build hedge relationships where one target asset is explained by one hedge or a basket of hedges,

estimate static, rolling, ridge, and Kalman-filter hedge ratios,

evaluate hedged books using volatility reduction, expected shortfall reduction, drawdown change, beta reduction, turnover, and cost drag,

test residual spreads with ADF, Engle-Granger, half-life, z-score rules, and trading gates,

transfer the same workflow to international ETFs, where currency, country beta, commodities, dollar pressure, and regional equity structure create much richer economic interpretations.

Dynamic hedging as a moving economic relationship

The main object in this project is the hedge ratio. A hedge ratio answers a very practical question: if we hold one asset, how much of another asset, or how much of a hedge basket, do we need to short to remove the part of the risk we don’t want?

In the simplest one-hedge case, the statistical model is:

\[

y_t = \alpha + \beta x_t + \varepsilon_t

\]

where:

\(y_t\) is the target return at time \(t\),

\(x_t\) is the hedge return at time \(t\),

\(\alpha\) is the average return that isn’t explained by the hedge,

\(\beta\) is the hedge ratio,

\(\varepsilon_t\) is the residual, meaning the part of the target move that the hedge didn’t explain.

If \(\beta = 1.2\), the interpretation is direct: a 1% move in the hedge asset is associated with about a 1.2% move in the target. A hedged book then holds the target and shorts \(1.2\) units of the hedge:

\[

r^{hedged}_t = y_t - \beta x_t

\]

That residual return is important. In pure hedging, we want \(r^{hedged}_t\) to be less volatile than \(y_t\). In residual trading, we ask for something stronger: we want the residual to behave like a mean-reverting spread. This is why the project naturally splits into two layers.

The first layer is risk reduction:

Can we remove the target’s systematic exposure without creating too much turnover?

The second layer is econometric trading:

After hedging, does the leftover spread mean-revert enough to trade?

Those two questions aren’t the same. A hedge can be excellent for risk reduction and still useless as a trading signal. A relationship can have high correlation and still fail a stationarity test. This project is useful because it keeps those ideas separate instead of pretending every hedgeable relationship is automatically a tradable pair.

1) Setup and project constants

We start by loading the risk, return, plotting, data, and hedging tools used throughout the project. The important part isn’t the import list. The important part is the workflow we prepare:

Return construction, because hedge ratios are estimated on return series in the first half of the project.

Regression estimation, because the hedge ratio is a regression coefficient.

Risk reporting, because a hedge ratio isn’t useful unless it lowers volatility, tail risk, or unwanted beta.

Trading simulation, because changing the hedge ratio creates turnover and costs.

Residual testing, because a spread must pass econometric tests before we treat it as tradable.

The constants also define the research design. We use daily data from 2015 to 2026, but most decisions require a warm-up history:

We use weekly rebalancing on Fridays. That matters because hedge ratios estimated every day can be too noisy to trade directly. Weekly rebalancing is a compromise between responsiveness and implementation realism.

The no-trade band is:

\[

b = 0.05

\]

So if the desired hedge ratio changes by less than 5 percentage points, we don’t update the traded hedge. This small detail becomes important later: it turns a smooth statistical beta path into a more realistic trading path.

The constants create a clean out-of-sample setup. We don’t estimate a hedge ratio on the full sample and then pretend it was available historically. We require an initial two-year training window, then we let the hedge evolve using only information available up to each date.

where turnover is the absolute change in hedge weights. If a strategy improves volatility but needs constant rebalancing, this cost line will reveal it. This is why the project evaluates both statistical quality and trading quality. A hedge ratio can look perfect in a regression and still be a weak trading object if it changes too often.

1.1 Hedge ratio as a minimum-variance problem

The regression coefficient has a trading meaning. In the one-hedge case, we can derive the optimal hedge ratio by minimizing the variance of the residual book:

This is the same slope coefficient we get from OLS when there’s one hedge variable. So OLS isn’t just a statistical convenience. It’s directly estimating the hedge ratio that minimizes residual variance inside the sample.

where \(\Sigma_{xx}\) is the covariance matrix of hedge returns and \(\boldsymbol{\sigma}_{xy}\) is the vector of covariances between each hedge and the target. This formula also shows why multicollinearity matters. If hedge assets are highly correlated, \(\Sigma_{xx}\) becomes harder to invert, and the estimated beta vector can become unstable.

1.2 What a good hedge ratio is allowed to do

A good hedge ratio doesn’t need to make the residual return positive. That’s a separate alpha question. In the hedge-ratio part of the project, we mainly want the residual to have less unwanted systematic risk than the target.

The cleanest hedge outcome looks like this:

\[

\text{Vol}(r^{hedged}) < \text{Vol}(y)

\]

\[

ES_{5\%}(r^{hedged}) \text{ is less negative than } ES_{5\%}(y)

\]

\[

|\beta(r^{hedged}, x)| < |\beta(y,x)|

\]

But there’s no guarantee that all three improve together. A hedge can reduce volatility while increasing drawdown if the hedge fails during the wrong regime. A hedge can reduce beta while leaving a large idiosyncratic tail. A hedge can look great before costs and weak after costs.

This is why the project doesn’t rank models only by \(R^2\) or residual variance. We use a broader set of trading diagnostics because the hedge is meant to be implemented, not just estimated.

2) Data construction

We combine ETF panels and stock panels from the repository’s data reproducibility layer. The code reads already-generated local files from the ../data/ directory, but in the public repository those files are reproduced through source folders, not by linking directly to final CSV/parquet files.

For reproduction, check these folders inside the data directory:

Each folder contains the reproducibility material for that data source, usually a README plus a download/build script. So the correct way to describe the data isn’t “open this exact CSV on GitHub.” The correct description is: the local notebook reads generated files, and the repo data folders explain how to regenerate those files.

The first application mixes ETFs and single stocks. That gives us three different hedge problems:

Relationship type

Example

What the hedge is trying to remove

Close ETF proxy

QQQ vs SPY, TLT vs IEF, AGG vs BND

broad common exposure such as equity beta, duration, or aggregate bond risk

Macro/factor proxy

HYG vs LQD/TLT/SPY, GDX vs GLD/SPY

credit, rates, equity beta, gold, and commodity-linked risk

Stock versus sector/factor basket

NVDA vs SMH/QQQ, AMZN vs XLY/QQQ

market, sector, and style exposure so the residual is closer to stock-specific behavior

We build both log returns and simple returns:

\[

r^{log}_t = \log(P_t) - \log(P_{t-1})

\]

\[

r^{simple}_t = \frac{P_t}{P_{t-1}} - 1

\]

Here \(P_t\) is the adjusted close price at time \(t\). Log returns are convenient for regression and statistical testing because they add cleanly across time. Simple returns are more natural for portfolio simulation because the hedged book’s profit and loss is calculated from actual percentage returns.

So the workflow isn’t random: we estimate relationships in a statistically cleaner return space, then evaluate the hedge in the same return space an investor would actually experience.

etf close panel: (2766, 32)

stock close panel: (2766, 4382)

combined price panel from 2015-01-01 to 2026-01-01: (2766, 4414)

The loaded panels are large enough for a serious test: 2766 daily ETF observations, 4382 stock columns, and 4414 combined price columns from 2015 to the start of 2026. The important point is that we aren’t building this only on a few carefully selected pairs. We have enough stock and ETF history to test both clean ETF relationships and messier single-name relationships.

The 2015 start date also gives the sample several very different regimes:

the low-rate expansion before 2020,

the COVID crash and recovery,

the inflation/rate shock of 2022,

the AI and mega-cap growth rebound after 2023.

A static hedge ratio that works across all of these regimes is impressive, but unlikely for many relationships. This is exactly why we compare static, rolling, ridge, and Kalman versions instead of trusting one regression estimate.

2.1 Why this universe is useful for econometrics

This universe is better than a random set of tickers because many relationships have a real structural reason to exist. Econometric tests are much more meaningful when the pair or hedge basket has economic content.

For example, AGG and BND are both broad US aggregate bond ETFs. If their residual fails stationarity tests, that would tell us something is wrong with the method or data. QQQ and SPY are both equity beta, but QQQ has more growth and technology exposure, so the residual should be a real growth tilt, not pure noise. TLT and IEF are both Treasury duration exposure, so the beta should mostly reflect duration scaling. HYG and LQD are both corporate credit, but HYG has more default and equity-cycle sensitivity.

For single stocks, the logic is weaker but still useful. Hedging NVDA with SMH and QQQ removes broad semiconductor and Nasdaq growth exposure. The remaining residual is closer to NVDA-specific information. It still won’t be pure alpha, but it’s less contaminated by market and sector factors.

So the data design supports both econometric learning and financial interpretation. We aren’t only asking whether a regression has a high \(R^2\). We’re asking whether the residual makes economic sense after the hedge is applied.

3) Target and hedge relationships

We define each hedge problem as a relationship with one target and one or more hedge assets. In a one-hedge case, the model is:

The lag on \(\beta_{t-1}\) is critical. It means we trade using yesterday’s available hedge ratio, not today’s hindsight hedge ratio.

The relationships are economically different:

QQQ versus SPY measures growth-heavy Nasdaq exposure relative to broad US equity beta.

TLT versus IEF measures long-duration exposure relative to intermediate-duration Treasuries.

AGG versus BND is almost a replication problem between two broad aggregate bond ETFs.

HYG versus LQD/TLT/SPY tries to isolate high-yield credit after investment-grade credit, rates, and equity beta.

GDX versus GLD/SPY separates gold miners from gold price and equity market components.

Single-stock relationships hedge mega-cap or high-beta stocks with sector ETFs and QQQ, trying to remove market/sector beta and leave idiosyncratic residual behavior.

Show code

@dataclass(frozen=True)class rel: name: str target: str hedges: list[str] pair: tuple[str, str] |None=Nonedef __post_init__(self):object.__setattr__(self, "name", self.name.lower())object.__setattr__(self, "target", self.target.lower())object.__setattr__(self, "hedges", [h.lower() for h inself.hedges])ifself.pair isnotNone:object.__setattr__(self, "pair", tuple(x.lower() for x inself.pair))@propertydef assets(self):return [self.target, *self.hedges]@propertydef hedge_label(self):return"+".join(self.hedges)def rel_tickers(rels): out = []for r in rels:for t in r.assets:if t notin out: out.append(t)return outdef filter_rels(rels, columns): available =set(map(str.lower, columns)) kept, missing = [], {}for r in rels: miss = [t for t in r.assets if t notin available]if miss: missing[r.name] = misselse: kept.append(r)return kept, missingdef rel_table(rels, columns): available =set(map(str.lower, columns)) rows = []for r in rels: rows.append({"relationship": r.name, "target": r.target, "hedges": ", ".join(r.hedges),"residual_pair": ""if r.pair isNoneelse" / ".join(r.pair),"included": all(t in available for t in r.assets)})return pd.DataFrame(rows)

All relationships are available with no missing tickers. That matters because a missing hedge asset would break the interpretation of the target residual. If NVDA is hedged with SMH and QQQ, we need both the semiconductor ETF and Nasdaq growth factor to exist over the whole sample. If one hedge disappears halfway through, the residual would change definition through time.

The list also makes clear that we aren’t using the same hedge logic for every target. Some relationships are near-replication pairs, like AGG and BND. Others are only partial explanatory models, like TSLA versus XLY and QQQ. We should expect the same hedge estimator to behave differently across these cases.

4) Coverage and first diagnostics

Before estimating hedge ratios, we inspect basic coverage and relationship quality. For each target and hedge proxy, we calculate:

\[

\sigma_y = \sqrt{252}\,\text{std}(y_t)

\]

\[

\sigma_x = \sqrt{252}\,\text{std}(x_t)

\]

\[

\rho_{yx} = \text{corr}(y_t, x_t)

\]

For a one-factor regression, the coefficient of determination is:

A high \(R^2\) means the hedge proxy explains a large share of the target’s return variance. A low \(R^2\) means the target has a large residual component, so hedging will be incomplete.

We also compute a rolling beta interquartile range:

This is a compact way to measure beta instability. A high correlation with a high beta IQR means the relationship is real, but the hedge ratio changes a lot over time. That’s exactly where dynamic hedge models can add value.

