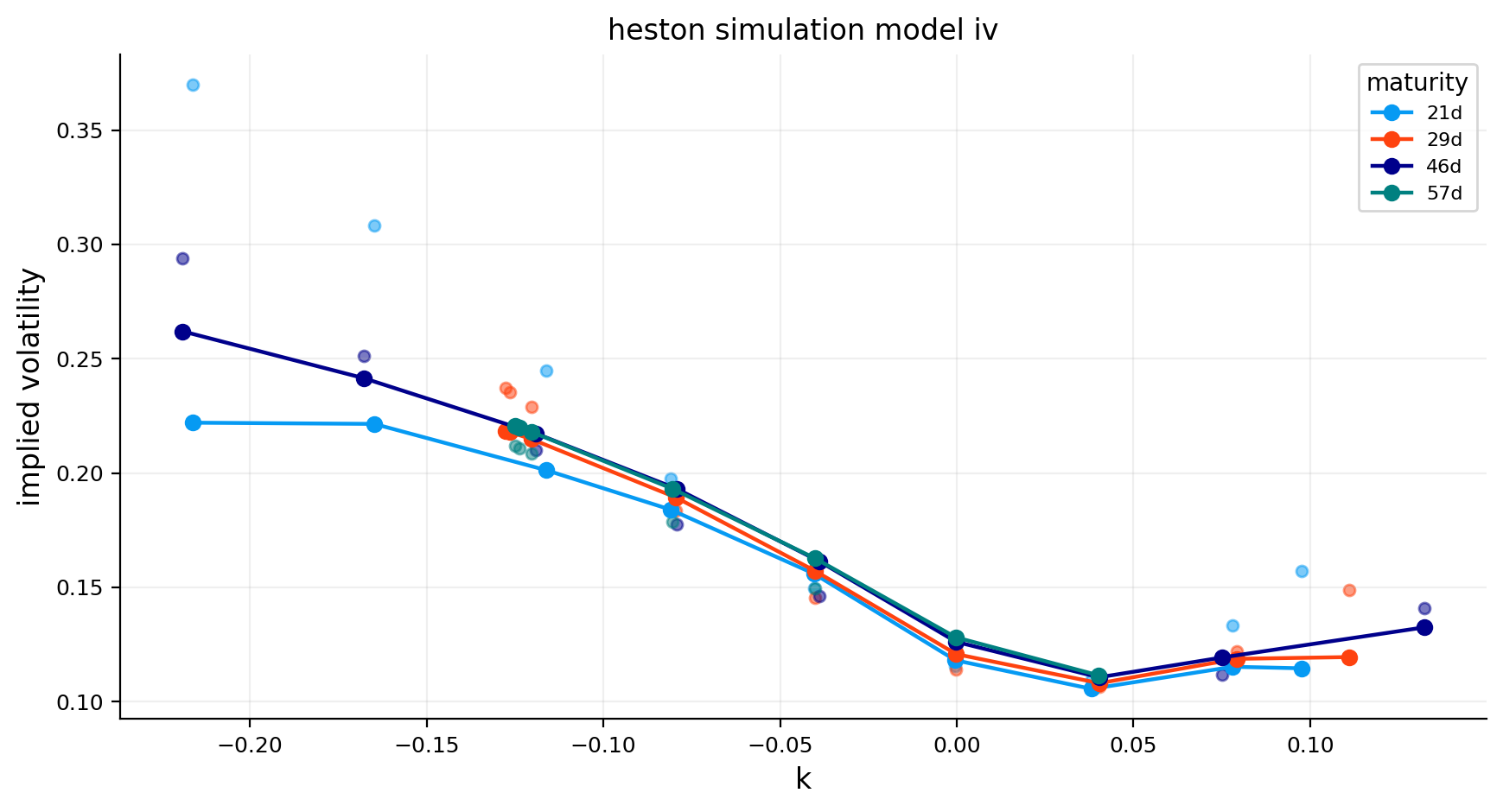

btc_bates = fit_bates_mc(

btc_model_quotes,

heston_start=btc_heston,

jump_start=btc_merton,

paths_opt=2048,

paths_final=8192,

steps_per_year=52,

random_method="antithetic",

common_random_numbers=True,

engine=engine,

random_state=random_state,

max_nfev=60,

)

btc_common_quotes = common_model_quotes(

btc_day,

model_quotes=btc_model_quotes,

min_tail_count=6,

)

model_comparison = compare_model_fits(

btc_common_quotes,

fits={

"svi": btc_svi,

"ssvi": btc_ssvi,

"sabr": btc_sabr,

"merton": btc_merton,

"heston": btc_heston,

"bates": btc_bates,

},

engine=engine,

)

dates_for_signal = signal_dates(

btc_calibration,

min_quotes=60,

min_expiries=3,

min_near_atm_quotes=10,

)

dates_for_signal = dates_for_signal[-120:]

btc_svi_daily = fit_svi_holdout(

btc_calibration,

dates=dates_for_signal,

train_mode="anchor_strikes",

weight_col="obs_weight",

warm_start=True,

engine=engine,

)

btc_sabr_daily = fit_sabr_holdout(

btc_calibration,

dates=dates_for_signal,

beta=1.0,

train_mode="anchor_strikes",

weight_col="obs_weight",

warm_start=True,

engine=engine,

)

btc_fair_values = model_fair_values(

btc_calibration,

fits={"svi": btc_svi_daily, "sabr": btc_sabr_daily},

ensemble_method="capped_weighted",

max_model_weight=0.70,

min_model_weight=0.30,

engine=engine,

)

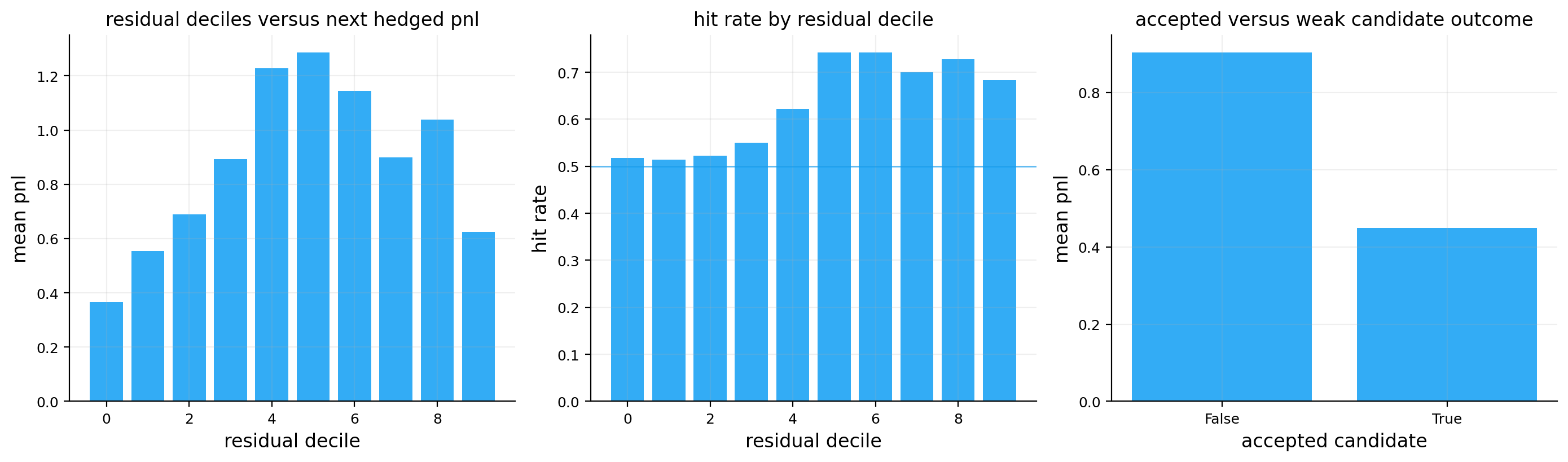

btc_scores = residual_scores(

btc_fair_values,

residual_col="ensemble_price_residual",

quote_cost_col="half_spread",

model_uncertainty_col="model_disagreement",

score_method="cost_adjusted_z",

)

btc_validation = next_day_residual_check(

btc_scores,

option_quotes=btc_calibration,

hedge_delta_col="delta",

cost_model="scheduled",

calendar="crypto_24_7",

engine=engine,

)

btc_residual_schedule = residual_entry_schedule(

btc_validation,

selector_name="btc_residual_fixed_3d",

hold_days=3,

max_entries=60,

entry_spacing_days=3,

require_signal_direction=True,

chronological=True,

)

btc_matched_schedule = matched_option_schedule(

btc_residual_schedule,

option_quotes=surface_quotes,

same_date=True,

same_option_type=True,

same_quantity_sign=True,

target_abs_delta=0.50,

dte_tolerance_days=7,

min_future_marks=3,

selector_name="btc_matched_atm_fixed_3d",

)

schedule_report = pd.DataFrame([

{"schedule": "residual", "entries": len(btc_residual_schedule)},

{"schedule": "matched_atm", "entries": len(btc_matched_schedule)},

])

btc_hedge_book = hedge_book_from_schedules(

surface_quotes,

schedules=[btc_residual_schedule, btc_matched_schedule],

lookahead_days=12,

)

empty_result = {

"nav": pd.DataFrame(),

"returns": pd.DataFrame(),

"pnl": pd.DataFrame(),

"components": pd.DataFrame(),

"exposures": pd.DataFrame(),

"trades": pd.DataFrame(),

"summary": pd.DataFrame(),

"diagnostics": {},

}

if btc_residual_schedule.empty or btc_matched_schedule.empty or btc_hedge_book.empty:

btc_residual_results = empty_result

btc_matched_results = empty_result

else:

btc_residual_results = run_scheduled_option_hedging_backtest(

option_path=btc_hedge_book,

entry_schedule=btc_residual_schedule,

spot_series=btc_spot,

greeks=btc_hedge_book,

hedge_price_series=btc_spot,

hedge_dividend_series=None,

hedge_beta_series=None,

strategies=("unhedged", "delta"),

option_multiplier=1.0,

trading_cost_bps=2.0,

use_bid_ask_costs=True,

delta_band=0.10,

delta_inner_band=0.03,

delta_share_lot=0.001,

delta_cooldown_days=0,

max_hold_days=3,

quote_price_unit="usd",

valuation_currency="USD",

pnl_mode="usd_equivalent",

calendar="crypto_24_7",

missing_option_mark="skip_day",

)

btc_matched_results = run_scheduled_option_hedging_backtest(

option_path=btc_hedge_book,

entry_schedule=btc_matched_schedule,

spot_series=btc_spot,

greeks=btc_hedge_book,

hedge_price_series=btc_spot,

hedge_dividend_series=None,

hedge_beta_series=None,

strategies=("unhedged", "delta"),

option_multiplier=1.0,

trading_cost_bps=2.0,

use_bid_ask_costs=True,

delta_band=0.10,

delta_inner_band=0.03,

delta_share_lot=0.001,

delta_cooldown_days=0,

max_hold_days=3,

quote_price_unit="usd",

valuation_currency="USD",

pnl_mode="usd_equivalent",

calendar="crypto_24_7",

missing_option_mark="skip_day",

)

