import warnings

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

from IPython.display import display

from quantfinlab.dataio import load_ohlcv, load_yfinance_panel

from quantfinlab.portfolio import covariance, expected_returns, optimizers, universe, walkforward

from quantfinlab.risk import (

capm, contributions,

correlation, distribution,

drawdown, performance,

stress, var, var_backtesting)

from quantfinlab.plotting import risk as risk_plots

warnings.filterwarnings("ignore")

rf_annual = 0.04

rf_daily = (1.0 + rf_annual) ** (1.0 / 252.0) - 1.0

us_finalists = ["EW", "MinVar EWMA", "MinVar Samp",

"MV EWMA Mom", "MV EWMA BSM",

"Ridge EWMA Mom", "MS EWMA Mom", "MS-FG EWMA Mom"]

us_strategy_specs = [

{"name": "EW", "optimizer": "EW"},

{"name": "MinVar EWMA", "optimizer": "MinVar", "cov_model": "EWMA"},

{"name": "MinVar Samp", "optimizer": "MinVar", "cov_model": "Sample"},

{"name": "MV EWMA Mom", "optimizer": "MV", "cov_model": "EWMA", "mu_model": "Momentum"},

{"name": "MV EWMA BSM", "optimizer": "MV", "cov_model": "EWMA", "mu_model": "BayesSteinMomentum"},

{"name": "Ridge EWMA Mom", "optimizer": "RidgeMV", "cov_model": "EWMA", "mu_model": "Momentum"},

{"name": "MS EWMA Mom", "optimizer": "MaxSharpe", "cov_model": "EWMA", "mu_model": "Momentum"},

{"name": "MS-FG EWMA Mom", "optimizer": "FrontierGrid", "cov_model": "EWMA", "mu_model": "Momentum"}]

panels = load_yfinance_panel(

"../data/nasdaq_close_volume.parquet",

source="yfinance_export",

fields=("close", "volume"),

date_col="Date")

close_prices, volumes = universe.clean_close_volume_panels(

panels["close"], panels["volume"], start="2016-01-01")

returns = universe.prices_to_returns(close_prices)

rebal_dates = universe.make_rebalance_dates(

returns.index, freq="ME", min_history_days=252)

stack = walkforward.run_walkforward_grid(

returns=returns, close=close_prices, volume=volumes,

rebalance_dates=rebal_dates,

cov_models={"EWMA": covariance.ewma_covariance, "Sample": covariance.sample_covariance},

mu_models={"Momentum": expected_returns.momentum_mu,

"BayesSteinMomentum": expected_returns.bayes_stein_momentum_mu},

optimizers={

"EW": optimizers.equal_weight,

"MinVar": optimizers.minimum_variance,

"MV": optimizers.mean_variance,

"RidgeMV": optimizers.ridge_mean_variance,

"MaxSharpe": optimizers.max_sharpe_slsqp,

"FrontierGrid": optimizers.max_sharpe_frontier_grid},

strategy_specs=us_strategy_specs,

rf_daily=rf_daily,

annualization=252)

results = {name: stack.backtests[name] for name in us_finalists}

display(stack.results.loc[us_finalists].round(4))

cache = dict(stack.cache)

def _default_cov_key(state_cache):

for state in state_cache.values():

cov_map = state.get("cov_ann_map", {})

for preferred in ("LedoitWolf", "OAS", "Sample", "EWMA", "ledoitwolf", "oas", "sample", "ewma"):

if preferred in cov_map:

return preferred

if cov_map:

return next(iter(cov_map.keys()))

return None

def _cov_key_for_backtest(result, fallback):

meta = dict(result.metadata or {})

return meta.get("cov_model") or fallback

fallback_cov_key = _default_cov_key(cache)

cov_key_for_rc = {name: _cov_key_for_backtest(res, fallback_cov_key) for name, res in results.items()}

common_idx = None

for res in results.values():

idx_res = pd.DatetimeIndex(res.net_returns.index)

common_idx = idx_res if common_idx is None else common_idx.intersection(idx_res)

if common_idx is None or len(common_idx) == 0:

raise ValueError("No overlapping index across US finalist returns.")

objects = {name: res.net_returns.reindex(common_idx).fillna(0.0) for name, res in results.items()}

spy = load_ohlcv("../data/spy_ohlcv.csv", source="yfinance_csv", fields=("close",))

market_ret = spy["close"].pct_change(fill_method=None).reindex(common_idx).fillna(0.0)

portfolios = {

name: {"backtest": results[name], "state_cache": cache, "cov_key": cov_key_for_rc[name]}

for name in results.keys()}

perf_tbl = performance.performance_table(objects, rf_daily=rf_daily, annualization=252)

shape_tbl = distribution.tail_shape_table(objects)

dd_summary_tbl = drawdown.drawdown_summary_table(objects)

dd_episodes_tbl = drawdown.drawdown_episodes_table(objects, top_n=1)

