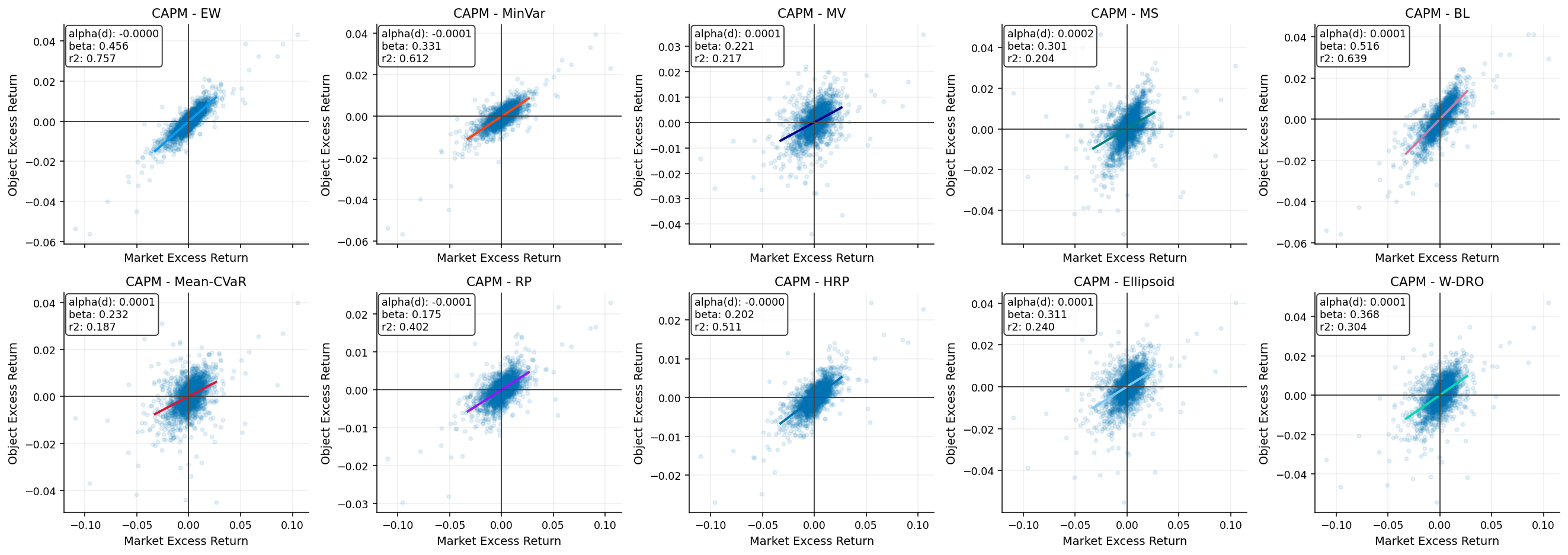

In this project we move from mean-variance portfolio construction into three families of portfolio models that care about risk in different ways:

Tail-risk models, where the objective is based on VaR/CVaR rather than variance.

Parity and hierarchical models, where the allocation is driven by risk contribution and correlation structure.

Robust models, where we admit that expected returns and distributions are uncertain and build portfolios that survive estimation error.

Wasserstein distributionally robust optimization, where the model protects against nearby alternative return distributions rather than trusting one sample.

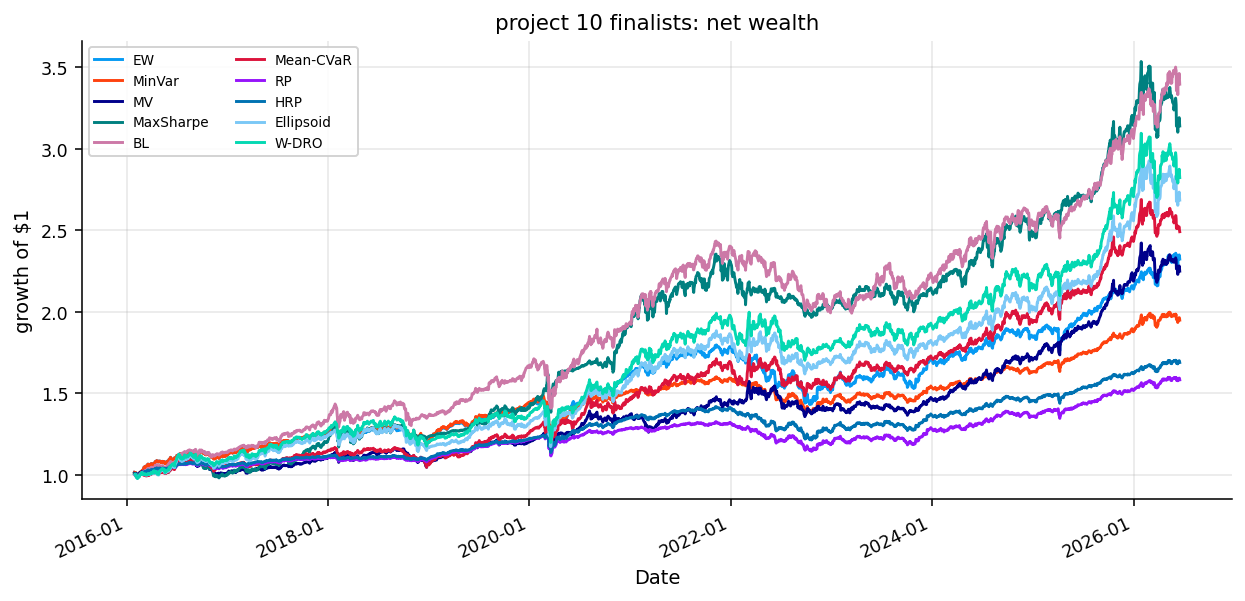

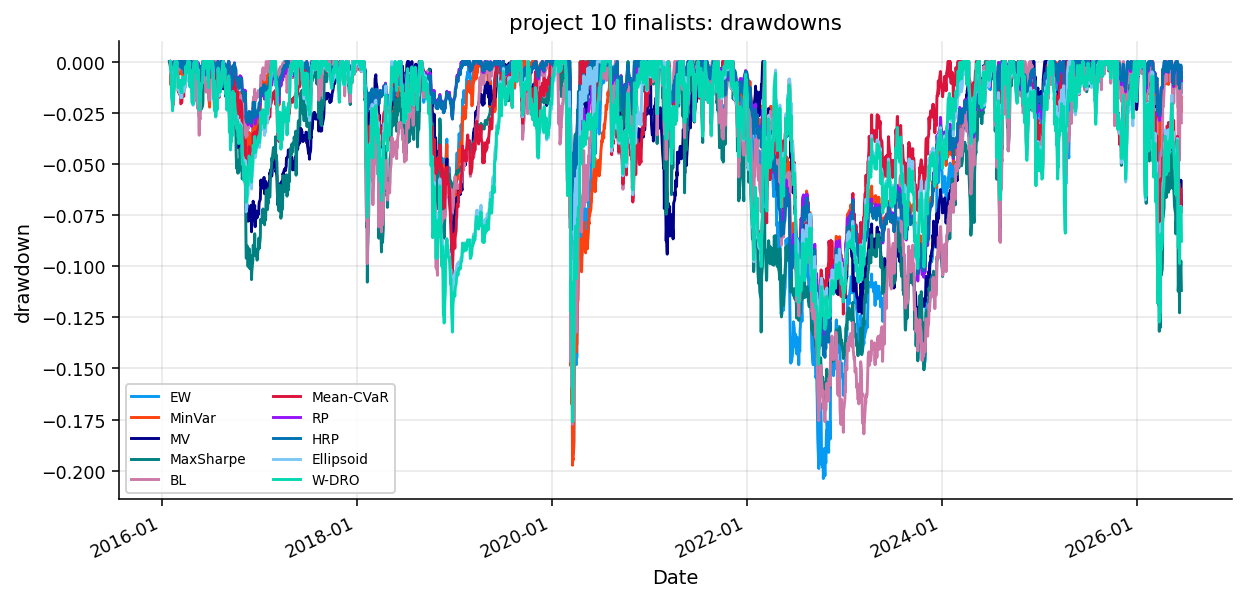

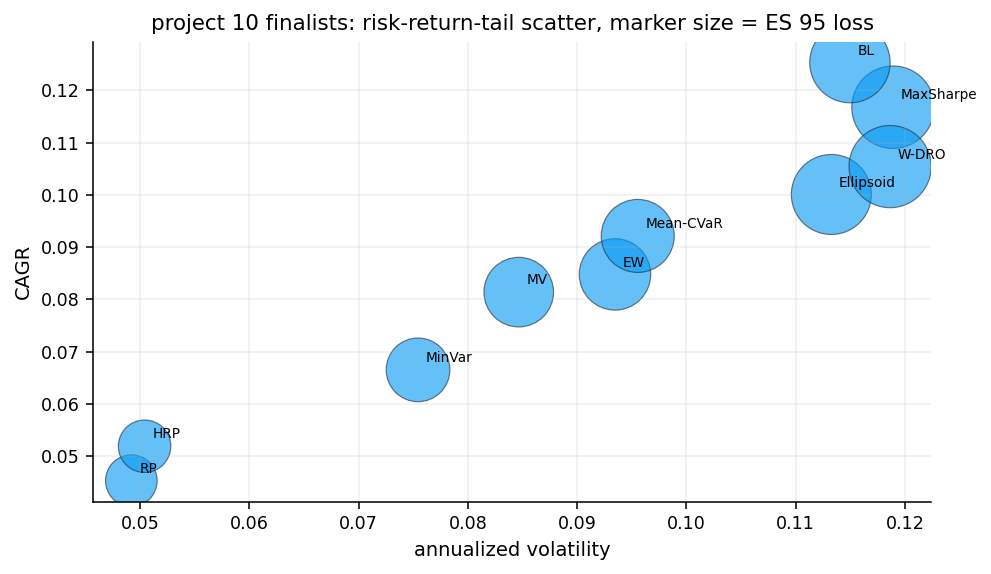

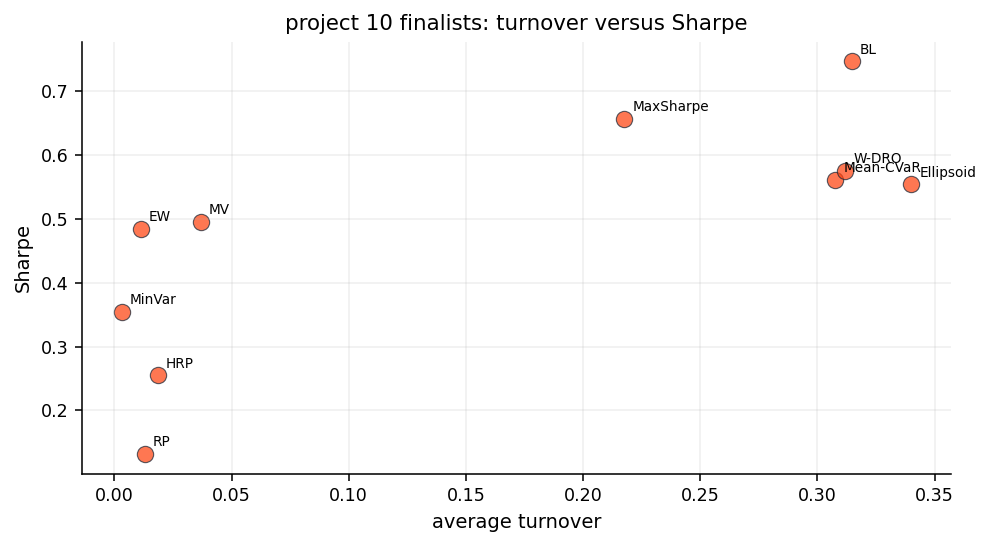

Full model comparison, where return, volatility, drawdown, expected shortfall, turnover, concentration, and stress behavior are compared together.

A secondary sector ETF application, where we repeat the same model families on a more equity-like universe using the library workflow.

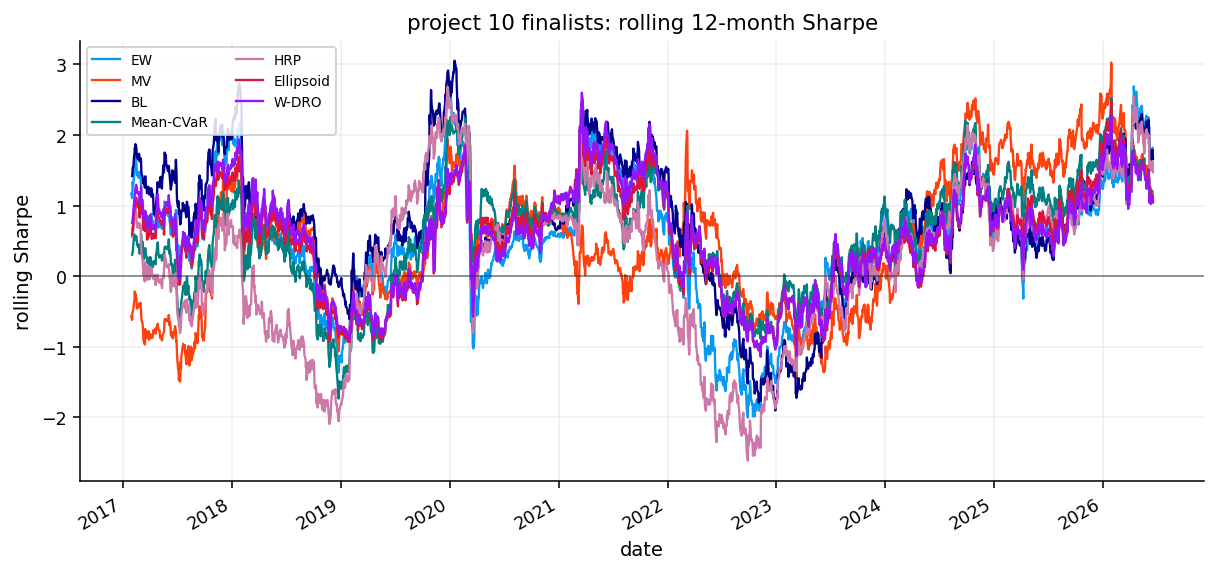

The important idea is that portfolio optimization isn’t one problem. It’s a set of related problems with different definitions of risk. Mean-variance says risk is covariance. CVaR says risk is the average loss in the worst tail. Risk parity says risk is the amount each asset contributes to total portfolio volatility. Robust optimization says risk also comes from being wrong about the inputs. This project puts those definitions next to each other and lets the backtest show what each one buys and what it costs.

A useful way to read the whole project is to keep four objects separate:

Object

Symbol

What changes across models

Expected return estimate

\(\hat{\mu}\)

ignored, used directly, shrunk, or penalized

Covariance estimate

\(\hat{\Sigma}\)

used for variance, risk contributions, clustering, and robust norms

Scenario matrix

\(R\)

used directly by CVaR and indirectly by covariance/mean estimates

Constraint set

\(\mathcal{C}\)

keeps all models long-only, fully invested, and capped

Most portfolio formulas look like they are optimizing weights, but they are really optimizing a translation of beliefs into weights. The belief can be “the mean estimate is useful”, “the worst 5% scenarios matter more than variance”, “each sleeve should contribute equal risk”, or “the estimates are unreliable and need an uncertainty penalty”.

That distinction helps later when two models hold similar assets for different reasons. For example, Mean-CVaR and Wasserstein DRMV can both like GLD or DBC in a certain window. Mean-CVaR may like them because they help satisfy the historical tail-loss budget. Wasserstein DRMV may like them because their robust return still survives the distributional penalty. The weights can look similar, but the explanation behind those weights is different.