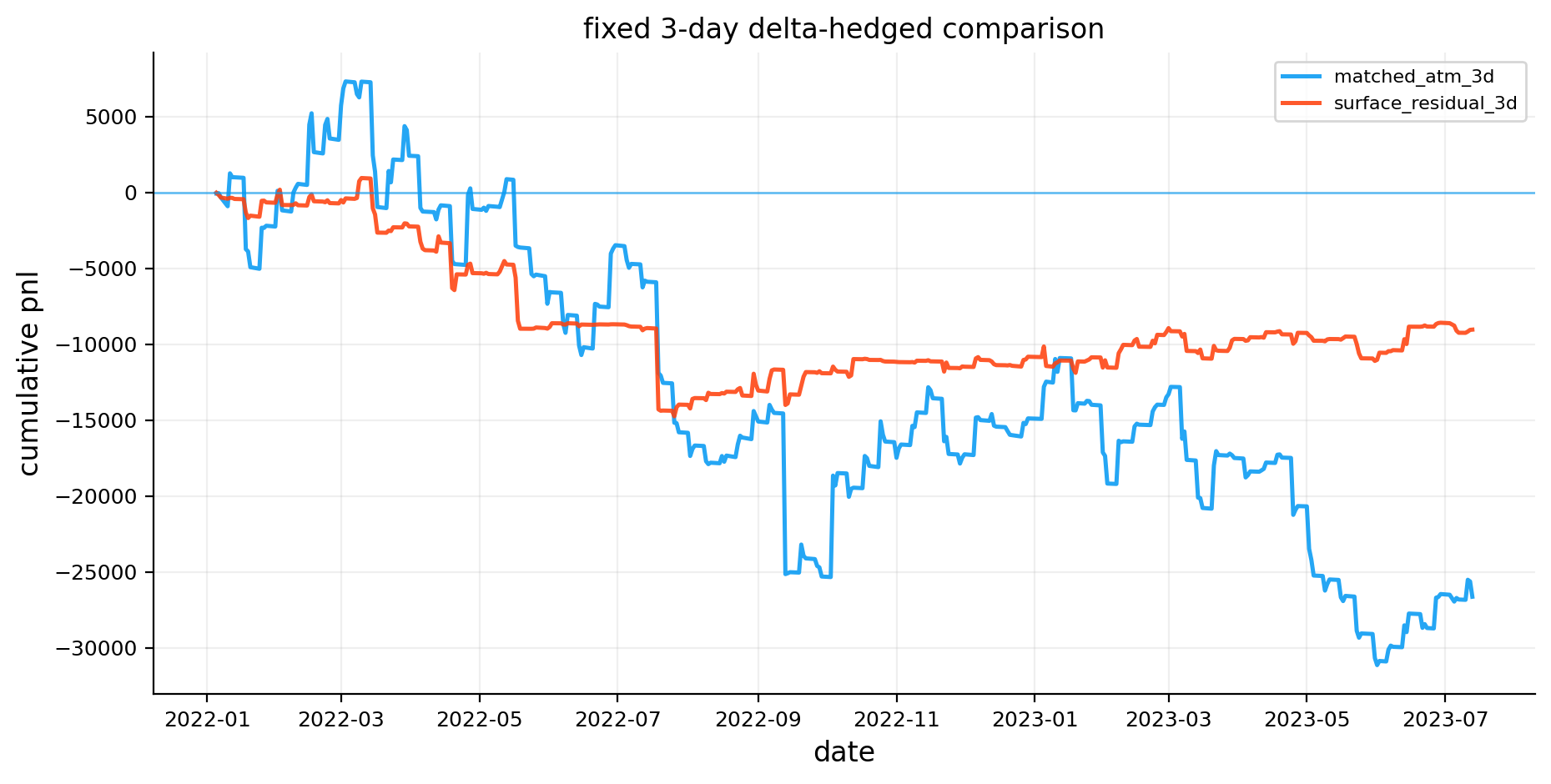

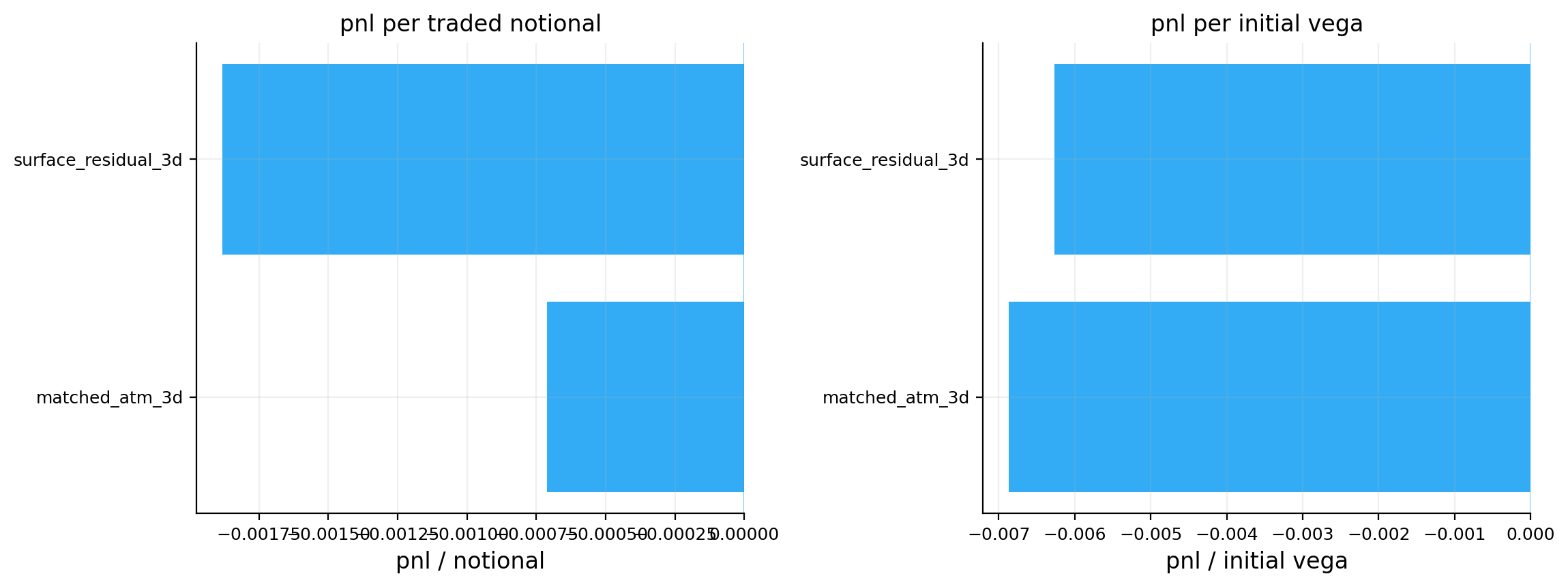

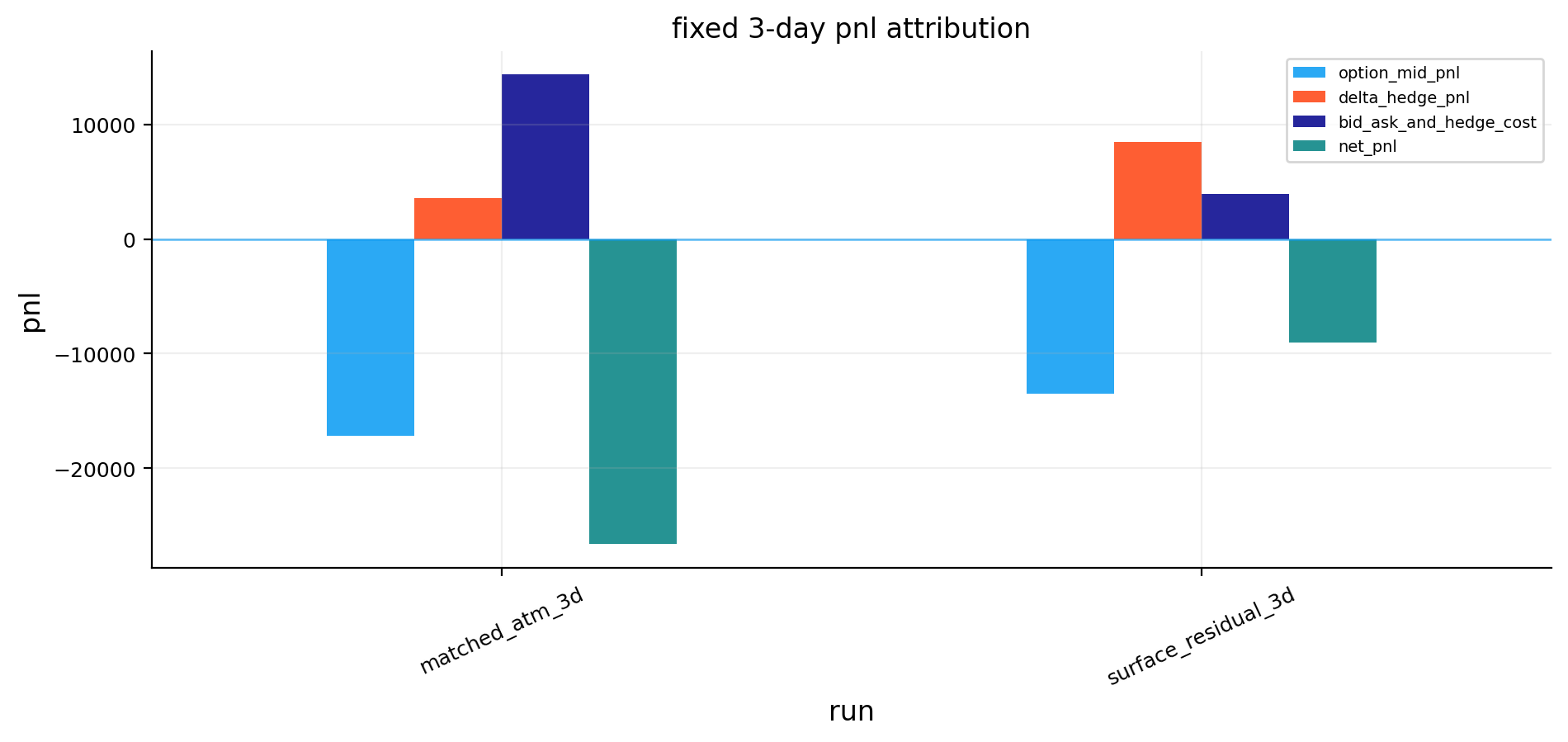

btc_hedge_comparison = scheduled_hedge_comparison(

{

"matched_atm_fixed_3d": btc_matched_results,

"residual_selector_fixed_3d": btc_residual_results,

},

normalize_by=("premium", "traded_notional", "initial_vega"),

)

btc_residual_diag = hedging_diagnostics(btc_residual_results)

btc_matched_diag = hedging_diagnostics(btc_matched_results)

btc_summary = market_summary(

asset="btc",

quotes=btc_day,

model_comparison=model_comparison,

validation=btc_validation,

hedge_comparison=btc_hedge_comparison,

engine=engine,

)

display(clean_report)

display(forward_report)

display(model_comparison)

display(btc_validation.attrs.get("summary", pd.DataFrame()))

display(schedule_report)

display(btc_hedge_comparison)

display(btc_residual_diag)

display(btc_matched_diag)

display(btc_summary)

fig = plt.figure(figsize=(15, 11), constrained_layout=True, dpi=300)

gs = fig.add_gridspec(4, 4)

ax_quote_map = fig.add_subplot(gs[0, 0])

ax_smile_terms = fig.add_subplot(gs[0, 1])

ax_model_overlay = fig.add_subplot(gs[0, 2])

ax_svi = fig.add_subplot(gs[0, 3])

ax_svi_ssvi = fig.add_subplot(gs[1, 0])

ax_ssvi_resid = fig.add_subplot(gs[1, 1])

ax_sabr_smiles = fig.add_subplot(gs[1, 2])

ax_sabr_params = fig.add_subplot(gs[1, 3])

ax_merton = fig.add_subplot(gs[2, 0])

ax_heston_mc = fig.add_subplot(gs[2, 1])

ax_heston_bates = fig.add_subplot(gs[2, 2])

ax_error_runtime = fig.add_subplot(gs[2, 3])

ax_benchmark = fig.add_subplot(gs[3, 0])

ax_disagreement = fig.add_subplot(gs[3, 1])

ax_deciles = fig.add_subplot(gs[3, 2])

ax_hedge = fig.add_subplot(gs[3, 3])