Show code

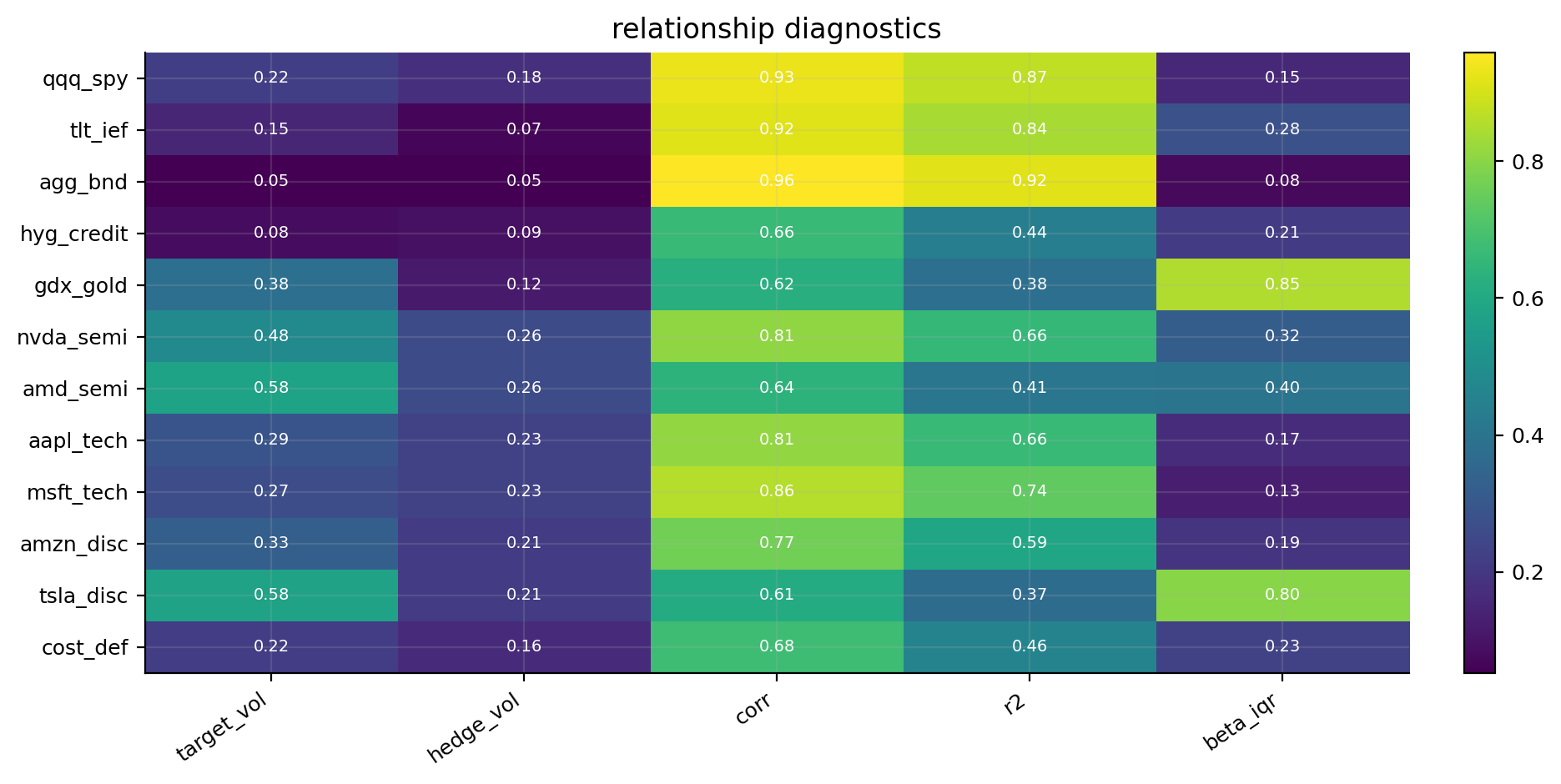

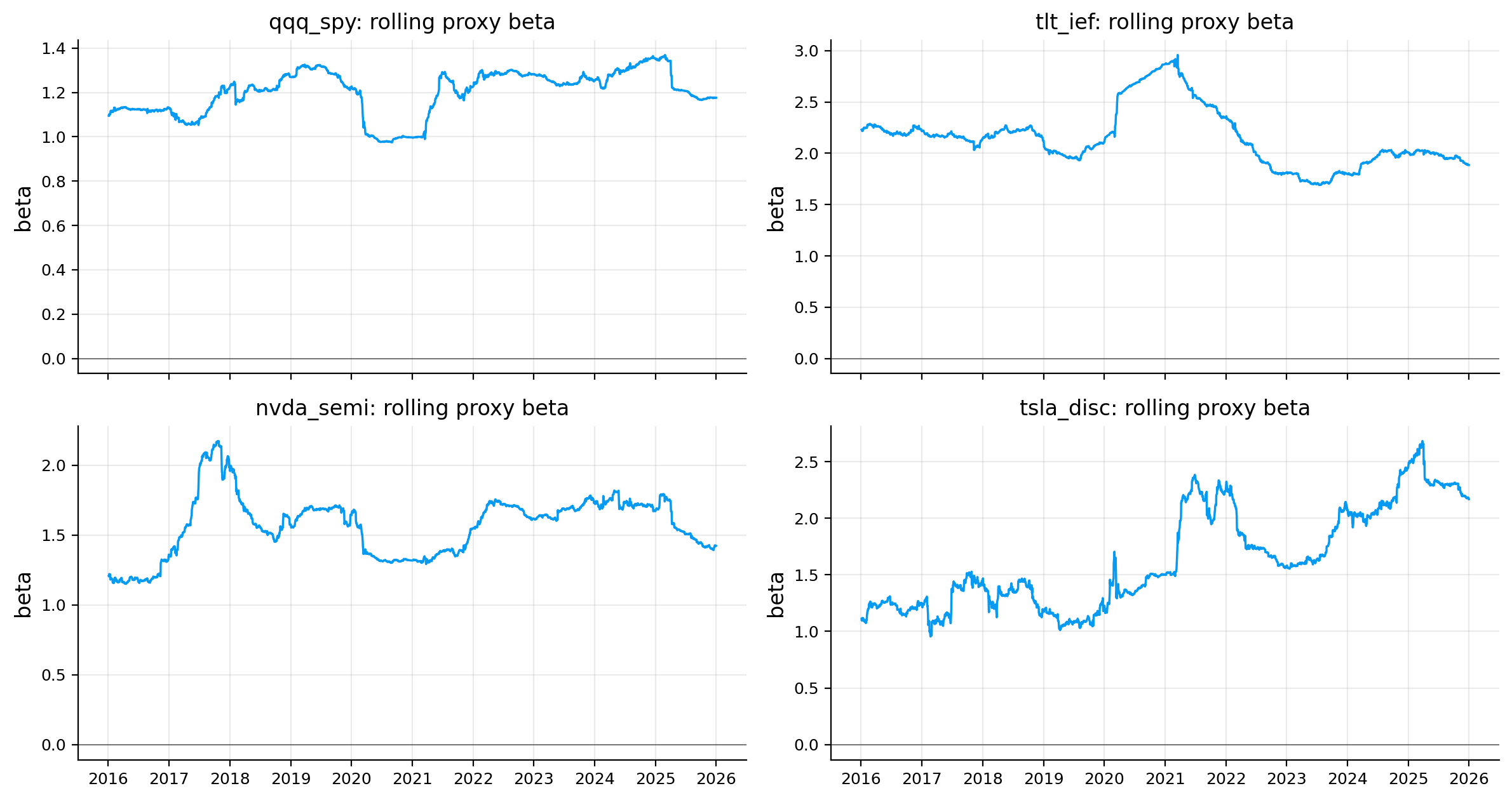

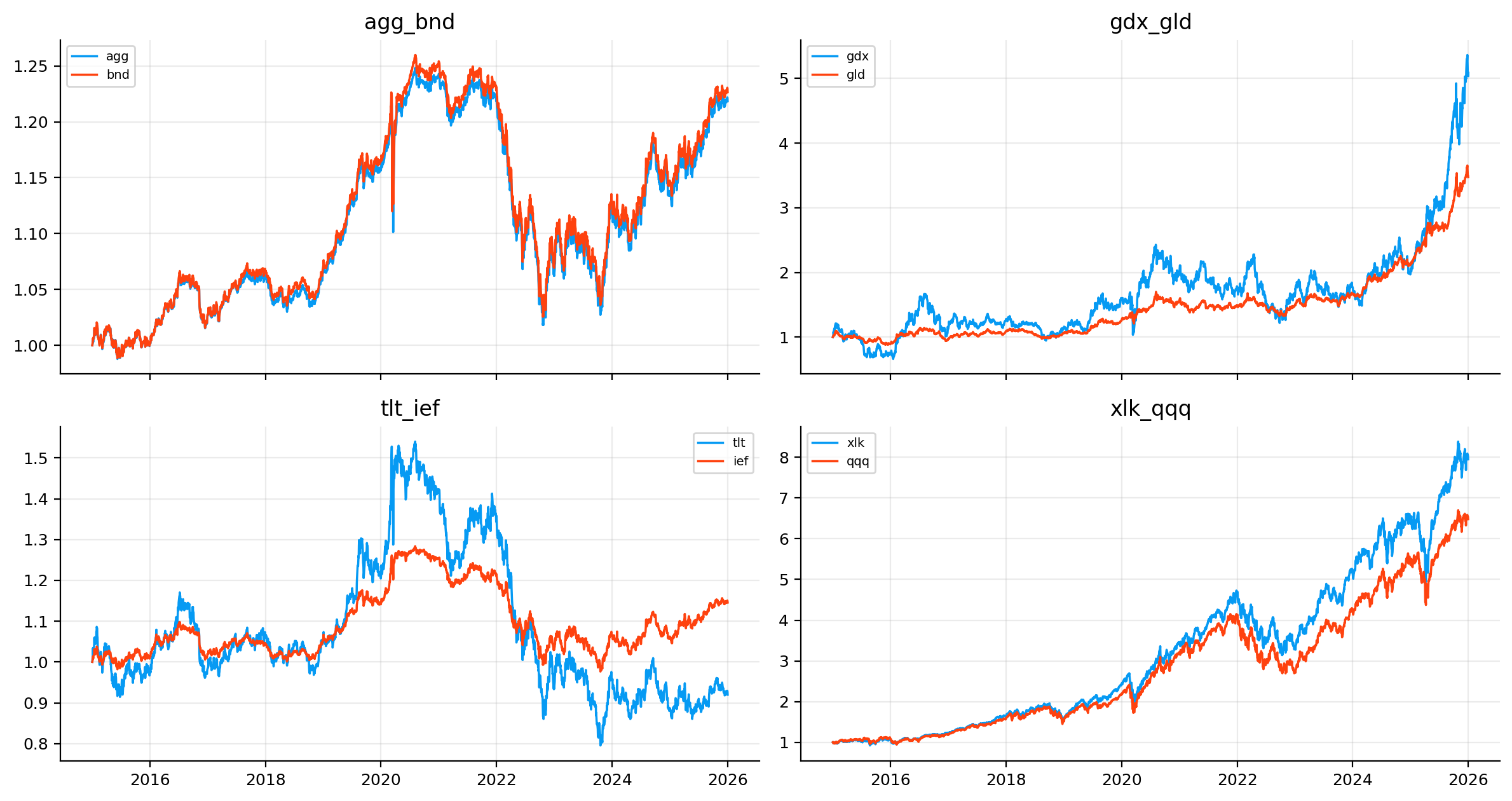

def hedge_proxy_ret(ret, r):return ret[r.hedges].mean(axis=1).rename(f"{r.name}_proxy")def coverage_table(frame, rels): rows = []for r in rels: sub = frame[r.assets] valid = sub.dropna(how="any") rows.append({"relationship": r.name, "target": r.target, "hedges": ", ".join(r.hedges),"start": valid.index.min() iflen(valid) else pd.NaT,"end": valid.index.max() iflen(valid) else pd.NaT,"obs": len(valid), "missing_pct": sub.isna().mean().mean(), "included": len(valid) >0})return pd.DataFrame(rows)def diag_table(ret, rels): rows = []for r in rels: y = ret[r.target] proxy = hedge_proxy_ret(ret, r) z = pd.concat([y, proxy], axis=1).dropna() z.columns = ["target", "proxy"] _, _, r2 = capm_ols(z["target"], z["proxy"]) b = rolling_beta(z["target"], z["proxy"], window=min(win, max(len(z) //2, 20))) rows.append({"relationship": r.name, "target_vol": z["target"].std() * np.sqrt(ann),"hedge_vol": z["proxy"].std() * np.sqrt(ann), "corr": z["target"].corr(z["proxy"]),"r2": r2, "beta_iqr": b.quantile(0.75) - b.quantile(0.25), "obs": len(z)})return pd.DataFrame(rows)tab_cov = coverage_table(px_main, rel_main)tab_diag = diag_table(ret_m_main, rel_main)display(tab_cov.round(4))display(tab_diag.round(4))fig, ax = plt.subplots(figsize=(9.5, 4.8))diag_cols = ["target_vol", "hedge_vol", "corr", "r2", "beta_iqr"]mat = tab_diag.set_index("relationship")[diag_cols]vals = mat.to_numpy(dtype=float)im = ax.imshow(vals, aspect="auto", cmap="viridis")ax.set_xticks(range(mat.shape[1]), mat.columns, rotation=35, ha="right")ax.set_yticks(range(mat.shape[0]), mat.index)ax.set_title("relationship diagnostics")for i inrange(mat.shape[0]):for j inrange(mat.shape[1]):if np.isfinite(vals[i, j]): ax.text(j, i, f"{vals[i, j]:.2f}", ha="center", va="center", fontsize=7, color="white")fig.colorbar(im, ax=ax, fraction=0.046, pad=0.04)plt.tight_layout()plt.show()fig, axes = plt.subplots(2, 2, figsize=(12, 6.4), sharex=True)for ax, name inzip(axes.ravel(), ["qqq_spy", "tlt_ief", "nvda_semi", "tsla_disc"]): r =next((x for x in rel_main if x.name == name), None)if r isNone: ax.axis("off")continue b = rolling_beta(ret_m_main[r.target], hedge_proxy_ret(ret_m_main, r), window=win).dropna() ax.plot(b.index, b.values, lw=1.25) ax.axhline(0, color="black", lw=0.7, alpha=0.5) ax.set_title(f"{name}: rolling proxy beta") ax.set_ylabel("beta") ax.grid(True, alpha=0.25)plt.tight_layout()plt.show()price_examples = [("agg_bnd", "agg", "bnd"), ("gdx_gld", "gdx", "gld"), ("tlt_ief", "tlt", "ief"), ("xlk_qqq", "xlk", "qqq")]price_examples = [(name, a, b) for name, a, b in price_examples if a in px.columns and b in px.columns]fig, axes = plt.subplots(2, 2, figsize=(12, 6.4), sharex=True)for ax, item inzip(axes.ravel(), price_examples): name, a, b = item sub = px[[a, b]].dropna()iflen(sub): norm = sub / sub.iloc[0] ax.plot(norm.index, norm[a], lw=1.25, label=a, color=colors[0]) ax.plot(norm.index, norm[b], lw=1.25, label=b, color=colors[1]) ax.set_title(name) ax.legend(fontsize=7) ax.grid(True, alpha=0.25)for ax in axes.ravel()[len(price_examples):]: ax.axis("off")plt.tight_layout()plt.show()

relationship

target

hedges

start

end

obs

missing_pct

included

0

qqq_spy

qqq

spy

2015-01-02

2025-12-31

2766

0.0

True

1

tlt_ief

tlt

ief

2015-01-02

2025-12-31

2766

0.0

True

2

agg_bnd

agg

bnd

2015-01-02

2025-12-31

2766

0.0

True

3

hyg_credit

hyg

lqd, tlt, spy

2015-01-02

2025-12-31

2766

0.0

True

4

gdx_gold

gdx

gld, spy

2015-01-02

2025-12-31

2766

0.0

True

5

nvda_semi

nvda

smh, qqq

2015-01-02

2025-12-31

2766

0.0

True

6

amd_semi

amd

smh, qqq

2015-01-02

2025-12-31

2766

0.0

True

7

aapl_tech

aapl

xlk, qqq

2015-01-02

2025-12-31

2766

0.0

True

8

msft_tech

msft

xlk, qqq

2015-01-02

2025-12-31

2766

0.0

True

9

amzn_disc

amzn

xly, qqq

2015-01-02

2025-12-31

2766

0.0

True

10

tsla_disc

tsla

xly, qqq

2015-01-02

2025-12-31

2766

0.0

True

11

cost_def

cost

xlp, qqq

2015-01-02

2025-12-31

2766

0.0

True

relationship

target_vol

hedge_vol

corr

r2

beta_iqr

obs

0

qqq_spy

0.2201

0.1783

0.9338

0.8720

0.1542

2765

1

tlt_ief

0.1504

0.0663

0.9163

0.8396

0.2781

2765

2

agg_bnd

0.0526

0.0537

0.9591

0.9198

0.0771

2765

3

hyg_credit

0.0831

0.0928

0.6638

0.4406

0.2101

2765

4

gdx_gold

0.3822

0.1182

0.6194

0.3837

0.8500

2765

5

nvda_semi

0.4836

0.2585

0.8094

0.6551

0.3215

2765

6

amd_semi

0.5782

0.2585

0.6392

0.4086

0.4010

2765

7

aapl_tech

0.2881

0.2273

0.8134

0.6617

0.1668

2765

8

msft_tech

0.2686

0.2273

0.8596

0.7388

0.1301

2765

9

amzn_disc

0.3280

0.2117

0.7675

0.5891

0.1925

2765

10

tsla_disc

0.5759

0.2117

0.6094

0.3714

0.7989

2765

11

cost_def

0.2163

0.1629

0.6772

0.4586

0.2274

2765

From the coverage table we can see that every main relationship has the full sample from 2015-01-02 to 2025-12-31, with 2766 price observations and 0% missing values. So any later difference across models is coming from the estimation method, not from unequal data coverage.

The diagnostic table already separates the easy hedge problems from the hard ones:

AGG/BND has correlation around 0.959 and \(R^2\) around 0.920. This is the cleanest relationship in the main sample. It’s almost a replication hedge.

QQQ/SPY has correlation around 0.934 and \(R^2\) around 0.872. SPY explains most Nasdaq movement, but the residual still contains a growth/tech component.

TLT/IEF has correlation around 0.916 and \(R^2\) around 0.840. This is a duration hedge problem. The two ETFs move together, but TLT has much higher duration sensitivity.

GDX/GLD has only moderate correlation around 0.619 and \(R^2\) around 0.384, with a very large beta IQR around 0.850. Gold miners aren’t just leveraged gold. They also contain equity beta, mining margin risk, and company-level stress.

TSLA/XLY+QQQ and AMD/SMH+QQQ have low-to-moderate explanatory power relative to their target volatility. Those names have major idiosyncratic components.

The diagnostic heatmap makes this visible: bond pairs are bright in correlation and \(R^2\), while GDX and high-volatility stocks stand out with higher target volatility and less stable betas.