We also need to keep risk measurement separate from portfolio construction. A model can optimize CVaR and then still be evaluated by Sharpe, Calmar, drawdown, turnover, and expected shortfall. The objective tells us what the model was trying to do. The final report tells us whether that objective produced a useful portfolio under realistic out-of-sample testing.

1) The Portfolio Problem After Mean-Variance

We already used mean-variance models earlier, so we don’t need to rebuild that whole theory again. The useful starting point here is the weakness that kept showing up: most portfolio models are extremely sensitive to the input estimates.

A portfolio optimizer receives three kinds of information:

where \(\hat{\mu}\) is the estimated expected return vector, \(\hat{\Sigma}\) is the estimated covariance matrix, and \(\mathcal{C}\) is the constraint set, such as long-only weights, full investment, and max-weight caps. If those inputs were known perfectly, the optimization problem would be clean. In real markets, they aren’t known. We estimate them from a finite rolling sample, and that makes every model partly a statistical model before it becomes a portfolio model.

The current project keeps the repeated data and baseline machinery short and spends the detail on the new question:

If variance and raw expected returns aren’t enough, how else can we define a portfolio that is safer, more balanced, or more robust?

We work with the same cross-asset ETF universe used in the previous portfolio projects. The data can be reproduced from the core_cross_asset_etfs folder inside the repository’s data layer. That folder contains the source notes and script workflow for rebuilding the file used by this project. We also repeat the workflow on sector ETFs later, using the sector_etfs data folder.

The baselines are also reused. Equal Weight, MinVar, MV, and MaxSharpe come from the same model family developed in Project 2, and Learned-Confidence BL comes from Project 6. Here they serve as reference portfolios, not as the main teaching topic.

We start by loading the project environment, imports, plotting settings, and the cross-asset ETF panel. There isn’t much theory in this cell. The important thing is that the later models depend on cvxpy for convex programs, SciPy clustering for hierarchical allocation, and the quantfinlab portfolio/risk-reporting utilities for consistent backtesting.

The repeated implementation convention is the same as earlier:

\[

r_{t,i} = \frac{P_{t,i}}{P_{t-1,i}} - 1

\]

where \(P_{t,i}\) is the adjusted close price of asset \(i\) at day \(t\), and \(r_{t,i}\) is the simple daily return. We stack the daily returns into a matrix

\[

R_t \in \mathbb{R}^{T \times N}

\]

where \(T\) is the rolling estimation window and \(N\) is the number of assets. Each row is one historical day and each column is one ETF.

For this project, the matrix matters more than in a simple mean-variance backtest because different models read it differently:

CVaR models read scenario losses from the rows of \(R_t\).

Parity models read covariance structure from \(\hat{\Sigma}_t\).

Robust models read both estimated means and estimation uncertainty.

Wasserstein DRO treats the empirical sample as only one possible distribution inside a neighborhood of plausible distributions.

After that compression, the optimizer no longer sees individual crisis days. It only sees average return and covariance. CVaR works differently. It keeps the scenario-level losses:

\[

\ell_s(w)=-r_s^\top w,\qquad s=1,\ldots,T

\]

That means one very bad historical day can directly enter the optimization if it belongs to the worst tail. This is why CVaR is more connected to realized stress scenarios than variance. Variance smooths bad days into a second moment. CVaR identifies the worst days and averages their losses.

For example, if two portfolios have the same volatility but one has many small losses and the other has rare crash losses, variance can treat them as similar. CVaR will usually prefer the first one because its worst 5% outcomes are less severe. This is exactly the kind of distinction that matters when we compare Mean-CVaR against MV and MaxSharpe later.

Show code

start_date ="2013-01-01"assets = ["SPY", "QQQ", "IWM", "EFA", "EEM", "TLT", "IEF", "SHY", "AGG", "LQD", "HYG", "GLD", "VNQ", "DBC"]signal_only_assets = ["UUP"] if"UUP"in close_all.columns else []close_after_start = close_all.loc[pd.Timestamp(start_date):].copy()missing_assets = [ticker for ticker in assets if ticker notin close_after_start.columns]if missing_assets:raiseValueError(f"missing required investable ETF columns: {missing_assets}")first_all_valid = close_after_start[assets].dropna(how="any").index.min()if pd.isna(first_all_valid):raiseValueError("no date where all investable ETFs have adjusted close data")close = close_after_start.loc[first_all_valid:, assets].ffill(limit=3).dropna(how="any")returns = prices_to_returns(close, kind="simple").replace([np.inf, -np.inf], np.nan).dropna(how="all").fillna(0.0)close = close.reindex(returns.index).ffill(limit=3)signal_tickers =list(dict.fromkeys(assets + signal_only_assets))signal_close = close_after_start.loc[first_all_valid:, signal_tickers].ffill(limit=3).reindex(returns.index).ffill(limit=3)signal_returns = prices_to_returns(signal_close, kind="simple").replace([np.inf, -np.inf], np.nan).reindex(returns.index).fillna(0.0)

The loaded close table contains 6,906 rows and 19 columns from 1999-01-04 to 2026-06-17. We don’t use the full historical range because the investable ETF universe needs aligned coverage. After the 2013 start filter and the all-valid ETF alignment, the investable return panel contains 3,384 daily observations from 2013-01-03 to 2026-06-17.

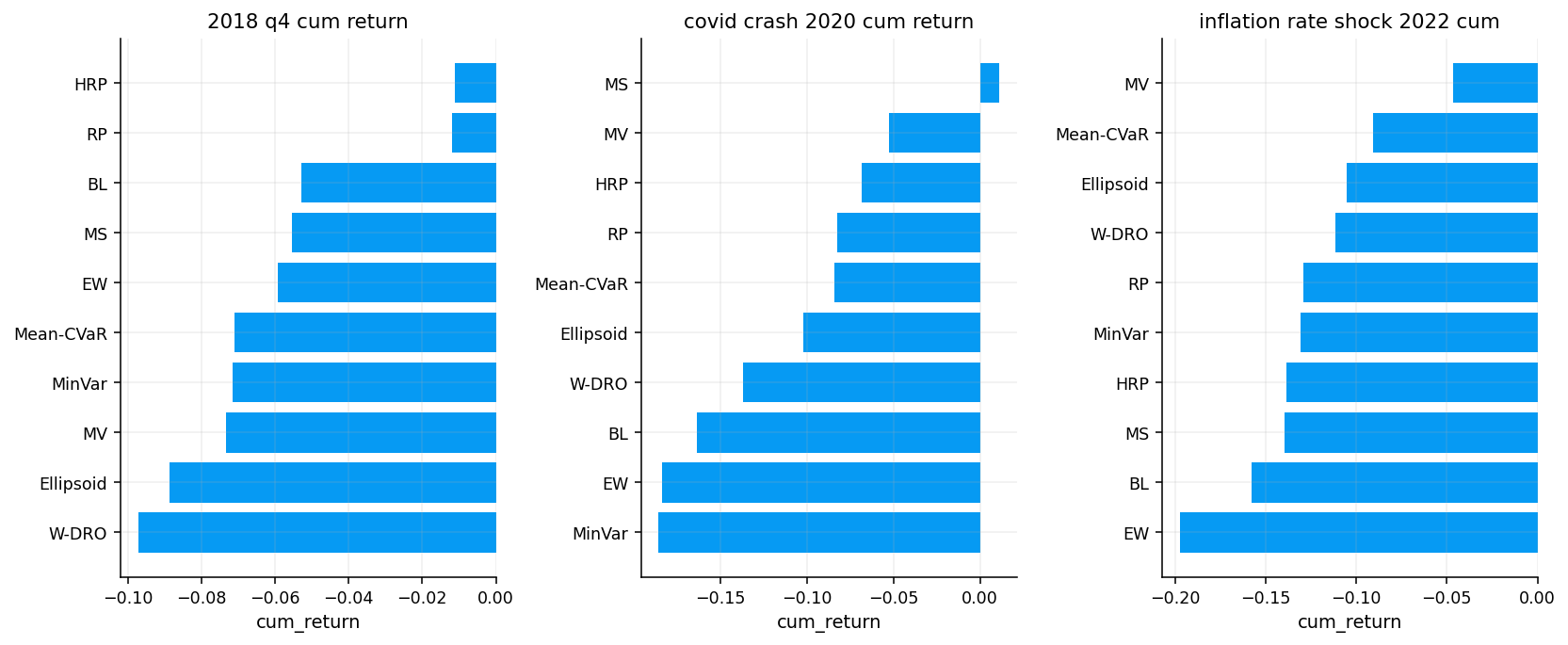

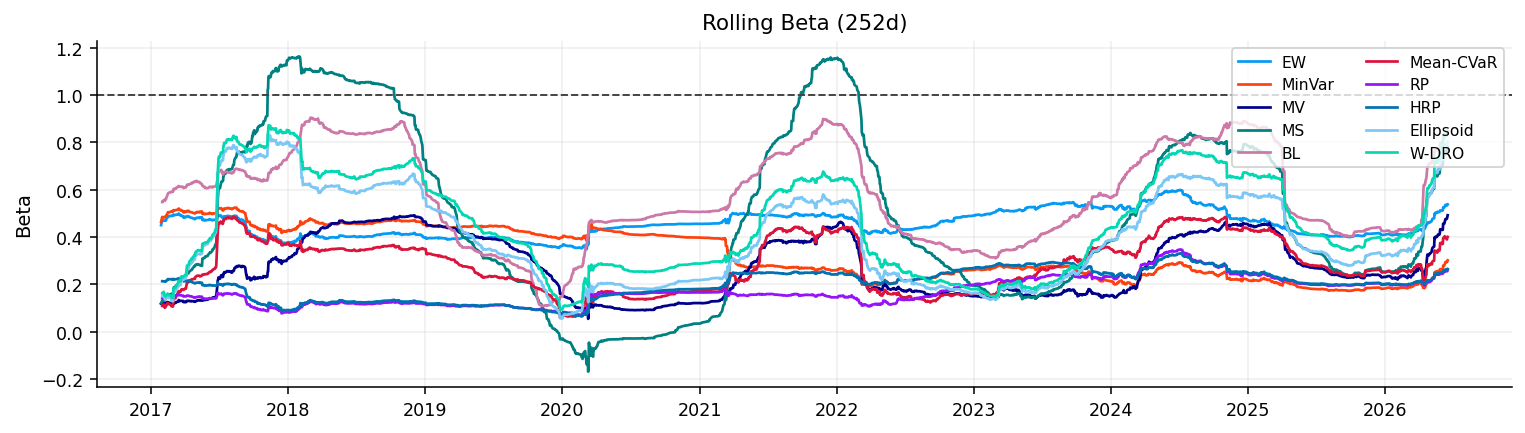

This is a clean setup for a portfolio model comparison. The panel has enough history to estimate multi-year covariance matrices, it spans calm markets, the COVID crash, the 2022 inflation/rate shock, and the 2023-2026 growth rebound. Those environments are important because the new models aren’t meant to look good only in average conditions. CVaR and robust models are especially useful when the average market environment is no longer representative of the next month.

The signal-only asset UUP is included for the Black-Litterman baseline, but the investable universe has 14 ETFs. The missing-value check is also clean: after alignment, there are zero missing values in the investable return panel. That matters because CVaR optimization uses historical scenarios directly. A missing value inside a scenario matrix would change the tail set and could distort which days count as bad outcomes.

2) Universe, Rebalancing, and Constraints

The tradable universe stays the same as the earlier cross-asset portfolio work, but the way constraints interact with the new models deserves attention.

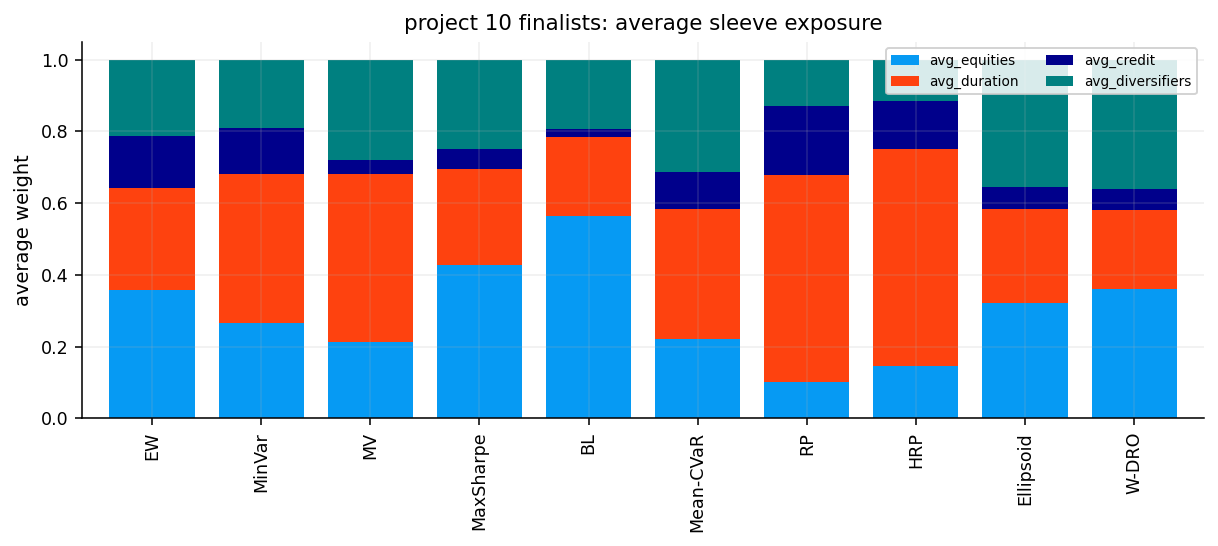

We use 14 ETFs across four sleeves:

Sleeve

Assets

Main risk carried

Equities

SPY, QQQ, IWM, EFA, EEM

equity beta, growth/cyclicality, global risk appetite

gold, real estate, commodities, inflation/real-asset exposure

We don’t re-explain every ETF here because the data and economic role of this universe were already discussed in the earlier portfolio notebooks. For Project 10, the key point is how these sleeves behave under different risk definitions.

A variance-focused model may prefer SHY because it has very low volatility. A CVaR model may prefer assets that avoid large negative tail scenarios. A risk parity model may give large weight to low-volatility bonds because they need more capital to contribute equal volatility risk. A robust model may penalize assets with high expected-return uncertainty, even when their point forecast looks attractive.