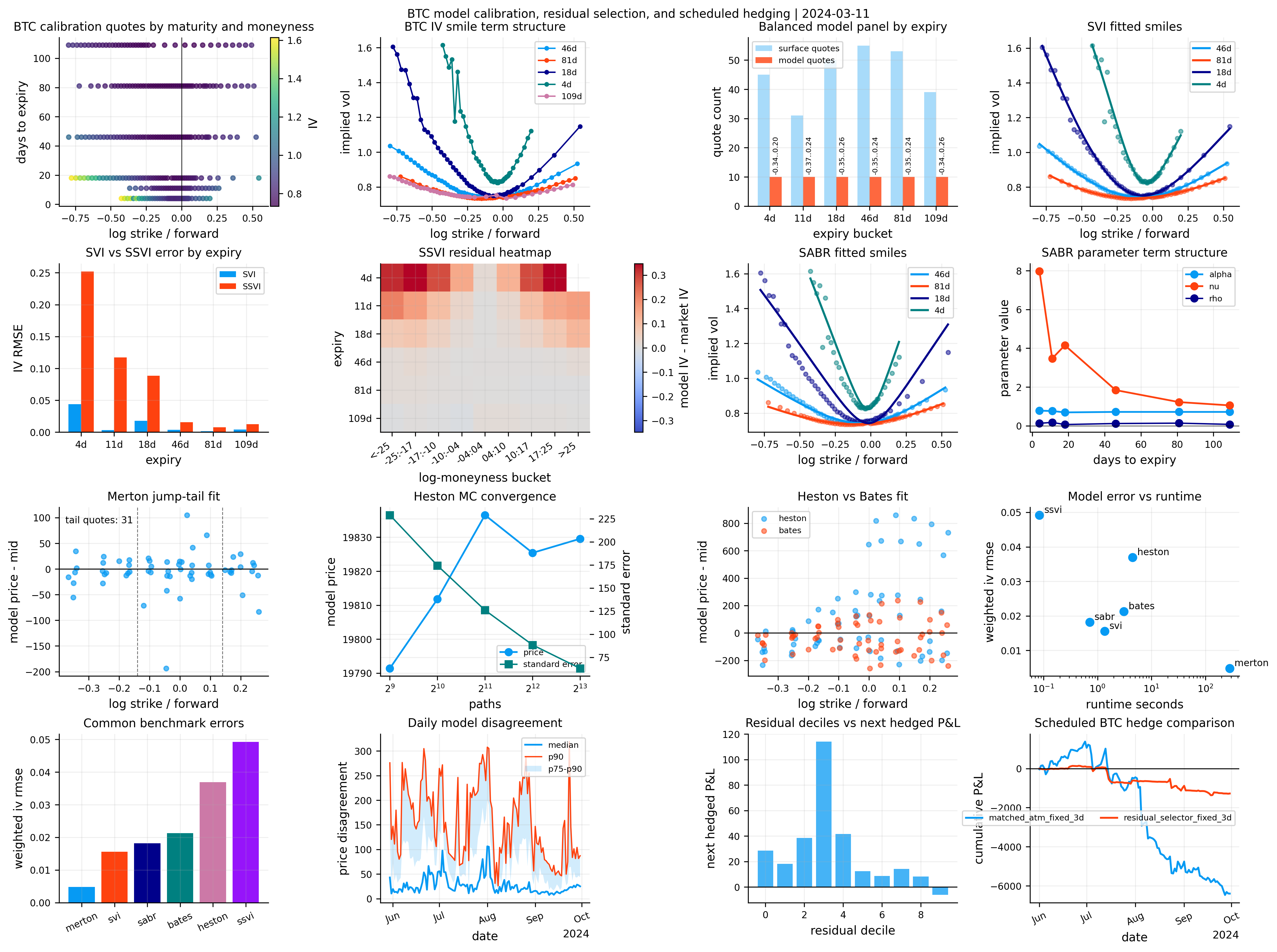

calibration_quote_map(ax_quote_map, btc_day, "k", "tau", "BTC calibration quotes by maturity and moneyness")

smile_term_structure(ax_smile_terms, btc_day, "k", "tau", "iv_mid", "BTC IV smile term structure")

model_quote_overlay(ax_model_overlay, btc_day, btc_model_quotes, "k", "tau", "Balanced model panel by expiry")

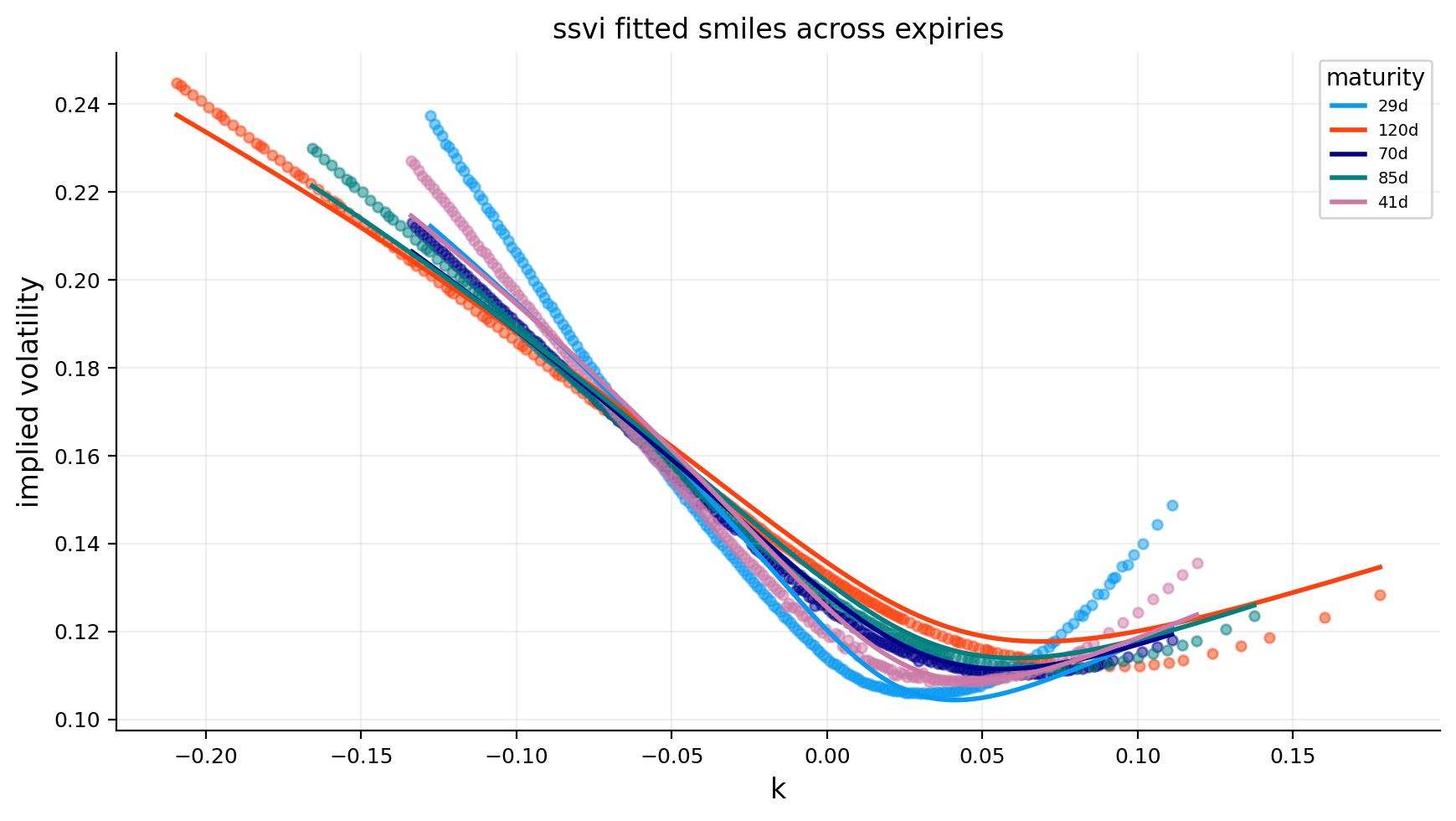

svi_smiles(ax_svi, btc_day, btc_svi, "SVI fitted smiles")