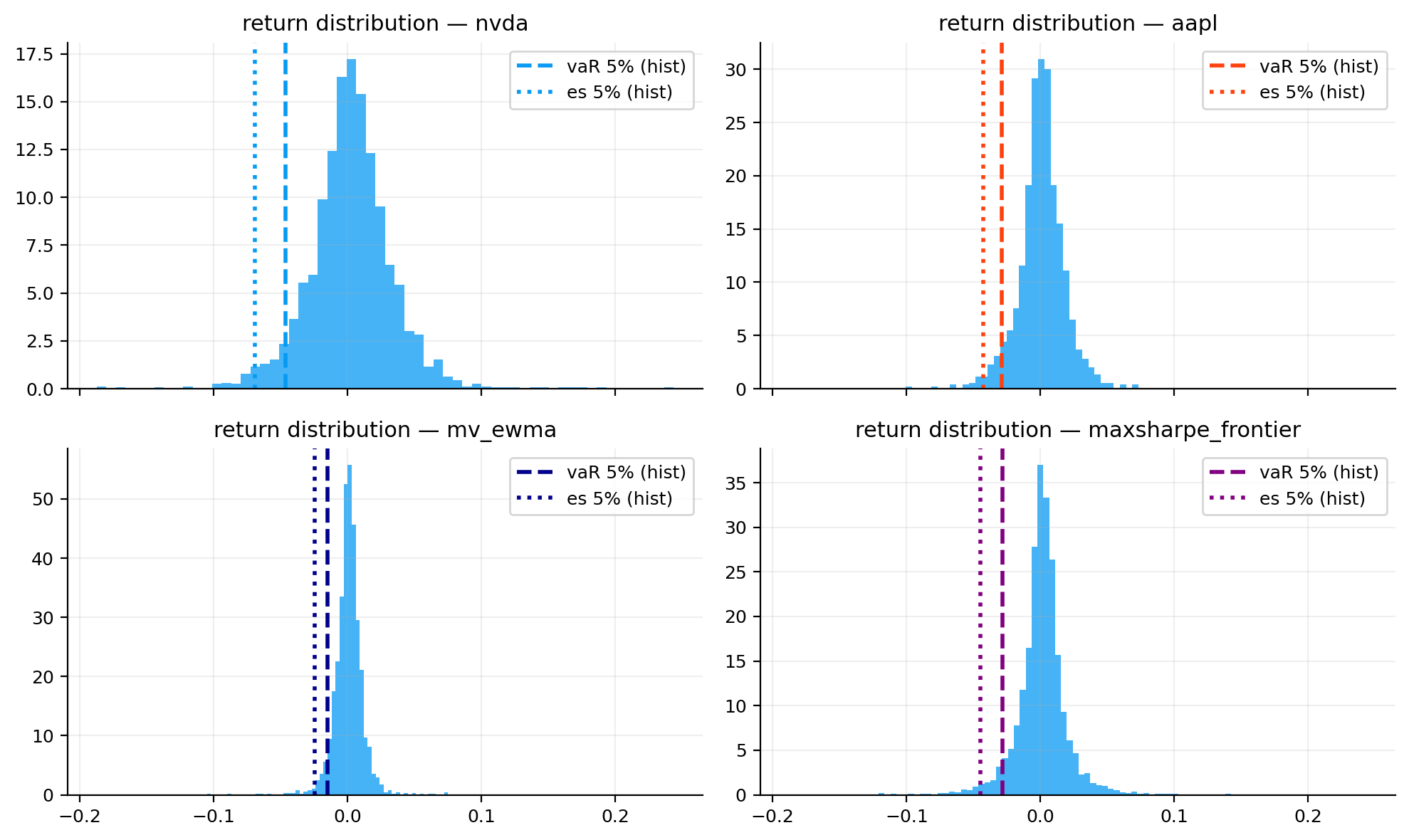

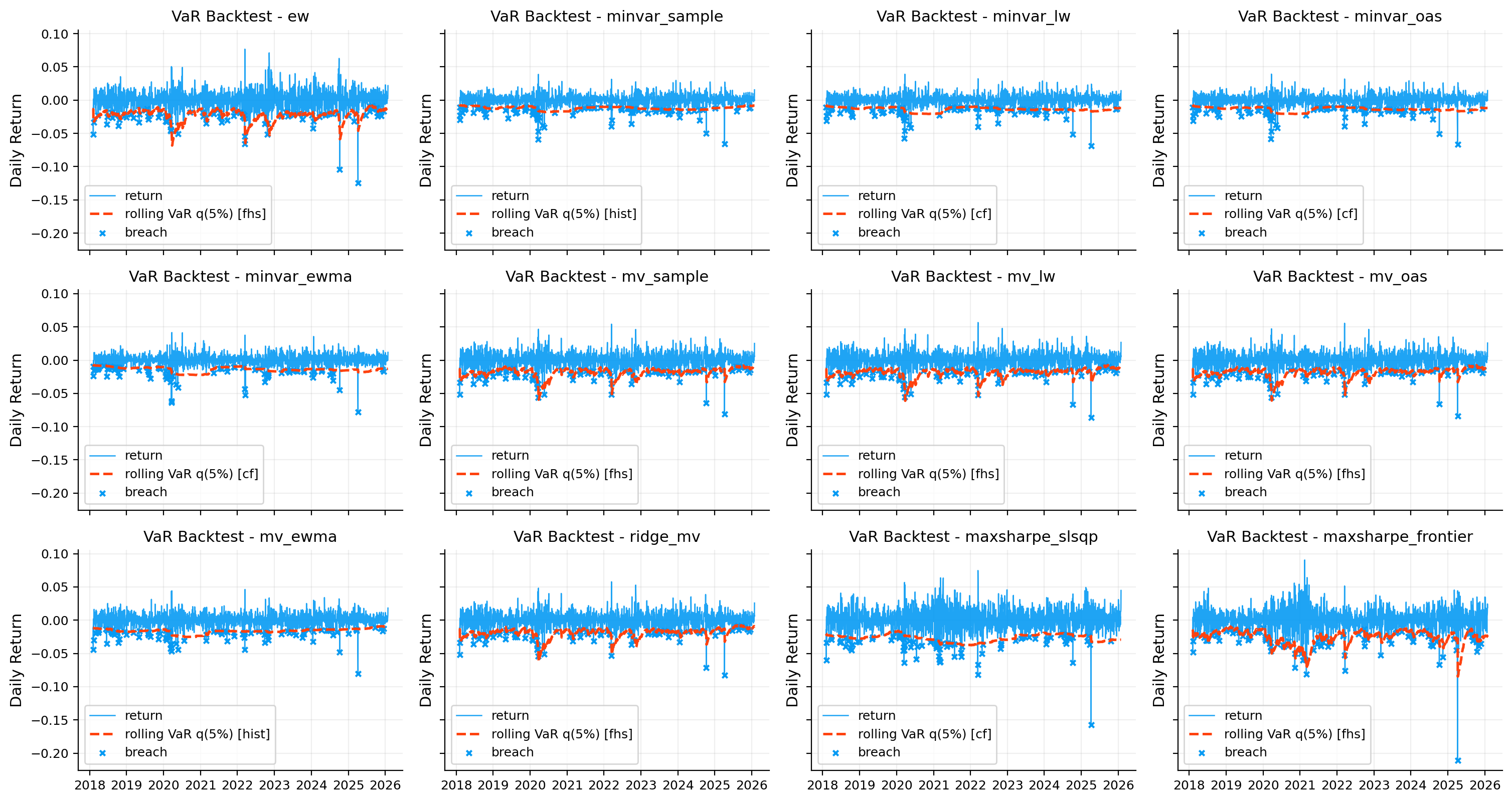

var_es_tbl = var.var_es_table(objects, alpha=0.05, methods=["hist", "cf", "fhs"])

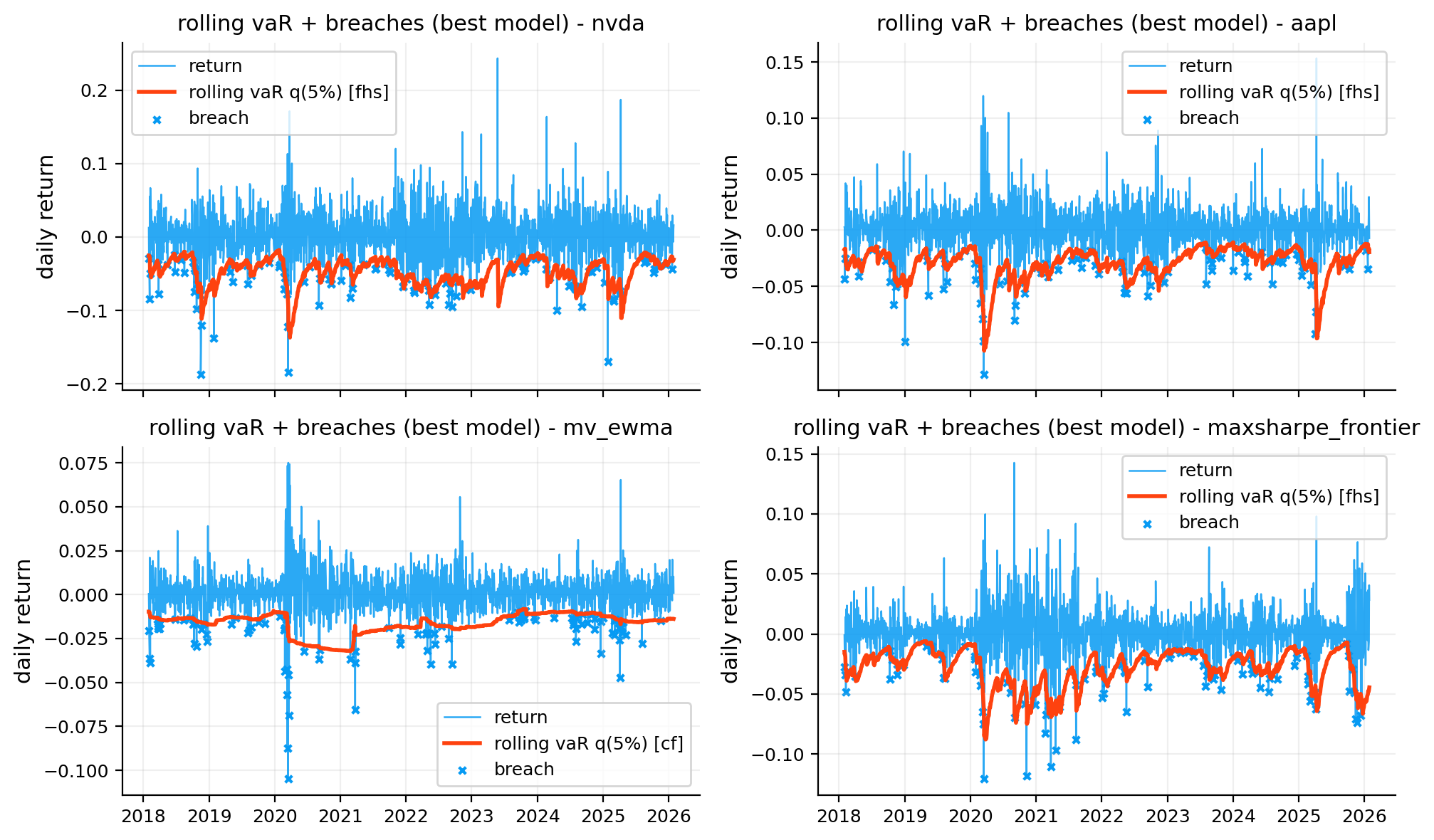

var_bt_tbl = var_backtesting.var_backtest_table(objects, alpha=0.05, methods=["hist", "cf", "fhs"], lookback=252)