The constraint set is:

\[

\mathbf{1}^\top w = 1

\]

\[

0 \le w_i \le \bar{w}_i

\]

where \(w_i\) is the weight of asset \(i\), \(\mathbf{1}^\top w=1\) means the portfolio is fully invested, and \(\bar{w}_i\) is the asset-specific cap. These caps are essential. Without caps, many of the optimizers would collapse into one or two assets because the sample makes some assets look much better or much safer than the others.

rebalance_dates = make_rebalance_dates(returns.index, freq=rebal_freq, min_history_days=max(cov_lookback, mu_lookback, 756))fixed_universe_by_date = {pd.Timestamp(dt): {"tickers": list(assets), "avg_dollar_volume": pd.Series(1.0, index=assets)} for dt in rebalance_dates}universe_table = pd.DataFrame({"asset": assets, "sleeve": [sleeve_map.get(asset, "other") for asset in assets], "asset_cap": asset_caps.reindex(assets).values})benchmark_table = pd.DataFrame({"asset": assets, "sleeve": [sleeve_map.get(asset, "other") for asset in assets], "benchmark_weight": benchmark_w.reindex(assets).values, "asset_cap": asset_caps.reindex(assets).values})rebalance_summary = pd.DataFrame([{"count": len(rebalance_dates), "first_rebalance": rebalance_dates[0], "last_rebalance": rebalance_dates[-1], "frequency": rebal_freq, "cov_lookback": cov_lookback, "mu_lookback": mu_lookback}])display(universe_table)display(benchmark_table.round(4))display(rebalance_summary)

asset

sleeve

asset_cap

0

SPY

equities

0.40

1

QQQ

equities

0.40

2

IWM

equities

0.35

3

EFA

equities

0.35

4

EEM

equities

0.35

5

TLT

duration

0.25

6

IEF

duration

0.25

7

SHY

duration

0.15

8

AGG

duration

0.30

9

LQD

credit

0.25

10

HYG

credit

0.15

11

GLD

diversifiers

0.30

12

VNQ

diversifiers

0.30

13

DBC

diversifiers

0.25

asset

sleeve

benchmark_weight

asset_cap

0

SPY

equities

0.2264

0.40

1

QQQ

equities

0.0943

0.40

2

IWM

equities

0.0566

0.35

3

EFA

equities

0.1132

0.35

4

EEM

equities

0.0566

0.35

5

TLT

duration

0.0943

0.25

6

IEF

duration

0.0755

0.25

7

SHY

duration

0.0377

0.15

8

AGG

duration

0.0566

0.30

9

LQD

credit

0.0377

0.25

10

HYG

credit

0.0283

0.15

11

GLD

diversifiers

0.0472

0.30

12

VNQ

diversifiers

0.0377

0.30

13

DBC

diversifiers

0.0377

0.25

count

first_rebalance

last_rebalance

frequency

cov_lookback

mu_lookback

0

126

2016-01-29

2026-06-17

ME

756

252

The universe table confirms the investable set and caps. SPY and QQQ can reach 40%, several equity and diversifier ETFs have 30-35% caps, and safer bond-like instruments have lower or moderate caps depending on their role. SHY is capped at 15%, which is important because a pure variance minimizer would otherwise lean too heavily into it.

The benchmark table gives the strategic reference weights. The largest neutral allocations are SPY at about 22.64%, EFA at 11.32%, QQQ and TLT at 9.43%, and IEF at 7.55%. This benchmark isn’t the object being optimized in the new models, but it gives useful context for later comparisons. When we see a model hold 40% SHY, 40% DBC, or 40% EEM, we can compare that to the much more balanced benchmark and ask whether the model’s risk definition is forcing a concentrated decision.

The rebalance setup gives 126 monthly rebalance dates from 2016-01-29 to 2026-06-17. We start in 2016 because the covariance lookback is 756 trading days, about three years. This is a good compromise: the window is long enough to estimate a stable covariance matrix and tail distribution, but short enough to adapt after large market structure changes.

We then rebuild the baseline grid. This is deliberately short because these models were already taught earlier. The grid searches through covariance and expected-return combinations, then selects:

Equal Weight as the simplest fully diversified reference.

MinVar as the variance-only defensive benchmark.

MV as the standard mean-variance benchmark.

MaxSharpe as the return-seeking frontier benchmark.

The selected versions are:

Role

Selected model

Equal weight

EW

Minimum variance

MinVar with OAS covariance

Mean-variance

MV with Ledoit-Wolf covariance and Bayes-Stein expected returns

MaxSharpe

MaxSharpe with sample covariance and Bayes-Stein Momentum expected returns

The point isn’t to teach these again. The point is to keep them in the comparison because the new models need a serious benchmark. If a CVaR or robust model can’t beat a simple MaxSharpe or BL baseline on a useful metric, then the more complex objective needs to justify itself through lower drawdowns, lower tail loss, lower turnover, or better stability.

def ordered_strategy_table(table): cols = ["Sharpe", "Max Drawdown", "Turnover", "CAGR"] ascending = [False, False, True, False] present = [col for col in cols if col in table.columns] asc = [ascending[cols.index(col)] for col in present]return table.replace([np.inf, -np.inf], np.nan).sort_values(present, ascending=asc)benchmark_summary = walkforward_grid.results.copy()benchmark_summary_ranked = ordered_strategy_table(benchmark_summary)

The baseline table already gives a useful warning. MaxSharpe has the highest baseline CAGR at 11.68% and Sharpe at 0.6553, but it also has high turnover of 21.77% per month and low effective diversification with average effective \(N\) around 3.20. That means it gets its performance from concentrated bets that move around.

MV with Ledoit-Wolf and Bayes-Stein is much more conservative: CAGR 8.14%, volatility 8.47%, Sharpe 0.4949, and a strong max drawdown of -13.78%. MinVar has even lower volatility but lower return. Equal Weight is stable and diversified, but its max drawdown is the worst among the baseline set at -20.38%.

So the baseline problem is already visible:

MaxSharpe gives strong performance, but it concentrates and trades.

MinVar controls volatility, but gives up too much return.

MV is balanced, but still depends on a fragile expected-return estimate.

Equal Weight is stable by construction, but doesn’t react to changing risk.

The new models will mostly try to control this exact tradeoff.

3) Learned-Confidence Black-Litterman as a Strong Reference

We rebuild the Learned-Confidence BL strategy from Project 6 and include it as a reference. We don’t re-teach the full Black-Litterman posterior here, but it helps to remember what BL contributes to the comparison.

The BL model starts from an equilibrium prior, generates active relative views, learns view confidence from realized payoff history, and converts the posterior return vector into a constrained portfolio. In this project, it gives us a strong “active but structured” benchmark.

The reason BL is important here is that the new models are not only competing against classical MV. They’re competing against a model that already tries to solve one of MV’s biggest weaknesses: the instability of raw expected returns. If a robust optimizer beats simple MV but loses to BL, that still tells us something. It means robustness helps relative to naive estimation, but perhaps not relative to a structured Bayesian view process.

The BL rebuild generates 544 candidate view rows, 538 selected view rows, 538 confidence rows, and 125 posterior rows. That confirms the BL baseline is active through almost the full monthly period.

It also improves the drawdown relative to the strategic benchmark: -18.20% versus -23.01%. Its turnover is high at 31.47% average monthly turnover, which is the cost of running active monthly views. The effective number of positions is about 5.20, so it is diversified enough to avoid a one-asset bet, but still meaningfully concentrated relative to Equal Weight.

This sets the bar high. A new model doesn’t need to beat BL on every metric, but it has to show a clear role. For example:

CVaR models can justify themselves if they reduce expected shortfall or drawdown.

Risk parity can justify itself if it gives a smoother defensive allocation.

Robust models can justify themselves if they preserve return while reducing dependence on fragile forecasts.

Wasserstein DRO can justify itself if it behaves like a less brittle version of aggressive mean-variance.

That is the comparison logic we use for the rest of the project.

Show code

results = {}results["Equal Weight"] = walkforward_grid.backtests[grid_equal_weight_name]results[best_minvar_name] = walkforward_grid.backtests[best_minvar_name]results[best_mv_name] = walkforward_grid.backtests[best_mv_name]results[best_maxsharpe_name] = walkforward_grid.backtests[best_maxsharpe_name]results["Learned-Confidence BL"] = learned_bl_resultdef compact_result_table(result_map): out = selection.build_strategy_summary(result_map, rf_daily=risk_free_daily, annualization=annualization).copy() out = out.rename(columns={"CAGR": "cagr", "Vol": "ann_vol", "Sharpe": "sharpe", "Sortino": "sortino", "Max Drawdown": "max_drawdown", "Calmar": "calmar", "Turnover": "avg_turnover", "Total Turnover": "total_turnover", "Cost Drag": "cost_drag", "Effective N": "avg_effective_n"}) rows = []for name, result in result_map.items(): weights = result.weights.reindex(columns=assets).fillna(0.0) ifnot result.weights.empty else pd.DataFrame(columns=assets) rows.append({"model": name, "avg_max_weight": float(attribution.max_weight(weights).mean()) ifnot weights.empty else np.nan}) extra = pd.DataFrame(rows).set_index("model") if rows else pd.DataFrame()ifnot extra.empty: out = out.join(extra, how="left") cols = ["cagr", "ann_vol", "sharpe", "sortino", "max_drawdown", "calmar", "avg_turnover", "total_turnover", "cost_drag", "avg_effective_n", "avg_max_weight"]return out[[c for c in cols if c in out.columns]]benchmark_table_compact = compact_result_table(results)display(benchmark_table_compact.round(4))

cagr

ann_vol

sharpe

sortino

max_drawdown

calmar

avg_turnover

total_turnover

cost_drag

avg_effective_n

avg_max_weight

Strategy

Equal Weight

0.0848

0.0935

0.4842

0.5934

-0.2038

0.4159

0.0114

1.4385

0.0010

14.0000

0.0714

MinVar (OAS)

0.0665

0.0754

0.3543

0.4044

-0.1973

0.3370

0.0031

0.3897

0.0003

9.1680

0.2394

MV (LedoitWolf, BayesStein)

0.0814

0.0847

0.4949

0.6049

-0.1378

0.5904

0.0369

4.6481

0.0028

5.0557

0.3212

MaxSharpe (Sample, BayesSteinMomentum)

0.1168

0.1189

0.6553

0.8164

-0.1653

0.7065

0.2177

27.4264

0.0158

3.2046

0.3897

Learned-Confidence BL

0.1253

0.1150

0.7458

0.9287

-0.1820

0.6888

0.3147

39.3320

0.0226

5.2021

0.2724

4) Shared Optimization Infrastructure

Before the new models start, we define a few shared optimization utilities. This part isn’t the center of the project, but it matters because the objective functions below are only useful if the optimizer returns valid portfolios.

The constraints are enforced repeatedly:

\[

\sum_{i=1}^{N} w_i = 1

\]

\[

w_i \ge 0

\]

\[

w_i \le \bar{w}_i

\]

where \(\bar{w}_i\) is the cap for asset \(i\). We also clean weights after optimization so that tiny numerical negatives are clipped, weights are renormalized, and cap violations are corrected.

The PSD square-root routine also matters. Several models need a matrix square root of a covariance-like matrix:

\[

A^{1/2}(A^{1/2})^\top \approx A

\]

For example, portfolio volatility can be written as:

That norm form is useful in conic optimization, robust optimization, and Wasserstein DRO. Since empirical covariance matrices can have tiny numerical eigenvalue problems, the implementation symmetrizes the matrix and floors small eigenvalues before taking the square root. This doesn’t change the model’s economic idea. It prevents the numerical solver from failing because of floating-point noise.

Show code

def psd_sqrt(mat, eps=1e-10): arr = np.asarray(mat, dtype=float) arr =0.5* (arr + arr.T) vals, vecs = np.linalg.eigh(arr) vals = np.maximum(vals, eps) out = (vecs * np.sqrt(vals)) @ vecs.Treturn0.5* (out + out.T)def cap_array(index, max_weight=None): idx = pd.Index(index)if max_weight isNone:return pd.Series(float(w_max), index=idx, dtype=float)ifisinstance(max_weight, (pd.Series, dict)): cap = pd.Series(max_weight, dtype=float).reindex(idx).fillna(w_max)else: arr = np.asarray(max_weight, dtype=float).reshape(-1) cap = pd.Series(arr, index=idx, dtype=float) if arr.size ==len(idx) else pd.Series(float(max_weight), index=idx, dtype=float) cap = cap.replace([np.inf, -np.inf], np.nan).fillna(w_max).clip(lower=0.0)iffloat(cap.sum()) <1.0-1e-10: cap = pd.Series(max(float(w_max), 1.0/len(idx)), index=idx, dtype=float)return capdef clean_weight_array(values, index, max_weight=None): idx = pd.Index(index) caps = cap_array(idx, max_weight) w = pd.Series(values, index=idx, dtype=float).replace([np.inf, -np.inf], np.nan).fillna(0.0).clip(lower=0.0) w = np.minimum(w, caps)iffloat(w.sum()) <=1e-12: w = pd.Series(1.0/len(idx), index=idx, dtype=float)else: w = w /float(w.sum())for _ inrange(50): over = w > caps +1e-12ifnotbool(over.any()):break extra =float((w[over] - caps[over]).sum()) w[over] = caps[over] room = (caps[~over] - w[~over]).clip(lower=0.0)iffloat(room.sum()) <=1e-12:break w.loc[room.index] = w.loc[room.index] + extra * room /float(room.sum()) w = np.minimum(w.clip(lower=0.0), caps)return w /float(w.sum()) iffloat(w.sum()) >1e-12else pd.Series(1.0/len(idx), index=idx, dtype=float)

Show code

def solve_cvx_problem(problem): installed =set(cp.installed_solvers())for solver in ["CLARABEL", "ECOS", "SCS"]:if solver notin installed:continuetry: problem.solve(solver=solver, verbose=False)if problem.status in ["optimal", "optimal_inaccurate"]:return problem.statusexceptException:passreturnstr(problem.status)def backtest_weight_frame(name, weights):return run_many_weights_backtests({name: weights}, returns=returns[assets], cost_bps=cost_bps, rf_daily=risk_free_daily, w_min=w_min, w_max=w_max, long_only=True, normalize=True, weight_timing="next_close")[name]def make_weight_frame_from_func(name, weight_func): usable_dates = [pd.Timestamp(dt) for dt in walkforward_grid.metadata["rebalance_dates"] if pd.Timestamp(dt) in walkforward_grid.cache][:-1] rows = [] fallback_count =0 prev_w = pd.Series(1.0/len(assets), index=assets, dtype=float)for dt in usable_dates: state = walkforward_grid.cache[pd.Timestamp(dt)] tickers =list(state.get("tickers", assets)) raw = weight_func(pd.Timestamp(dt), state, prev_w.reindex(tickers).fillna(0.0))if raw isNone: fallback_count +=1 raw = prev_w.reindex(tickers).fillna(0.0) w = clean_weight_array(raw, tickers).reindex(assets).fillna(0.0) w = clean_weight_array(w, assets) rows.append(w.rename(pd.Timestamp(dt))) prev_w = w local_fallback_counts[name] = fallback_countreturn pd.DataFrame(rows).reindex(columns=assets).fillna(0.0)local_fallback_counts = {}model_rebalance_dates = [pd.Timestamp(dt) for dt in walkforward_grid.metadata["rebalance_dates"] if pd.Timestamp(dt) in walkforward_grid.cache][:-1]first_cache_date = model_rebalance_dates[0]display(pd.Series(list(walkforward_grid.cache[first_cache_date].keys()), name=str(first_cache_date.date())).to_frame("cache_keys"))

cache_keys

0

tickers

1

R_cov

2

R_mu

3

mu_raw_map

4

mu_ann_map

5

mu_info_map

6

cov_ann_map

7

avg_dollar_volume

The cache-key output shows the walk-forward engine stores the pieces every model needs at each rebalance date:

tickers, the current asset universe.

R_cov, the rolling return matrix used for covariance and scenario-risk estimation.

R_mu, the rolling return matrix used for expected-return estimation.

mu_ann_map, expected-return estimates under different models.

cov_ann_map, covariance estimates under different estimators.

avg_dollar_volume, retained from the general selection system.

This is important because all Project 10 models run on the same walk-forward information set. A CVaR model doesn’t get future returns. A robust model doesn’t get future realized volatility. A risk-parity model doesn’t get to know which period is coming next. Each rebalance sees only the historical window up to that date, produces weights, and then those weights are tested out-of-sample over the next period.