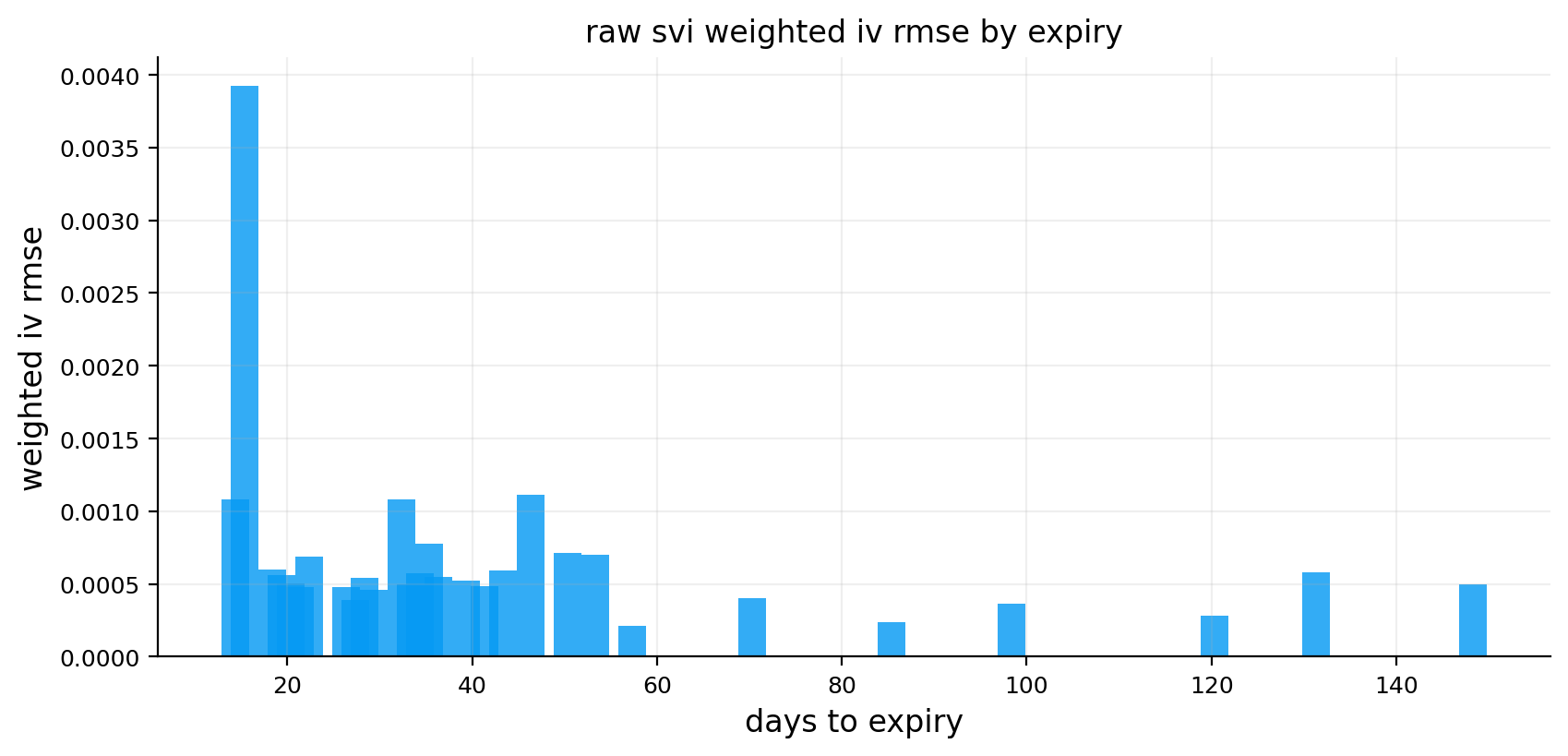

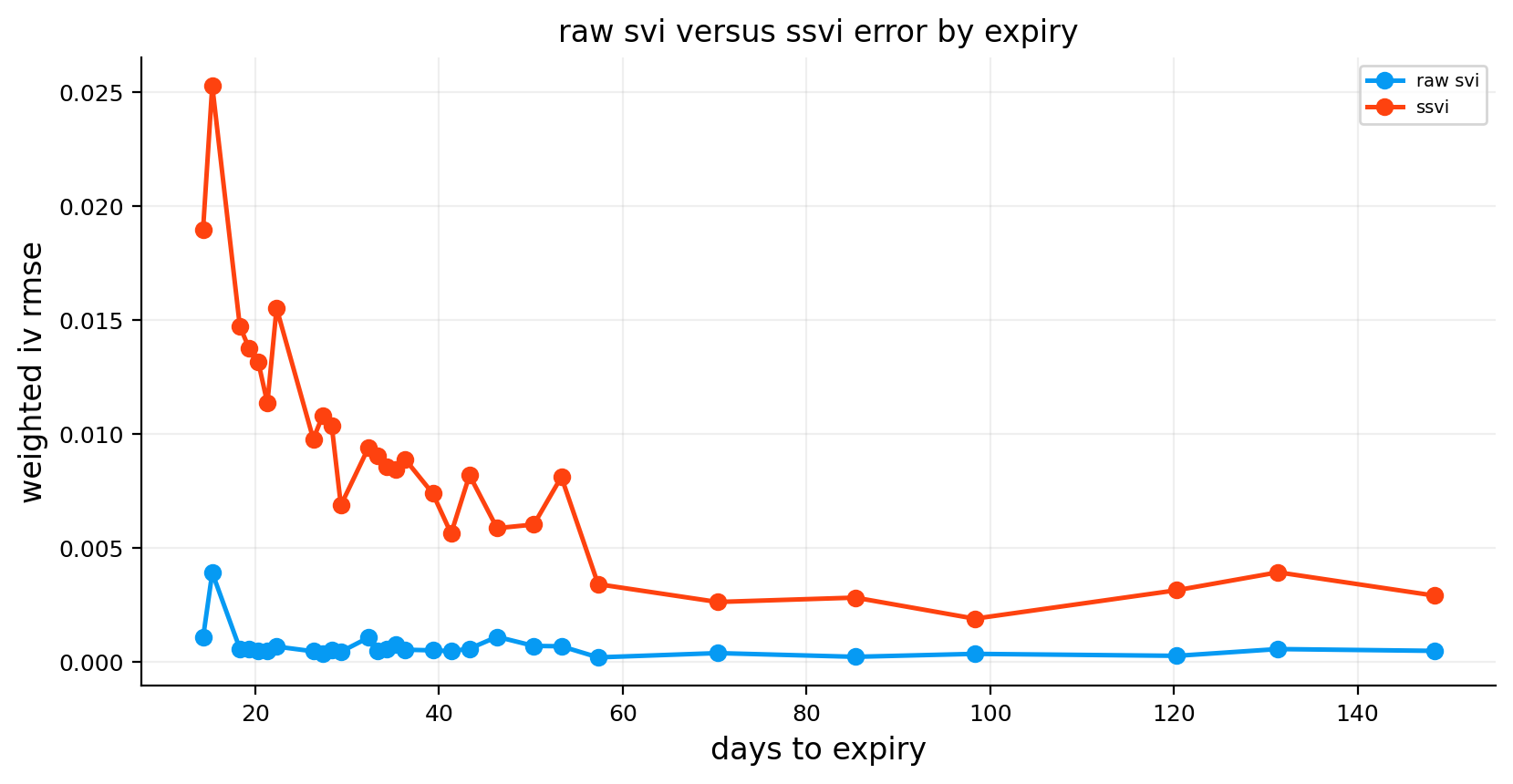

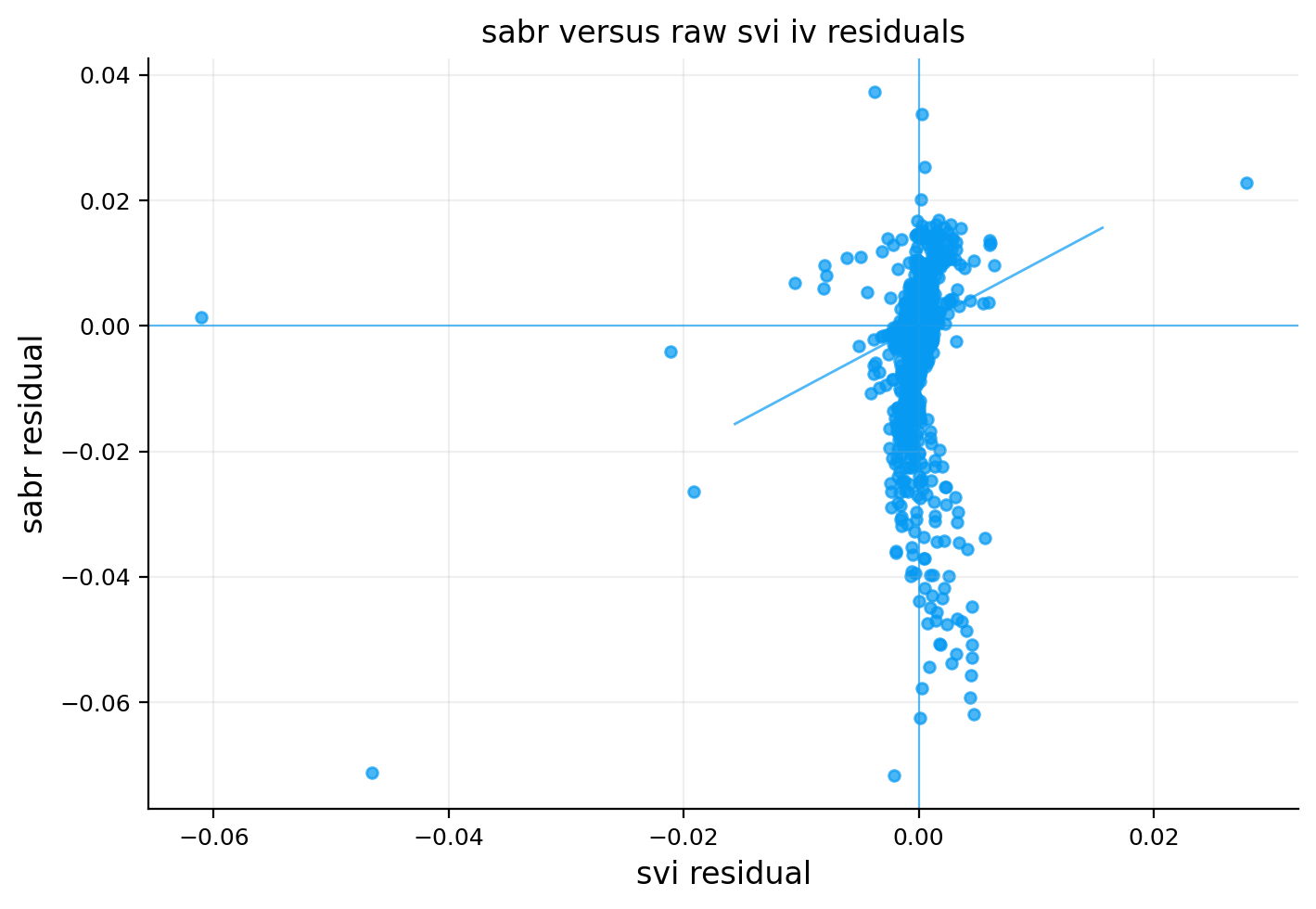

svi_ssvi_errors(ax_svi_ssvi, btc_svi, btc_ssvi, "SVI vs SSVI error by expiry")