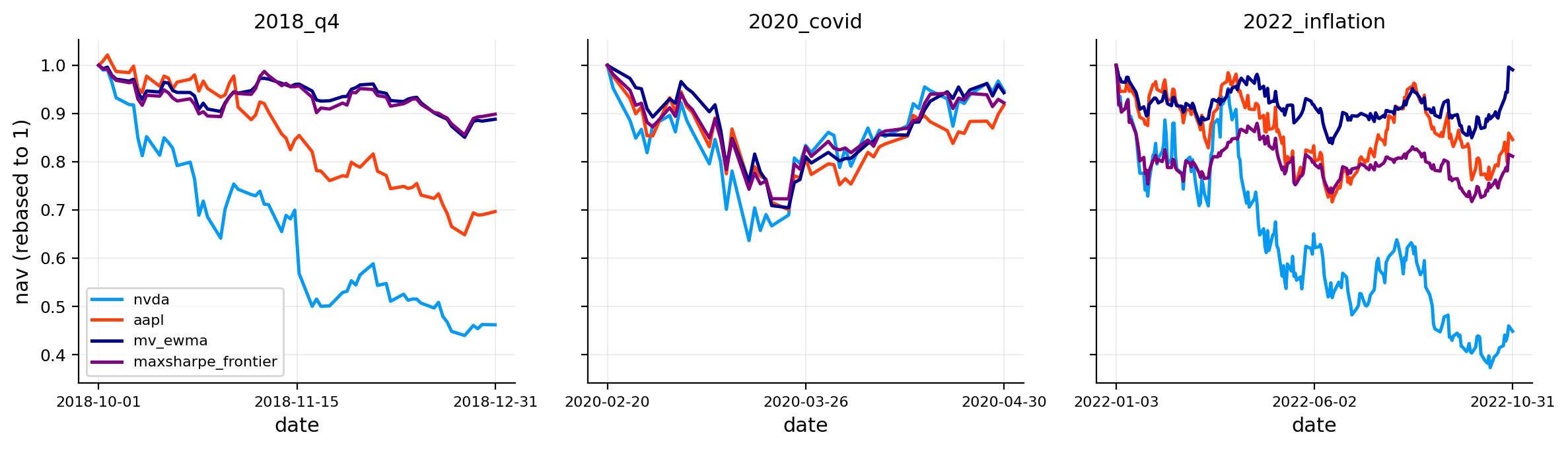

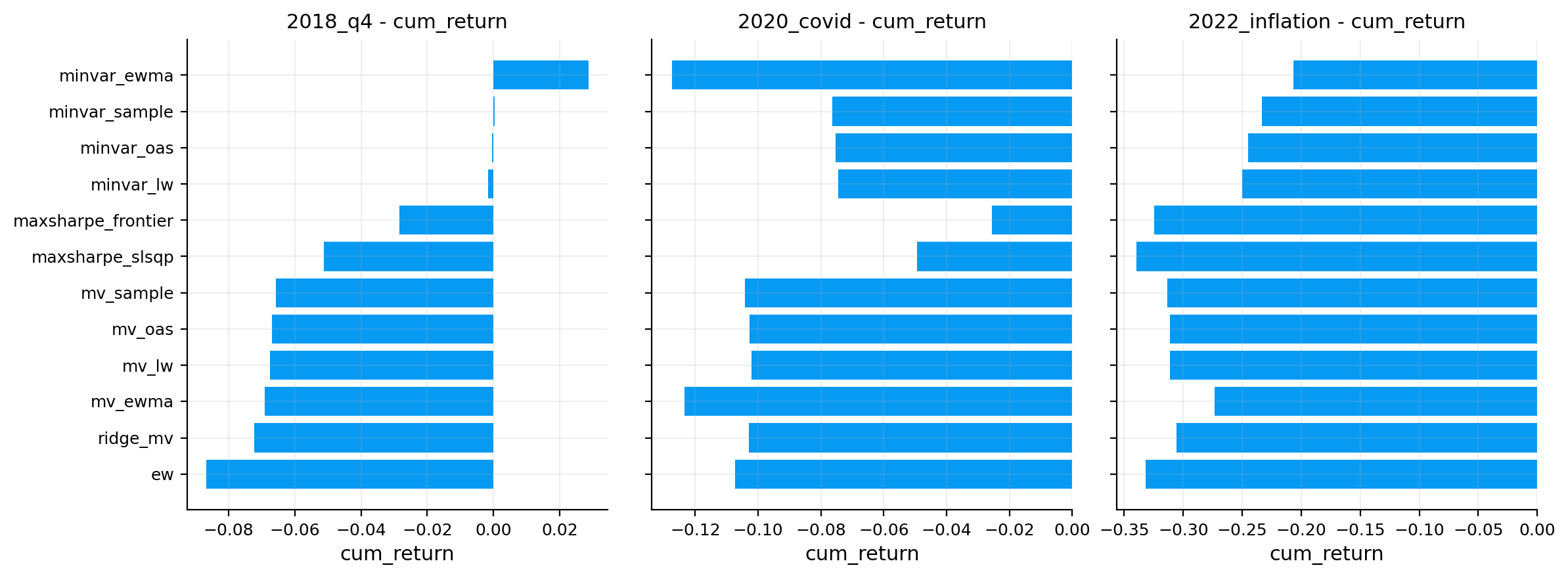

stress_windows = {

"2018_q4": ("2018-10-01", "2018-12-31"),

"2020_covid": ("2020-02-20", "2020-04-30"),

"2022_inflation": ("2022-01-03", "2022-10-31")}

stress_tbl = stress.stress_table(objects, windows=stress_windows, worst_only=True)

stress_tbl_full = stress.stress_table(objects, windows=stress_windows, worst_only=False)