That makes the later comparison much more meaningful. Differences in performance come from the objective and constraints, not from giving one model a better data window.

5) CVaR as a Tail-Risk Objective

Variance is easy to optimize, but it treats upside and downside symmetrically. A large positive return increases variance, and a large negative return also increases variance. For portfolio construction, investors usually don’t dislike both equally. The painful part is the left tail, especially months or days where many assets fall together.

To model that directly, we define portfolio return in scenario \(s\) as:

\[

r_{p,s} = r_s^\top w

\]

where \(r_s \in \mathbb{R}^N\) is the vector of asset returns in historical scenario \(s\), and \(w\) is the portfolio weight vector. Portfolio loss is the negative return:

\[

\ell_s(w) = -r_s^\top w

\]

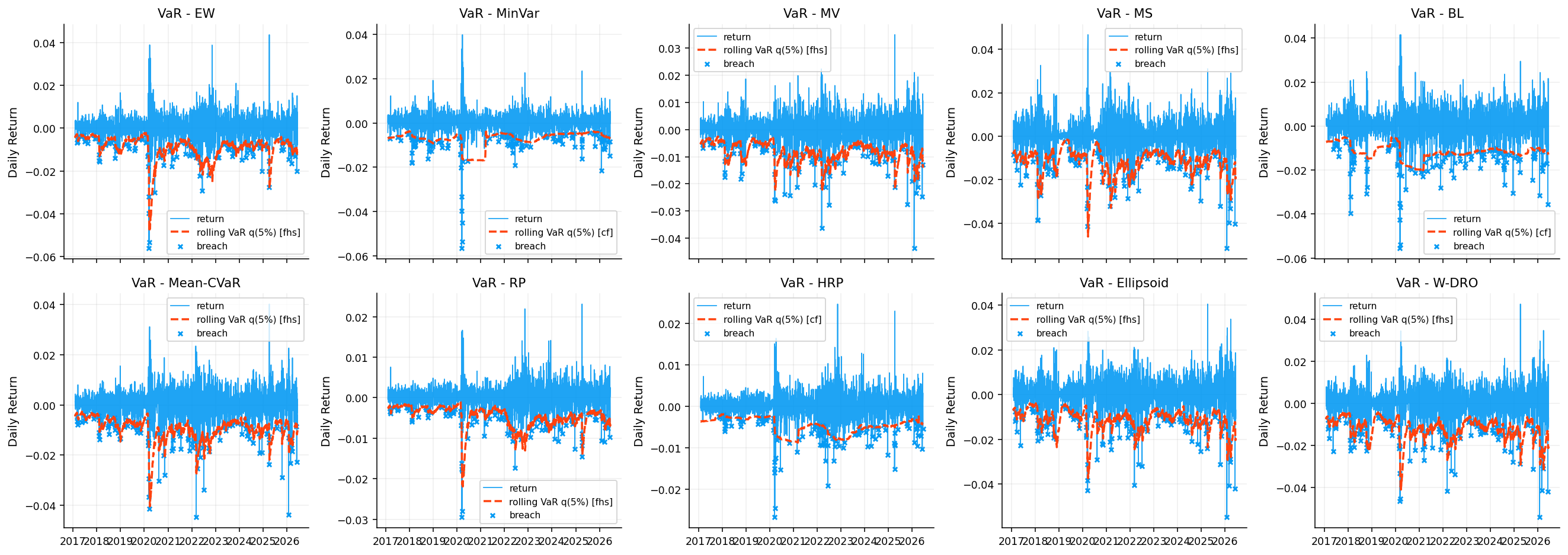

Large positive \(\ell_s(w)\) means a bad portfolio outcome. At confidence level \(\alpha\), Value-at-Risk is the loss threshold:

It asks: once we are already in the bad 5% of outcomes, what is the average loss? That is why CVaR is usually a better portfolio risk objective than VaR. VaR only finds the cliff edge. CVaR looks over the edge and measures how bad the fall is.

5.1 Rockafellar-Uryasev CVaR Linear Program

The useful optimization trick is that empirical CVaR can be written as a convex problem. We introduce one scalar \(\eta\) and one slack variable \(u_s\) per historical scenario.

The variable \(\eta\) acts like the estimated VaR level. The slack \(u_s\) measures how far scenario \(s\) exceeds that VaR threshold. The empirical CVaR objective is:

The second constraint says \(u_s\) is active only when the loss is above \(\eta\). If the scenario loss is smaller than \(\eta\), then \(\ell_s(w)-\eta\) is negative and \(u_s\) can stay at zero. If the loss is larger than \(\eta\), then \(u_s\) has to cover the excess loss above the threshold.

So the optimizer is doing two things at once:

It chooses \(\eta\), the tail cutoff.

It chooses \(w\), the portfolio that makes the average excess loss beyond \(\eta\) as small as possible.

For a pure minimum-CVaR portfolio, the optimization problem is:

with the full-investment, long-only, cap, and CVaR slack constraints. This is one of the cleanest examples of why CVaR is practical: a tail-risk quantity that sounds complicated becomes a convex linear program over historical scenarios.

The slack-variable construction is also useful because it gives a very intuitive picture of what the optimizer is doing. Suppose we have five simplified loss scenarios:

If the tail threshold \(\eta\) is set near 1.0%, then only the 3.0% scenario creates a large positive slack. The small losses below \(\eta\) don’t matter much for the CVaR term. If the optimizer changes the weights and lowers the 3.0% scenario to 2.0%, the CVaR objective improves even if several normal scenarios barely change.

That is why CVaR optimization can produce portfolios that look different from variance-minimizing portfolios. Variance cares about all deviations, including the middle of the distribution. CVaR spends most of its attention on the tail set:

The tail set itself depends on \(w\). When we change the portfolio, the worst scenarios can change. A portfolio with more commodities may have a different bad-scenario set than a portfolio with more duration. So the CVaR optimizer is not only reducing the size of losses in a fixed tail. It is also changing which historical days become the relevant tail days.

This is one reason CVaR is powerful but sample-sensitive. If the rolling window doesn’t contain the type of crisis that is coming next, the optimized tail may be the wrong tail.

The minimum-CVaR model solves this tail-risk minimization problem at each rebalance. It doesn’t ask which assets have the highest expected return. It only asks which long-only capped allocation minimizes the average loss in the worst 5% of the rolling historical scenarios.

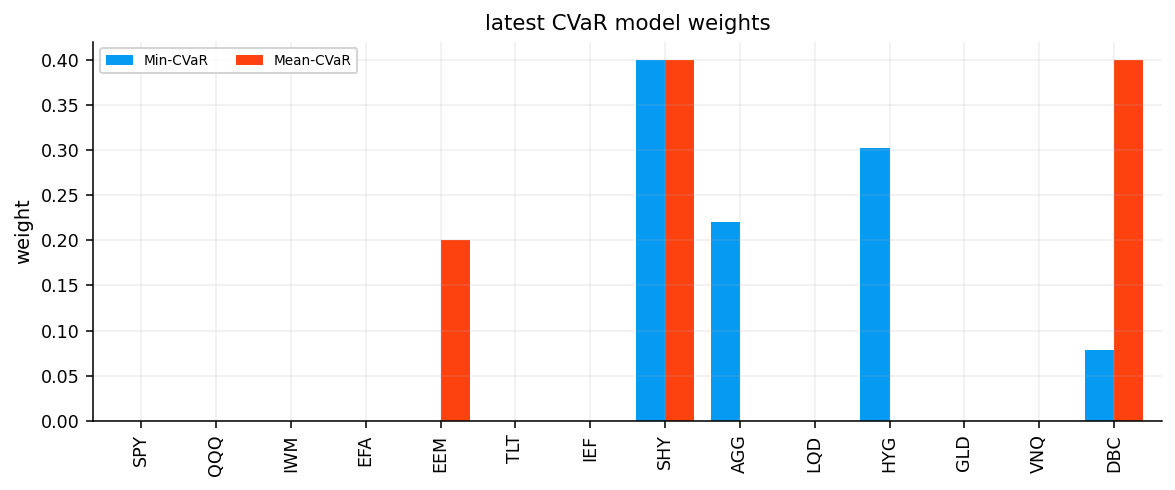

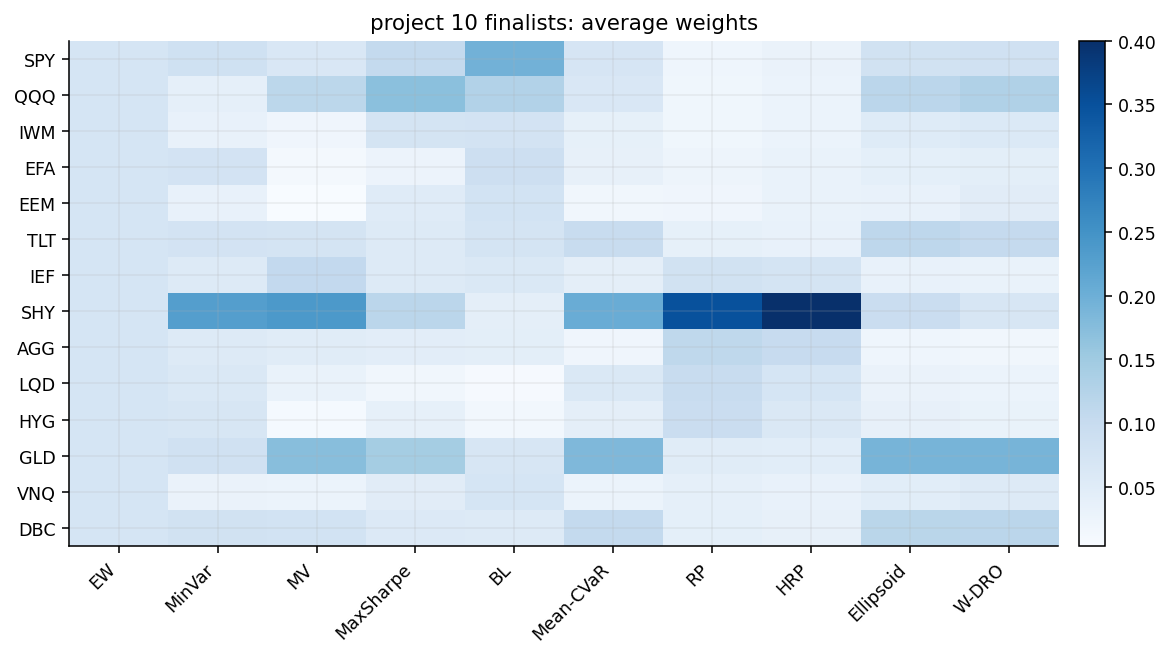

That objective creates a very defensive latest allocation:

SHY receives the max 40%.

HYG receives about 30.17%.

AGG receives about 21.99%.

DBC receives about 7.84%.

Most equity and long-duration assets receive zero.

At first, HYG may look surprising because high-yield credit is risky. But the model isn’t reading labels. It reads the empirical tail scenarios inside the rolling training window. If HYG’s recent worst-tail behavior is less damaging than equity or long-duration bonds under that particular window, the optimizer can still include it. This is one reason CVaR models need careful interpretation: they are only as good as the tail scenarios in the estimation window.

The latest training tail numbers are tiny, with a 95% VaR loss around 0.31% and CVaR loss around 0.44%. That is the in-window optimized tail loss, not a promise about future drawdown.

Show code

cvar_alpha =0.95min_cvar_rows = []def min_cvar_weight(dt, state, prev_w): tickers =list(state["tickers"]) caps = cap_array(tickers).to_numpy(dtype=float) r_train = state["R_cov"].reindex(columns=tickers).astype(float).dropna(how="any") r = r_train.to_numpy(dtype=float) t, n = r.shape w = cp.Variable(n) eta = cp.Variable() u = cp.Variable(t) losses =-r @ w cvar = eta + cp.sum(u) / ((1.0- cvar_alpha) * t) problem = cp.Problem(cp.Minimize(cvar), [cp.sum(w) ==1.0, w >=0.0, w <= caps, u >=0.0, u >= losses - eta]) status = solve_cvx_problem(problem)if w.value isNoneor status notin ["optimal", "optimal_inaccurate"]:returnNone out = clean_weight_array(w.value, tickers) loss_values =-r @ out.reindex(tickers).values var =float(np.quantile(loss_values, cvar_alpha)) tail = loss_values[loss_values >= var] min_cvar_rows.append({"date": dt, "var_95_loss": var, "cvar_95_loss": float(tail.mean()) iflen(tail) else var, "status": status})return outmin_cvar_weights = make_weight_frame_from_func("Min-CVaR 95", min_cvar_weight)min_cvar_result = backtest_weight_frame("Min-CVaR 95", min_cvar_weights)results["Min-CVaR 95"] = min_cvar_resultmin_cvar_diag = pd.DataFrame(min_cvar_rows).set_index("date")display(min_cvar_weights.iloc[-1].sort_values(ascending=False).to_frame("Min-CVaR 95").round(4))display(compact_result_table({"Min-CVaR 95": min_cvar_result}).round(4))display(min_cvar_diag.tail(1).round(6))

Min-CVaR 95

SHY

0.4000

HYG

0.3017

AGG

0.2199

DBC

0.0784

IEF

0.0000

GLD

0.0000

LQD

0.0000

QQQ

0.0000

SPY

0.0000

EFA

0.0000

EEM

0.0000

TLT

0.0000

VNQ

0.0000

IWM

0.0000

cagr

ann_vol

sharpe

sortino

max_drawdown

calmar

avg_turnover

total_turnover

cost_drag

avg_effective_n

avg_max_weight

Strategy

Min-CVaR 95

0.024

0.036

-0.4073

-0.4977

-0.125

0.1918

0.0248

3.099

0.0027

2.9749

0.4

var_95_loss

cvar_95_loss

status

date

2026-05-29

0.003132

0.004446

optimal

The backtest shows the limitation of pure Min-CVaR very clearly. It has the smallest annualized volatility among all models at 3.60%, the lowest historical ES at 0.54%, and the lowest worst month at -3.31%. That means the objective does what it was designed to do: it produces a portfolio with very small realized tail losses.

The Sharpe is negative because the project assumes a 4% annual risk-free rate. A portfolio that earns only 2.40% annualized has failed the basic opportunity-cost test. In other words, pure tail minimization can become too defensive. It reduces loss severity, but it may reduce the expected return so much that the portfolio is no longer economically attractive.

This is the first major lesson from the project: tail control alone isn’t enough. A usable model needs to control tail risk while still earning a return premium. That motivates the Mean-CVaR model next.

The Min-CVaR result also teaches an important economic lesson about the difference between risk minimization and portfolio usefulness. In mathematical terms, the model solved exactly the problem we gave it:

\[

\min_w CVaR_{0.95}(w)

\]

But the objective doesn’t contain a reward term. If an asset helps reduce the worst 5% losses but has poor expected return, the optimizer can still love it. If another asset has strong expected return but occasionally appears in the tail set, the optimizer can reject it completely.

This is why pure risk minimization often creates portfolios that look safe in a risk table but weak in a wealth curve. The optimizer isn’t failing. The objective is incomplete for an investor who needs positive real returns. A risk-minimizing sleeve can be useful inside a larger allocation, but as a standalone strategy it can become too close to cash or short-duration bonds.

The result also shows why comparing only max drawdown or ES can be misleading. Min-CVaR has excellent tail metrics, but if it earns less than the assumed risk-free rate, its Sharpe becomes negative. That is not a technical detail. It means the strategy has failed after accounting for opportunity cost.