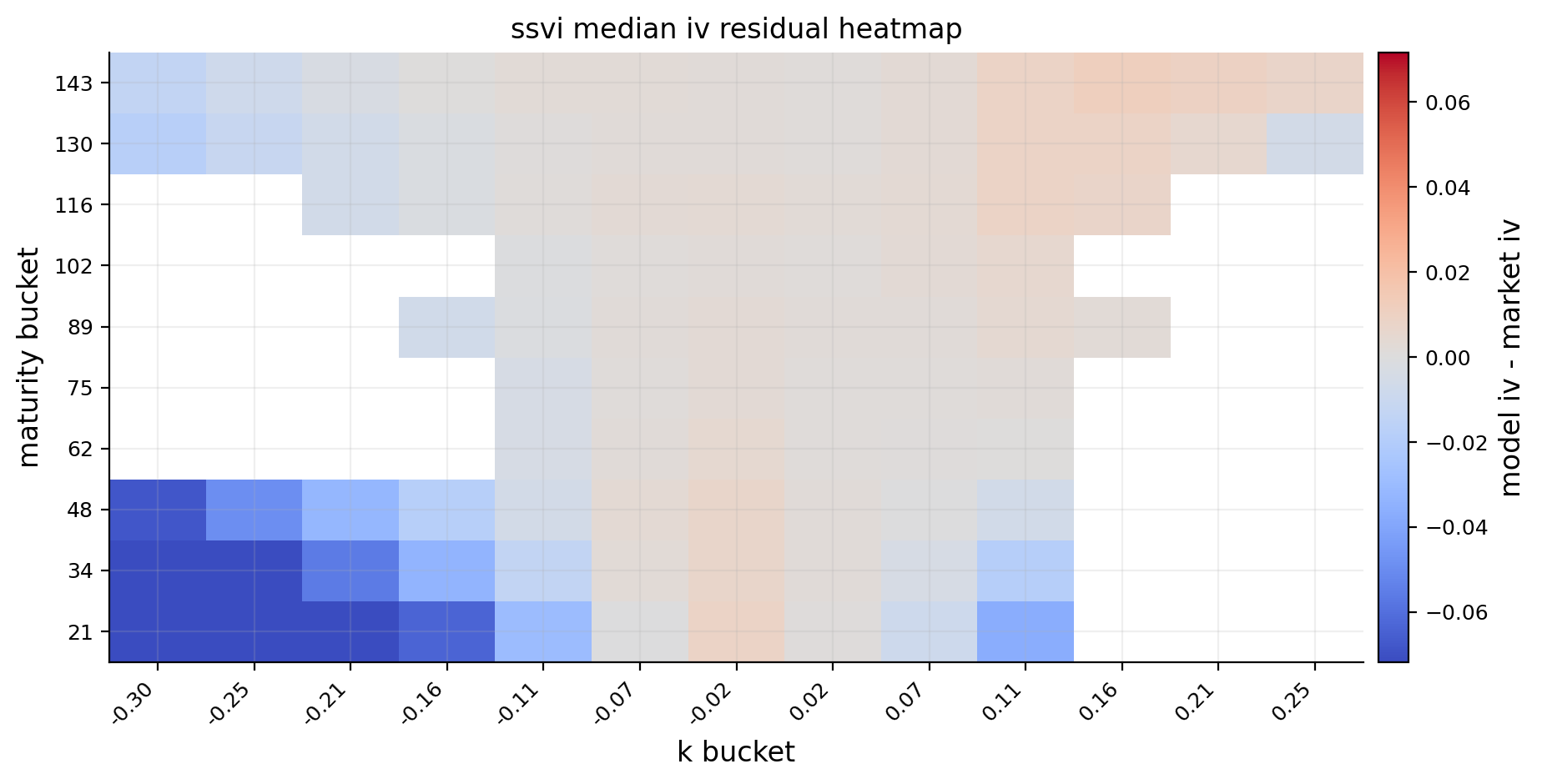

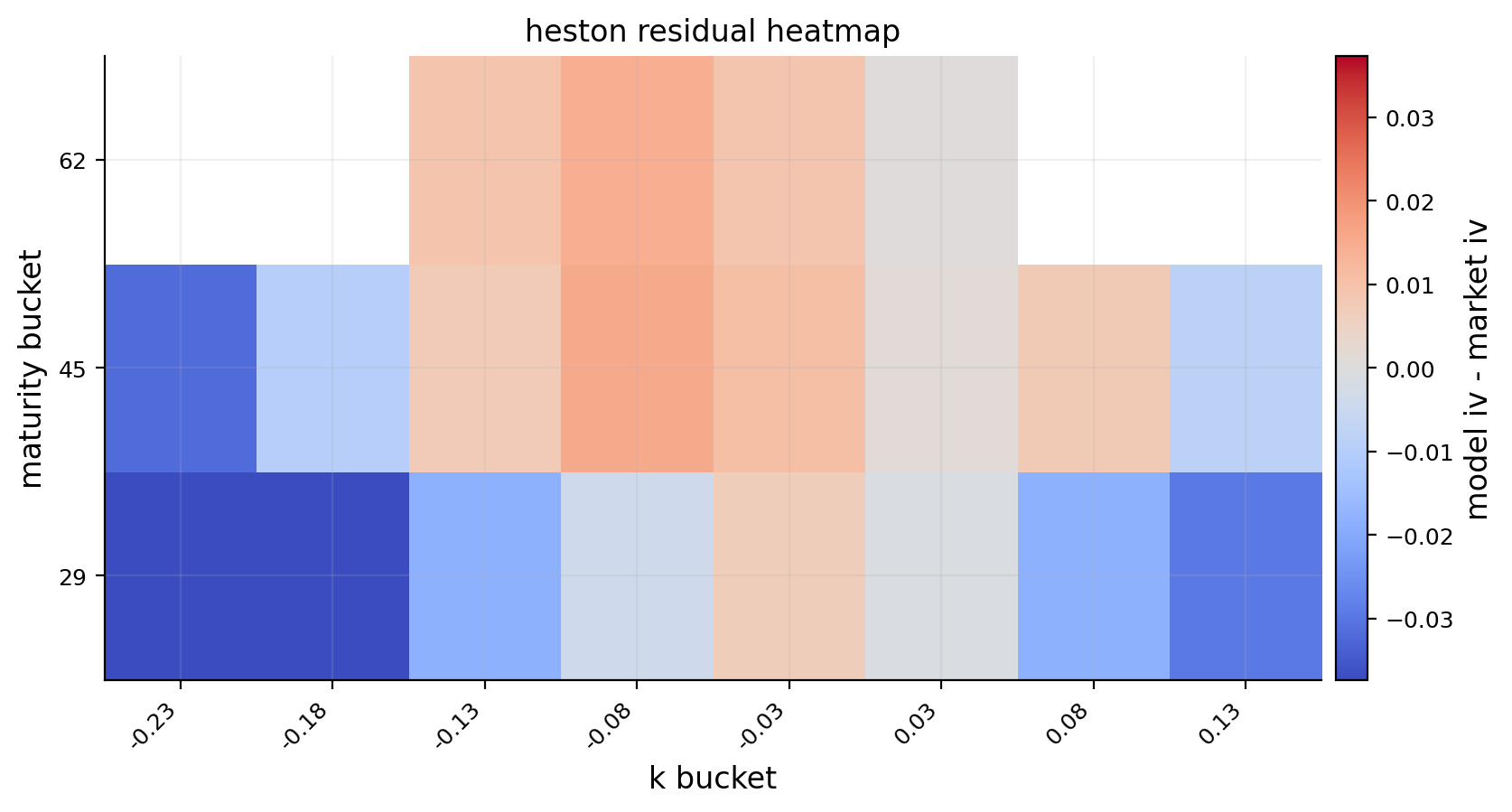

ssvi_residuals(ax_ssvi_resid, btc_day, btc_ssvi, "SSVI residual heatmap")

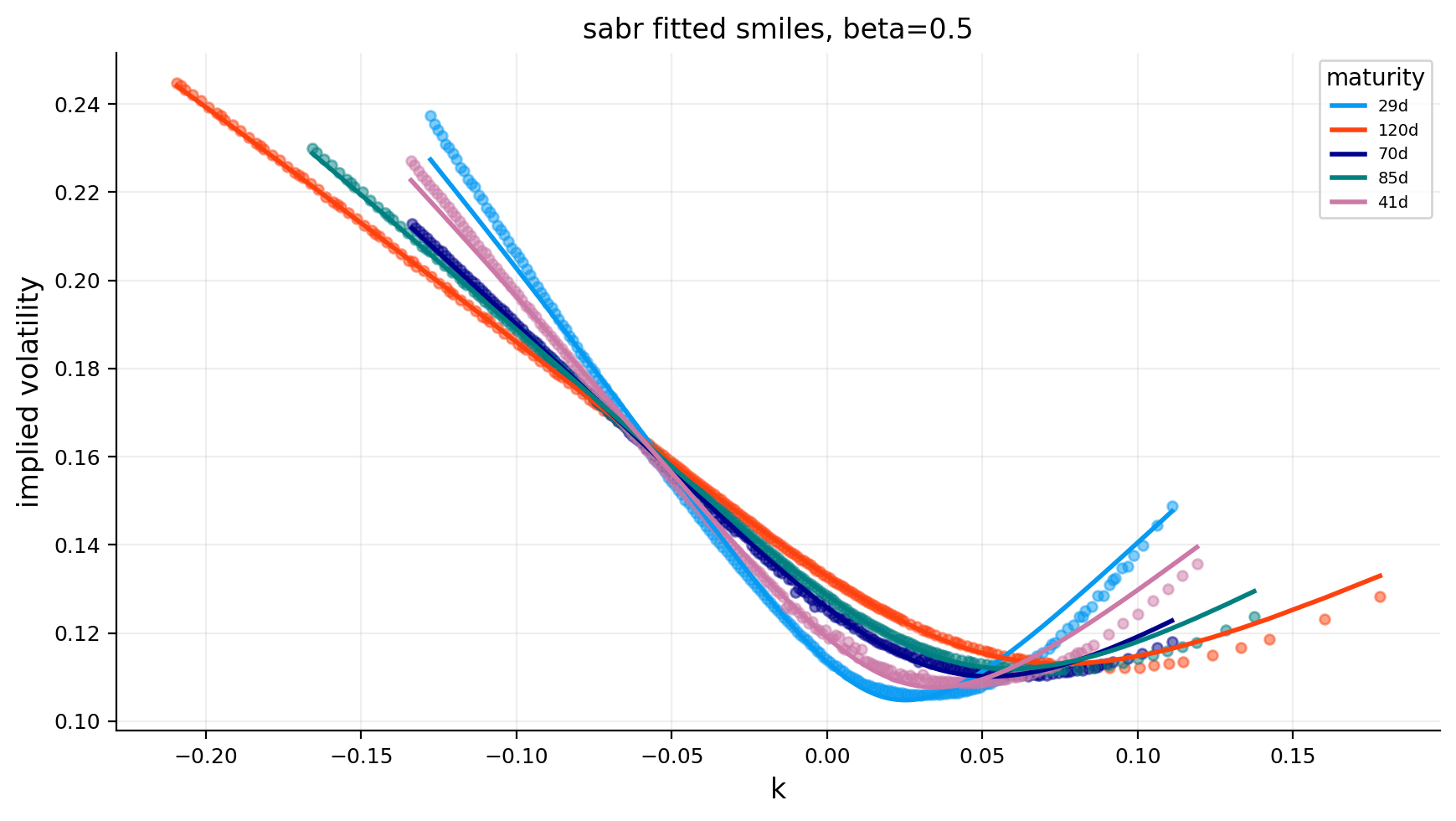

sabr_smiles(ax_sabr_smiles, btc_day, btc_sabr, "SABR fitted smiles")