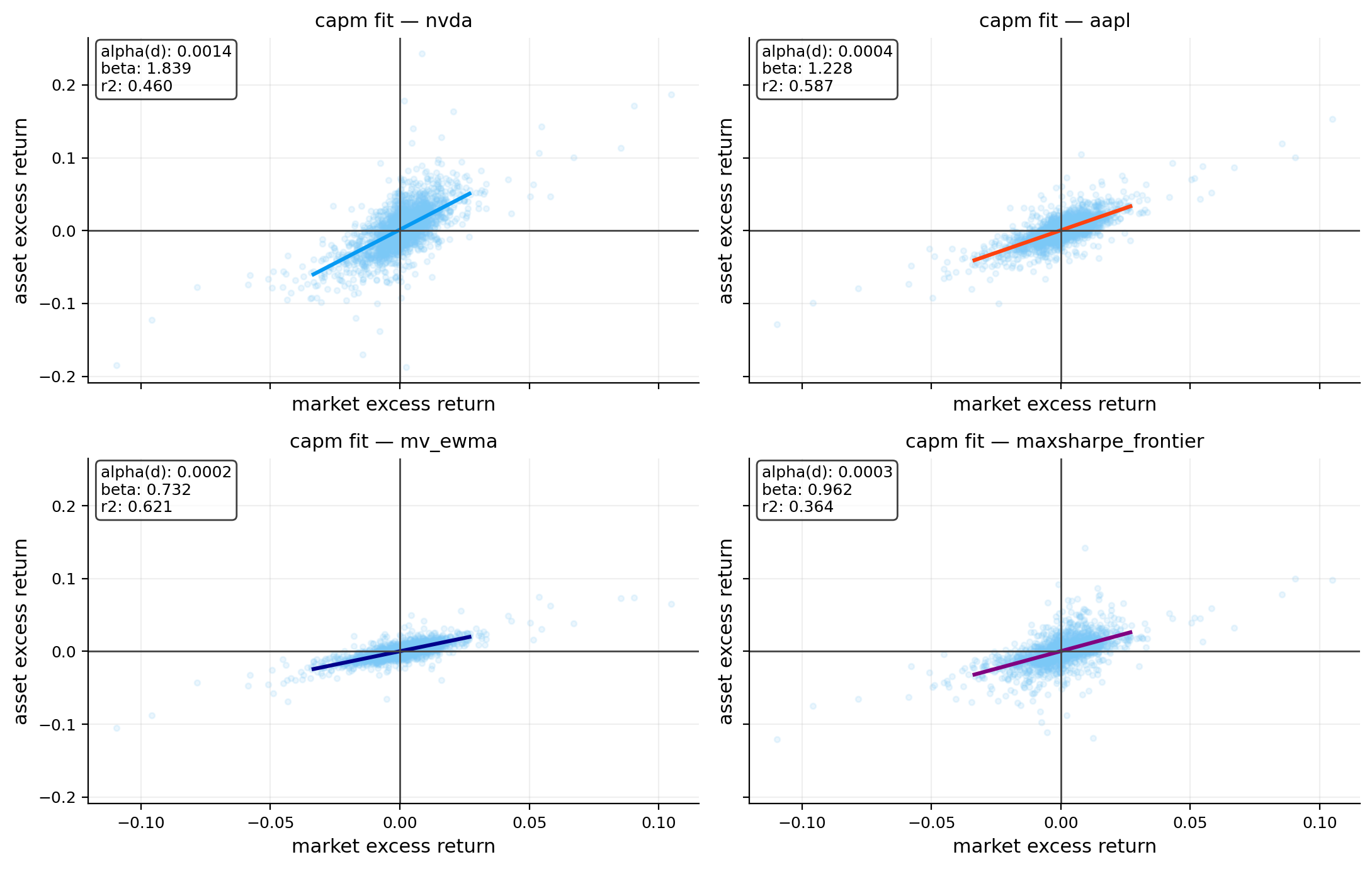

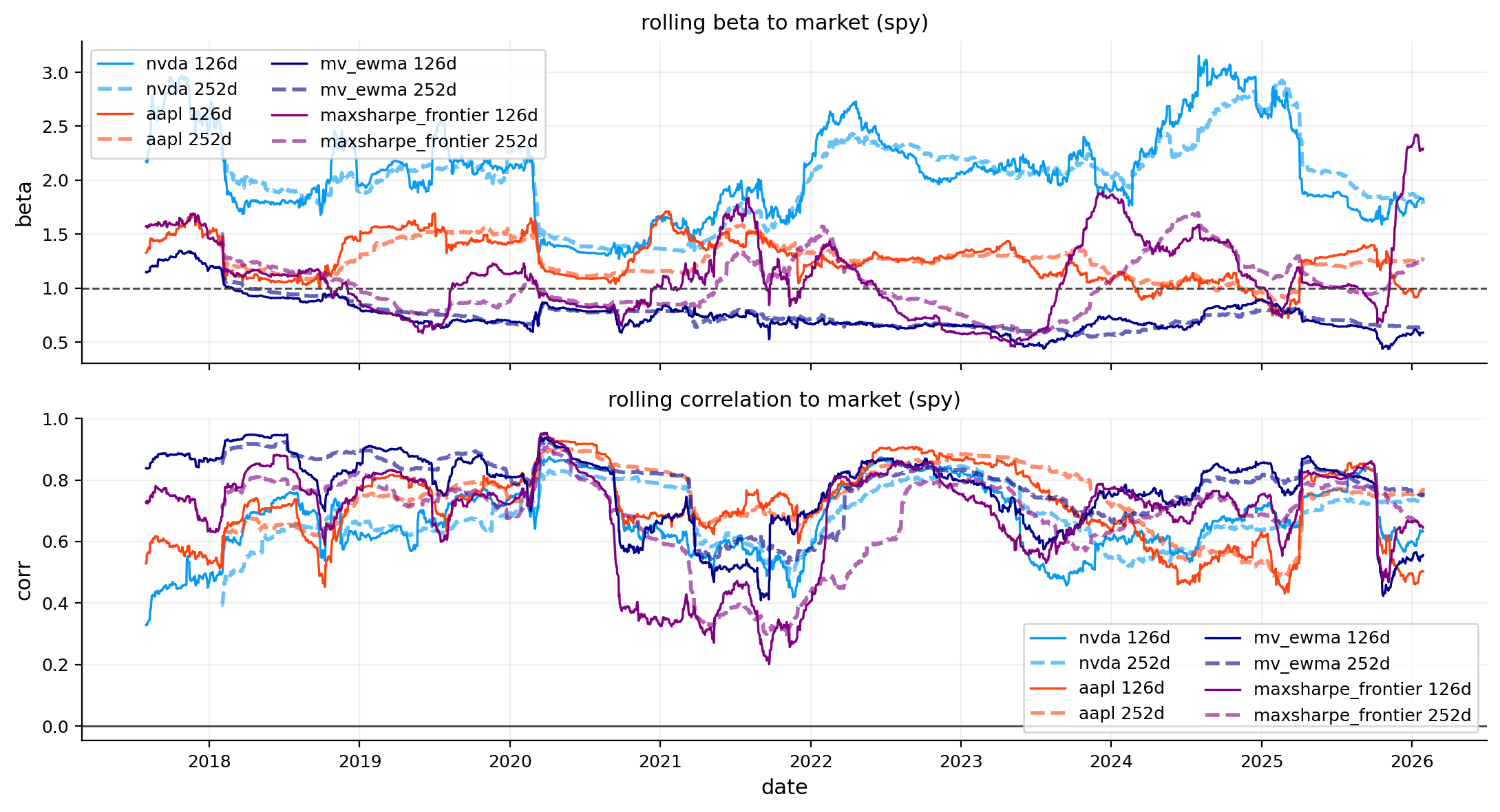

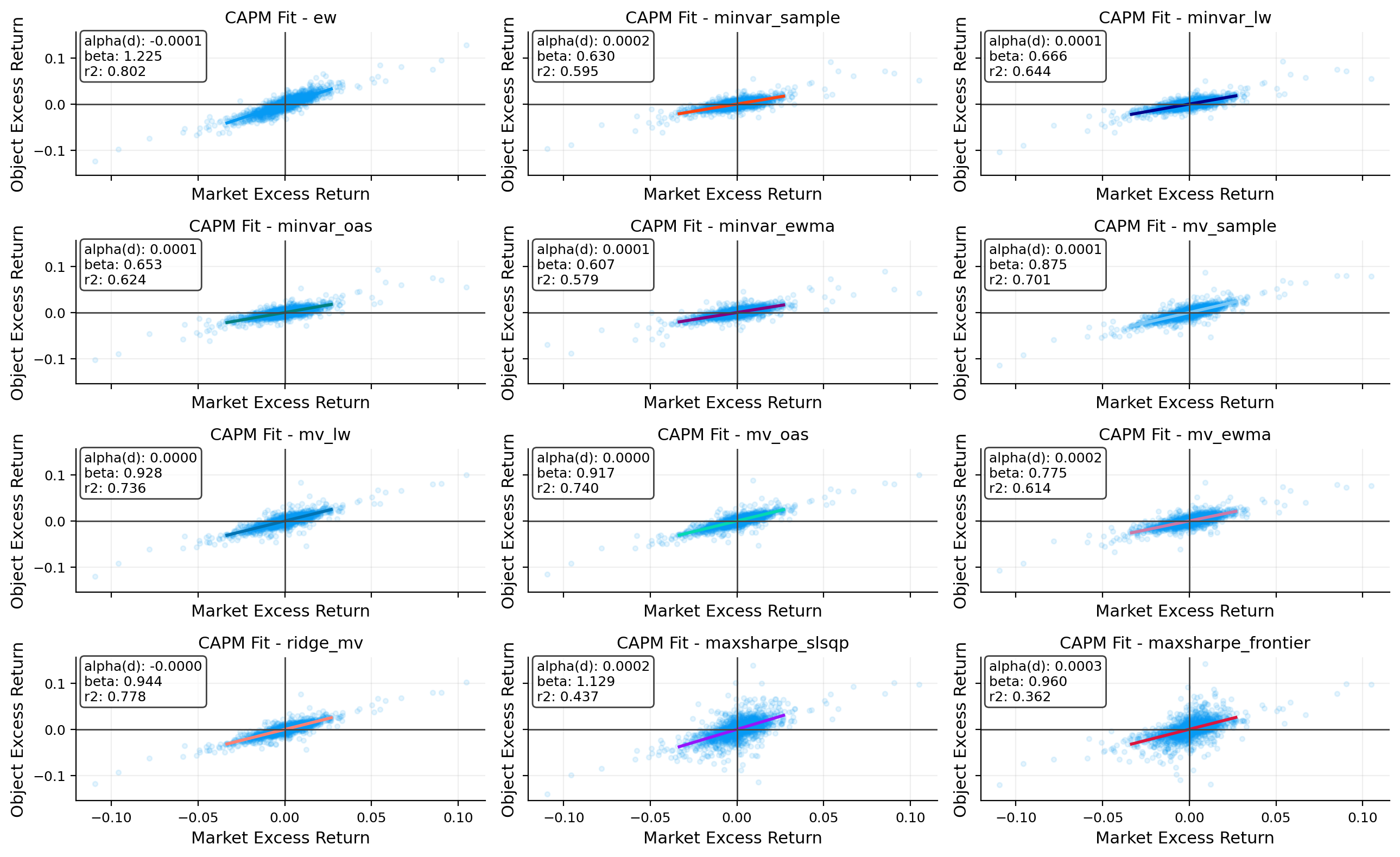

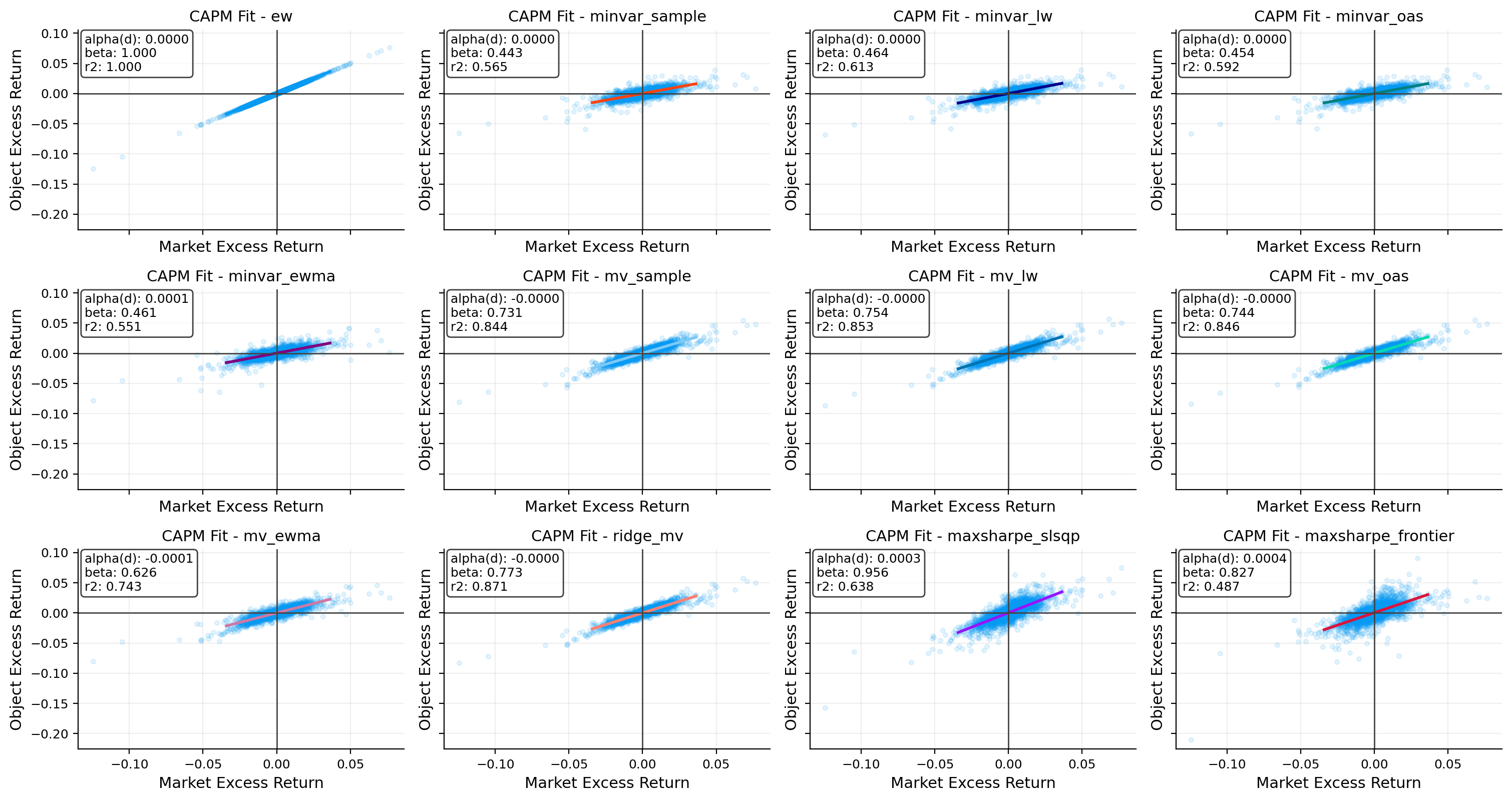

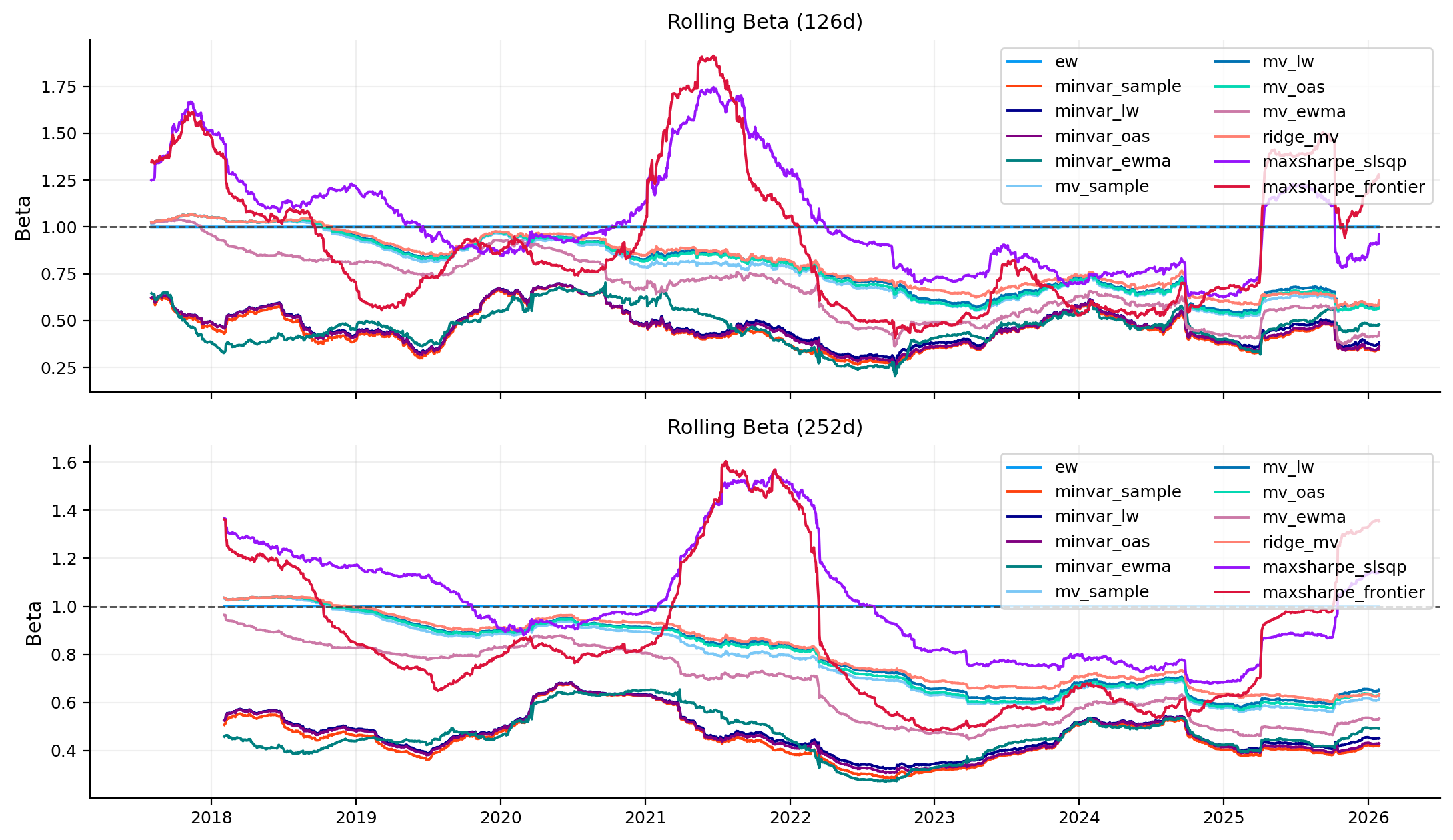