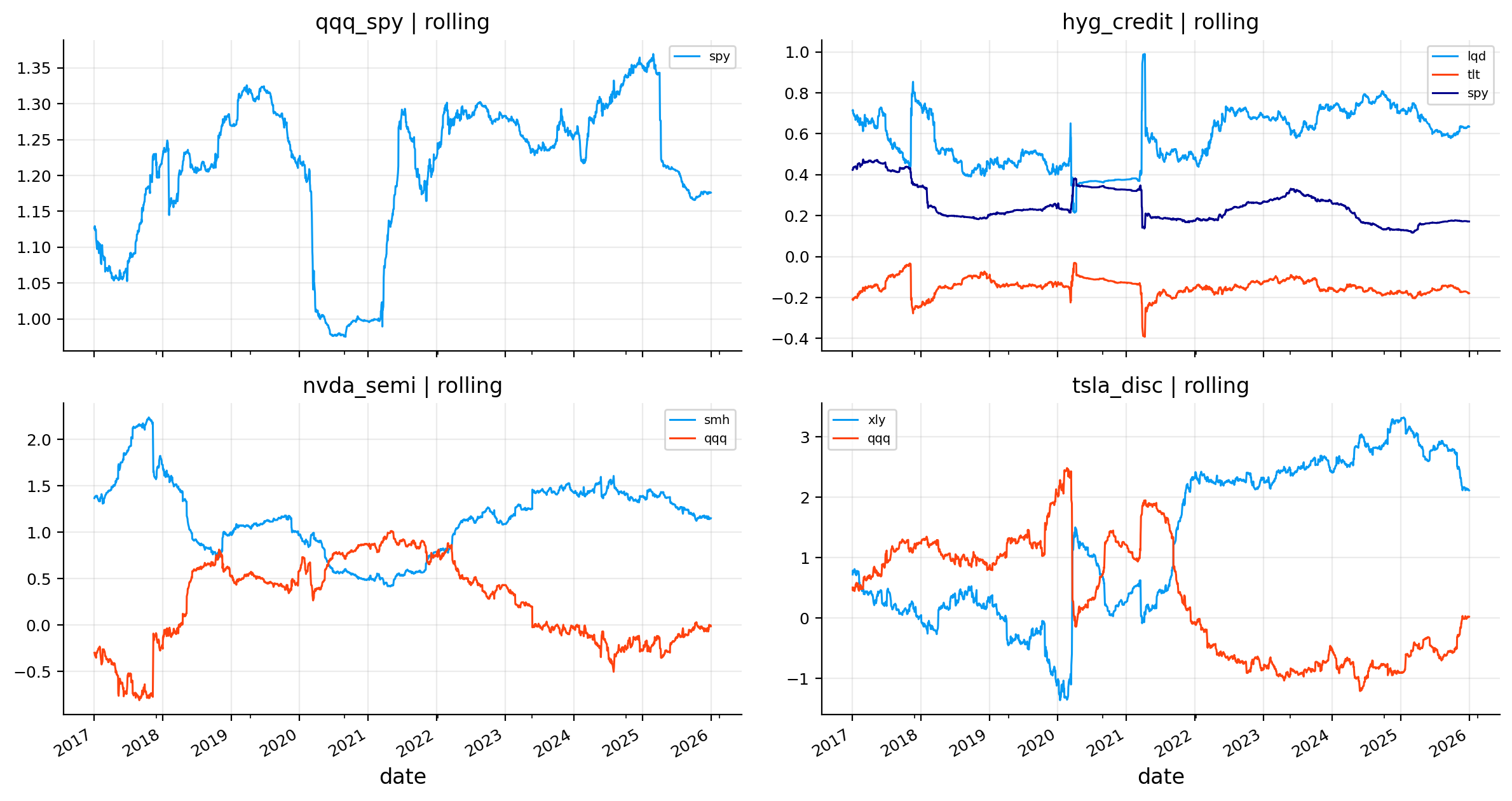

4.1 Rolling beta and normalized price behavior

The rolling beta plots give a first visual sense of why a static hedge can be too rigid. The rolling beta for QQQ/SPY stays mostly around the 1.1 to 1.3 zone, but it still shifts across regimes. During periods when growth stocks dominate, QQQ needs a higher SPY hedge to remove market beta. During stress or rotation periods, the beta compresses.

For TLT/IEF, the beta is much higher because TLT has longer duration. If IEF is a medium-duration Treasury ETF and TLT is long duration, then one dollar of IEF doesn’t offset one dollar of TLT. The hedge ratio has to scale up with duration exposure.

For NVDA/SMH+QQQ and TSLA/XLY+QQQ, the rolling paths are less stable. That instability is economically reasonable. These stocks aren’t just sector exposures. NVDA has AI, semiconductor, and company-specific earnings repricing. TSLA has consumer discretionary beta, growth beta, rate sensitivity, and company-specific volatility. A hedge ratio can remove broad exposure, but it can’t turn these stocks into clean ETF spreads.

The normalized price plots show the same point from a price-level perspective. AGG and BND track very closely. TLT and IEF track directionally but with large divergence because their durations differ. GDX and GLD diverge sharply in some periods, especially when miner margins or equity risk dominate gold itself. XLK and QQQ are close but not identical, since QQQ is a Nasdaq index and XLK is a technology sector ETF.

4.2 Residual variance and \(R^2\) intuition

The diagnostic \(R^2\) is useful because it tells us how much of the target’s return variance can be explained by the hedge proxy. In a one-factor regression with intercept:

\[

R^2 = \rho_{yx}^2

\]

So if QQQ and SPY have correlation around \(0.934\), then \(R^2\) is about:

\[

0.934^2 \approx 0.872

\]

That matches the table. It means about 87% of QQQ’s daily return variance is explained by SPY in the full sample. The remaining 13% is the residual growth/technology component.

For a hedge book, the residual variance is:

\[

\sigma^2_{res} = \sigma_y^2(1-R^2)

\]

in the simple one-factor static case. This explains why high-correlation relationships are easier to hedge. If \(R^2\) is high, the residual variance has to be much lower than target variance. If \(R^2\) is low, even the optimal hedge can only remove part of the target risk.

That’s why GDX is hard. Its relationship with GLD and SPY is real, but not dominant. A large part of GDX movement remains outside those hedges.

5) Hedge-book mechanics and static OLS

Now we build the actual hedge-book logic. A hedge estimator gives a beta path. The trading book converts that path into returns, turnover, costs, and NAV.

For a target \(y_t\) and hedge vector \(\mathbf{x}_t\), the gross hedged return is:

This is important because a dynamic hedge isn’t free. If a beta estimator jumps around every week, it can look better before costs and worse after costs. The hedge-book metrics track:

volatility reduction: how much annualized volatility falls relative to the unhedged target,

expected shortfall reduction: how much the left-tail loss improves,

maximum drawdown difference: whether the hedge reduces peak-to-trough pain,

beta reduction: how much residual exposure to the hedge proxy remains,

turnover and cost drag: whether the model is implementable.

Static OLS is the first benchmark. We estimate one fixed beta from the first 504 observations:

\[

\hat{\boldsymbol{\beta}}_{OLS} = (X^\top X)^{-1}X^\top y

\]

Then we hold that hedge ratio through the rest of the sample, with weekly book evaluation. Static OLS is simple and low-turnover, but it assumes the relationship is stable after the training period.

This asks whether the residual book really removed exposure to the hedge proxy. If beta reduction is high but drawdown improvement is bad, the hedge removed the intended factor but introduced or exposed another source of risk.

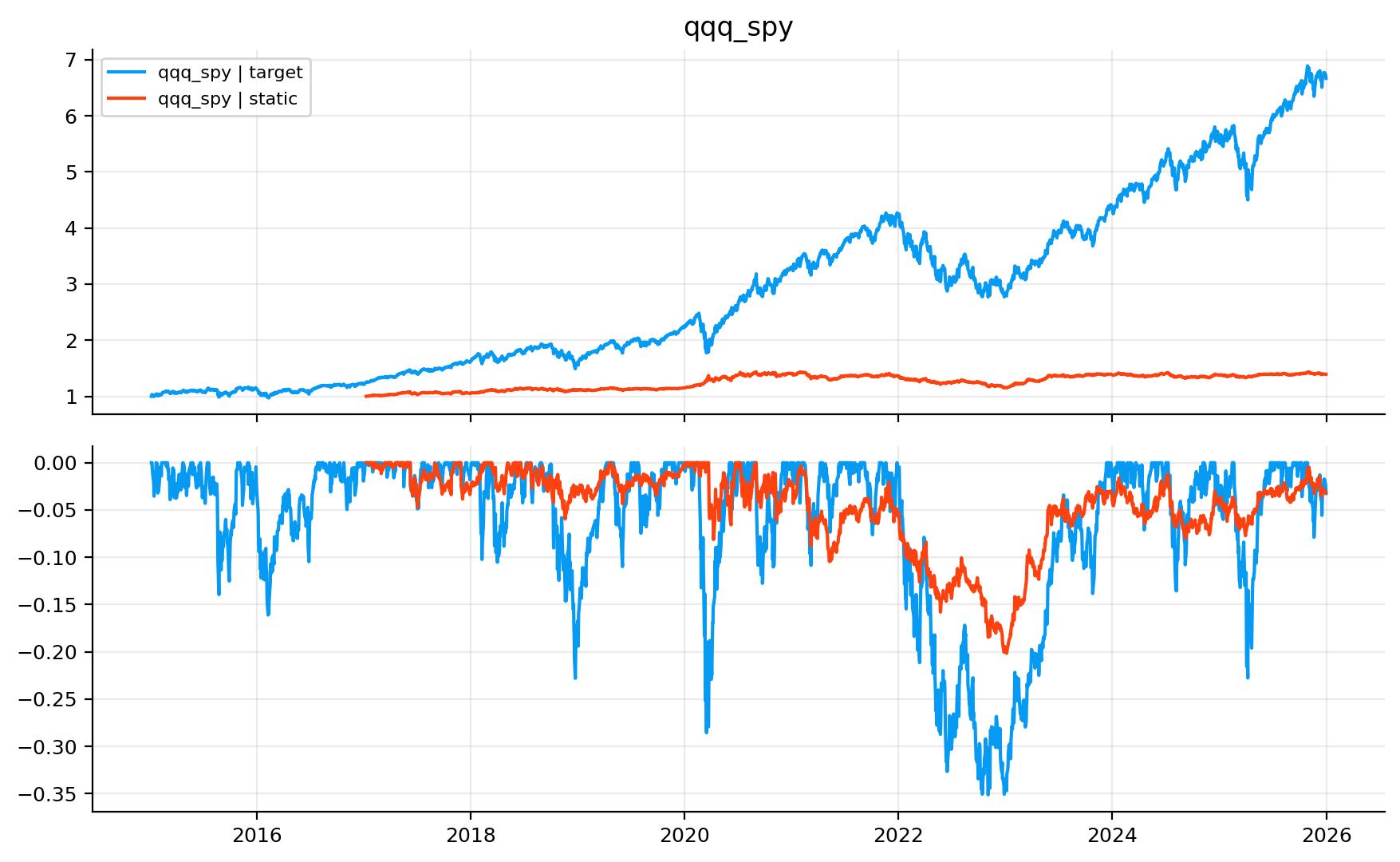

From the static OLS table, the first result is strong: a fixed hedge ratio already removes a lot of risk in many relationships.

The cleanest case is AGG/BND, with about 71.5% volatility reduction and 81.1% expected-shortfall reduction. That makes sense because AGG and BND are both broad aggregate bond ETFs. A static hedge works because the relationship is structurally stable.

QQQ/SPY also works very well, with about 64.2% volatility reduction and 65.1% ES reduction. This doesn’t mean QQQ becomes risk-free. It means most of QQQ’s movement is still broad equity beta, and SPY can remove a large part of it. The remaining residual is the growth/technology tilt.

TLT/IEF gives about 58.4% volatility reduction and a very strong drawdown improvement around 19.4 percentage points. That’s a duration-scaling hedge. IEF doesn’t perfectly offset TLT, but it captures much of the Treasury-rate factor.

The weak warning sign is GDX/GLD, where static hedging reduces volatility only about 20.5% and makes the maximum drawdown difference negative by about 46 percentage points. This is exactly why GDX is a hard hedge target. Gold miners can sell off with equities even when gold behaves defensively. A static GLD/SPY mix doesn’t fully capture that regime-switching behavior.

For the single stocks, static hedging lowers volatility meaningfully, especially NVDA, AAPL, MSFT, and AMZN. But drawdown improvement isn’t universal. AMD, AAPL, and MSFT show negative max-drawdown differences under static hedging, which means the hedge reduced day-to-day volatility but didn’t necessarily protect the worst path. This is a useful distinction: lower variance doesn’t always mean better drawdown control.

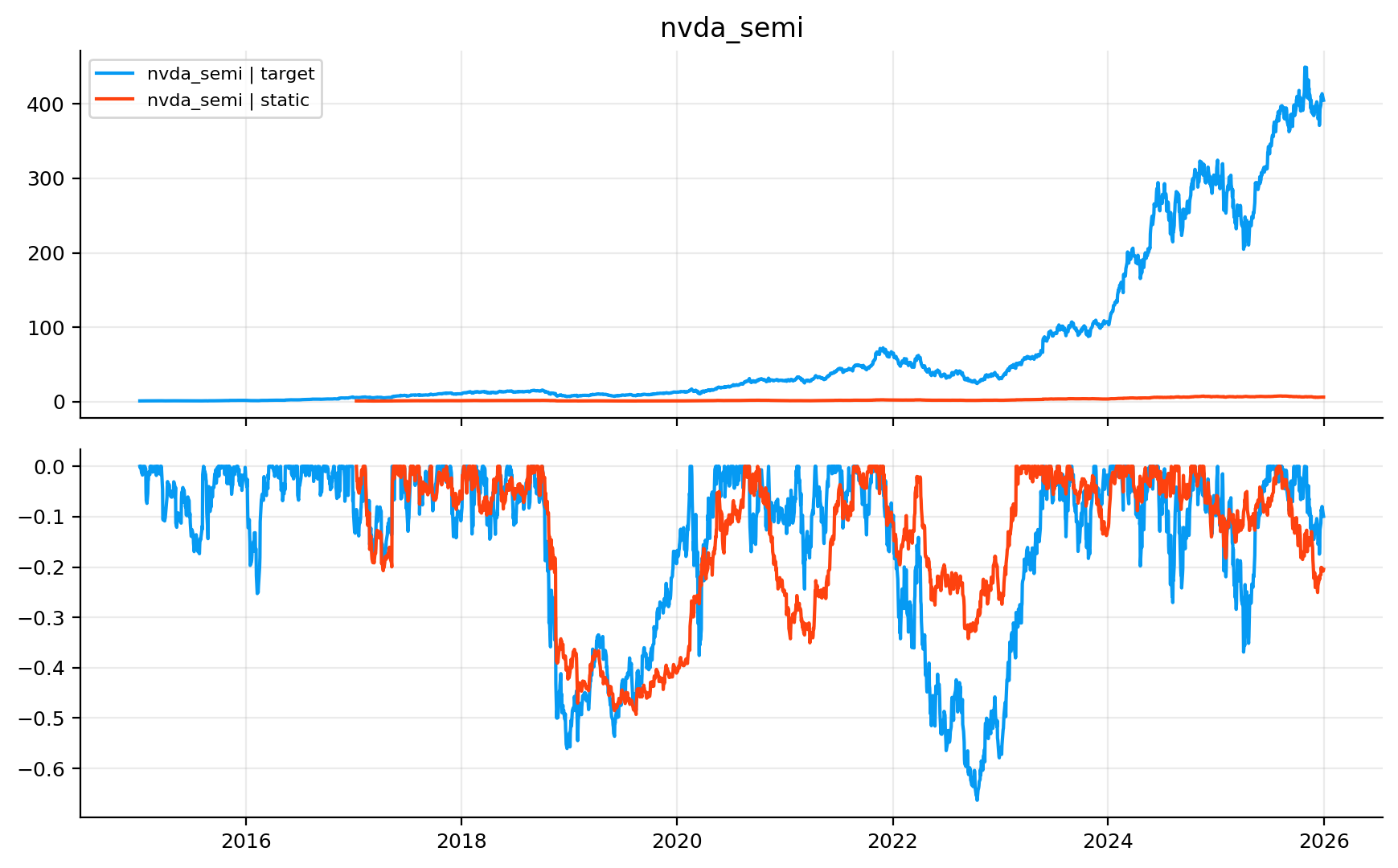

The NAV and drawdown plots for QQQ/SPY and NVDA/SMH+QQQ help explain the difference between hedging and investing.