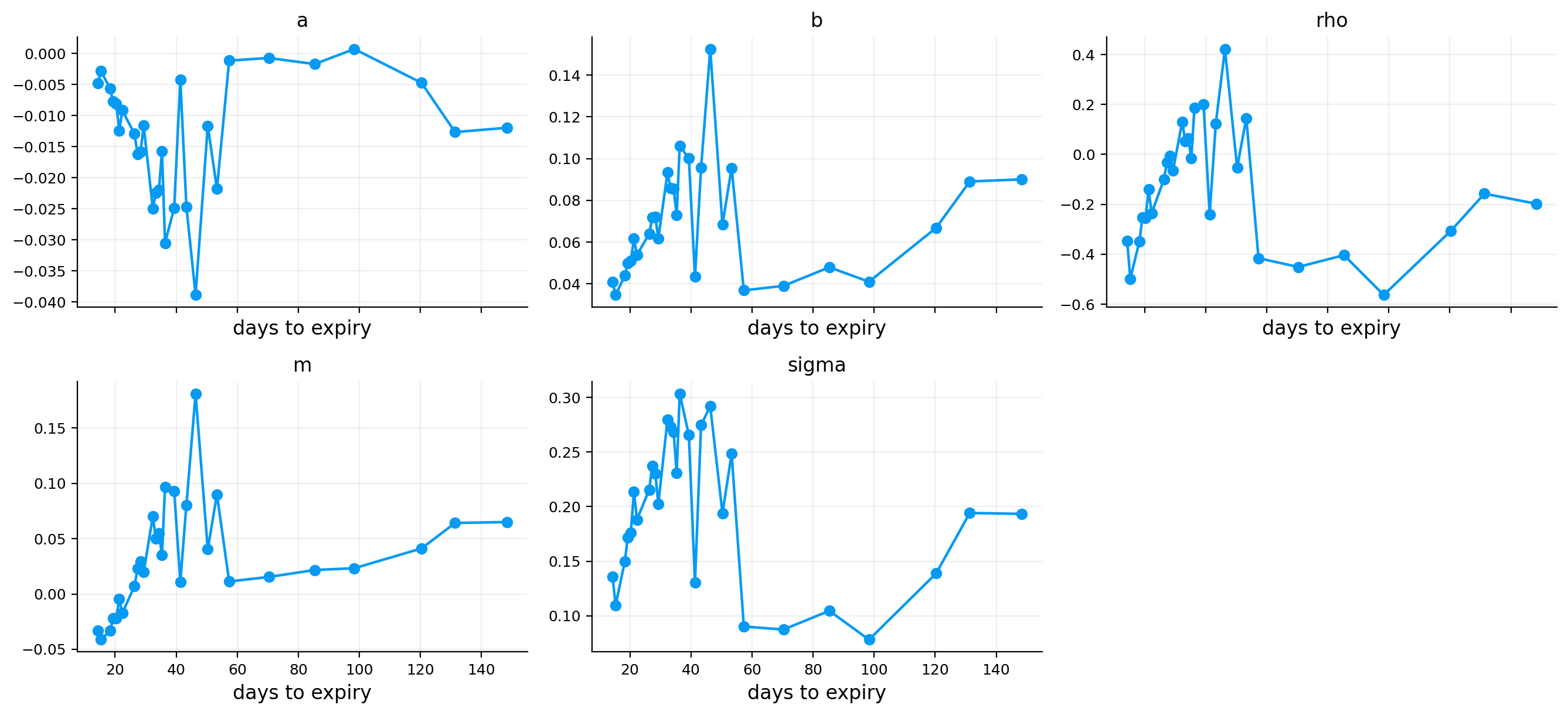

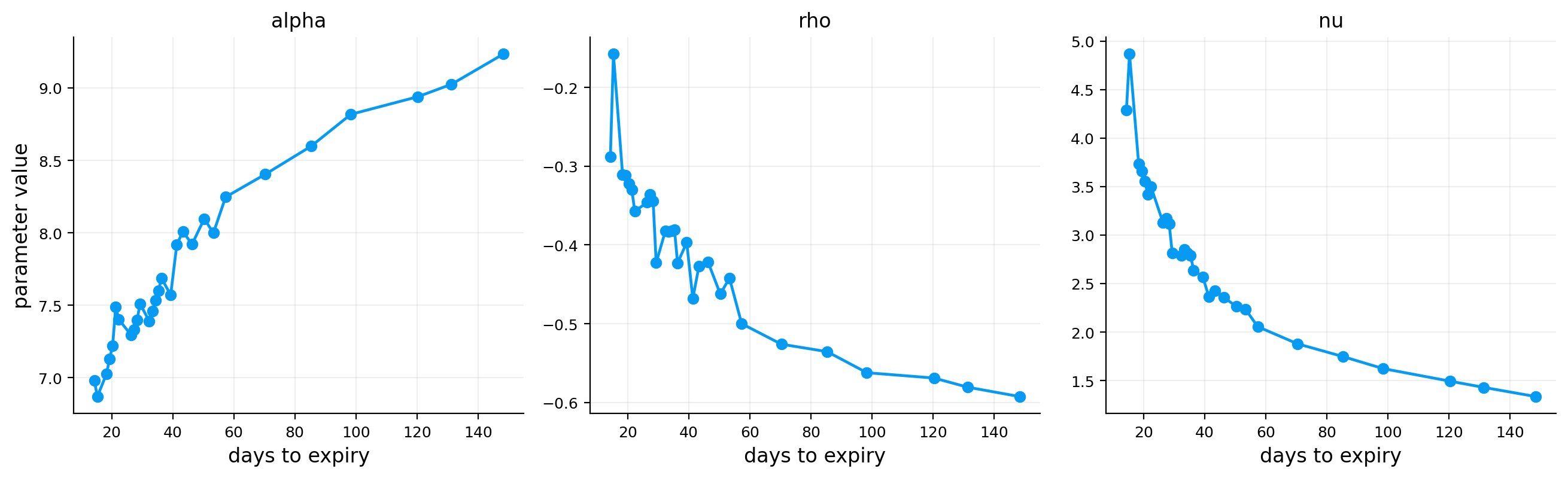

sabr_terms(ax_sabr_params, btc_sabr, "SABR parameter term structure")

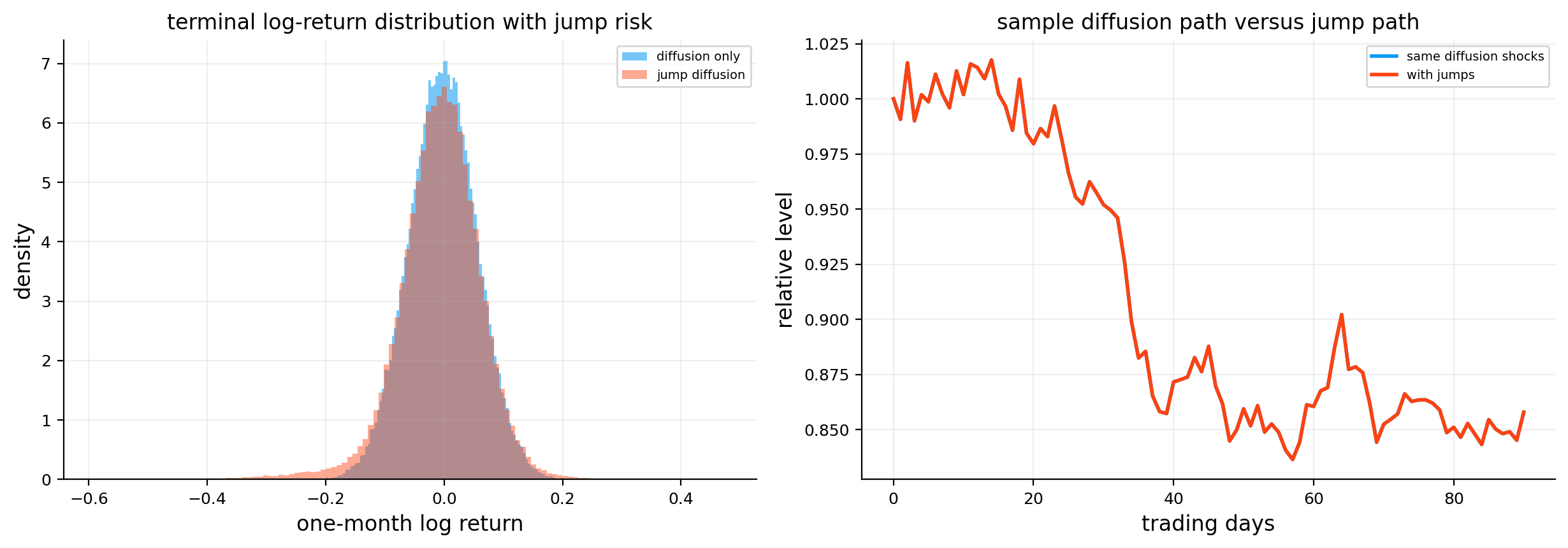

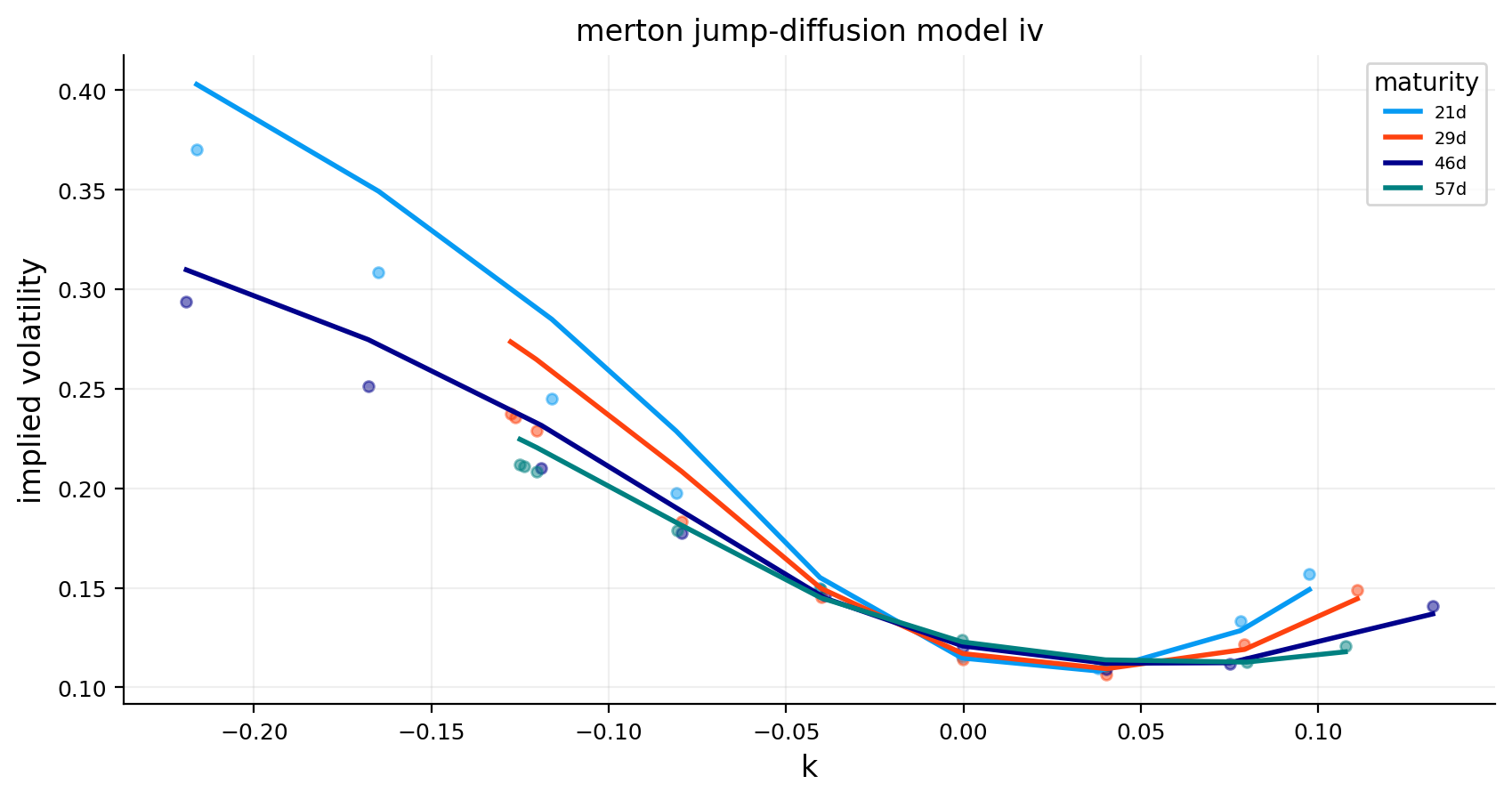

merton_tail_fit(ax_merton, btc_model_quotes, btc_merton, "Merton jump-tail fit")