capm_tbl, capm_roll = capm.capm_table(objects, market_ret=market_ret, rf_daily=rf_daily, rolling=[126, 252])

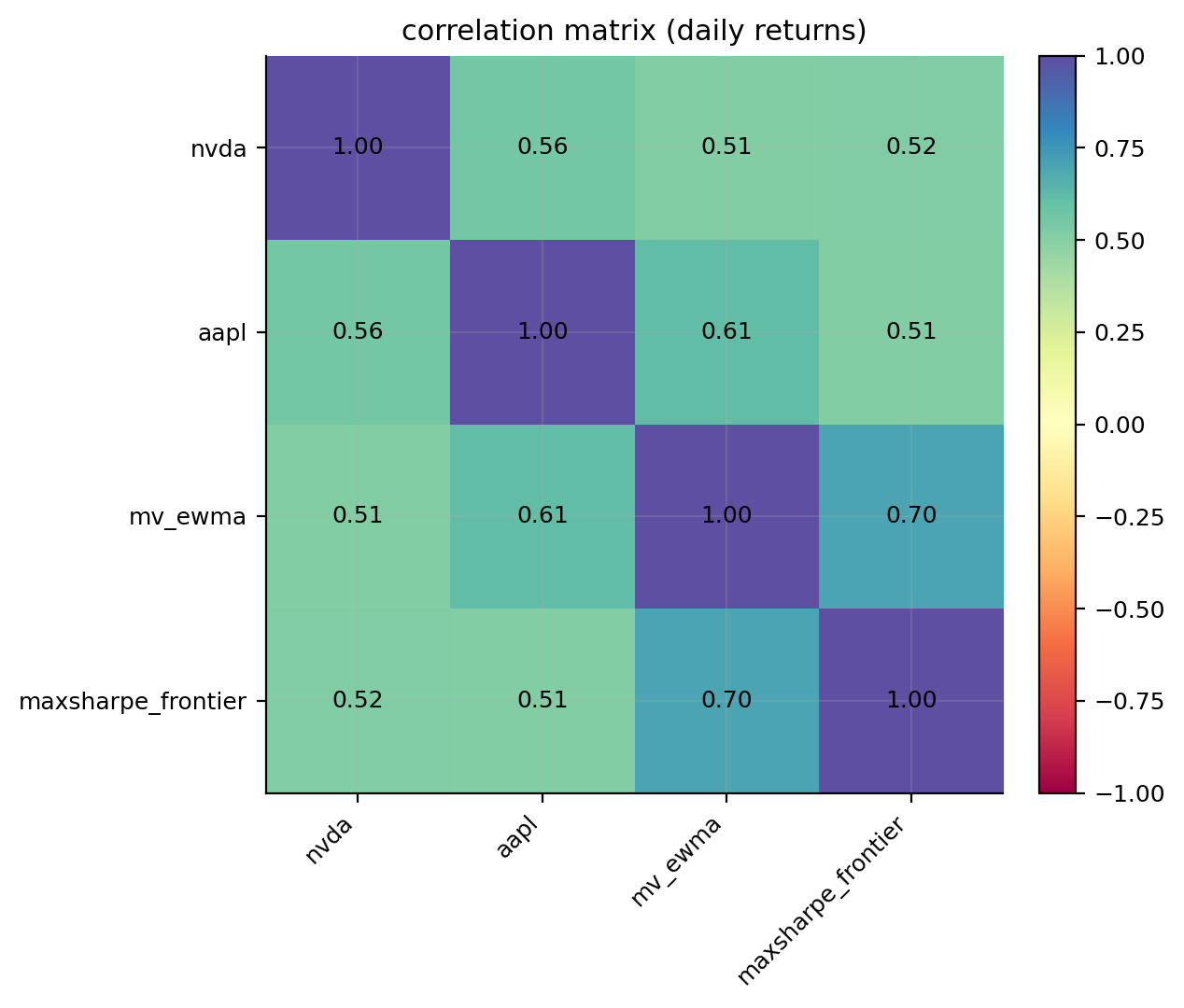

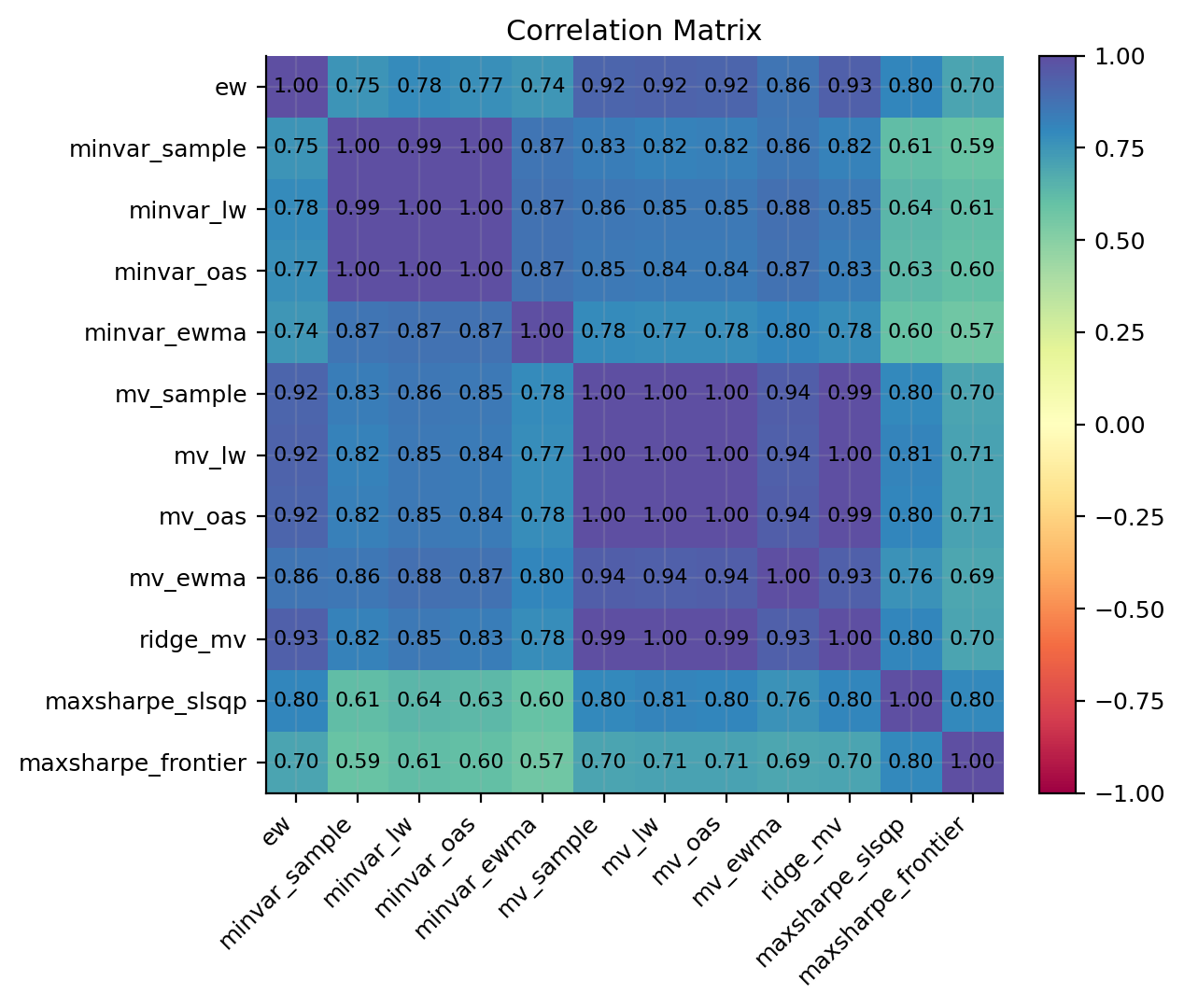

corr_tbl = correlation.corr_matrix(objects)