6) Mean-CVaR: Return Maximization Under a Tail Budget

The pure Min-CVaR objective minimizes the left tail but ignores return. Mean-CVaR changes the problem. Instead of minimizing CVaR directly, we maximize expected return subject to a CVaR limit.

The expected return estimate is:

\[

\hat{\mu}^\top w

\]

where \(\hat{\mu}\) is the annualized expected-return vector selected from the walk-forward grid. The CVaR constraint is:

\[

CVaR_{0.95}(w) \le B

\]

where \(B\) is a tail-risk budget. In this project, the budget is based on the equal-weight portfolio’s in-sample CVaR:

\[

B = c \cdot CVaR_{0.95}(w_{\text{EW}})

\]

where \(c\) is a budget scale. A value below 1.0 means the portfolio must have lower in-sample CVaR than equal weight. A value above 1.0 allows more tail risk than equal weight.

The optimization becomes:

\[

\max_{w,\eta,u}\; \hat{\mu}^\top w

\]

subject to:

\[

\eta + \frac{1}{(1-\alpha)T}\sum_{s=1}^{T}u_s \le B

\]

This is a much more useful portfolio construction problem. The model can take risk, but only if the worst-scenario average loss remains inside the allowed budget.

Mean-CVaR can be read as a risk-budget spending problem. The model receives a budget \(B\) and tries to buy as much expected return as possible without spending more than that amount of tail risk.

The Lagrangian intuition is useful. If we attach a multiplier \(\gamma \ge 0\) to the CVaR constraint, the problem behaves like:

\[

\max_w\; \hat{\mu}^\top w - \gamma \, CVaR_\alpha(w)

\]

The constrained form and penalized form are closely related. In the constrained form, we choose the tail budget directly. In the penalized form, we choose how expensive tail risk is. We use the constrained form because the budget is easier to interpret: it is a fraction of the equal-weight portfolio’s in-sample CVaR.

This makes the result more transparent. A 0.90 budget scale means:

So the model must produce a portfolio whose in-sample tail loss is at least 10% lower than equal weight. That is much clearer than saying “we use a tail penalty of \(\gamma\)” because \(\gamma\) is harder to understand economically.

When the optimized CVaR sits almost exactly at the budget, it means the tail constraint is binding. The model would like to take more expected-return exposure, but the CVaR limit prevents it.

Show code

mean_cvar_rows = []def training_cvar_loss(r, wv): loss_values =-r @ wv var =float(np.quantile(loss_values, cvar_alpha)) tail = loss_values[loss_values >= var]returnfloat(tail.mean()) iflen(tail) else vardef mean_cvar_weight(dt, state, prev_w): tickers =list(state["tickers"]) caps = cap_array(tickers).to_numpy(dtype=float) r_train = state["R_cov"].reindex(columns=tickers).astype(float).dropna(how="any") r = r_train.to_numpy(dtype=float) mu_ann = state["mu_ann_map"][best_maxsharpe_cov][best_maxsharpe_mu].reindex(tickers).fillna(0.0).astype(float) ew = np.repeat(1.0/len(tickers), len(tickers)) ew_cvar = training_cvar_loss(r, ew) t, n = r.shapefor scale in [0.90, 1.00, 1.10]: budget = scale * ew_cvar w = cp.Variable(n) eta = cp.Variable() u = cp.Variable(t) losses =-r @ w cvar = eta + cp.sum(u) / ((1.0- cvar_alpha) * t) problem = cp.Problem(cp.Maximize(mu_ann.values @ w), [cp.sum(w) ==1.0, w >=0.0, w <= caps, u >=0.0, u >= losses - eta, cvar <= budget]) status = solve_cvx_problem(problem)if w.value isnotNoneand status in ["optimal", "optimal_inaccurate"]: out = clean_weight_array(w.value, tickers) cvar_value = training_cvar_loss(r, out.reindex(tickers).values) mean_cvar_rows.append({"date": dt, "ew_cvar_95_loss": ew_cvar, "budget_scale": scale, "cvar_budget": budget, "cvar_95_loss": cvar_value, "mu_ann": float(mu_ann.values @ out.reindex(tickers).values), "status": status})return outreturnNonemean_cvar_weights = make_weight_frame_from_func("Mean-CVaR 95", mean_cvar_weight)mean_cvar_result = backtest_weight_frame("Mean-CVaR 95", mean_cvar_weights)results["Mean-CVaR 95"] = mean_cvar_resultmean_cvar_diag = pd.DataFrame(mean_cvar_rows).set_index("date")cvar_table = compact_result_table({"Min-CVaR 95": min_cvar_result, "Mean-CVaR 95": mean_cvar_result})cvar_latest_weights = pd.concat({"Min-CVaR": min_cvar_weights.iloc[-1], "Mean-CVaR": mean_cvar_weights.iloc[-1]}, axis=1)display(cvar_table.round(4))display(mean_cvar_diag[["ew_cvar_95_loss", "budget_scale", "cvar_budget", "cvar_95_loss", "mu_ann"]].tail(5).round(6))ax = cvar_latest_weights.plot(kind="bar", figsize=(8.5, 3.6), width=0.78)ax.set_title("latest CVaR model weights")ax.set_ylabel("weight")ax.legend(fontsize=7, ncol=2, frameon=True, framealpha=0.85)plt.tight_layout()plt.show()

cagr

ann_vol

sharpe

sortino

max_drawdown

calmar

avg_turnover

total_turnover

cost_drag

avg_effective_n

avg_max_weight

Strategy

Min-CVaR 95

0.0240

0.0360

-0.4073

-0.4977

-0.1250

0.1918

0.0248

3.0990

0.0027

2.9749

0.4000

Mean-CVaR 95

0.0921

0.0955

0.5609

0.7014

-0.1461

0.6305

0.3077

38.4629

0.0223

3.3662

0.3887

ew_cvar_95_loss

budget_scale

cvar_budget

cvar_95_loss

mu_ann

date

2026-01-30

0.011656

0.9

0.010490

0.010469

-0.001971

2026-02-27

0.011499

0.9

0.010349

0.010325

-0.002675

2026-03-31

0.011943

0.9

0.010749

0.010723

-0.002571

2026-04-30

0.011943

0.9

0.010749

0.010728

0.023956

2026-05-29

0.012068

0.9

0.010861

0.010839

0.001603

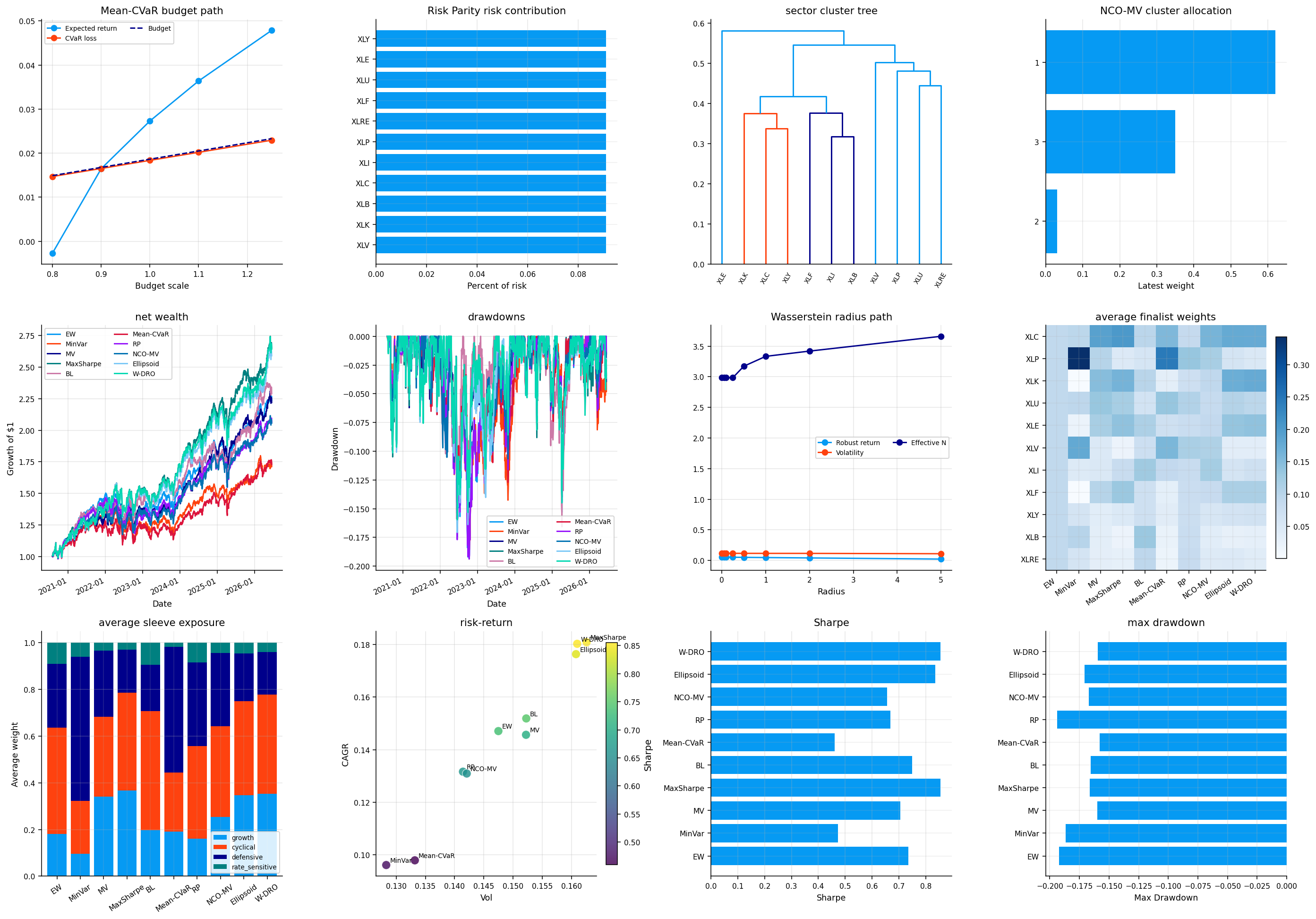

The Mean-CVaR model tests budget scales of 0.90, 1.00, and 1.10 and keeps the first feasible solution in the implementation flow. The displayed recent rows show the 0.90 budget being used in the last months. For example, on 2026-05-29, equal-weight CVaR is about 0.01207, the budget is 0.01086, and the optimized portfolio’s CVaR is 0.01084. The model is using almost the full tail budget, which is what we expect from a constrained optimizer. If expected return is being maximized, there is usually no reason to leave a valuable risk budget unused.

The performance comparison between Min-CVaR and Mean-CVaR is the important part:

\[

\text{Min-CVaR Sharpe}=-0.4073

\]

\[

\text{Mean-CVaR Sharpe}=0.5609

\]

Mean-CVaR sacrifices some tail purity, but it becomes a real investment strategy. It earns 9.21% CAGR with 9.55% volatility, historical ES of 1.45%, and max drawdown of -14.61%. This is one of the strongest examples in the project of why risk control needs to be tied to a return objective. A portfolio that only avoids losses can become cash-like. A portfolio that spends a controlled tail budget can still participate in risk premia.

Show code

def latest_mean_cvar_budget(scale): dt = model_rebalance_dates[-1] state = walkforward_grid.cache[dt] tickers =list(state["tickers"]) caps = cap_array(tickers).to_numpy(dtype=float) r = state["R_cov"].reindex(columns=tickers).astype(float).dropna(how="any").to_numpy(dtype=float) mu_ann = state["mu_ann_map"][best_maxsharpe_cov][best_maxsharpe_mu].reindex(tickers).fillna(0.0).astype(float) ew_cvar = training_cvar_loss(r, np.repeat(1.0/len(tickers), len(tickers))) t, n = r.shape w = cp.Variable(n) eta = cp.Variable() u = cp.Variable(t) losses =-r @ w cvar = eta + cp.sum(u) / ((1.0- cvar_alpha) * t) budget =float(scale) * ew_cvar problem = cp.Problem(cp.Maximize(mu_ann.values @ w), [cp.sum(w) ==1.0, w >=0.0, w <= caps, u >=0.0, u >= losses - eta, cvar <= budget]) status = solve_cvx_problem(problem)if w.value isNoneor status notin ["optimal", "optimal_inaccurate"]:return {"budget_scale": scale, "cvar_budget": budget, "status": status} out = clean_weight_array(w.value, tickers)return {"budget_scale": scale, "cvar_budget": budget, "expected_ann_return": float(mu_ann.values @ out.reindex(tickers).values), "cvar_95_loss": training_cvar_loss(r, out.reindex(tickers).values), "effective_n": float(1.0/ np.square(out.values).sum()), "max_weight": float(out.max()), "status": status}latest_cvar_path = pd.DataFrame([latest_mean_cvar_budget(x) for x in [0.80, 0.90, 1.00, 1.10, 1.25]])display(latest_cvar_path.round(6))

budget_scale

cvar_budget

expected_ann_return

cvar_95_loss

effective_n

max_weight

status

0

0.80

0.009655

0.000591

0.009634

3.086826

0.4

optimal

1

0.90

0.010861

0.001603

0.010839

2.780100

0.4

optimal

2

1.00

0.012068

0.002401

0.012045

3.008913

0.4

optimal

3

1.10

0.013275

0.003098

0.013250

3.068390

0.4

optimal

4

1.25

0.015085

0.004068

0.015056

2.870796

0.4

optimal

The CVaR budget-path table makes the tradeoff visible. At the latest rebalance, as the budget scale rises from 0.80 to 1.25, the allowed CVaR budget moves from about 0.00966 to 0.01509. The optimized expected annual return rises from about 0.00059 to 0.00407.

The relationship is monotonic in the expected direction:

More tail budget allows more return-seeking allocations.

The realized training CVaR stays just below the budget.

The max-weight constraint remains binding at 40% across the path.

Effective \(N\) stays low, around 2.8 to 3.1, meaning the optimal tail-return tradeoff is still concentrated.

This is a useful diagnostic. If expected return didn’t rise when the CVaR budget loosened, then the expected-return estimate wouldn’t be giving the optimizer a meaningful direction. Here it does rise, but slowly. The model is saying that within the latest rolling window, buying more expected return requires accepting more left-tail exposure, and the portfolio quickly hits concentration constraints.

For example, if the allowed CVaR budget is very tight, the model has to hold more defensive assets even when their expected return is low. When the budget loosens, it can add assets like GLD, DBC, or equity/credit exposures if their expected-return estimate justifies the extra tail risk.

The budget path is also a small local efficient frontier. Each row answers:

\[

\text{Given this tail budget, what is the highest estimated return we can hold?}

\]

This is different from the classical mean-variance frontier, where the risk constraint is usually volatility:

\[

w^\top\Sigma w \le \sigma_\star^2

\]

Here the risk constraint is tail loss:

\[

CVaR_{0.95}(w) \le B_\star

\]

The difference matters because the two constraints can prefer different assets. A portfolio can have moderate volatility but ugly crash behavior if its losses are skewed or if it loads on assets that gap down together. A CVaR constraint directly limits the average loss inside the historical bad tail.

The latest budget table shows max weight stays at 0.40 across all budget scales. That tells us the cap constraint is binding together with the tail constraint. The optimizer wants to allocate more to the assets that best satisfy return-per-tail-risk, but the max-weight rule prevents unlimited concentration. This is exactly why constraints are part of the model, not just implementation details. In constrained portfolio optimization, the final weights come from the objective and the constraint geometry.