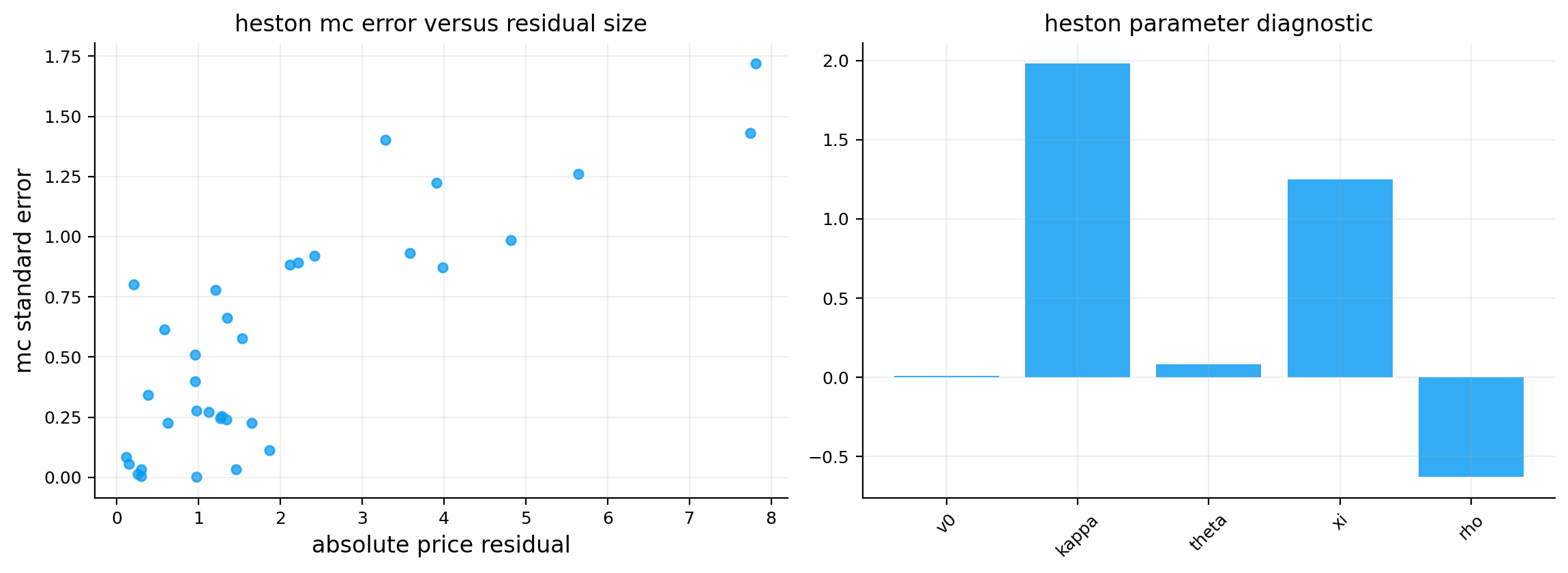

heston_mc_check(ax_heston_mc, btc_heston, "Heston MC convergence")