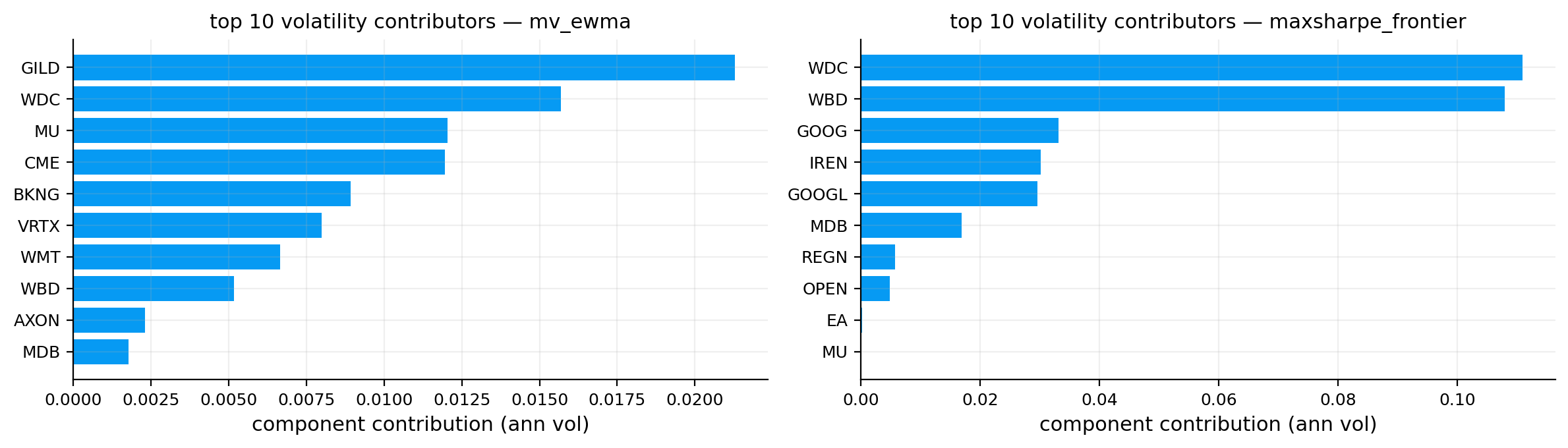

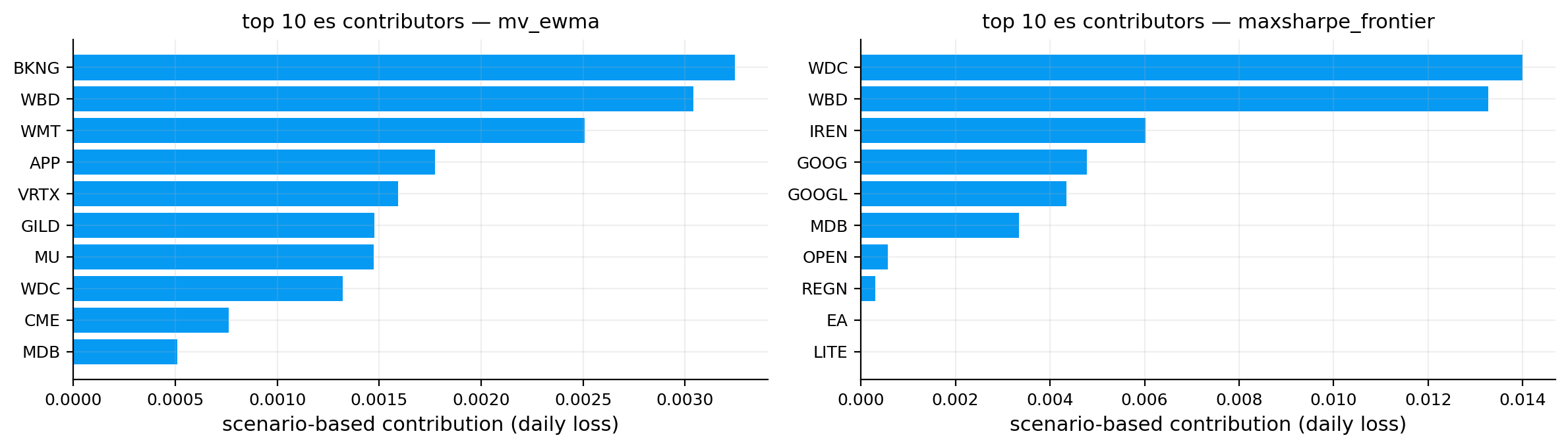

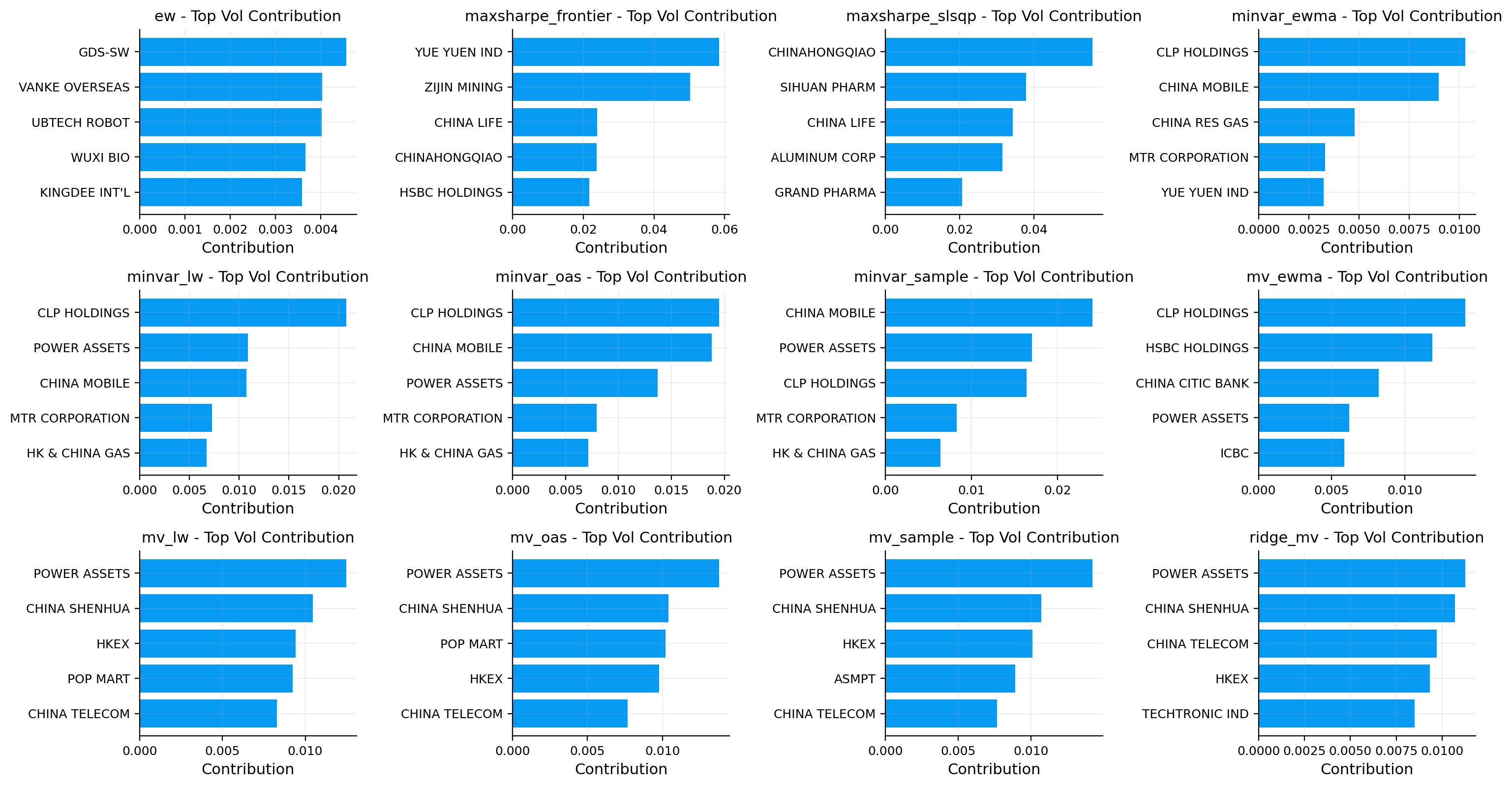

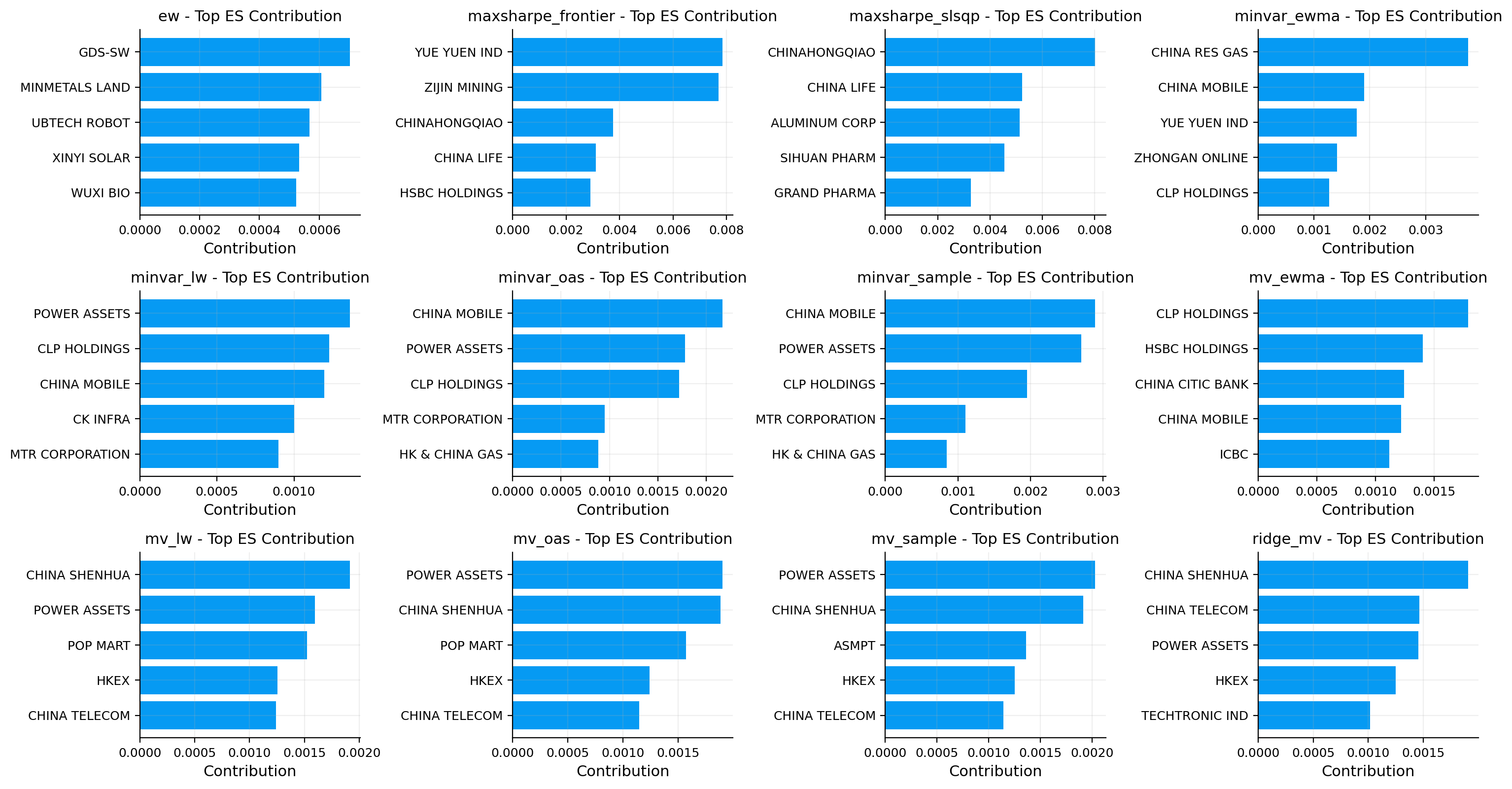

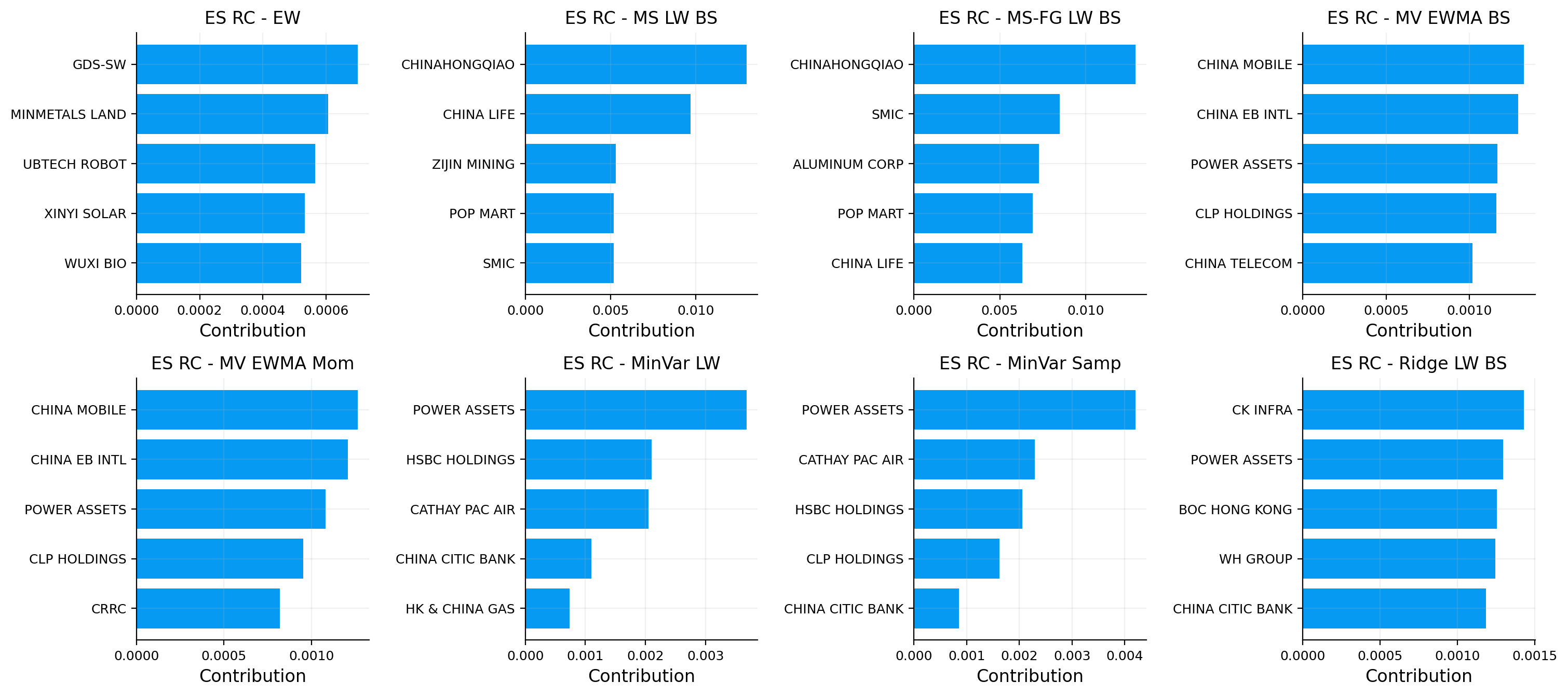

vol_rc_tbl, es_rc_tbl, overlap_tbl = contributions.attribution_tables(portfolios, es_alpha=0.05, top_k=10)

display(perf_tbl.round(4))

display(shape_tbl.round(4))

display(dd_summary_tbl.round(4))

display(dd_episodes_tbl.round(4))