For QQQ/SPY, the static hedged book is much flatter than the target. That’s exactly the point. We aren’t trying to beat QQQ with the hedge book. We’re trying to strip away the SPY beta and isolate the relative return of QQQ over broad market exposure. The drawdown panel shows a much smaller drawdown profile than unhedged QQQ, especially around 2020 and 2022.

For NVDA, the target NAV explodes after 2023 because NVDA had a huge idiosyncratic and AI-related rally. A hedged book removes some semiconductor and Nasdaq beta, but it also removes part of the exposure that helped NVDA compound. This is a common practical tradeoff:

A hedge that removes systematic downside also removes systematic upside. The residual book is cleaner, but it won’t behave like the original target asset.

So the correct evaluation depends on the goal. If the goal is pure exposure to NVDA, hedging looks like giving up upside. If the goal is isolating NVDA-specific alpha after sector and growth exposure, hedging is the right tool.

6) Rolling OLS hedge ratios

Static OLS assumes one relationship for the whole out-of-sample period. Rolling OLS relaxes that assumption. At each date \(t\), we estimate beta from the previous 252 trading days:

Rolling OLS improves many risk metrics relative to static OLS, but it also raises turnover.

The strongest improvements appear where the relationship genuinely changes through time. HYG credit improves from about 42.0% to 49.4% volatility reduction, and ES reduction rises from 47.4% to 52.4%. That makes sense because HYG’s exposure to LQD, TLT, and SPY changes across credit regimes. In calm markets, HYG behaves more like carry and equity beta. In stress, it becomes more credit-loss sensitive.

GDX/gold also improves from 20.5% to 36.7% volatility reduction, although drawdown is still bad. Dynamic beta helps, but GDX remains a difficult spread because gold miners have nonlinear exposure to gold, rates, equity stress, and operational leverage.

The tradeoff appears in turnover. For stock relationships, rolling OLS can become expensive in trading terms. TSLA/XLY+QQQ reaches annualized turnover above 5.19, and AAPL and AMD are also above 3. Even with only 5 bps cost, this starts to matter. With higher real-world costs or less liquid implementation, rolling OLS could be too active.

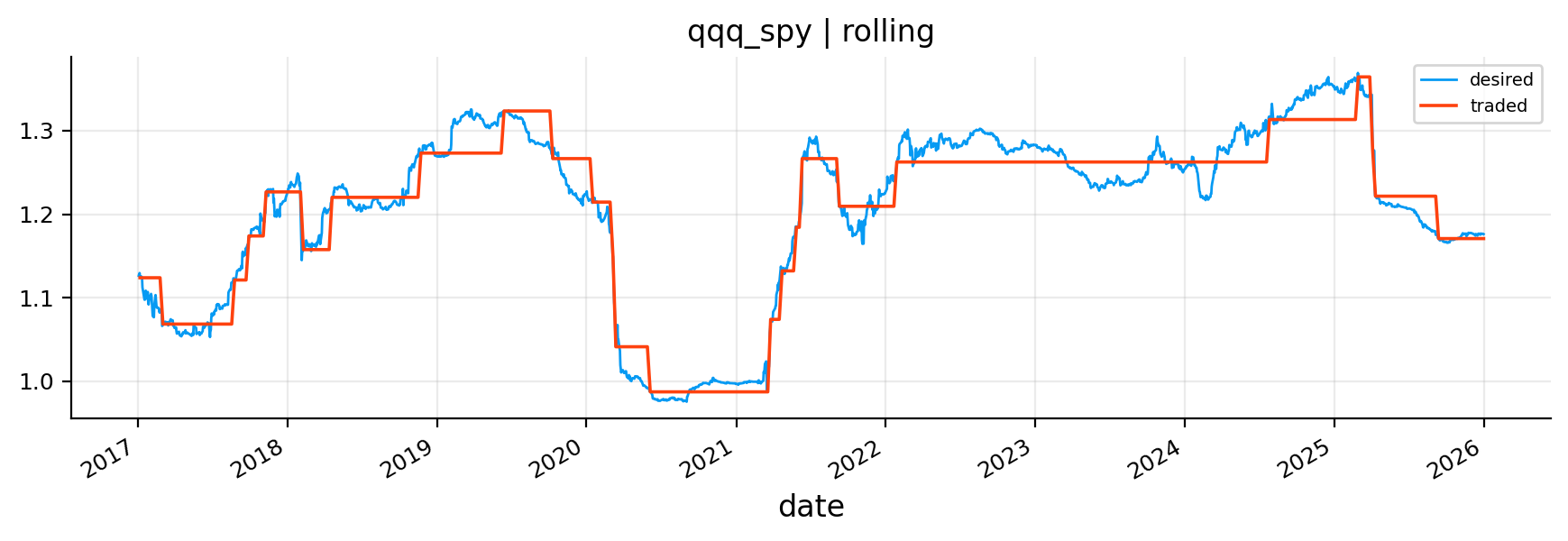

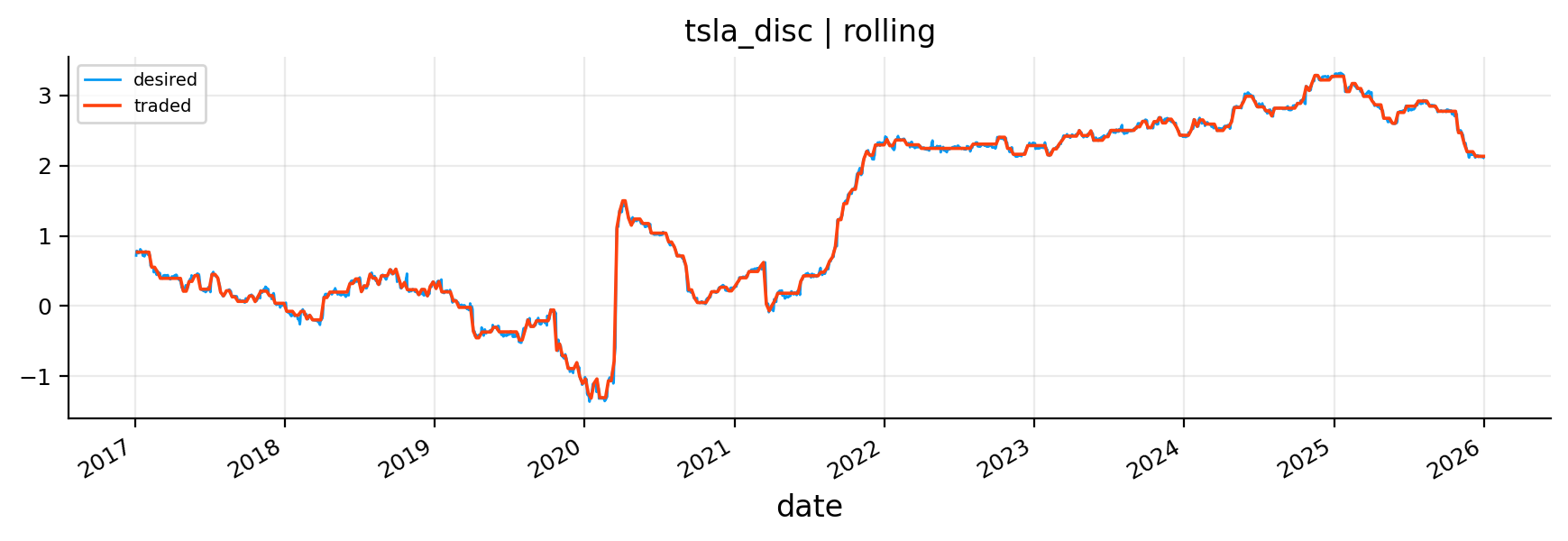

The rolling beta plots show why. For QQQ/SPY, the desired beta is fairly smooth, and the traded beta only updates occasionally. For TSLA, the desired beta path shifts much more aggressively. The no-trade band helps, but it can’t fully remove the instability when the relationship itself is unstable.

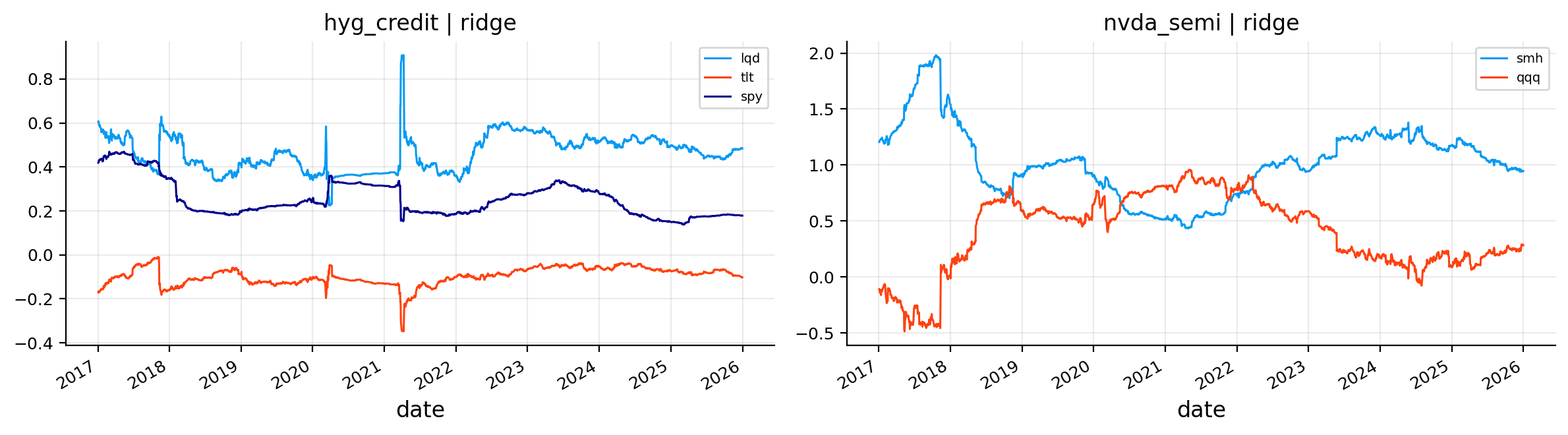

7) Ridge regression for hedge ratios

Ridge regression is the next improvement. It doesn’t make beta time-varying by itself; in this project we still estimate it on rolling windows. The difference is that ridge penalizes large and unstable coefficients.

Ridge is especially useful in multi-hedge relationships where hedge assets are correlated with each other. For example, SMH and QQQ both contain growth/technology exposure. XLY and QQQ both contain mega-cap growth components. LQD, TLT, and SPY can all explain parts of HYG during different regimes. In those settings, pure OLS can assign extreme coefficients because it tries to separate correlated explanatory variables too aggressively.

Ridge shrinks the solution toward smaller coefficients. It accepts a little bias in exchange for lower variance and better stability.

The ridge results are close to rolling OLS on volatility and ES reduction, but turnover is much lower.

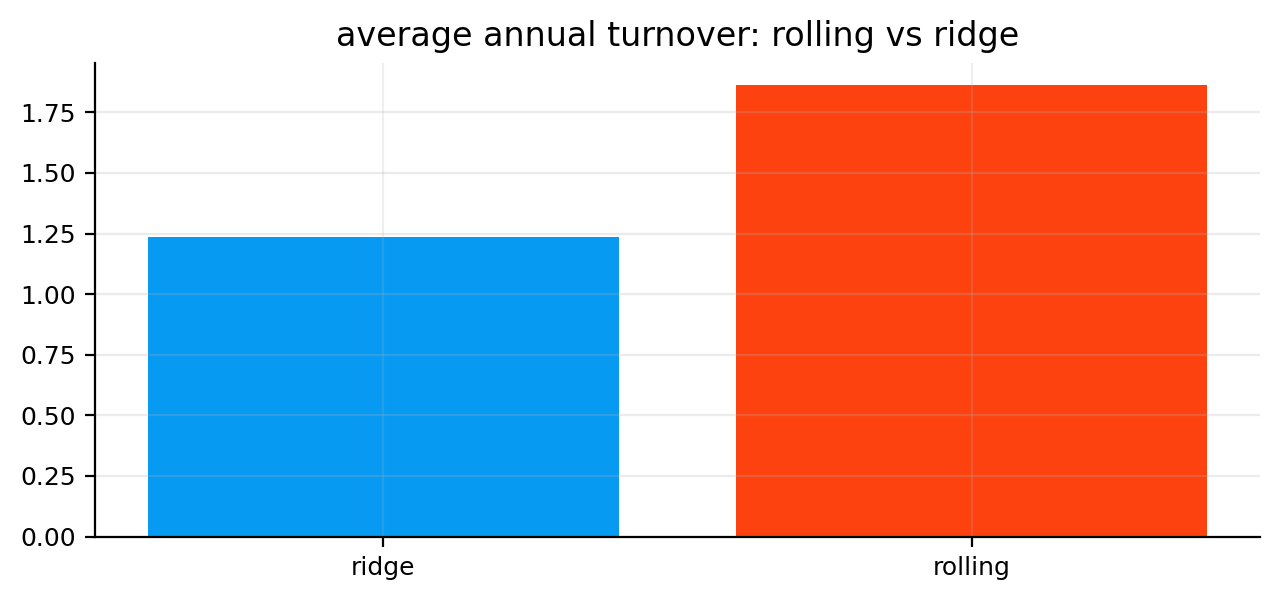

This is visible in the comparison bar: average annual turnover falls from about 1.86 for rolling OLS at the 5% band to about 1.24 for ridge. The difference is more important than it looks. The risk reduction is nearly the same, but the ridge path trades less.

A few relationship-level details stand out:

QQQ/SPY gets about 64.9% volatility reduction, almost identical to rolling OLS, with slightly lower turnover.

TLT/IEF keeps the strong hedge quality, with around 60.7% volatility reduction and the best drawdown improvement in that block.

GDX/gold improves a lot relative to static OLS, but the drawdown problem remains. Ridge can’t remove economic model risk. It only stabilizes coefficients.

NVDA/SMH+QQQ and MSFT/XLK+QQQ are strong examples where ridge keeps high risk reduction while controlling turnover relative to rolling OLS.

This is a useful practical lesson. The best hedge estimator isn’t always the most flexible one. A slightly biased estimator can be better if it avoids unstable coefficient paths.

7.1 Bias-variance tradeoff in hedge estimation

The difference between rolling OLS and ridge is a classic bias-variance tradeoff.

Rolling OLS is unbiased under the usual regression assumptions, but it can have high variance when hedge variables overlap. Ridge adds shrinkage, so the coefficients are biased toward zero, but the estimator becomes more stable:

A hedge ratio is a trading input, so lower estimator variance can be more valuable than zero bias. A slightly biased hedge that trades smoothly can be better than a theoretically unbiased hedge that jumps around and creates cost.

This is especially true in multi-hedge single-stock models. If SMH and QQQ both explain NVDA, OLS may fight over which hedge gets credit. Ridge softens that fight. It doesn’t remove the economic overlap, but it prevents the regression from translating that overlap into extreme coefficient changes.

8) Kalman filter hedge ratios

The Kalman filter is the most important econometric model in this project. Static OLS says the hedge ratio is one number. Rolling OLS says the hedge ratio can change, but only by re-estimating a regression on a fixed window. The Kalman filter uses a different idea: the hedge ratio is a hidden state that moves through time and is only observed indirectly through returns.

That language sounds abstract, but the finance idea is simple. The true beta between two assets is never directly visible. We only see daily target returns and hedge returns. From those observations, we infer the beta. When the relationship changes slowly, we want beta to drift. When today’s return is just noise, we don’t want beta to overreact.