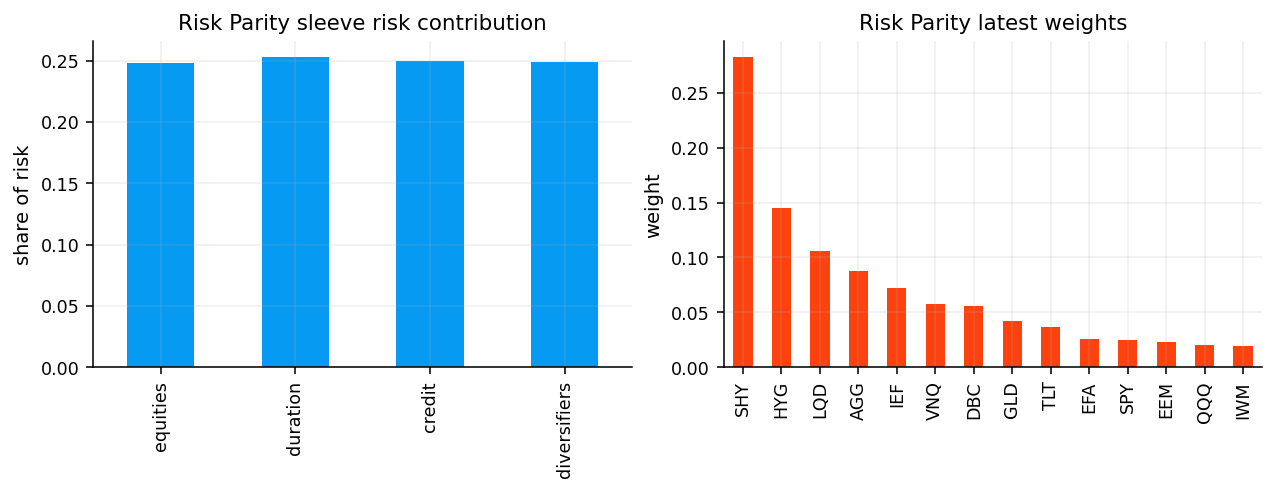

7) Risk Parity and Risk Contributions

Risk parity takes a different view of diversification. Equal weight gives each asset the same capital weight. Risk parity tries to give each asset, or each sleeve, the same contribution to portfolio risk.

For a portfolio with weights \(w\) and covariance matrix \(\Sigma\), portfolio variance is:

\[

\sigma_p^2 = w^\top \Sigma w

\]

Portfolio volatility is:

\[

\sigma_p = \sqrt{w^\top \Sigma w}

\]

The marginal contribution of asset \(i\) to portfolio volatility is the partial derivative:

This derivative tells us how much portfolio volatility would change if we slightly increased asset \(i\)’s weight. The total risk contribution of asset \(i\) is weight times marginal contribution:

\[

RC_i = w_i \frac{(\Sigma w)_i}{\sigma_p}

\]

If we divide by total portfolio volatility, we get the percentage contribution:

The percentage contributions sum to 1. Risk parity tries to make these contributions equal, or equal across predefined groups:

\[

PRC_i \approx b_i

\]

where \(b_i\) is the target risk budget. For equal risk contribution across assets, \(b_i=1/N\). For sleeve parity, the target can be equal across sleeves, as this project checks in the diagnostics.

The risk-contribution formula also shows why correlation matters. Expanding the numerator for asset \(i\):

\[

(\Sigma w)_i = \sum_{j=1}^{N}\Sigma_{ij}w_j

\]

So asset \(i\)’s contribution is not based only on its own volatility. It depends on how it covaries with everything else in the portfolio. If an asset has high standalone volatility but negative or low correlation with the rest of the portfolio, its risk contribution can be lower than its standalone volatility suggests. If a low-volatility asset is highly correlated with the largest portfolio positions, its contribution can be larger than expected.

This is why risk parity is a portfolio-level concept. We don’t equalize individual volatilities. We equalize each asset’s contribution to the portfolio’s total volatility. The covariance terms decide how much each asset adds to the combined risk.

A two-asset example makes this clear. With weights \(w_1,w_2\), volatilities \(\sigma_1,\sigma_2\), and correlation \(\rho\), portfolio variance is:

When \(\rho\) is high, diversification is weak and the higher-volatility asset usually needs much lower capital weight. When \(\rho\) is low or negative, the same asset can receive more weight because it doesn’t add as much total portfolio risk.

7.1 Why Risk Parity Often Holds More Bonds

Risk parity is easy to misunderstand if we only look at weights. Low-volatility assets often receive large capital weights because they need more dollars to contribute the same risk.

Suppose Asset A has 20% volatility and Asset B has 5% volatility. If they are weakly correlated, a 10% weight in A can contribute similar volatility risk to a 40% weight in B. So a risk parity portfolio may look “bond heavy” or “SHY heavy”, but that doesn’t mean it is trying to maximize bond exposure. It is trying to equalize the volatility contribution.

The model solves this kind of target indirectly by minimizing the gap between actual risk contributions and target risk contributions. In simplified form:

subject to the usual portfolio constraints. The exact numerical implementation can be different, but the target is the same: distribute risk contribution rather than distribute capital equally.

In this project, we also inspect sleeve-level risk contribution. The sleeve contribution for group \(g\) is the sum of asset contributions inside that group:

\[

PRC_g = \sum_{i \in g} PRC_i

\]

This is useful because a portfolio can have equal asset-level contributions but still load too much on one economic sleeve if several correlated assets belong to the same sleeve.

This is exactly the target behavior. The capital weights are not equal, but the sleeve risk contributions are nearly equal. That means the optimizer is succeeding at the risk-budgeting problem.

The performance is defensive. Risk Parity has 4.53% CAGR, 4.92% annualized volatility, 0.132 Sharpe, -13.74% max drawdown, and historical ES of 0.73%. Its main strength is risk control, not return. This model becomes a tail-control benchmark: if another model has much higher return but also much higher ES, we can see the cost of buying that return.

8) Hierarchical Risk Parity

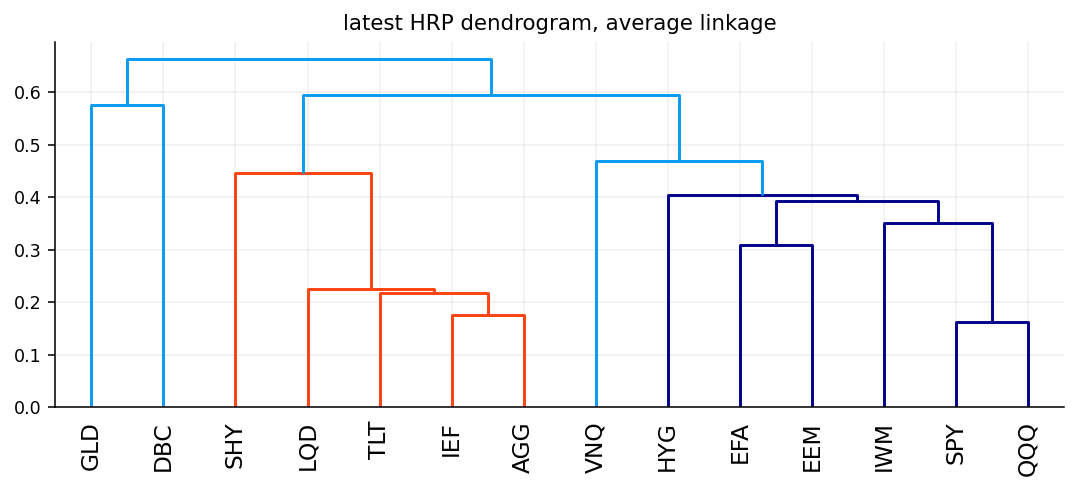

HRP, or Hierarchical Risk Parity, starts from a different idea: assets shouldn’t be allocated as if all correlations are equally important. The first step is to understand which assets naturally cluster together.

The model converts correlation into a distance:

\[

d_{ij} = \sqrt{\frac{1-\rho_{ij}}{2}}

\]

where \(\rho_{ij}\) is the correlation between assets \(i\) and \(j\). This distance has useful properties:

If two assets are perfectly correlated, \(\rho_{ij}=1\), then \(d_{ij}=0\).

If two assets are uncorrelated, \(\rho_{ij}=0\), then \(d_{ij}=\sqrt{1/2}\).

If two assets are perfectly negatively correlated, \(\rho_{ij}=-1\), then \(d_{ij}=1\).

The clustering algorithm uses these distances to build a tree. Assets that move together are placed near each other. Once the tree is built, HRP orders the covariance matrix according to the tree structure and recursively splits the ordered list into clusters. At each split, it allocates more weight to the lower-risk cluster.

For a cluster \(C\), the cluster variance is estimated using an inverse-variance portfolio inside the cluster:

If a parent cluster is split into left and right subclusters with variances \(\sigma_L^2\) and \(\sigma_R^2\), the lower-variance side receives more capital. The recursive process continues until weights are assigned to individual assets.

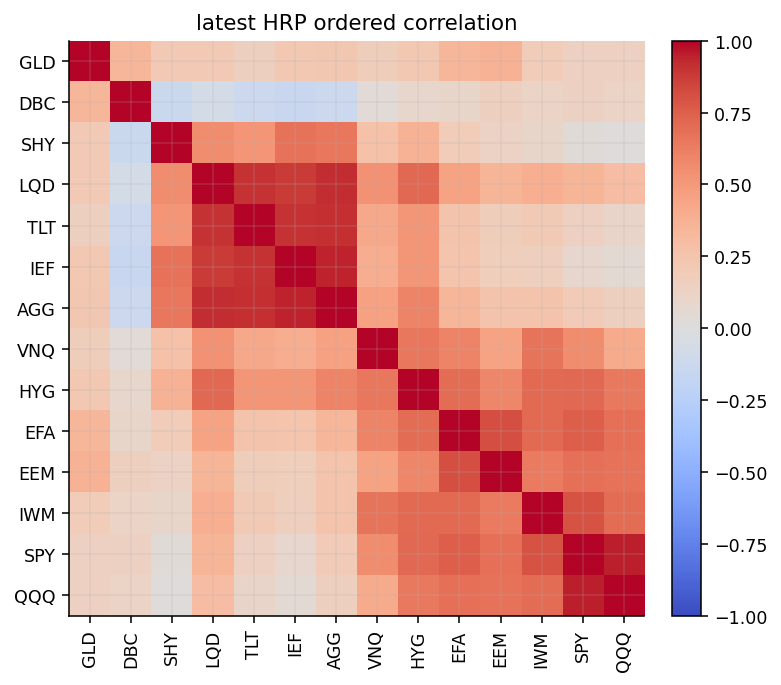

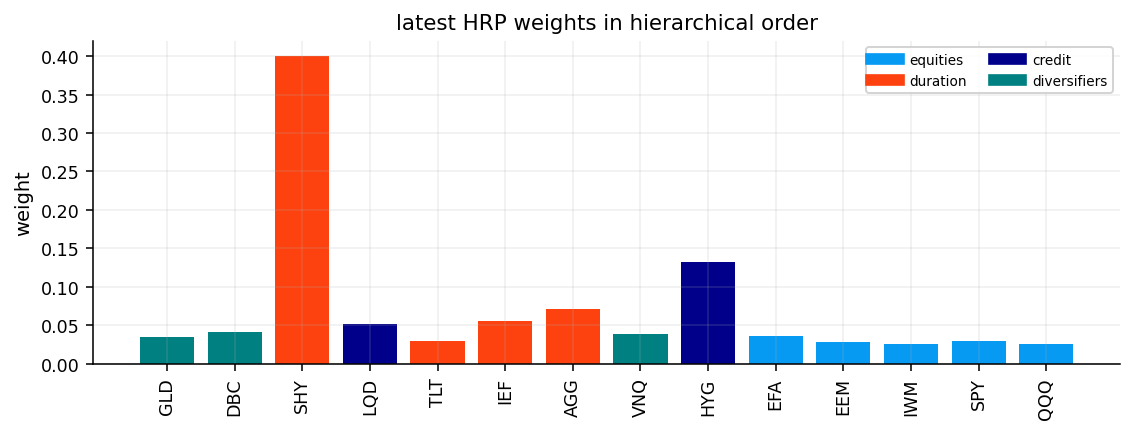

The latest HRP dendrogram and ordered-correlation heatmap show the cross-asset structure clearly. Duration and bond-like assets cluster together, equity and credit-like assets cluster together, and diversifiers form their own partial grouping. This is economically sensible because the model isn’t told those labels directly. It sees them through correlation.

The latest HRP weights are extremely defensive:

SHY receives the cap at 40%.

HYG receives 13.17%.

AGG receives 7.11%.

IEF and LQD receive around 5%.

Equity ETFs receive small weights.

The cap on SHY matters here. HRP sees SHY as a low-risk cluster anchor, and without a cap it would likely receive even more. This is one of the practical issues with HRP in a cross-asset ETF universe: if the universe contains near-cash instruments, hierarchical allocation can become too defensive unless the constraints prevent it.

The HRP backtest has 5.19% CAGR, 5.04% volatility, 0.2547 Sharpe, -14.46% max drawdown, and ES of 0.75%. It improves tail behavior compared with aggressive models, but it doesn’t earn enough return to compete with BL, MaxSharpe, Mean-CVaR, or robust MV.

The HRP allocation process can be understood as a sequence of local decisions. At each branch of the tree, we ask how risky the left cluster is relative to the right cluster. If the left cluster has variance \(\sigma_L^2\) and the right cluster has variance \(\sigma_R^2\), the allocation to the left side is proportional to the inverse of its cluster variance:

So if the left cluster is much safer than the right cluster, \(\sigma_L^2\) is small and \(\alpha_L\) is large. The safer cluster receives more capital. This is repeated down the tree until every asset has a final weight.

This recursive structure is why HRP can be stable. It doesn’t invert the full covariance matrix in the same way a mean-variance optimizer does. Instead, it uses the hierarchy to break the problem into smaller allocation decisions. The cost is that HRP doesn’t directly optimize expected return, and in a universe with very low-volatility assets it can become heavily defensive.

9) Nested Clustered Optimization

NCO, or Nested Clustered Optimization, uses clustering like HRP but doesn’t stop at recursive bisection. It treats each cluster as a sub-portfolio and then optimizes across those cluster portfolios.

The workflow is:

Use the correlation distance matrix to cluster the assets.

Solve an inner optimization inside each cluster.

Treat each cluster portfolio as one synthetic asset.

Solve an outer optimization across the cluster portfolios.

Multiply outer cluster weights by inner asset weights to get final asset weights.

If cluster \(g\) contains assets in index set \(C_g\), the inner weights are:

Then the outer optimizer chooses cluster weights \(a_g\). The final asset weight for asset \(i\) in cluster \(g\) is:

\[

w_i = a_g \cdot w_{g,i}^{\text{inner}}

\]

This structure is useful because it prevents one large correlated group from dominating the optimizer asset-by-asset. The optimizer first decides how much risk/return to allocate to clusters, then distributes inside each cluster.

NCO is more optimization-heavy than HRP, so its result depends more on the quality of the mean estimate. Inside each cluster, the inner optimizer decides which assets represent that cluster best. Then the outer optimizer decides how much capital each cluster gets.

where each column is a cluster portfolio placed in the full asset space, with zeros outside its cluster. If \(a\in\mathbb{R}^G\) is the vector of outer cluster weights, then the final asset portfolio is:

Then the outer optimizer solves a smaller portfolio problem over \(G\) cluster portfolios instead of \(N\) individual assets. This can reduce instability when \(N\) is large or when assets are strongly correlated. In this project, \(N=14\), so the dimensionality benefit is modest. The bigger question is whether the clustering creates a better economic structure. In the results, HRP’s simpler structure wins.