display(var_es_tbl.round(4))

display(var_bt_tbl.round(4))

display(stress_tbl.round(4))

display(capm_tbl.round(4))

display(overlap_tbl)

fig, axes = plt.subplots(4, 2, figsize=(18, 20), constrained_layout=True)

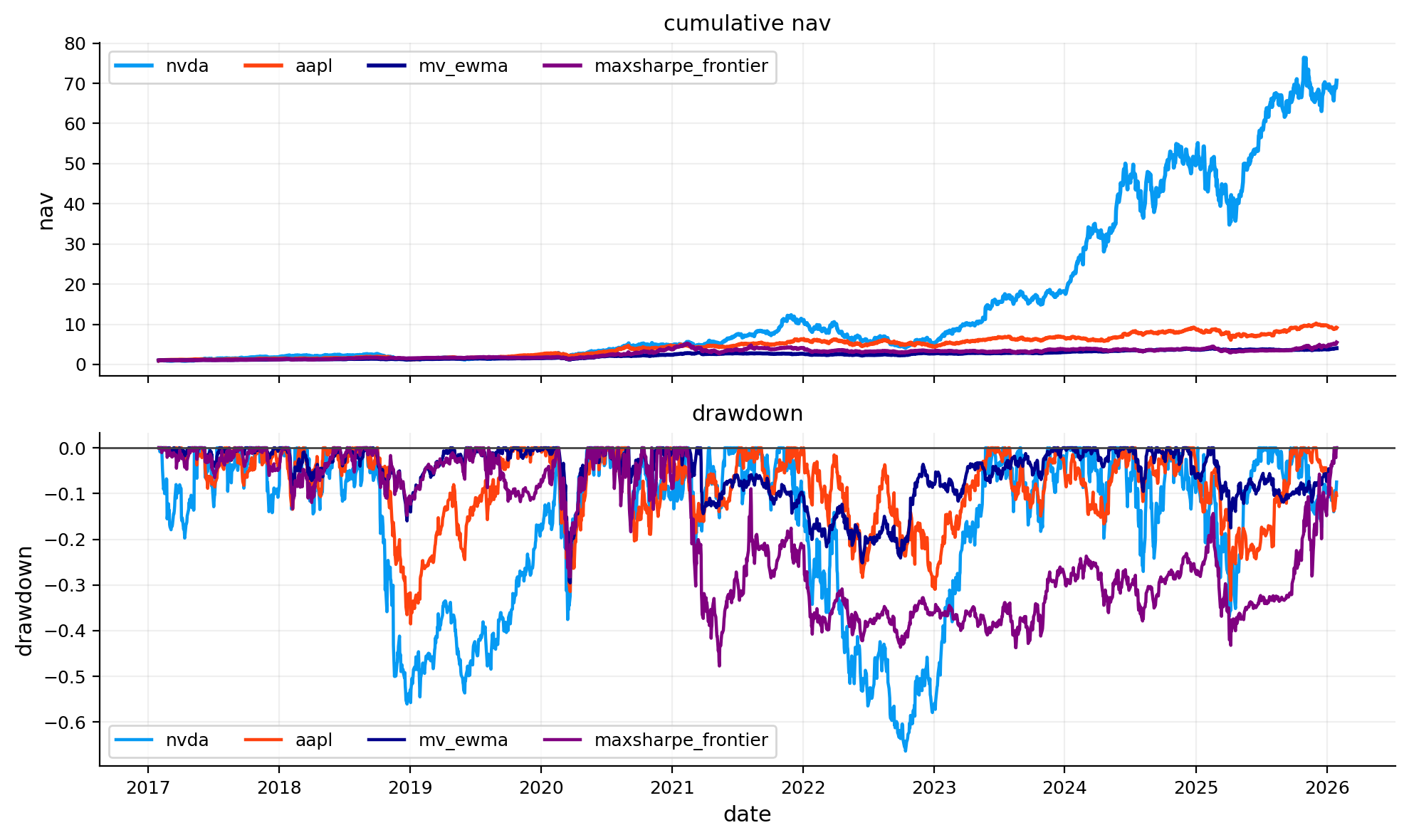

risk_plots.plot_nav_compare(ax=axes[0, 0], objects=objects, title="Cumulative NAV - US finalists")

risk_plots.plot_drawdown_compare_objects(ax=axes[0, 1], objects=objects, title="Drawdowns - US finalists")