So the Kalman filter is built for exactly this problem:

it keeps a current belief about the hedge ratio,

it predicts what today’s target return should be given that belief,

it measures the surprise between the predicted and realized target return,

it updates the hedge ratio only as much as the surprise deserves.

This makes it more structured than rolling OLS. Rolling OLS has a hard memory cutoff. The Kalman filter has a soft memory: old information fades because uncertainty accumulates, but it isn’t suddenly dropped from the model.

8.1 The state-space model

The Kalman filter starts by writing the hedge problem as a state-space model. There are two equations.

The first equation connects the hidden hedge ratio to the observed target return. This is the observation equation:

\(y_t\) is the target return, for example NVDA’s daily return,

\(\mathbf{x}_t\) is the vector of hedge returns, for example SMH and QQQ returns,

\(\boldsymbol{\beta}_t\) is the vector of hedge ratios at time \(t\),

\(\alpha_t\) is the time-varying intercept,

\(\varepsilon_t\) is the return shock the hedge basket didn’t explain.

We assume the unexplained return shock is Gaussian noise:

\[

\varepsilon_t \sim \mathcal{N}(0, R)

\]

The scalar \(R\) is observation noise. If \(R\) is large, daily returns are very noisy relative to the regression relationship. In that case, one bad prediction doesn’t prove beta changed. If \(R\) is small, a forecast error is more informative, so beta can update more.

The second equation describes how the hidden state moves. We collect the intercept and all hedge ratios into one vector:

The matrix \(Q\) is process noise. It controls how much the hedge ratios are allowed to move from one day to the next. High \(Q\) means we believe the relationship is unstable and beta can move quickly. Low \(Q\) means we believe the relationship is stable and beta should move slowly.

\(R\) is noise in returns. \(Q\) is noise in the hidden beta path. The whole Kalman filter is basically a disciplined balance between these two uncertainties.

8.2 Prediction step: belief before seeing today’s return

At the end of yesterday, the filter has two objects:

The notation \(t-1|t-1\) means “our estimate at time \(t-1\) after using information available through time \(t-1\).”

\(\boldsymbol{\theta}_{t-1|t-1}\) is yesterday’s best estimate of the state, meaning yesterday’s intercept and hedge ratios.

\(P_{t-1|t-1}\) is the uncertainty around that estimate. It’s a covariance matrix, so the diagonal entries measure uncertainty around each state component, and the off-diagonal entries measure how those uncertainties move together.

Before seeing today’s return, we predict today’s state. Since the state follows a random walk, the best prediction for today’s beta is yesterday’s beta:

The notation \(t|t-1\) means “our estimate for time \(t\) before seeing time \(t\) data.” The point isn’t that beta truly didn’t move. The point is that before seeing new data, the expected change in the random walk is zero.

But our uncertainty does increase:

\[

P_{t|t-1} = P_{t-1|t-1} + Q

\]

This equation is easy to misread if we only stare at the formula. It means: even if our best beta estimate stays the same, we become less certain because another day has passed and the hidden relationship could have drifted. The amount of extra uncertainty is exactly \(Q\).

Financially, this is sensible. If the hedge ratio between TLT and IEF was estimated yesterday, it probably didn’t become completely different overnight. But if rates moved, duration risk repriced, or bond volatility shifted, we should be a little less sure today than we were yesterday.

8.3 Measurement step: prediction error and its uncertainty

Now we observe today’s hedge returns and target return. To write the regression compactly, we create the design vector:

This is simply the regression prediction using the current beta belief. If the target is HYG and the hedges are LQD, TLT, and SPY, this predicted return is the return HYG “should” have earned based on today’s credit, rate, and equity moves.

Then we compare prediction with reality:

\[

v_t = y_t - \hat{y}_{t|t-1}

\]

This \(v_t\) is called the innovation. It’s the new information in today’s observation. If \(v_t\) is near zero, the old beta explained today’s return well. If \(v_t\) is large, something was missed: either beta changed, the target had an idiosyncratic shock, or the observation is noisy.

The filter also needs to know how surprising that innovation is. That’s the innovation variance:

\[

S_t = \mathbf{h}_t^\top P_{t|t-1}\mathbf{h}_t + R

\]

This equation has two parts:

\(\mathbf{h}_t^\top P_{t|t-1}\mathbf{h}_t\) is uncertainty coming from our uncertain state estimate. If beta is poorly known, the prediction is uncertain.

\(R\) is observation noise. Even with a perfect beta estimate, daily returns still contain noise.

So \(S_t\) answers: how much prediction error should we expect before calling today’s move a real beta signal? A large \(S_t\) means we expected noisy prediction errors, so a given \(v_t\) isn’t too informative. A small \(S_t\) means the prediction should have been accurate, so the same \(v_t\) matters more.

8.4 Kalman gain and state update

The Kalman gain decides how much the hedge ratio should move after seeing the innovation:

\[

K_t = \frac{P_{t|t-1}\mathbf{h}_t}{S_t}

\]

Here \(K_t\) is a vector with one entry for each state component: one for the intercept and one for each hedge ratio. It works like an adaptive learning rate.

The numerator \(P_{t|t-1}\mathbf{h}_t\) says how much uncertainty in each state component matters for today’s prediction. If the SPY hedge coefficient is very uncertain and today’s SPY return is large, the SPY beta component receives more attention. If a hedge return is tiny today, there isn’t much information about that hedge’s beta, even if the prediction error is large.

The denominator \(S_t\) scales the update by total prediction uncertainty. If today’s prediction was expected to be noisy, the filter updates less. If today’s prediction was supposed to be precise, the filter updates more.

If the target return is higher than predicted, \(v_t > 0\). Depending on the signs and magnitudes inside \(K_t\), the filter may raise one or more hedge ratios. If the target return is lower than predicted, \(v_t < 0\), the update goes in the opposite direction.

After updating the state, the filter reduces uncertainty:

\[

P_{t|t} = (I - K_t\mathbf{h}_t^\top)P_{t|t-1}

\]

The identity matrix \(I\) keeps dimensions correct. The term \(K_t\mathbf{h}_t^\top\) represents how much information today’s observation gave us about the state. After using a useful observation, we’re more confident than before, so uncertainty falls.

The full cycle is therefore:

carry yesterday’s hedge ratio forward,

add uncertainty because the true beta may have moved,

predict today’s target return,

measure the forecast surprise,

decide how informative the surprise is,

update the hedge ratio,

reduce uncertainty after learning from the observation.

That’s why the Kalman filter feels smoother than rolling OLS but still more adaptive than static OLS. It doesn’t throw away history, and it doesn’t blindly trust every new observation.

8.5 Likelihood selection for \(Q\) and \(R\)

The filter needs \(Q\) and \(R\), and choosing them casually would make the model arbitrary. So we select them from the training window using likelihood.

The likelihood measures how plausible the observed forecast errors are under a candidate pair of \(Q\) and \(R\). For each observation, the Gaussian log-likelihood contribution is:

\(v_t\) is the innovation, the one-step-ahead forecast error,

\(S_t\) is the innovation variance,

\(\log(2\pi S_t)\) penalizes models that claim too much uncertainty,

\(v_t^2/S_t\) penalizes models that produce forecast errors too large relative to their claimed uncertainty.

The total likelihood over the training sample is:

\[

\mathcal{L} = \sum_{t=1}^{T}\ell_t

\]

The model tries several process-noise and observation-noise settings, then chooses the setting with the best penalized likelihood. The penalty matters because a very large \(Q\) can make beta chase the target too closely. That may improve in-sample forecast errors, but it creates unstable hedge ratios and high turnover.

A good Kalman hedge isn’t the most reactive hedge. It’s the hedge that updates fast enough to follow genuine regime changes, but slowly enough to ignore noise.

8.6 Kalman filter versus rolling windows

The most important conceptual difference is how each method treats old data.

Rolling OLS has a hard memory cutoff:

\[

\mathcal{W}_t = \{t-251,\ldots,t\}

\]

Everything inside the window is used equally, and everything outside the window is ignored completely. This makes the estimator easy to understand, but it creates artificial jumps when important observations enter or leave the window.

The Kalman filter has soft memory. Past data affects the current state through the previous posterior estimate and its uncertainty. If the filter is confident, one new observation doesn’t move beta much. If the filter is uncertain, the same observation can move beta more.

So rolling OLS adapts by deleting history. Kalman adapts by updating beliefs. That’s why Kalman is usually smoother and lower-turnover. But smoothness can become a weakness if the true beta changes abruptly. In that case, rolling OLS may react faster.

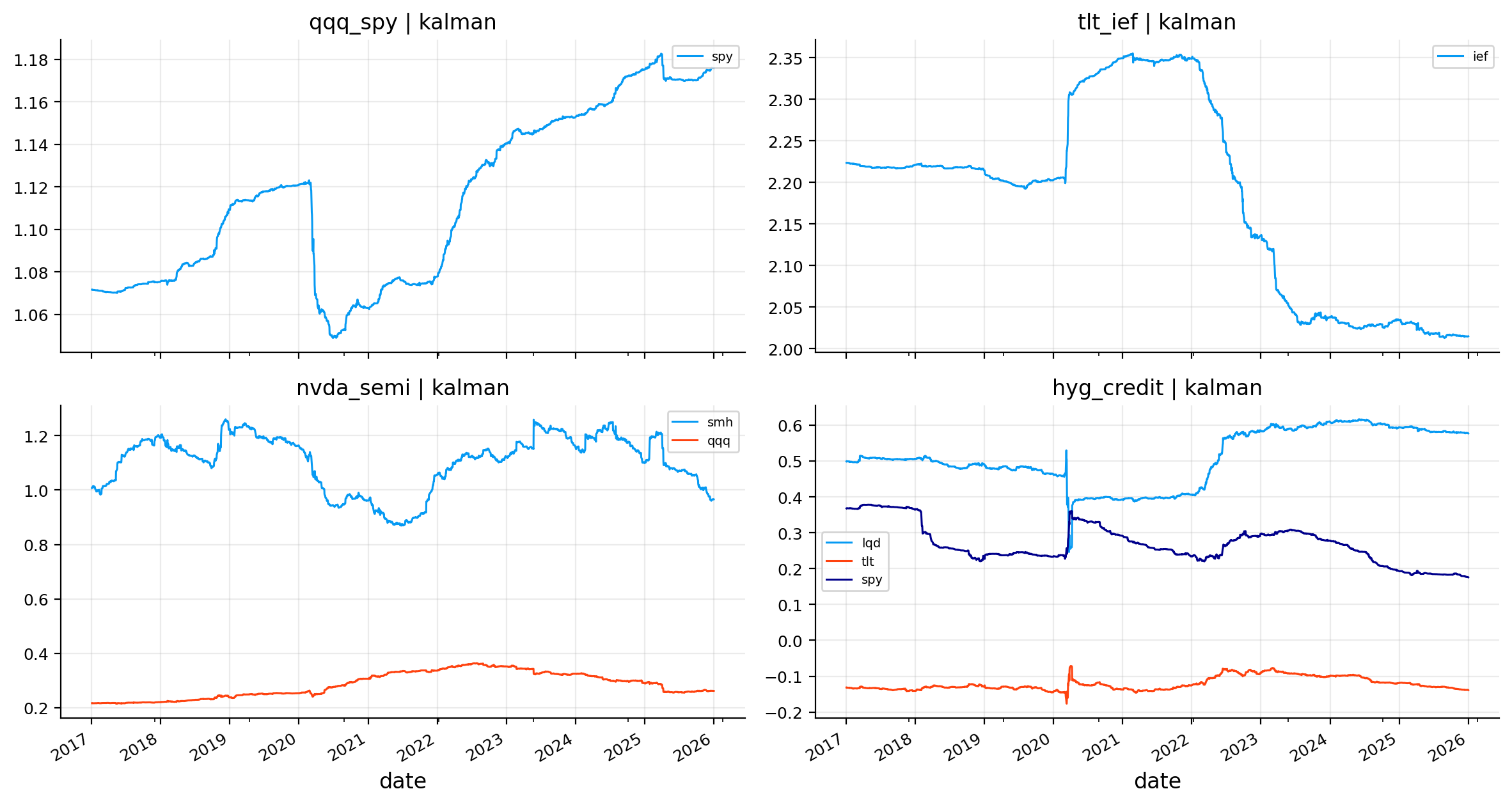

The Kalman results show exactly that smoother behavior.

Risk reduction is strong across most relationships, but turnover is much lower than rolling OLS and ridge in many of the noisy stock relationships. For example:

NVDA/SMH+QQQ gets about 45.6% volatility reduction with annualized turnover around 0.33, compared with ridge turnover around 1.59 and rolling turnover above 2.22.

AMD/SMH+QQQ has turnover around 0.33, much lower than ridge and rolling, while keeping similar volatility reduction.

HYG credit gets nearly the same ES reduction as rolling OLS, but with much lower turnover.

QQQ/SPY is stable under all methods, so Kalman doesn’t need to win there. Its advantage is more about smooth implementation than maximum score.

The Kalman beta plots show smooth paths. QQQ/SPY gradually rises through the sample. TLT/IEF shifts sharply around the rate shock period and then compresses. HYG credit shows changing weights across LQD, TLT, and SPY, which fits the economics of credit: high yield alternates between behaving like credit carry, duration exposure, and equity risk.

Kalman isn’t automatically best. In some cases it may be too smooth, especially when a relationship changes quickly. But it’s the cleanest statistical answer to dynamic hedge-ratio estimation because it explicitly models beta as an evolving latent state.

9) No-trade band sensitivity

After estimating a desired beta path, we decide how aggressively to trade it. The no-trade band controls this. If the band is zero, every weekly beta change is traded. If the band is wider, small beta changes are ignored.

We test:

\[

b \in \{0.00, 0.025, 0.05, 0.075, 0.10\}

\]

For each band, we recompute the hedge books for rolling, ridge, and Kalman models, then evaluate average risk reduction, turnover, cost, and a composite score.

The composite score is intentionally multi-objective. It rewards:

higher volatility reduction,

higher ES reduction,

better drawdown improvement,

stronger beta reduction,

more stable beta paths,

and penalizes:

turnover,

cost drag,

negative drawdown effects.

A pure volatility score would be too narrow. A hedge model can reduce variance by taking an unstable residual exposure that creates drawdown or trading costs. The score tries to avoid that.