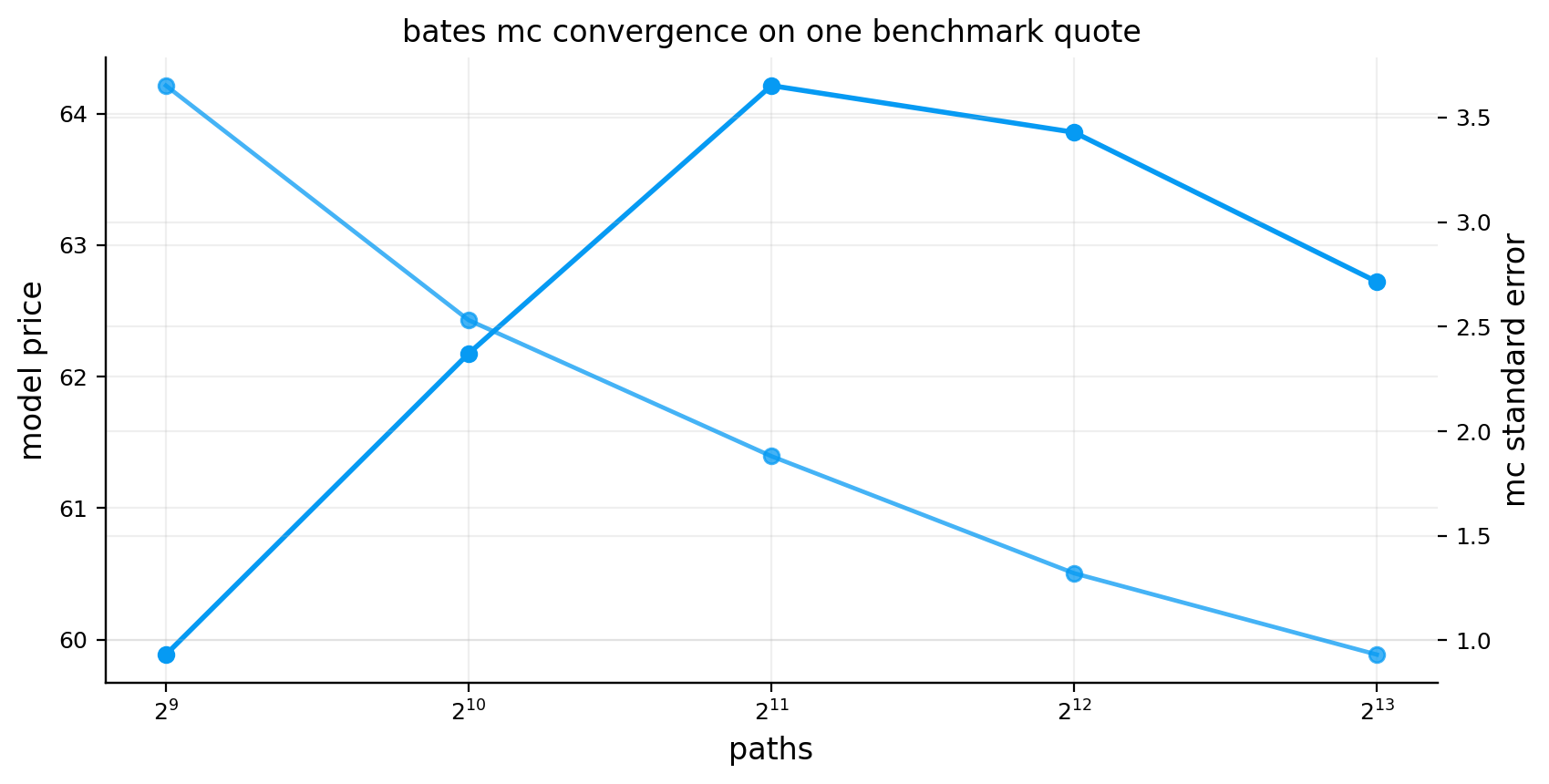

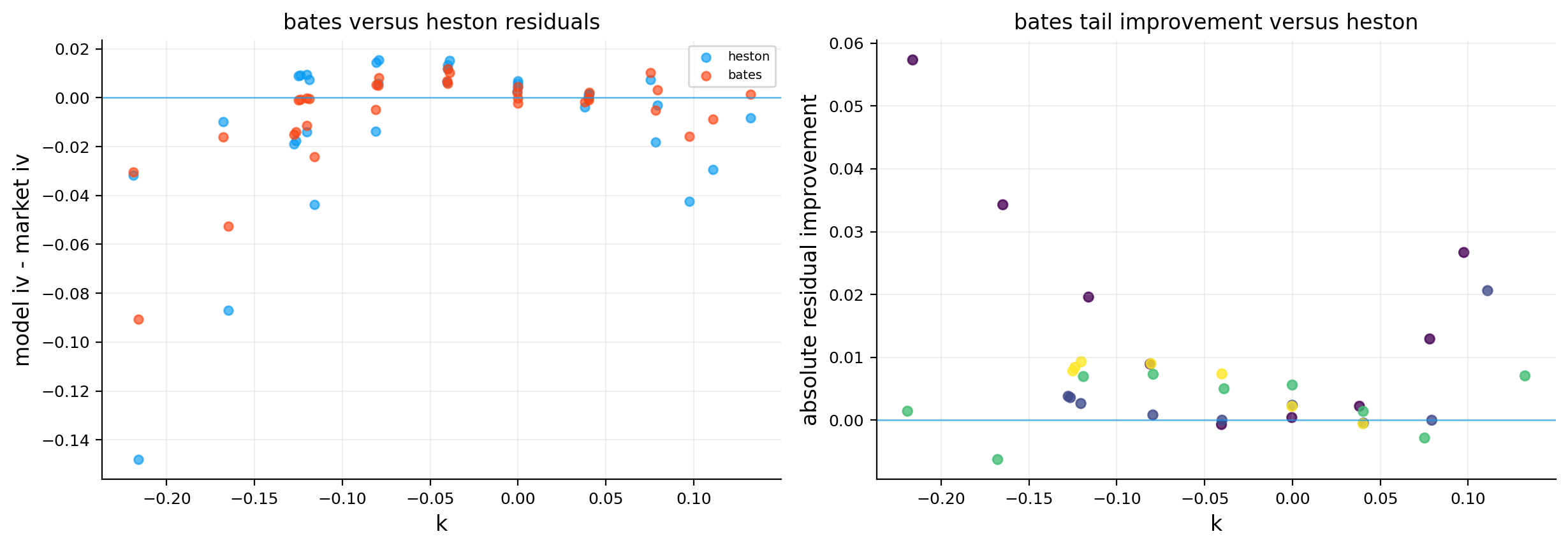

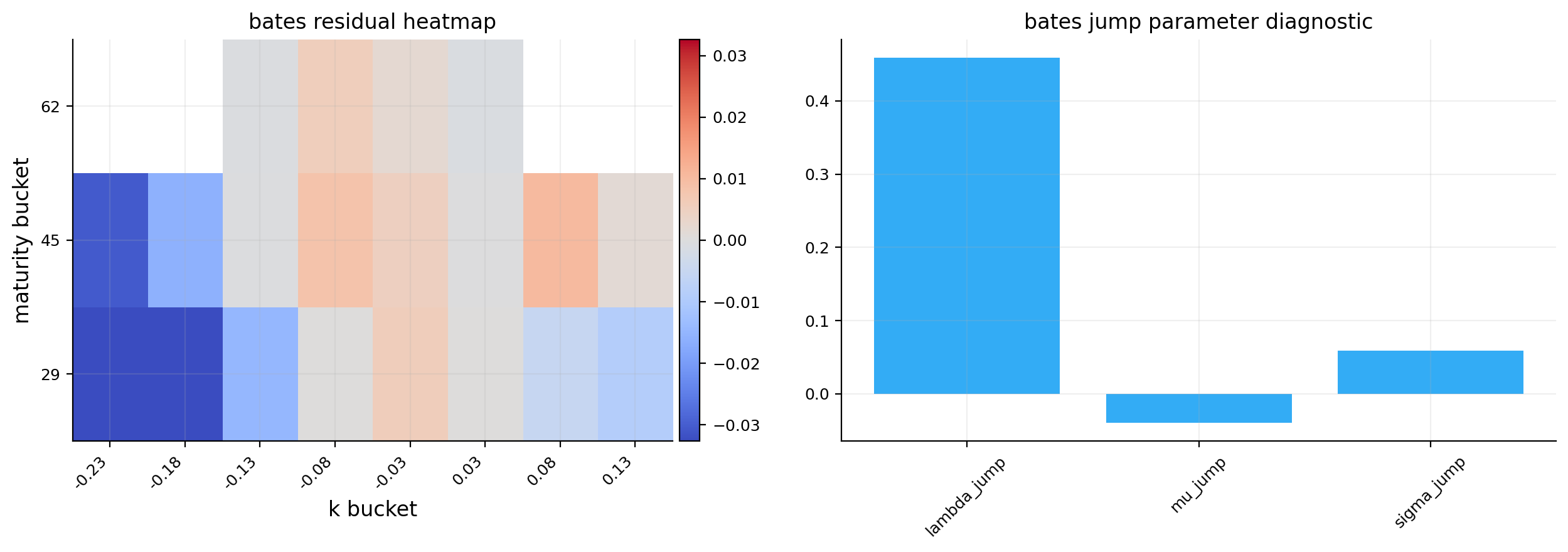

heston_bates_fit(ax_heston_bates, btc_model_quotes, btc_heston, btc_bates, "Heston vs Bates fit")

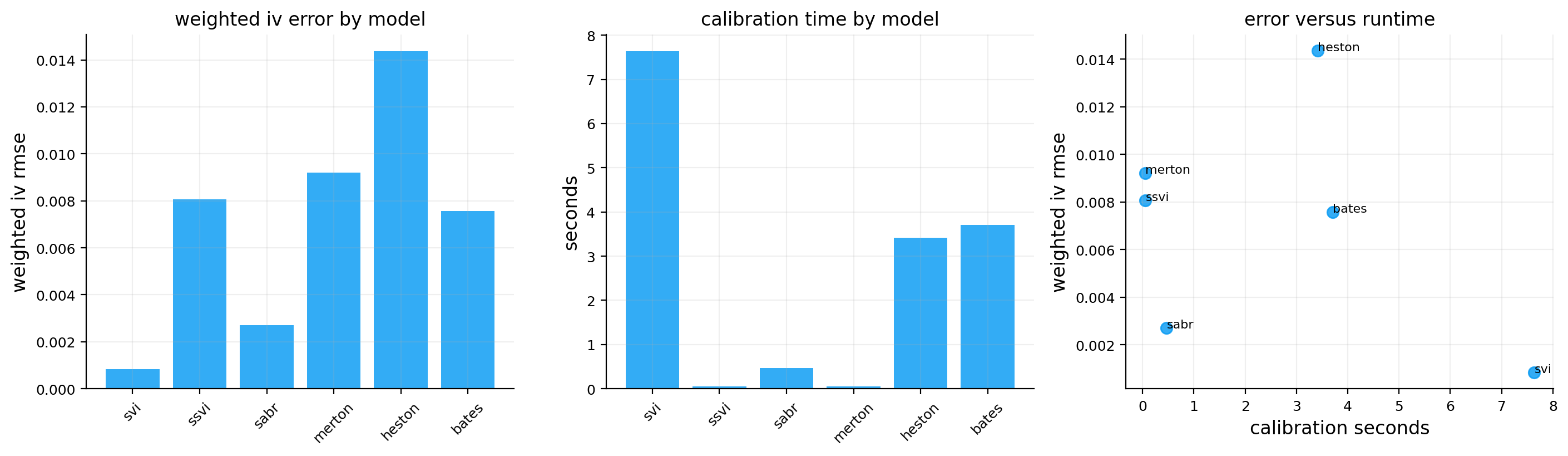

model_speed_accuracy(ax_error_runtime, model_comparison, "Model error vs runtime")

benchmark_errors(ax_benchmark, model_comparison, "Common benchmark errors")

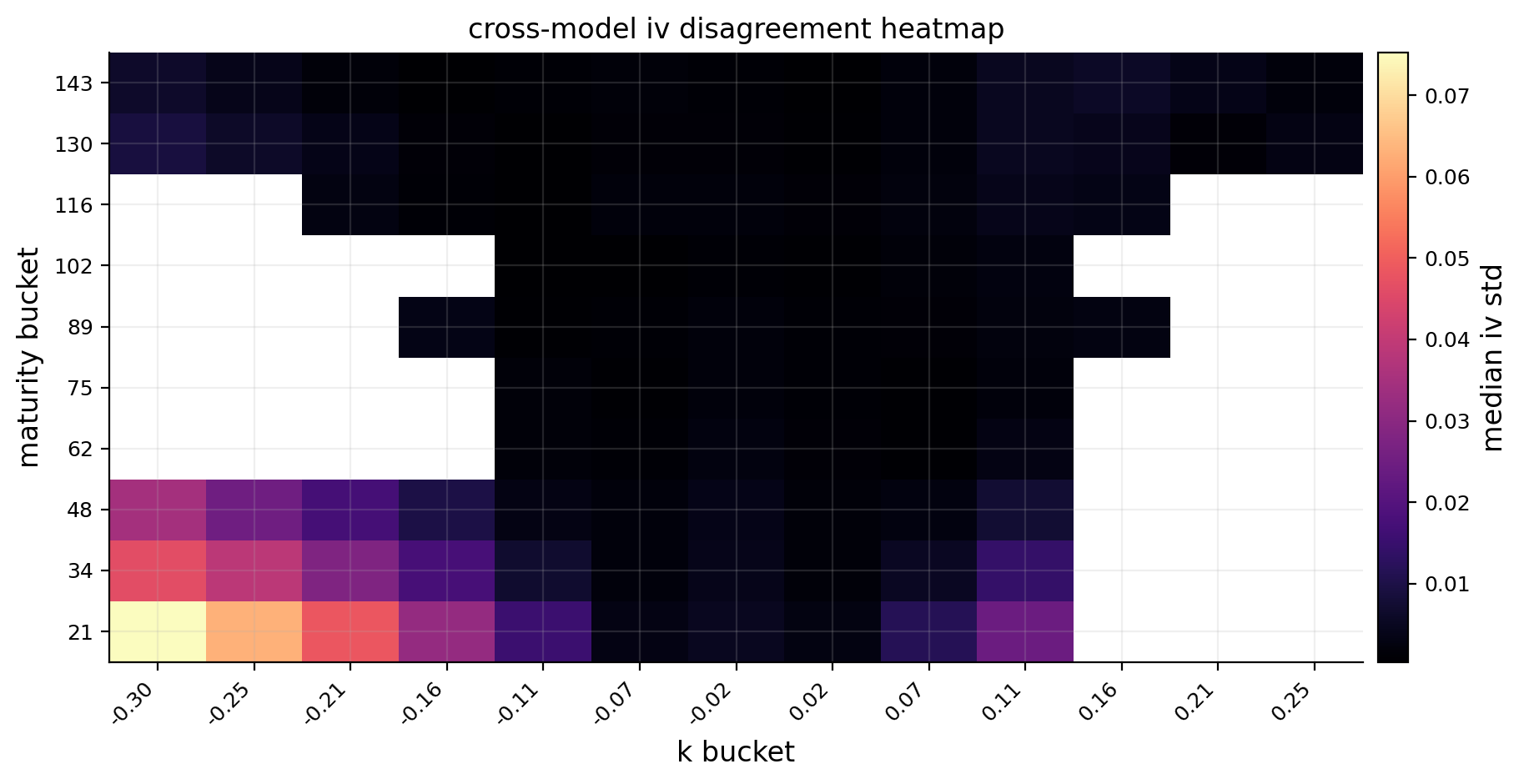

model_disagreement(ax_disagreement, btc_fair_values, "Daily model disagreement")

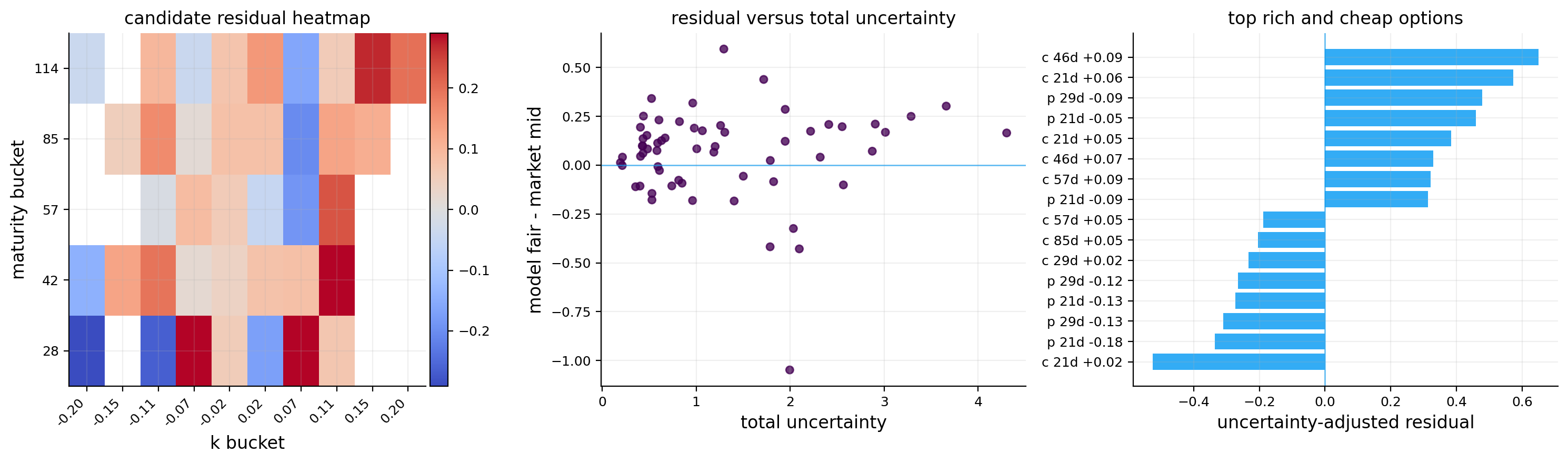

residual_deciles(ax_deciles, btc_validation, "Residual deciles vs next hedged P&L")

scheduled_hedge_equity(ax_hedge, {"matched_atm_fixed_3d": btc_matched_results, "residual_selector_fixed_3d": btc_residual_results}, btc_hedge_comparison, "Scheduled BTC hedge comparison")

for ax in fig.axes:

ax.title.set_fontsize(10)

ax.tick_params(axis="both", labelsize=8)

fig.suptitle(

f"BTC model calibration, residual selection, and scheduled hedging | {pd.Timestamp(main_date).date()}",

fontsize=10,

y=1.01,

)

plt.show()