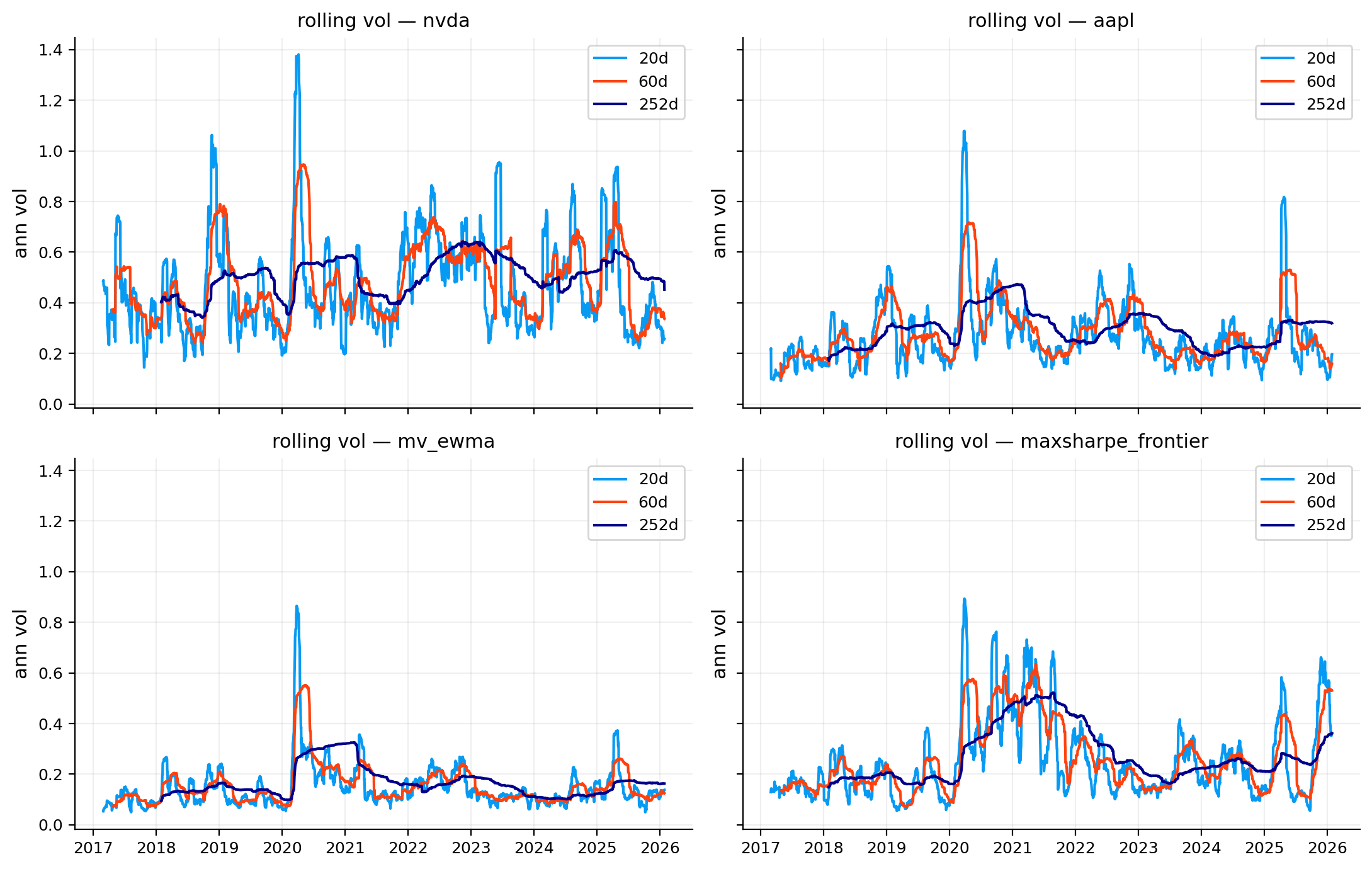

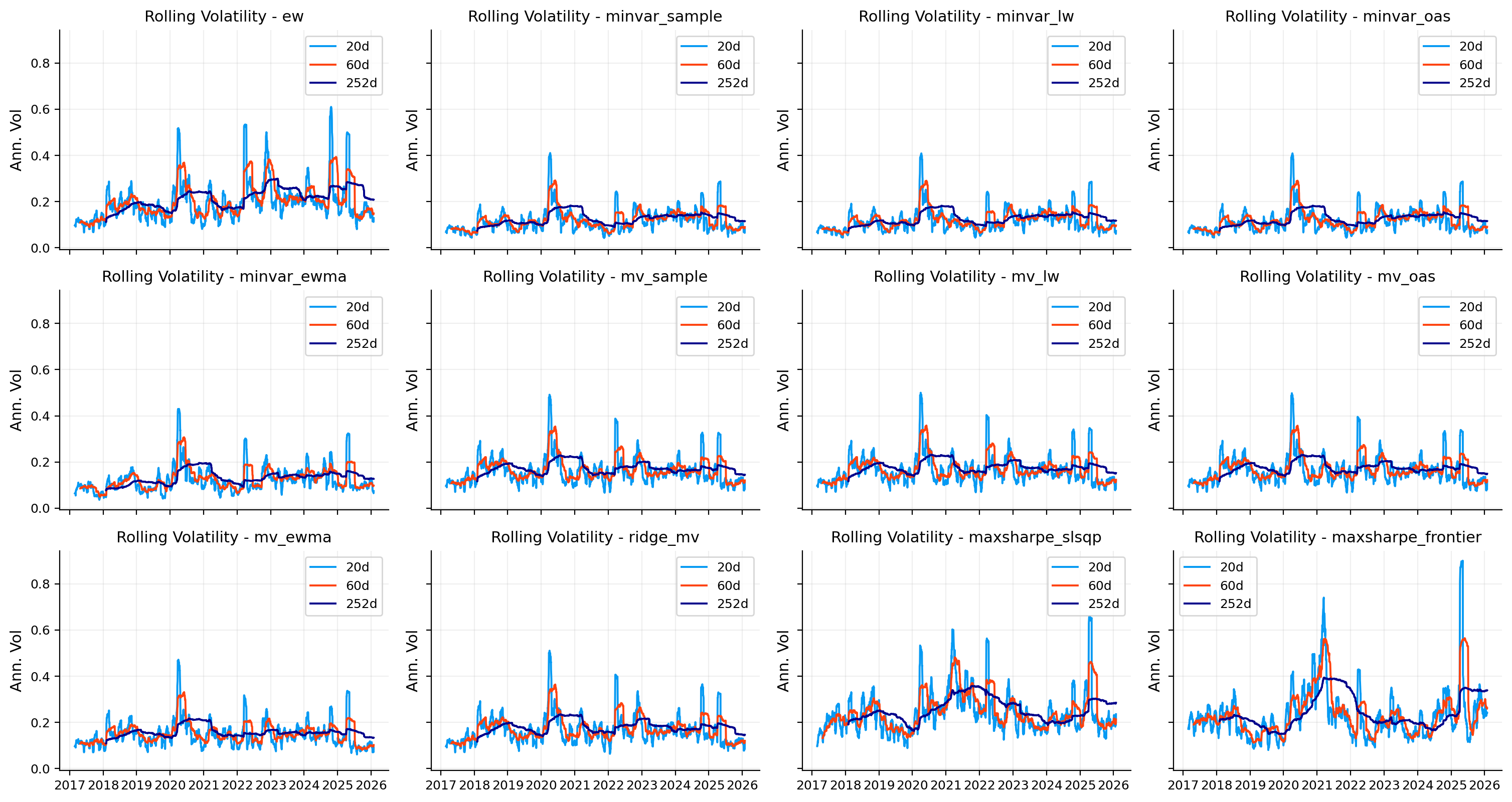

risk_plots.plot_rolling_volatility(ax=axes[1, 0], objects=objects, windows=[20, 60, 252], annualization=252, title="Rolling volatility")

risk_plots.plot_var_backtest_summary(ax=axes[1, 1], var_backtest_table=var_bt_tbl, title="VaR backtest accuracy")

risk_plots.plot_stress_heatmap(ax=axes[2, 0], stress_table=stress_tbl_full, title="Historical stress windows")

risk_plots.plot_rolling_beta(ax=axes[2, 1], rolling_beta=capm_roll, title="Rolling CAPM beta")

risk_plots.plot_corr_heatmap(ax=axes[3, 0], corr=corr_tbl, title="Correlation matrix")

risk_plots.plot_contribution_bars(ax=axes[3, 1], contribution_table=vol_rc_tbl, top_k=10, title="Top volatility contributors")

plt.show()

print("US finalists in risk analysis:", us_finalists)