Show code

def band_norm(s, lower=False): x = pd.to_numeric(s, errors="coerce").replace([np.inf, -np.inf], np.nan)if x.notna().sum() <=1: out = pd.Series(0.5, index=s.index)else: lo, hi = x.quantile(0.05), x.quantile(0.95) xc = x.clip(lo, hi) span = xc.max() - xc.min() out = pd.Series(0.5, index=s.index) if span <=1e-12else (xc - xc.min()) / spanreturn (1- out if lower else out).fillna(0.5)def band_score(tab): parts = []for _, g in tab.groupby("relationship", sort=False): h = g.copy() vol_s = band_norm(h["vol_red"]) dd_bad = (-pd.to_numeric(h["maxdd_diff"], errors="coerce")).clip(lower=0.0).div(0.10).clip(upper=1.0).fillna(0.0) vol_s = vol_s.mask(h["maxdd_diff"] <-0.05, np.minimum(vol_s, 0.50)) h["score"] = (0.30* vol_s+0.20* band_norm(h["es_red"])+0.15* band_norm(h["maxdd_diff"])+0.15* band_norm(h["beta_red"])+0.10* band_norm(h["beta_stability"])-0.05* (1- band_norm(h["turnover_ann"], lower=True))-0.05* (1- band_norm(h["cost_drag_ann"], lower=True))-0.10* dd_bad ) parts.append(h)return pd.concat(parts, ignore_index=True) if parts else pd.DataFrame()band_grid = [0.00, 0.025, 0.05, 0.075, 0.10]dyn_models = ["rolling", "ridge", "kalman"]sens_rows = []for bnd in band_grid: books_sens =dict(books_target)for r in rel_main:for m in dyn_models: b1 = rebalance_beta(beta_daily[(r.name, m)], ret_b_main.index) b2 = band_beta(b1, band=bnd) books_sens[f"{r.name} | {m}"] = book_result(hedge_book(ret_b_main, r, b2)) tab_sens = model_table(books_sens, rel_main, ret_m_main)for m, g in band_score(tab_sens).groupby("model"): sens_rows.append({"model": m, "band": bnd, "avg_vol_red": g["vol_red"].mean(),"avg_es_red": g["es_red"].mean(), "avg_turnover_ann": g["turnover_ann"].mean(),"avg_cost_drag_ann": g["cost_drag_ann"].mean(), "avg_score": g["score"].mean()})tab_band = pd.DataFrame(sens_rows)display(tab_band.round(4))fig, axes = plt.subplots(1, 2, figsize=(11.5, 3.5), sharex=True)for m, g in tab_band.groupby("model"): axes[0].plot(g["band"], g["avg_turnover_ann"], marker="o", label=m) axes[1].plot(g["band"], g["avg_score"], marker="o", label=m)axes[0].set_title("annual turnover vs band")axes[1].set_title("score vs band")for ax in axes: ax.grid(True, alpha=0.25) ax.set_xlabel("band")axes[0].legend(fontsize=8)plt.tight_layout()plt.show()

model

band

avg_vol_red

avg_es_red

avg_turnover_ann

avg_cost_drag_ann

avg_score

0

kalman

0.000

0.4501

0.4719

0.5335

0.0003

0.3277

1

ridge

0.000

0.4568

0.4816

1.8476

0.0009

0.5336

2

rolling

0.000

0.4566

0.4812

2.5414

0.0013

0.3320

3

kalman

0.025

0.4481

0.4700

0.3931

0.0002

0.3118

4

ridge

0.025

0.4563

0.4807

1.4766

0.0007

0.5592

5

rolling

0.025

0.4562

0.4807

2.1618

0.0011

0.3695

6

kalman

0.050

0.4460

0.4680

0.3508

0.0002

0.2542

7

ridge

0.050

0.4548

0.4796

1.2358

0.0006

0.5659

8

rolling

0.050

0.4559

0.4799

1.8619

0.0009

0.4351

9

kalman

0.075

0.4454

0.4677

0.3155

0.0002

0.2837

10

ridge

0.075

0.4541

0.4780

1.1076

0.0006

0.5537

11

rolling

0.075

0.4543

0.4779

1.6460

0.0008

0.3969

12

kalman

0.100

0.4434

0.4647

0.2917

0.0001

0.2599

13

ridge

0.100

0.4523

0.4766

1.0123

0.0005

0.5549

14

rolling

0.100

0.4523

0.4754

1.4877

0.0007

0.3939

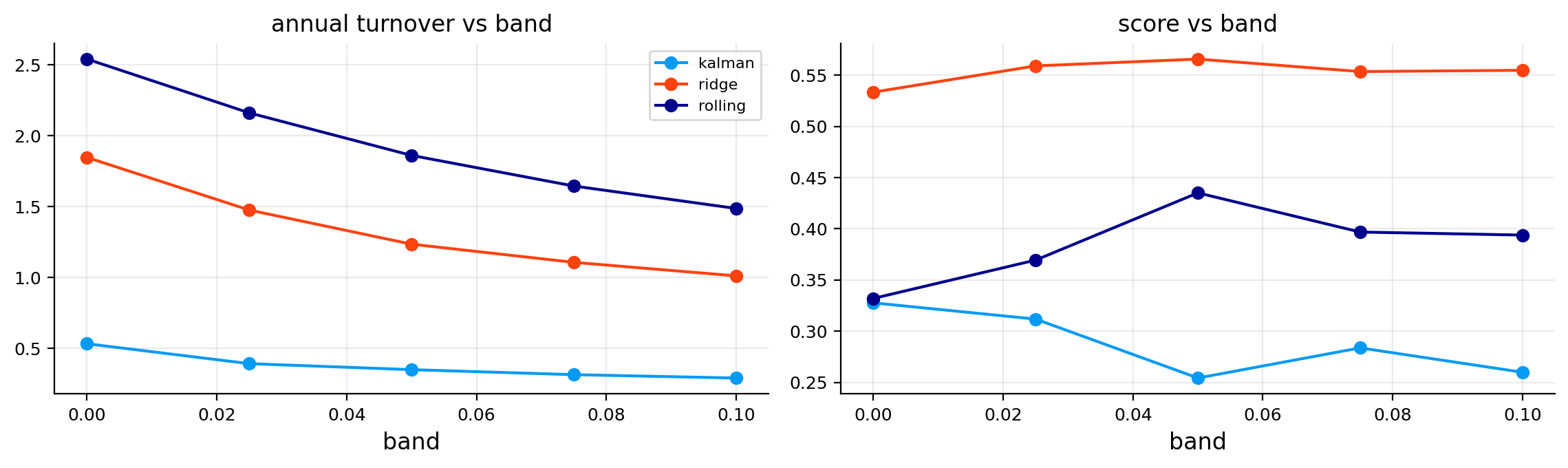

The band sensitivity table gives a clean implementation lesson.

Kalman has the lowest turnover at every band. At band zero, its average annual turnover is only about 0.53, while ridge is around 1.85 and rolling is around 2.54. This confirms the state-space model is already smoothing the beta path before the no-trade band is applied.

Ridge has the highest average score across the tested bands. At the 5% band, ridge reaches the best average score, around 0.566, with average volatility reduction around 45.5% and average ES reduction around 48.0%. Rolling OLS has similar risk reduction but higher turnover, so its score is lower.

The plots show the tradeoff visually:

turnover falls as the band gets wider,

score for ridge improves up to about the 5% band and then stays near the top,

rolling benefits from a band because raw rolling beta is too jumpy,

Kalman doesn’t benefit much from wider bands because it already trades slowly.

So the 5% band is a reasonable choice. It removes many small noisy updates without freezing the hedge ratio too much.

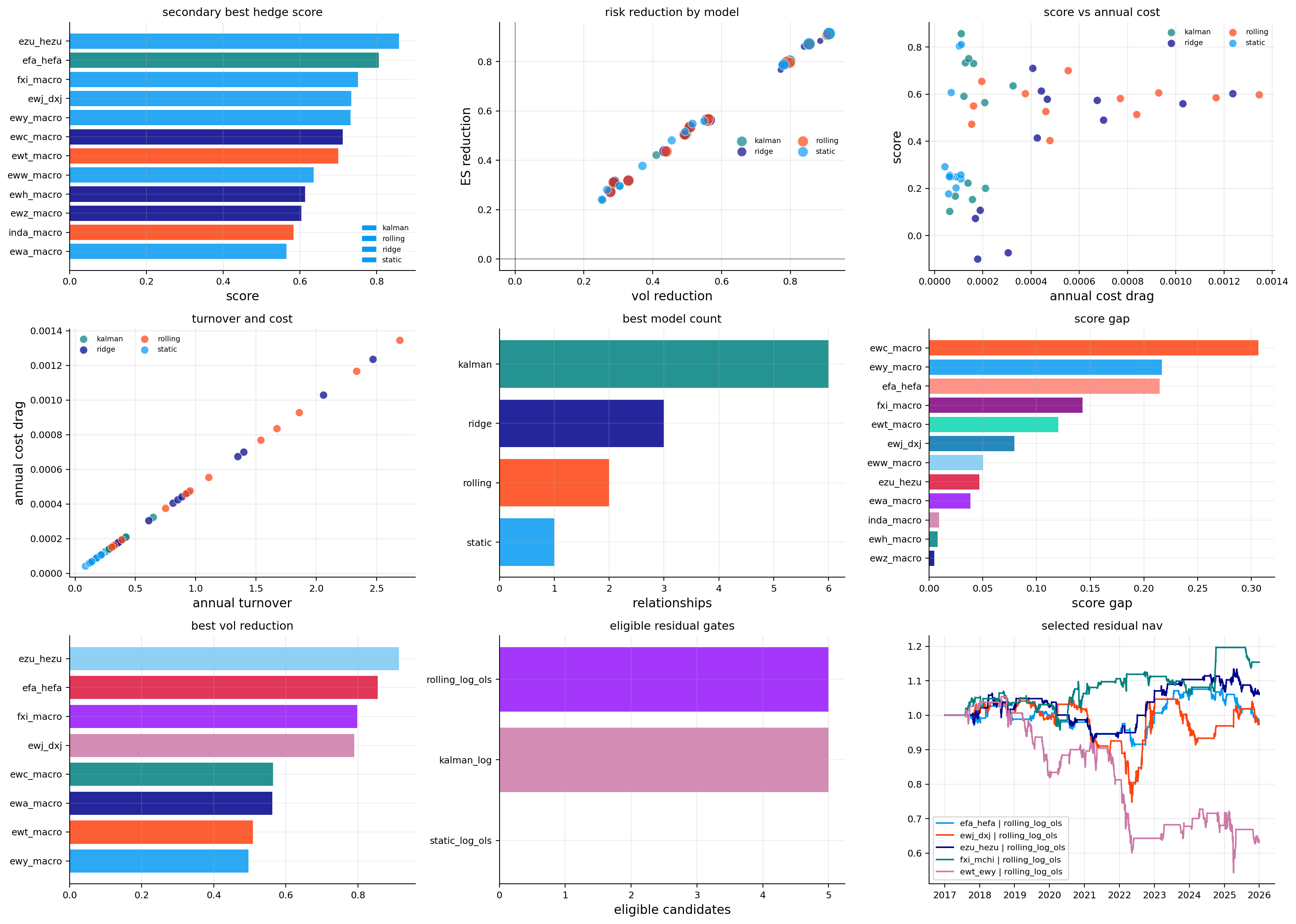

10) Model scoring and best hedge selection

Now we combine the static, rolling, ridge, and Kalman results into one comparison table. The scoring is done within each relationship, not globally. That detail matters.

A 40% volatility reduction in TSLA isn’t the same difficulty as a 40% reduction in AGG. AGG/BND is a clean ETF replication problem. TSLA/XLY+QQQ is a much harder idiosyncratic stock problem. Scoring within each relationship avoids unfairly rewarding easy pairs only because they are easy.

For relationship \(i\) and model \(m\), the score has the structure:

A large score gap means one model clearly dominates for that relationship. A small score gap means the choice is less certain.

Show code

def norm_group(s, lower=False): x = pd.to_numeric(s, errors="coerce").replace([np.inf, -np.inf], np.nan)if x.notna().sum() ==0: out = pd.Series(0.5, index=s.index)else: xc = x.clip(x.quantile(0.05), x.quantile(0.95)) span = xc.max() - xc.min() out = pd.Series(0.5, index=s.index) if span <=1e-12else (xc - xc.min()) / spanreturn (1- out if lower else out).fillna(0.5)def score_table(tab): parts = []for _, g in tab.groupby("relationship", sort=False): h = g.copy() vol_s = norm_group(h["vol_red"]) dd_bad = (-pd.to_numeric(h["maxdd_diff"], errors="coerce")).clip(lower=0.0).div(0.10).clip(upper=1.0).fillna(0.0) vol_s = vol_s.mask(h["maxdd_diff"] <-0.05, np.minimum(vol_s, 0.50)) h["score"] = (0.30* vol_s+0.20* norm_group(h["es_red"])+0.15* norm_group(h["maxdd_diff"])+0.15* norm_group(h["beta_red"])+0.10* norm_group(h["beta_stability"])-0.05* (1- norm_group(h["turnover_ann"], lower=True))-0.05* (1- norm_group(h["cost_drag_ann"], lower=True))-0.10* dd_bad ) parts.append(h)return pd.concat(parts, ignore_index=True) if parts else pd.DataFrame()def best_table(tab): idx = tab.groupby("relationship")["score"].idxmax() cols = ["relationship", "model", "score", "vol_red", "es_red", "maxdd_diff", "cost_drag_ann"]return tab.loc[idx, cols].rename(columns={"model": "best_model"}).reset_index(drop=True)def robust_table(tab): wins = best_table(tab)["best_model"].value_counts() iflen(tab) else pd.Series(dtype=int) rows = []for m, g in tab.groupby("model"): rows.append({"model": m, "median_score": g["score"].median(),"median_vol_red": g["vol_red"].median(), "median_es_red": g["es_red"].median(),"median_cost_drag_ann": g["cost_drag_ann"].median(), "win_count": int(wins.get(m, 0)),"failure_count": int(((g["vol_red"] <=0) | (g["score"] <=0)).sum())})return pd.DataFrame(rows).sort_values(["median_score", "win_count"], ascending=False)

Show code

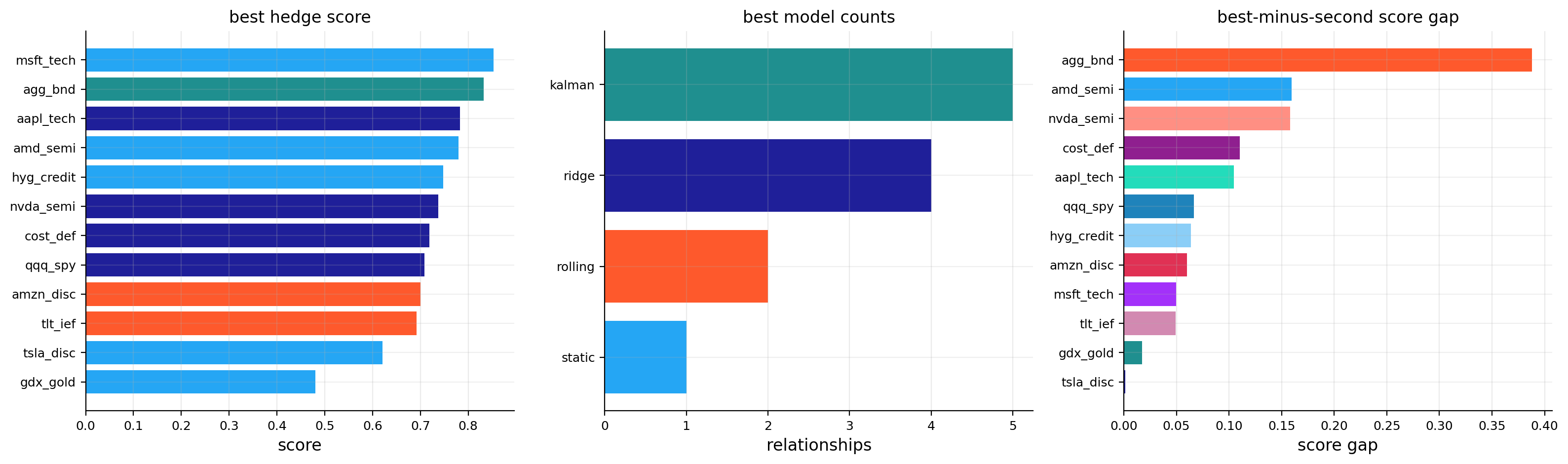

books_all = {}books_all.update(books_target)books_all.update(books_static)books_all.update(books_roll)books_all.update(books_ridge)books_all.update(books_kalman)bt_all = books_alltab_model = model_table(bt_all, rel_main, ret_m_main)tab_score = score_table(tab_model)tab_best = best_table(tab_score)tab_robust = robust_table(tab_score)score_cols = ["relationship", "model", "vol_red", "es_red", "maxdd_diff", "beta_red","turnover_ann", "cost_drag_ann", "beta_stability", "rebalance_count"]display(tab_score[score_cols].round(4).head(20))fig, axes = plt.subplots(1, 3, figsize=(16, 4.8))best_plot = tab_best.sort_values("score").copy()model_order =list(best_plot["best_model"].dropna().unique())model_colors = {m: colors[i %len(colors)] for i, m inenumerate(model_order)}axes[0].barh(best_plot["relationship"], best_plot["score"], color=[model_colors[m] for m in best_plot["best_model"]], alpha=0.88)axes[0].set_title("best hedge score")axes[0].set_xlabel("score")axes[0].grid(True, axis="x", alpha=0.25)counts = tab_best["best_model"].value_counts().sort_values()axes[1].barh(counts.index, counts.values, color=[colors[i %len(colors)] for i inrange(len(counts))], alpha=0.88)axes[1].set_title("best model counts")axes[1].set_xlabel("relationships")axes[1].grid(True, axis="x", alpha=0.25)gaps = {}for name, g in tab_score.groupby("relationship"): vals = g["score"].dropna().sort_values(ascending=False).values gaps[name] = vals[0] - vals[1] iflen(vals) >1else np.nangap_series = pd.Series(gaps).sort_values()axes[2].barh(gap_series.index, gap_series.values, color=[colors[(i +2) %len(colors)] for i inrange(len(gap_series))], alpha=0.88)axes[2].set_title("best-minus-second score gap")axes[2].set_xlabel("score gap")axes[2].grid(True, axis="x", alpha=0.25)plt.tight_layout()plt.show()tab_quality = tab_model.groupby("relationship").agg( best_vol_red=("vol_red", "max"), median_vol_red=("vol_red", "median"), best_es_red=("es_red", "max"), best_maxdd_diff=("maxdd_diff", "max"), median_cost_drag_ann=("cost_drag_ann", "median")).reset_index()display(tab_best.round(4))display(tab_robust.round(4))display(tab_quality.round(4))