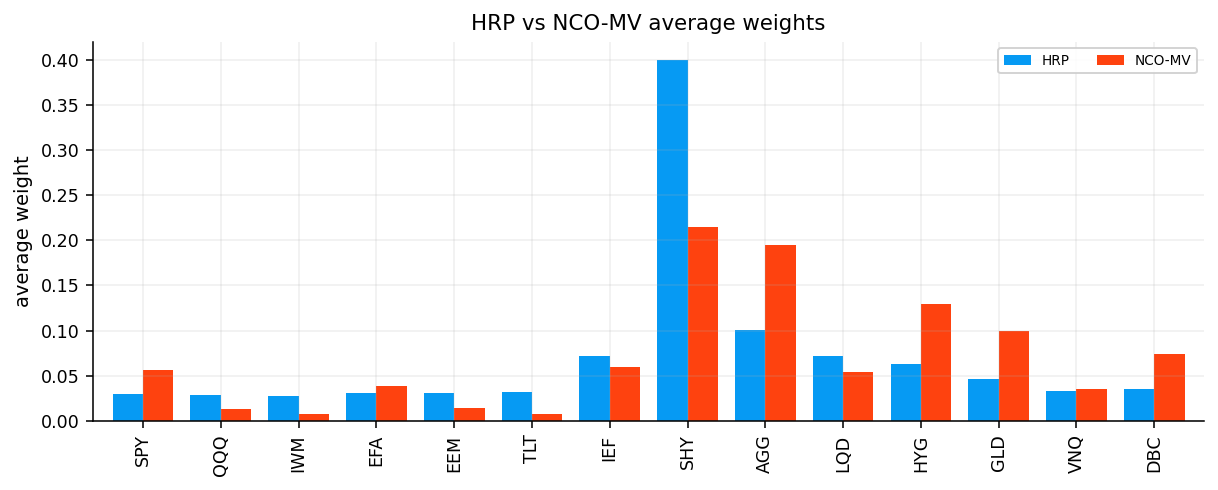

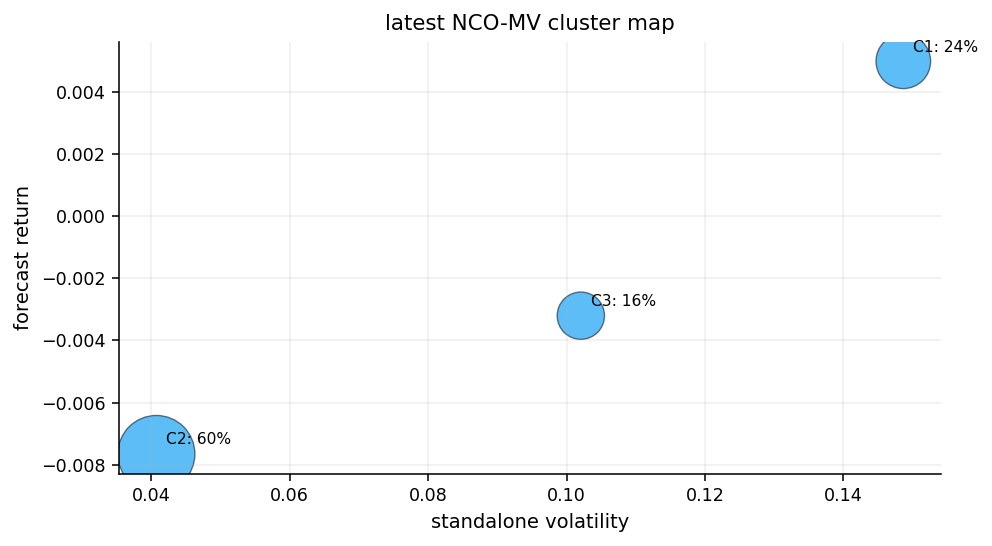

The latest NCO weights allocate 60% to the bond cluster, 24.45% to the GLD/DBC cluster, and 15.55% to the risky cluster. Within the bond cluster, SHY and AGG each hit 24% in the latest output, while TLT and LQD get zero. Within the real-asset cluster, GLD and DBC split the allocation.

The cluster map makes the same point visually. The bond cluster has the lowest standalone volatility but a negative forecast return. The diversifier cluster has a higher forecast return and higher volatility. The risky cluster has medium volatility but also a negative forecast in the latest window. The optimizer therefore places most weight in the low-vol bond cluster and keeps a meaningful diversifier sleeve.

In the backtest, NCO-MV has the same CAGR as HRP, 5.19%, but higher volatility at 6.36% and lower Sharpe at 0.2128. It also has much higher turnover, 16.45% average monthly turnover versus 1.86% for HRP. That makes HRP the better hierarchical model in this application.

The selected hierarchical model is HRP because it has higher Sharpe, better drawdown behavior, and much lower turnover than NCO-MV. This doesn’t mean NCO is theoretically weak. It means that in this cross-asset universe and sample, the extra optimization layer didn’t create enough return to justify the additional turnover and risk.

The HRP versus NCO comparison is useful because it separates two ideas:

Clustering helps us understand portfolio structure.

Optimizing inside and across clusters can add return-seeking behavior, but it can also reintroduce mean-estimation risk.

HRP mostly avoids expected-return forecasts. NCO uses them. When the expected-return signal is noisy or when the universe has a very defensive low-volatility cluster, the NCO optimizer can still become unstable. HRP is simpler and slower-moving, which is exactly why it wins the hierarchical selection here.

10) Robust Optimization: Estimation Error as a Portfolio Risk

Robust optimization is the most important conceptual block in this project. The starting point is that \(\hat{\mu}\) is an estimate, not the truth. In mean-variance optimization, small changes in \(\hat{\mu}\) can cause large changes in weights, especially when the covariance matrix has correlated assets and the optimizer is trying to rank similar opportunities.

A standard mean-variance objective is:

\[

\max_w\; \hat{\mu}^\top w - \frac{\lambda}{2}w^\top\hat{\Sigma}w

\]

where \(\lambda\) controls risk aversion. The problem is that the optimizer behaves as if \(\hat{\mu}\) is exact. Robust optimization changes the objective to say: choose a portfolio that still looks acceptable under a bad but plausible version of the expected-return vector.

where \(\mathcal{U}\) is an uncertainty set around the estimated mean vector. The inner minimization is the adversary. It asks: if the true expected return is somewhere inside this plausible set, which version hurts the chosen portfolio the most?

This turns estimation uncertainty into a direct cost. A portfolio with large exposure to uncertain return forecasts gets penalized more than a portfolio whose expected return is more reliable.

Expected-return uncertainty is usually more damaging than covariance uncertainty. A rough reason is that portfolio variance is quadratic and constrained by \(\Sigma\), while expected return enters linearly:

\[

\hat{\mu}^\top w

\]

If one asset’s expected return estimate is too high by only a few percent annualized, a mean-variance optimizer may allocate heavily to it because the linear reward looks attractive. The optimizer doesn’t know that the estimate is noisy. It just sees a higher number.

The sampling error of a mean estimate is also large. For asset \(i\), if daily returns have volatility \(\sigma_i\) and the mean is estimated from \(T\) independent observations, the standard error is approximately:

After annualization, the uncertainty can still be large relative to the expected return itself. If an asset has an annual expected return estimate of 5% but the standard error is also several percent, the sign and rank of the forecast are not very reliable.

Robust optimization makes this uncertainty explicit. Instead of pretending \(\hat{\mu}\) is the truth, it asks the optimizer to survive a pessimistic adjustment to \(\hat{\mu}\). The stronger the uncertainty set, the less the optimizer can exploit fragile forecast differences.

10.1 Box Uncertainty

The first robust model uses a box uncertainty set. Each expected return can move independently within a range:

\[

(\mu^{\text{worst}})^\top w = \sum_{i=1}^{N}(\hat{\mu}_i-\rho s_i)w_i

\]

The optimization is then:

\[

\max_w\; (\hat{\mu}-\rho s)^\top w - \frac{\lambda}{2}w^\top\Sigma w

\]

subject to the portfolio constraints.

The box model is intuitive and easy to explain: every asset’s forecast return is haircut by its own estimation uncertainty before the optimizer sees it. Assets with noisy high returns lose more of their appeal.

For a long-only portfolio, the box robust derivation is especially simple. The worst-case return is:

Since every \(w_i\ge 0\), the adversary lowers every \(\mu_i\) to its lower bound. So:

\[

\min_{\mu\in\mathcal{U}_{\text{box}}}\mu^\top w = \sum_{i=1}^{N}(\hat{\mu}_i-\rho s_i)w_i

\]

If shorting were allowed, the adversary would behave differently. For a negative weight, lowering \(\mu_i\) would help the portfolio, so the adversary would raise \(\mu_i\) instead. The general penalty would involve \(|w_i|\):

\[

\hat{\mu}^\top w - \rho\sum_{i=1}^{N}s_i|w_i|

\]

Because this project is long-only, the simpler haircut form is enough. This is also why box robustness can be interpreted as forecast haircutting. We create a conservative expected-return vector first, then run a standard constrained mean-variance optimizer on that conservative vector.

The box radius controls how skeptical we are. If \(\rho=0\), the model becomes standard MV. If \(\rho\) is large, only assets with very strong forecasts survive the haircut.

For SPY, the estimated return is slightly negative and becomes more negative after the haircut. For QQQ, a small positive raw forecast becomes slightly negative. EEM still has a strong positive robust forecast: 3.06% raw, 2.77% after the haircut. DBC remains the strongest, 5.41% raw and 5.16% robust. GLD also stays positive after the haircut.

The resulting latest portfolio is concentrated:

EEM at 40%.

DBC at 40%.

GLD at 15.25%.

IWM at 2.82%.

SHY at 1.93%.

Most assets receive zero.

This is an important detail. Robust doesn’t automatically mean diversified. If a few assets keep strong forecasts even after the uncertainty haircut, the model can still concentrate in them. The robust adjustment changes the expected-return vector; the cap constraint still determines how concentrated the solution can be.

Box Robust MV performs much better than the defensive parity models. It earns 9.92% CAGR with 11.18% volatility, 0.5520 Sharpe, -15.57% max drawdown, and ES of 1.72%. That is close to Mean-CVaR and Ellipsoid Robust MV, but with slightly weaker Sharpe.

The model’s cost is turnover. Average turnover is 34.62% per month, and total turnover reaches 43.27 over the sample. The reason is that the robust expected-return vector still changes with the momentum forecast and standard errors. When the robust forecast ranking changes, the optimizer moves capital between the few names with positive robust expected returns.

So Box Robust MV is not a low-turnover defensive model. It is a return-seeking model with conservative mean estimates. This distinction matters because the word “robust” can sound like it should automatically produce smooth weights. In this implementation, robustness is about mean-estimation uncertainty, not about minimizing trading.

10.2 Ellipsoidal Uncertainty

The second robust model uses an ellipsoid uncertainty set. Instead of allowing each expected return to move independently inside a box, it allows the whole vector to move inside a covariance-shaped region:

\(\Omega\) is the uncertainty covariance of the mean estimate.

\(\Omega^{1/2}\) is its matrix square root.

\(z\) is a standardized shock vector.

\(\rho\) controls the size of the uncertainty region.

The worst-case expected return for a portfolio has a closed form:

\[

\min_{\mu \in \mathcal{U}_{\text{ellipsoid}}} \mu^\top w = \hat{\mu}^\top w - \rho\|\Omega^{1/2}w\|_2

\]

This formula is worth slowing down. The term \(\hat{\mu}^\top w\) is the normal estimated portfolio return. The penalty term \(\rho\|\Omega^{1/2}w\|_2\) is the amount the adversary can subtract from that return. The penalty is larger when the portfolio loads on directions where the mean estimate is more uncertain.

If \(\Omega=\Sigma/T\), then uncertainty is larger for assets and combinations with higher return variance and smaller sample size. So the model is saying: we trust expected returns less when they come from volatile assets or unstable directions.

The ellipsoid penalty comes from Cauchy-Schwarz. Write the uncertain mean as:

\[

\mu = \hat{\mu}+\Omega^{1/2}z

\]

with \(\|z\|_2\le \rho\). Portfolio return under this mean is:

\[

\mu^\top w = \hat{\mu}^\top w + z^\top \Omega^{1/2}w

\]

The adversary chooses \(z\) to make the second term as negative as possible. The most negative possible value is:

This is useful because it turns a difficult “min over all plausible means” problem into a convex norm penalty. The penalty is portfolio-level, not asset-by-asset. If the portfolio loads on an uncertain combination of assets, the norm gets large. If it spreads across directions where forecast error cancels or is less severe, the norm is smaller.

This is why ellipsoid robustness is often more elegant mathematically than box robustness. It respects the covariance structure of estimation error.

The ellipsoid robust objective becomes:

\[

\max_w\; \hat{\mu}^\top w - \rho\|\Omega^{1/2}w\|_2 - \frac{\lambda}{2}w^\top\Sigma w

\]

This has a different behavior than box robustness. Box uncertainty penalizes each asset independently. Ellipsoid uncertainty penalizes the portfolio’s exposure to uncertain directions. If two assets have correlated estimation errors, the ellipsoid penalty sees that. This is one reason ellipsoid robust optimization can be more realistic for portfolios: return-estimation errors are rarely independent across related assets.

For example, if SPY and QQQ both look attractive because the same growth regime has performed well, a box model may haircut them separately. An ellipsoid model can also recognize that their forecast errors are related. Loading on both doesn’t give two independent forecasts. It creates one larger exposure to a common uncertain direction.

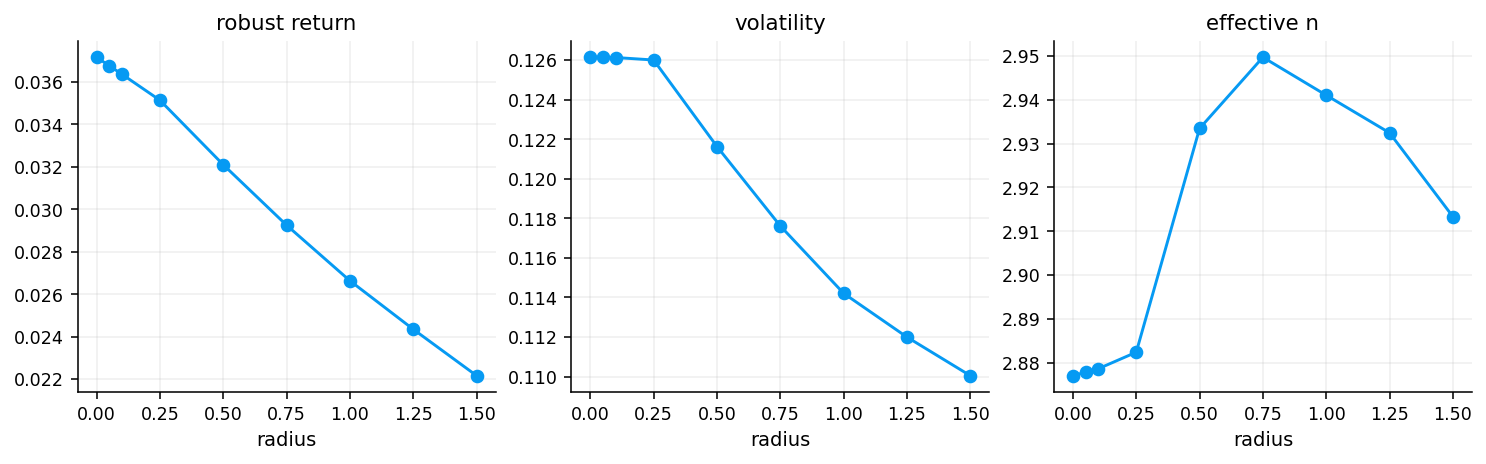

The ellipsoid radius path shows how the penalty changes as uncertainty aversion rises. With radius 0.00, there is no robust penalty, and empirical return is about 3.72% in the latest state. As the radius increases to 1.50, the robust return falls to about 2.22%. Volatility also declines modestly from about 12.61% to 11.00%, and effective \(N\) stays around 2.9.