relationship

model

vol_red

es_red

maxdd_diff

beta_red

turnover_ann

cost_drag_ann

beta_stability

rebalance_count

0

qqq_spy

static

0.6417

0.6509

0.1496

0.9547

0.1236

0.0001

1.0000

1

1

qqq_spy

rolling

0.6488

0.6592

0.1628

0.9773

0.2895

0.0001

0.9133

25

2

qqq_spy

ridge

0.6491

0.6586

0.1652

0.9835

0.2597

0.0001

0.9156

21

3

qqq_spy

kalman

0.6392

0.6480

0.1560

0.9537

0.1424

0.0001

0.9531

5

4

tlt_ief

static

0.5837

0.5382

0.1944

0.9163

0.2484

0.0001

1.0000

1

5

tlt_ief

rolling

0.6078

0.5837

0.2272

0.9963

0.6379

0.0003

0.7848

54

6

tlt_ief

ridge

0.6066

0.5834

0.2291

0.9657

0.6048

0.0003

0.7909

53

7

tlt_ief

kalman

0.5902

0.5486

0.2172

0.9354

0.2941

0.0001

0.8085

8

8

agg_bnd

static

0.7153

0.8112

0.1456

0.9857

0.1061

0.0001

1.0000

1

9

agg_bnd

rolling

0.7013

0.8079

0.1379

0.9974

0.1774

0.0001

0.9476

8

10

agg_bnd

ridge

0.6910

0.7960

0.1365

0.9694

0.1652

0.0001

0.9951

6

11

agg_bnd

kalman

0.6873

0.7880

0.1381

0.9936

0.1532

0.0001

0.9100

5

12

hyg_credit

static

0.4197

0.4741

0.0097

0.8018

0.1523

0.0001

1.0000

1

13

hyg_credit

rolling

0.4942

0.5236

0.0720

0.9729

0.8388

0.0004

0.8880

64

14

hyg_credit

ridge

0.4870

0.5163

0.0798

0.9339

0.6489

0.0003

0.8906

47

15

hyg_credit

kalman

0.4866

0.5234

0.0531

0.9651

0.2450

0.0001

0.9509

16

16

gdx_gold

static

0.2050

0.2059

-0.4645

0.3172

0.3950

0.0002

1.0000

1

17

gdx_gold

rolling

0.3674

0.3913

-0.2852

0.9591

1.4500

0.0007

0.7736

104

18

gdx_gold

ridge

0.3689

0.3923

-0.2580

0.9972

1.3368

0.0007

0.7808

96

19

gdx_gold

kalman

0.3685

0.3884

-0.2578

0.9668

1.2393

0.0006

0.8161

100

relationship

best_model

score

vol_red

es_red

maxdd_diff

cost_drag_ann

0

aapl_tech

ridge

0.7829

0.4397

0.4676

0.0575

0.0006

1

agg_bnd

static

0.8328

0.7153

0.8112

0.1456

0.0001

2

amd_semi

kalman

0.7801

0.2970

0.3185

-0.0112

0.0002

3

amzn_disc

rolling

0.7000

0.4059

0.4538

0.1401

0.0009

4

cost_def

ridge

0.7187

0.2857

0.2854

0.0843

0.0004

5

gdx_gold

kalman

0.4807

0.3685

0.3884

-0.2578

0.0006

6

hyg_credit

kalman

0.7479

0.4866

0.5234

0.0531

0.0001

7

msft_tech

kalman

0.8533

0.5283

0.5442

0.1731

0.0002

8

nvda_semi

ridge

0.7379

0.4613

0.4859

0.1700

0.0008

9

qqq_spy

ridge

0.7087

0.6491

0.6586

0.1652

0.0001

10

tlt_ief

rolling

0.6924

0.6078

0.5837

0.2272

0.0003

11

tsla_disc

kalman

0.6207

0.2350

0.2454

0.0927

0.0003

model

median_score

median_vol_red

median_es_red

median_cost_drag_ann

win_count

failure_count

1

ridge

0.6413

0.4505

0.4767

0.0005

4

0

2

rolling

0.6252

0.4513

0.4753

0.0008

2

0

0

kalman

0.4382

0.4294

0.4576

0.0001

5

0

3

static

0.1168

0.4084

0.4394

0.0001

1

1

relationship

best_vol_red

median_vol_red

best_es_red

best_maxdd_diff

median_cost_drag_ann

0

aapl_tech

0.4416

0.4213

0.4681

0.0575

0.0004

1

agg_bnd

0.7153

0.6962

0.8112

0.1456

0.0001

2

amd_semi

0.2970

0.2948

0.3219

0.0050

0.0007

3

amzn_disc

0.4059

0.3955

0.4538

0.1401

0.0004

4

cost_def

0.2857

0.2813

0.2854

0.0843

0.0002

5

gdx_gold

0.3689

0.3679

0.3923

-0.2578

0.0006

6

hyg_credit

0.4942

0.4868

0.5236

0.0798

0.0002

7

msft_tech

0.5283

0.5264

0.5473

0.1770

0.0002

8

nvda_semi

0.4613

0.4584

0.4859

0.1705

0.0005

9

qqq_spy

0.6491

0.6452

0.6592

0.1652

0.0001

10

tlt_ief

0.6078

0.5984

0.5837

0.2291

0.0002

11

tsla_disc

0.2408

0.2365

0.2485

0.1003

0.0011

The best-model table gives a balanced picture rather than one universal winner.

Ridge has the strongest median score, around 0.641, and wins four relationships: AAPL, COST, NVDA, and QQQ. This fits the theory. Ridge is especially useful when hedge variables are correlated and the target has a meaningful but noisy factor structure.

Kalman wins the most relationships, with five wins: AMD, GDX, HYG, MSFT, and TSLA. This doesn’t mean Kalman has the highest median score. It means it’s very useful in specific cases where smoother time variation beats rolling-window instability. Kalman also has the lowest median cost drag, which is economically important.

Rolling OLS wins AMZN and TLT. These are cases where more responsiveness helps enough to overcome higher turnover.

Static OLS only wins AGG/BND. That’s exactly the relationship where static OLS should win. AGG and BND are so structurally close that a dynamic model adds unnecessary movement.

The weakest relationship remains GDX/gold, even though Kalman wins it. The best score is only about 0.481, and the best max-drawdown difference is still negative. That’s a warning that the relationship is only partially hedgeable. We can reduce volatility, but we don’t fully control the worst path.

The best-minus-second score gap plot is useful because some wins are probably not robust. If the best model barely beats the second-best model, the choice is more about implementation preference. If the gap is large, the model choice is more meaningful.

10.1 Why the best model can differ by relationship

There’s no reason to expect one estimator to dominate every hedge problem. The underlying economics decide what kind of estimator is appropriate.

For replication relationships, like AGG/BND, the true beta is stable. Static OLS can win because dynamic models only add noise.

For factor-overlap relationships, like QQQ/SPY or NVDA/SMH+QQQ, ridge can work well because the hedge assets explain real common factors but can be correlated with each other.

For regime-sensitive relationships, like HYG credit or GDX gold miners, Kalman can help because exposures change across stress, recovery, inflation, and liquidity regimes.

For fast-changing relationships, rolling OLS can win because it responds faster than a conservative Kalman filter. That responsiveness costs more turnover, but sometimes the risk reduction is worth it.

This relationship-specific logic is why the scoring table is more useful than a single average metric. The goal isn’t to crown one method as universally best. The goal is to match the estimator to the hedge problem.

11) Residual spreads and econometric testing

The first part of we use hedge ratios for risk reduction. Now we use hedge ratios for residual trading.

The logic changes. For hedging, a residual can be useful simply because it has lower volatility than the target. For residual trading, the residual needs a stronger property: it should be mean-reverting. A low-volatility residual that trends away for years can still create a terrible trade.

For residual trading we switch from returns to log prices. For a target price \(P^y_t\) and hedge price \(P^x_t\), the price relationship is:

If \(s_t\) is stationary, deviations from its mean are temporary. A high \(s_t\) means the target is expensive relative to the hedge after adjusting for the estimated long-run relationship. A low \(s_t\) means the target is cheap relative to the hedge. This creates the logic for a mean-reversion trade.

If \(s_t\) has a unit root, the situation is different. A high spread can stay high, move higher, or reflect a permanent economic break. In that case, z-score trading becomes dangerous because the model keeps expecting a reversal that may never arrive.

So the tests in this section aren’t decorative. They decide whether a residual is even allowed to become a trading signal.

11.1 ADF, Engle-Granger, and half-life

The Augmented Dickey-Fuller test checks whether the spread behaves like a stationary process or like a drifting process with a unit root. A simple version of the test regression is:

The sign of \(\gamma\) matters. If \(s_{t-1}\) is high and \(\gamma < 0\), then the expected change \(\Delta s_t\) is negative, pulling the spread back down. If \(s_{t-1}\) is low, the same negative \(\gamma\) implies a positive expected move. This is mean reversion in regression form.

Engle-Granger cointegration is related, but the starting question is slightly different. It asks whether two non-stationary price series share a stable long-run relationship. First we estimate:

\[

y_t = \alpha + \beta x_t + s_t

\]

Then we test whether \(s_t\) is stationary. If \(y_t\) and \(x_t\) individually wander through time but their residual \(s_t\) mean-reverts, the pair is cointegrated. Financially, this means the two assets can drift, trend, and compound, but their relative valuation has an equilibrium pull.

Half-life translates the strength of mean reversion into trading language. We estimate:

\[

\Delta s_t = a + b s_{t-1} + e_t

\]

and approximate:

\[

\text{half-life} = -\frac{\ln 2}{b}, \quad b < 0

\]

If the half-life is 10 trading days, a spread shock is expected to decay by about half in roughly two weeks. If the half-life is 60 trading days, the same trade may require three months of patience. If the half-life is infinite or negative in the wrong way, the spread isn’t mean-reverting enough for this setup.

Here we require a half-life between 2 and 63 trading days. Very fast spreads are hard to trade after costs. Very slow spreads can trap capital and generate painful drawdowns before the expected reversion happens.

Show code

def statsmodels_tools():from statsmodels.tsa.stattools import adfuller, cointreturn adfuller, cointdef price_ols_beta(px, target, hedge): lp = np.log(px[[target, hedge]][px[[target, hedge]] >0]).dropna() out = pd.DataFrame(np.nan, index=px.index, columns=["alpha", "beta"])iflen(lp) < n_train:return out a, b = ols_fit(lp[target].iloc[:n_train], lp[[hedge]].iloc[:n_train]) out.loc[lp.index[n_train -1]:, ["alpha", "beta"]] = [a, b[0]]return outdef roll_price_beta(px, target, hedge): lp = np.log(px[[target, hedge]][px[[target, hedge]] >0]).dropna() out = pd.DataFrame(np.nan, index=px.index, columns=["alpha", "beta"])for i inrange(max(win, n_train) -1, len(lp)): sample = lp.iloc[i - win +1:i +1] a, b = ols_fit(sample[target], sample[[hedge]]) out.loc[lp.index[i], ["alpha", "beta"]] = [a, b[0]]return outdef kf_price_beta(px, target, hedge): lp = np.log(px[[target, hedge]][px[[target, hedge]] >0]).dropna() out = pd.DataFrame(np.nan, index=px.index, columns=["alpha", "beta"])iflen(lp) < n_train:return out a, b = ols_fit(lp[target].iloc[:n_train], lp[[hedge]].iloc[:n_train]) state = np.array([a, b[0]], dtype=float) h0 = np.column_stack([np.ones(n_train), lp[hedge].iloc[:n_train].to_numpy(float)]) resid = lp[target].iloc[:n_train].to_numpy(float) - h0 @ state obs_var =max(np.nanvar(resid, ddof=1), 1e-8) pcov = np.eye(2) *0.10 qcov = np.diag([1e-7, 1e-5]) out.loc[lp.index[n_train -1], ["alpha", "beta"]] = statefor i inrange(n_train, len(lp)): h = np.array([1.0, lp[hedge].iloc[i]]) pcov = pcov + qcov s =float(h @ pcov @ h.T + obs_var)if s >1e-12: k = (pcov @ h.T) / s state = state + k * (lp[target].iloc[i] - h @ state) pcov = (np.eye(2) - np.outer(k, h)) @ pcov out.loc[lp.index[i], ["alpha", "beta"]] = statereturn outdef log_spread(px, target, hedge, beta): lp = np.log(px[[target, hedge]][px[[target, hedge]] >0]) b = beta.reindex(lp.index).ffill()return (lp[target] - b["alpha"] - b["beta"] * lp[hedge]).replace([np.inf, -np.inf], np.nan)def eg_test(y, x): _, coint = statsmodels_tools() z = pd.concat([y, x], axis=1).dropna()returnfloat(coint(z.iloc[:, 0], z.iloc[:, 1])[1]) iflen(z) >=30else np.nandef adf_test(s): adfuller, _ = statsmodels_tools() x = pd.Series(s).dropna()try:returnfloat(adfuller(x, autolag="AIC")[1]) iflen(x) >=30else np.nanexceptException:return np.nandef half_life(s): x = pd.Series(s).dropna() z = pd.concat([x.diff(), x.shift(1)], axis=1).dropna()iflen(z) <30:return np.nan _, b = ols_fit(z.iloc[:, 0], z.iloc[:, [1]])return-np.log(2) / b[0] if b[0] <0else np.inf

11.2 Z-score trading rule

After a spread passes the econometric gate, we still need a trading rule. We use a rolling z-score:

\(\bar{s}_{t,126}\) is the 126-day rolling mean of the spread,

\(\sigma_{s,t,126}\) is the 126-day rolling standard deviation,

\(z_t\) measures how many recent standard deviations the spread is away from its local mean.

The rule is simple:

Condition | Position logic |

|,-|,-| | \(z_t > 2\) | target is rich relative to hedge, short the spread | | \(z_t < -2\) | target is cheap relative to hedge, long the spread | | \(|z_t| < 0.5\) | spread has mostly normalized, exit | | \(|z_t| > 3.5\) | move is too extreme, stop and cool down |

The stop rule is important. A very large z-score can mean opportunity, but it can also mean the relationship has broken. The cool-down period prevents the strategy from immediately re-entering after a large adverse move.

The signal is lagged by one day before trading, so we don’t use same-day information incorrectly. If the spread position is \(q_t \in \{-1,0,+1\}\), the daily strategy return is:

The term inside parentheses is the hedged residual return. The lagged \(q_{t-1}\) means the position was decided before today’s return was known. The cost term subtracts trading costs from position changes.

This is a residual mean-reversion trade, not a directional investment in the target. We’re betting on the relative relationship returning toward its recent equilibrium.

11.3 Dynamic residuals and a subtle econometric caveat

Dynamic hedge ratios make spreads more stationary, but this has to be interpreted carefully. If \(\beta_t\) changes through time, the spread is no longer the residual of one fixed long-run relationship. It’s the residual after allowing the relationship itself to move.

That can be useful for trading because markets aren’t static. Currency regimes, duration relationships, and sector betas change. But it also means an ADF test on a dynamic residual isn’t the same as proving classical cointegration under a fixed beta.

This is why the gate treats static and dynamic sources differently. Static spreads are expected to pass a stricter long-run relation test. Dynamic spreads are allowed if the resulting residual is stationary, tradable, and not created by excessive beta turnover.

The beta-turnover filter is important:

\[

\overline{|\Delta \beta|} \le 0.25

\]

Without this filter, a hyperactive beta could force almost any spread to look stationary by chasing the target too closely. We want adaptive residuals, not overfit residuals.

The residual gate table is strict, and that’s good. We don’t want every visually correlated pair to become a trading signal.

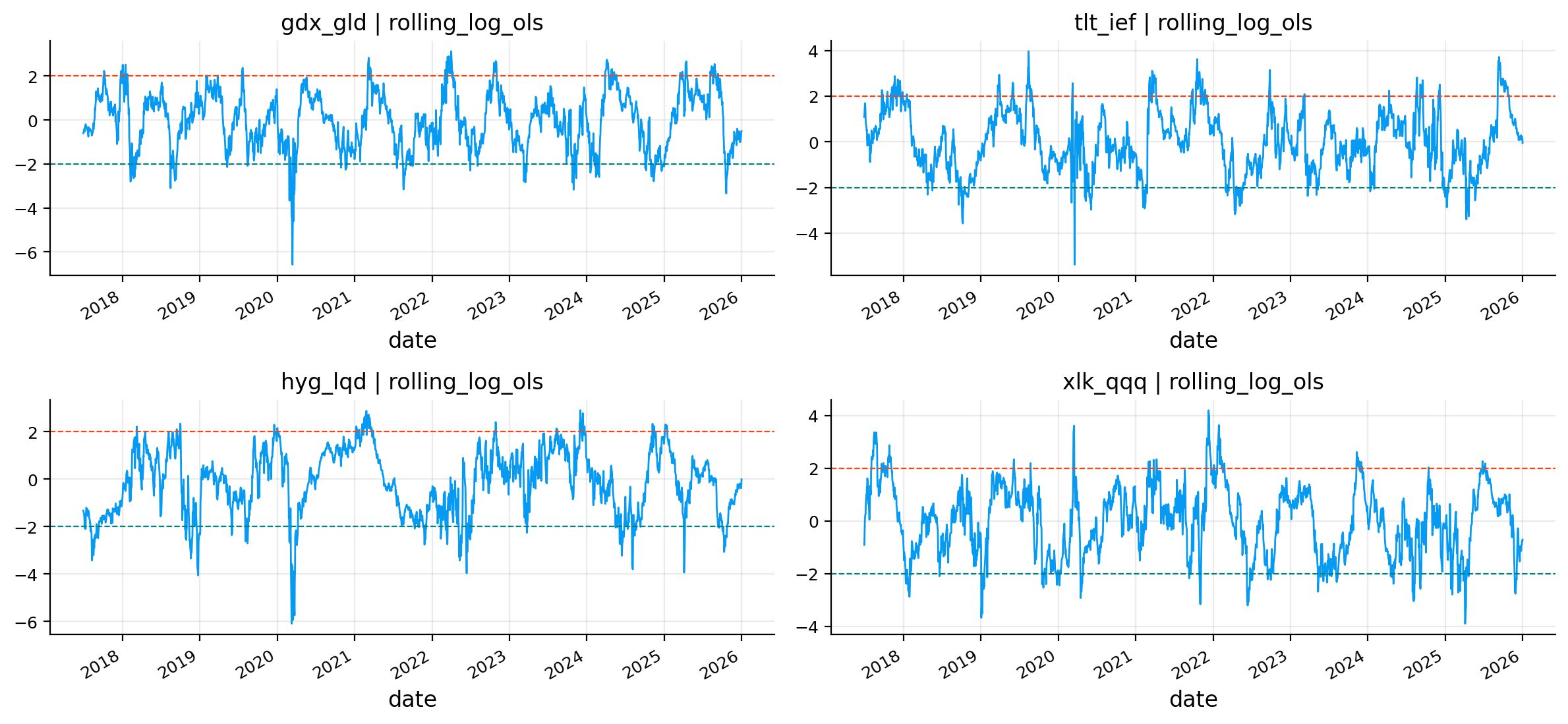

The static log-OLS spreads mostly fail because they don’t produce stationary residuals. For example, GDX/GLD static has ADF p-value around 0.9985 and infinite half-life, so it clearly fails. The spread can drift, and a z-score strategy would be dangerous.

The dynamic log-OLS spreads often pass because the changing beta absorbs slow structural drift. Eligible rolling spreads include:

GDX/GLD, with ADF p-value near zero and half-life around 18.8 days,

TLT/IEF, with ADF p-value around 0.0028 and half-life around 37.1 days,

HYG/LQD, with ADF p-value around 0.0028 and half-life around 42.5 days,

XLK/QQQ, with ADF p-value near zero and half-life around 30.4 days.

The Kalman log spreads often have very small half-lives, sometimes near 1 day. That sounds attractive at first, but it can be a warning. A very adaptive beta can absorb too much of the spread movement, leaving a residual that looks statistically stationary but has too little economically tradable structure. This is why the gate includes half-life, spread volatility, trades, cost, and beta turnover, not just ADF p-values.

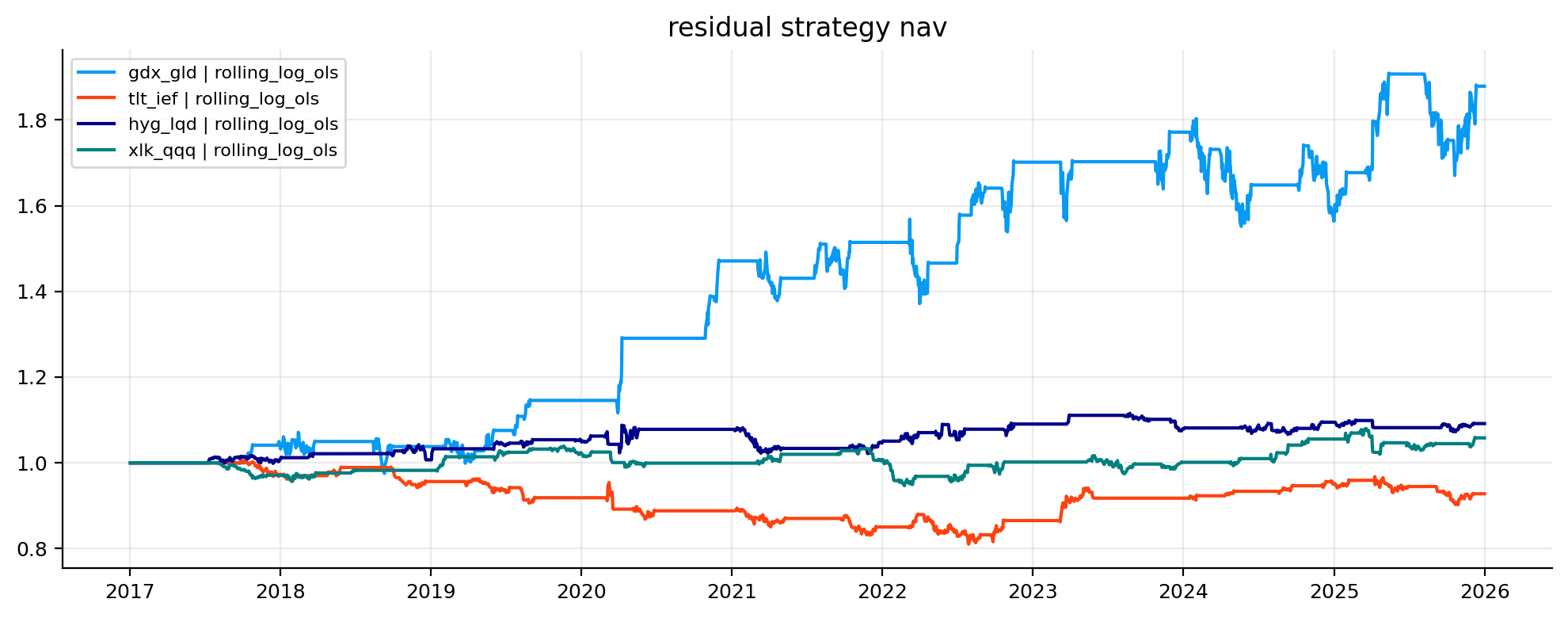

After the gates, we focus on selected rolling log-OLS residual strategies. The performance table reports trades, average holding period, net return, annualized volatility, Sharpe, max drawdown, and cost drag.

The strongest result is GDX/GLD rolling log-OLS. It has 28 trades, average holding period around 25 days, net return around 87.9%, annualized volatility around 11.8%, and Sharpe around 0.65. This is economically plausible. Gold miners versus gold often produce wide deviations because miners behave partly like equities and partly like leveraged gold exposure. When the spread is estimated dynamically, some deviations appear tradable.

HYG/LQD is modest but positive, with net return around 9.2% and Sharpe around 0.26. That fits the credit-spread intuition. High yield and investment-grade credit are related, but HYG has equity and default-risk components that can overshoot.

XLK/QQQ is also positive but small. That makes sense because XLK and QQQ overlap heavily. The spread is cleaner, but the opportunity set is narrower.

TLT/IEF passes the statistical gate but loses money, with net return around -7.2% and Sharpe around -0.15. This is a very useful failure. A spread can look statistically stationary and still be weak as a trading strategy. The residual might revert, but not fast enough after costs and signal timing, or the rate-regime shifts may create losses during the holding period.

The z-score plots show why residual trading needs discipline. The spread often spends long periods near zero, then moves sharply through entry levels. The strategy only trades when the deviation is large enough, and exits when the residual normalizes.

The residual NAV plot is even more informative. GDX/GLD dominates the selected residual strategies. It has step-like gains, which means the strategy earns most of its return during specific episodes rather than smoothly every month. HYG/LQD and XLK/QQQ grow slowly. TLT/IEF drifts below 1 and stays weak.

That pattern is realistic. Residual trading isn’t a stable coupon. It depends on episodic mispricing or temporary dislocation. The econometric tests help avoid terrible candidates, but they don’t guarantee positive P&L. The final test is still the backtested trade path after costs.

Show code

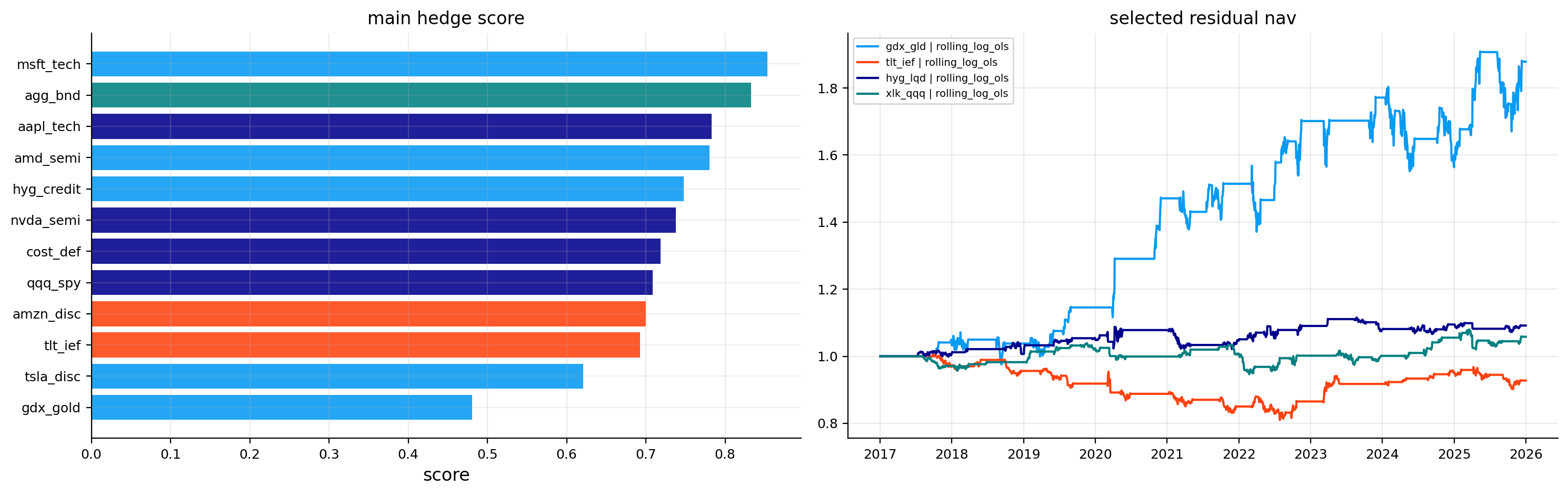

display(tab_best.round(4))display(tab_resid[tab_resid["key"].isin(keep_keys)].drop(columns="key").round(4))fig, axes = plt.subplots(1, 2, figsize=(15, 4.8))best_plot = tab_best.sort_values("score").copy()model_order =list(best_plot["best_model"].dropna().unique())model_colors = {m: colors[i %len(colors)] for i, m inenumerate(model_order)}axes[0].barh(best_plot["relationship"], best_plot["score"], color=[model_colors[m] for m in best_plot["best_model"]], alpha=0.88)axes[0].set_title("main hedge score")axes[0].set_xlabel("score")axes[0].grid(True, axis="x", alpha=0.25)for key in keep_keys[:6]: nav = resid_bt[key].net_values axes[1].plot(nav.index, nav / nav.iloc[0], label=key)axes[1].set_title("selected residual nav")axes[1].legend(fontsize=7)axes[1].grid(True, alpha=0.25)plt.tight_layout()plt.show()

relationship

best_model

score

vol_red

es_red

maxdd_diff

cost_drag_ann

0

aapl_tech

ridge

0.7829

0.4397

0.4676

0.0575

0.0006

1

agg_bnd

static

0.8328

0.7153

0.8112

0.1456

0.0001

2

amd_semi

kalman

0.7801

0.2970

0.3185

-0.0112

0.0002

3

amzn_disc

rolling

0.7000

0.4059

0.4538

0.1401

0.0009

4

cost_def

ridge

0.7187

0.2857

0.2854

0.0843

0.0004

5

gdx_gold

kalman

0.4807

0.3685

0.3884

-0.2578

0.0006

6

hyg_credit

kalman

0.7479

0.4866

0.5234

0.0531

0.0001

7

msft_tech

kalman

0.8533

0.5283

0.5442

0.1731

0.0002

8

nvda_semi

ridge

0.7379

0.4613

0.4859

0.1700

0.0008

9

qqq_spy

ridge

0.7087

0.6491

0.6586

0.1652

0.0001

10

tlt_ief

rolling

0.6924

0.6078

0.5837

0.2272

0.0003

11

tsla_disc

kalman

0.6207

0.2350

0.2454

0.0927

0.0003

pair

beta_source

trades

avg_hold

net_return

ann_vol

sharpe

maxdd

cost_drag

cost_drag_ann

4

gdx_gld

rolling_log_ols

28

25.1429

0.8787

0.1181

0.6535

-0.1395

0.1518

0.0086

7

tlt_ief

rolling_log_ols

26

32.1538

-0.0721

0.0469

-0.1545

-0.1949

0.0718

0.0083

10

hyg_lqd

rolling_log_ols

28

27.9643

0.0917

0.0408

0.2597

-0.0610

0.0520

0.0052

13

xlk_qqq

rolling_log_ols

30

24.6000