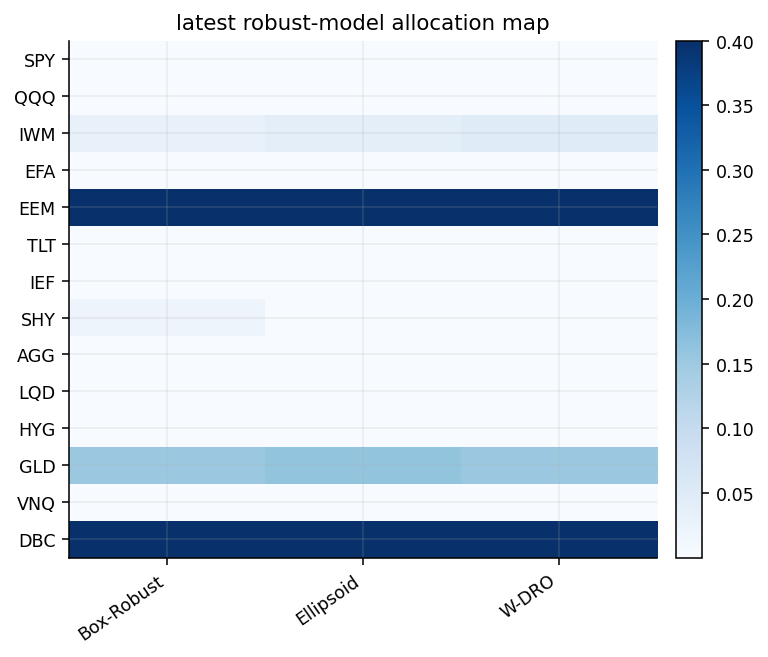

The latest allocation comparison between box and ellipsoid is very close. Both models hold:

EEM at 40%.

DBC at 40%.

GLD around 15-16%.

small IWM exposure.

little or no allocation to the rest.

The ellipsoid model drops SHY to zero and gives a slightly larger weight to IWM and GLD. The difference is not dramatic because the latest forecast environment is very directional: EEM and DBC dominate even after robust penalties. When the top forecasts are that strong, both box and ellipsoid uncertainty still point to a similar constrained solution.

In the backtest, Ellipsoid Robust MV slightly beats Box Robust MV: CAGR 10.01% versus 9.92%, Sharpe 0.5533 versus 0.5520, and turnover 34.01% versus 34.62%. The difference is small, but enough for the selection rule to choose Ellipsoid Robust MV.

The robust-model comparison confirms that the two uncertainty sets are close in this implementation. Both models have:

CAGR around 10%.

Annualized volatility around 11.2-11.3%.

Sharpe around 0.55.

Max drawdown around -15.6%.

High turnover above 34% average monthly.

Effective \(N\) around 3.1.

This tells us that most of the robust model’s behavior comes from the shared inputs: Ledoit-Wolf covariance, momentum expected returns, risk-aversion \(\lambda=2.0\), and the asset caps. The choice between box and ellipsoid affects the penalty geometry, but the latest and historical allocations still respond to the same broad signal.

The useful interpretation is that robust MV becomes a middle ground between MaxSharpe and Mean-CVaR. It is more return-seeking than tail-risk-only methods, but more cautious than a raw aggressive frontier model. Its drawdown is better than BL and MaxSharpe, but its ES is not as low as Risk Parity or HRP.

Box and ellipsoid robust optimization protect against uncertainty in the expected-return vector. Wasserstein distributionally robust optimization goes deeper. It protects against uncertainty in the entire return distribution.

We start with the empirical distribution of historical returns:

where \(\delta_{r_s}\) is a point mass at historical return vector \(r_s\). Standard empirical optimization trusts this distribution exactly. Wasserstein DRO says the true distribution may be near the empirical distribution but not equal to it.

where \(W(P,\hat{P}_T)\) is the Wasserstein distance between distributions, and \(\varepsilon\) is the radius. A larger radius means we admit more distributional uncertainty.

The model then optimizes worst-case performance over all distributions in that ball. In this implementation, the robust mean-variance form creates two penalties:

A return penalty that subtracts a term proportional to \(\|w\|_2\).

A volatility inflation that adds the same uncertainty term to empirical volatility.

The resulting objective is:

\[

\max_w\; \hat{\mu}^\top w - \sqrt{\delta}\|w\|_2 - \frac{\lambda}{2}\left(\|\Sigma^{1/2}w\|_2+\sqrt{\delta}\|w\|_2\right)^2

\]

where \(\sqrt{\delta}\) is the radius-scaled uncertainty penalty used by the implementation.

Every term in the Wasserstein objective has a clear role:

\[

\hat{\mu}^\top w

\]

is the empirical expected return estimate.

\[

\sqrt{\delta}\|w\|_2

\]

is the distributional uncertainty tax on return. It penalizes concentrated portfolios because \(\|w\|_2\) is larger when weights are concentrated. For equal weights over \(N\) assets, \(\|w\|_2=1/\sqrt{N}\). For a single-asset portfolio, \(\|w\|_2=1\).

\[

\|\Sigma^{1/2}w\|_2

\]

is empirical portfolio volatility.

\[

\|\Sigma^{1/2}w\|_2+\sqrt{\delta}\|w\|_2

\]

is robust volatility. The model behaves as if the true volatility may be larger than the sample volatility by an amount tied to distributional uncertainty and concentration.

So Wasserstein DRO attacks two common optimizer problems at once:

It doesn’t fully trust the mean estimate.

It doesn’t fully trust the empirical risk estimate.

It penalizes portfolios that depend too heavily on a few positions.

That is why this model is often more stable than an aggressive return optimizer, but still more return-seeking than pure risk parity.

The Wasserstein penalty also has an intuitive concentration effect. The norm \(\|w\|_2\) behaves like an inverse diversification measure:

For a portfolio with 40%, 40%, and 20% in three assets:

\[

\|w\|_2 = \sqrt{0.4^2+0.4^2+0.2^2}=0.60

\]

So the same Wasserstein radius creates a much larger tax for the concentrated portfolio. This is exactly what we want from a distributionally robust model. If we are unsure about the true return distribution, relying on a small number of bets is more dangerous than spreading across many exposures.

The penalty doesn’t force equal weight at the radius used here, but it changes the economics of concentration. A concentrated portfolio must have enough estimated return advantage to pay the ambiguity tax and still look attractive after robust risk inflation.

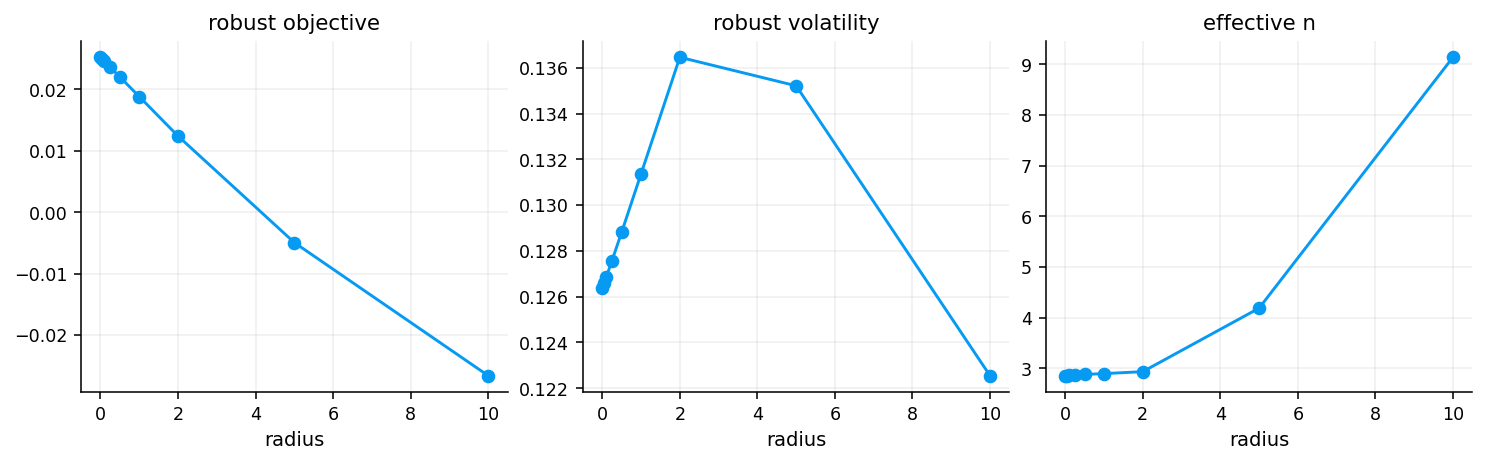

The Wasserstein radius path gives a clean sensitivity analysis. At radius 0, the model behaves close to empirical robust MV: empirical return about 3.72%, volatility around 12.64%, effective \(N\) around 2.85, max weight 40%.

As the radius rises:

The return penalty increases.

Robust return falls.

Robust volatility becomes larger than empirical volatility.

Effective \(N\) eventually rises.

The max weight finally starts falling at very large radii.

At radius 10, the model has effective \(N\) around 9.14 and max weight about 23.06%. That is a very different portfolio from the radius 0 or 1 solution. The model is being forced to diversify because distributional uncertainty is now expensive enough that concentrated weights are unattractive.

The project uses radius 1.0. At that level, the latest portfolio is still concentrated in DBC, EEM, GLD, and IWM. The model hasn’t become a defensive equal-weight portfolio. It remains return-seeking, but with an explicit distributional penalty.

The latest Wasserstein DRMV weights are:

DBC at 40%.

EEM at 40%.

GLD at 15.23%.

IWM at 4.77%.

zero in most other assets.

This resembles the box/ellipsoid robust allocation because the current return signals are strongly concentrated in the same assets. The difference is in the objective accounting. Wasserstein DRMV tracks its uncertainty tax, robust volatility, robust return, risk penalty, and objective through time.

The latest three rows show a fairly stable \(\sqrt{\delta}\) around 0.009. Empirical return changes month by month, from 3.39% to 6.63% to 3.71%, while the DRO penalty stays around 0.53-0.54%. This means the uncertainty tax is meaningful, but it doesn’t dominate the expected-return forecast at radius 1.0.

The backtest result is strong relative to other new models: 10.54% CAGR, 11.86% volatility, Sharpe 0.5743, and -17.61% max drawdown. It beats Box and Ellipsoid on return and Sharpe, but it also has a larger ES and higher drawdown than Mean-CVaR. That is the expected personality of the model: robust, but still return-seeking.

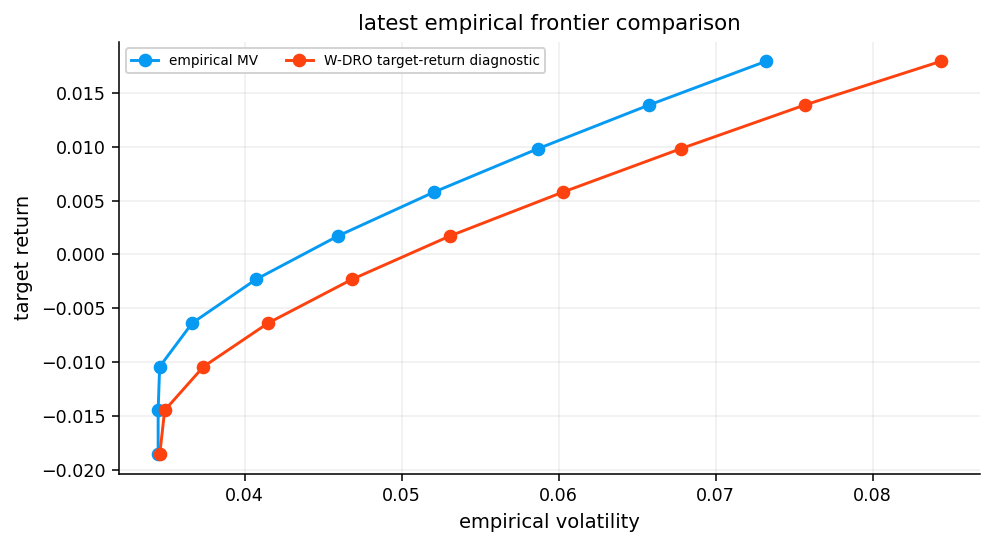

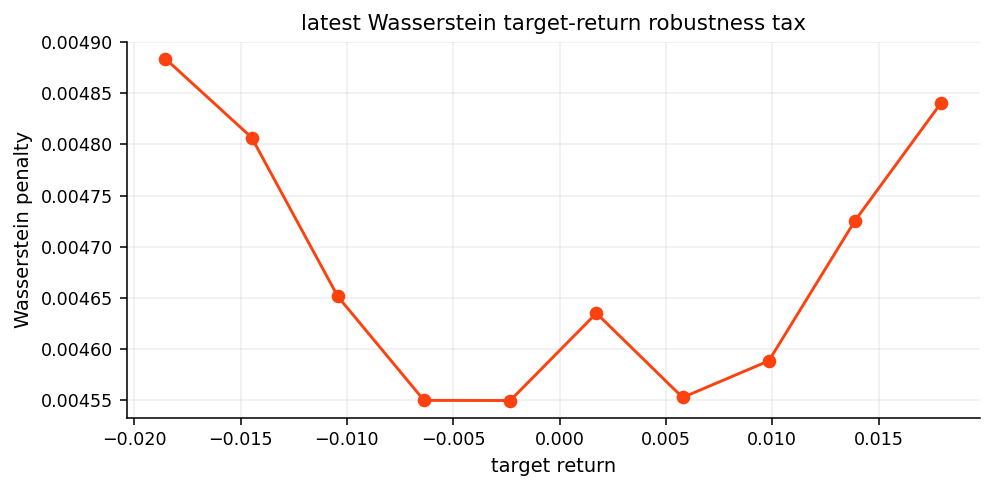

11.1 Wasserstein Target-Return Diagnostic

The target-return diagnostic asks a slightly different question. Instead of maximizing robust utility, we set a required robust return and minimize robust risk.

where \(r^\star\) is the target robust return. The left side of the return constraint is the expected return after the Wasserstein tax. The objective is robust risk, empirical volatility plus the same distributional concentration penalty.

This diagnostic produces a robust frontier. For each target return, we see how much empirical volatility and robust risk are needed. It is similar in spirit to an efficient frontier, but the risk axis includes distributional uncertainty.

The target-return table shows both empirical and Wasserstein-adjusted portfolios are feasible across the target grid. As target return increases from about -1.85% to 1.79%, empirical volatility rises from about 3.45% to 7.32%. The Wasserstein robust risk rises from about 3.95% to 8.92%.

The robust frontier lies above the empirical frontier because it adds the Wasserstein tax. That gap is useful. It shows how much risk the model attributes to distributional ambiguity rather than observed covariance alone.